Unknown chargesmean unknown risk

Understand your business exposure before it compounds.

Seeing a NFO PAYMENT charge on your statement?

Common ways NFO PAYMENT RECEIVED charges might appear on your statement

- NFO PAYMENT RECEIVED

- CHKCARD NFO PAYMENT RECEIVED

- CHECKCARD NFO PAYMENT RECEIVED

- POS DEBIT NFO PAYMENT RECEIVED

- POS PUR NFO PAYMENT RECEIVED

- POS PURCHASE NFO PAYMENT RECEIVED

- POS REFUND NFO PAYMENT RECEIVED

- PRE-AUTH NFO PAYMENT RECEIVED

- PENDING NFO PAYMENT RECEIVED

- Visa Check Card NFO PAYMENT RECEIVED MC

- Misc. Debit NFO PAYMENT RECEIVED

What is NFO PAYMENT RECEIVED?

NFO PAYMENT RECEIVED is a generic descriptor that appears on bank or credit card statements. According to a user-submitted listing on other sites, this label often shows up for online payments, sometimes for scheduled transactions or payments processed through an app. Because the descriptor is vague, it does not clearly identify the merchant or service involved.

Common causes for NFO PAYMENT RECEIVED charges

- A payment made to a credit card or loan account that posted as a “payment received,” but was processed via a third-party or app, so shows as a descriptor rather than the primary creditor.

- A scheduled online payment that debited from checking/savings and posted under the generic “NFO PAYMENT RECEIVED” label.

- A pending or pre-authorization transaction where the final merchant descriptor failed to post, leaving the generic “NFO PAYMENT RECEIVED” statement line instead.

- Potential mis-postings: either the payment processed correctly but appears under a confusing descriptor, or it may be unauthorized/fraudulent if you did not initiate anything matching that label.

Decoding NFO PAYMENT RECEIVED charge tags

- NFO is a non-specific code that many consumers cannot link it to a recognizable merchant.

- PAYMENT RECEIVED suggests the transaction is logged as a payment rather than a purchase.

- Variations like CHKCARD, CHECKCARD, POS DEBIT, PRE-AUTH, PENDING reflect the bank’s internal processing category (e.g., debit card payment, in-store POS, authorization hold).

- Because the descriptor lacks a business name, you’ll often need to cross-check your own account logs (loans, credit cards, apps) to determine what the payment was for.

What to do if you see NFO PAYMENT RECEIVED and don’t recognize it

- Review all your current accounts (credit cards, loans, subscriptions, apps) to identify any payment you recently made.

- Search your email and account notifications for confirmation of payments processed around the date the descriptor appeared.

- If you find no matching payment, contact your bank or card issuer, ask for the transaction’s merchant trace details, and consider disputing it as unauthorized.

- Monitor your account for any additional unexpected charges or payments, as this descriptor may indicate an indirect routing of a payment or even fraud.

- Consider changing login credentials for accounts you actively use for payments and enabling transaction alerts to catch future unfamiliar descriptors early.

What to do

if you

don’t recognize this charge

Spot, verify, and resolve suspicious charges in minutes.

Contact your bank.

Call your bank using the number on the back of your card.

Contact the merchant.

Call their customer service to verify the charge and get transaction details.

Dispute the charge & monitor account.

If it appears fraudulent, report it to your bank or card issuer.

