Vendor Payment Automation: How It Works and Key Benefits

Businesses that still rely on manual steps to pay vendor invoices may risk staggering behind their competition. Old-fashioned processes like emailing PDFs, chasing approvals, re-entering data across systems, and issuing paper checks cost time and money. What seems manageable with a handful of vendors becomes overwhelming as businesses scale and payment complexity increases.

The consequences of fractured processes can appear quickly: payments get delayed, errors multiply, fraud risk increases, and cash flow visibility suffers. Ultimately, damaged vendor relationships often follow, as delays and errors may frustrate suppliers and lead them to look for business elsewhere.

Vendor payment automation addresses these challenges by standardizing how electronic payments are approved and executed. Rather than handling each payment as a unique event, automation creates a controlled, predictable process where payments move reliably through defined workflows.

This article explains what vendor payment automation is, how it works, the key benefits it delivers, when it becomes necessary, and the best practices for implementing it effectively. We’ll also explore how the Slash business banking platform supports smarter vendor payment automation by centralizing payment execution, improving cash flow visibility, and more.¹

What Is Vendor Payment Automation?

Vendor payment automation refers to the use of specialized software to automate how a business transfers funds to suppliers, from processing invoices to completing payment. It’s a bit different from accounts payable (AP) automation, which encompasses intake, validation, approval, and settlement. Vendor payment automation focuses on payment execution specifically, while processes like expense categorization and reconciliation fall outside of that scope.

Companies that still pay their suppliers manually often rely on spreadsheets, email chains, repeated data entry across systems, and manual reconciliation. Each payment becomes its own project, requiring coordination across multiple people and platforms.

In automated setups, payments follow defined paths within centralized systems. Invoices are validated against existing purchase orders, payment methods are pre-selected for each vendor, execution happens on specified dates, and transaction records sync with accounting systems. Platforms like Slash go further by allowing users to schedule and track recurring transfers for cyclical expenses, allowing users to automate several months of payments with nothing more