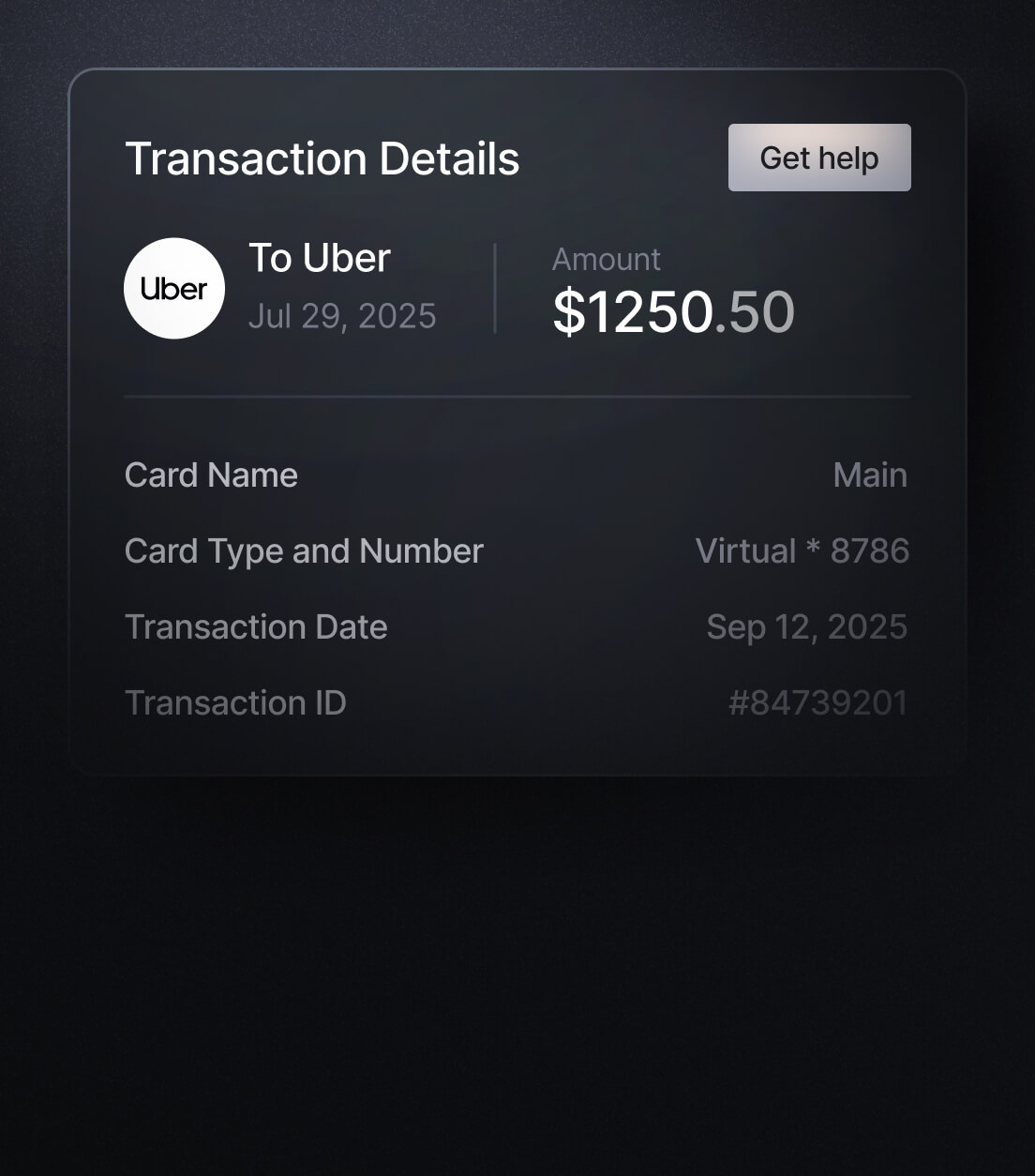

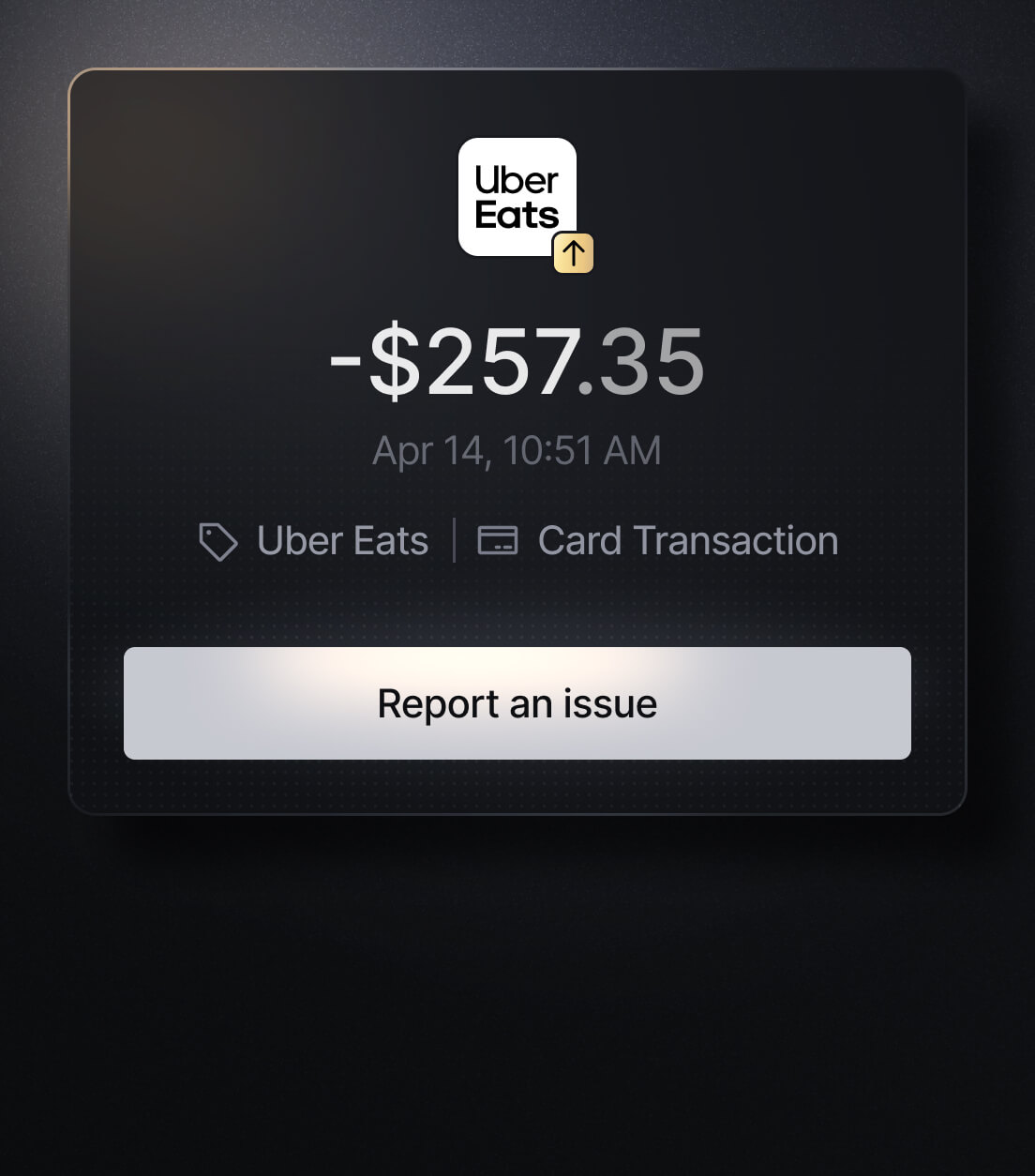

Easily Identify Every Charge with Slash

See exactly where, when, and how each charge occurred, complete with merchant names, payment types, and connected team cards with Slash’s detailed card logs and expense tracking tools.

Discover more insights

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.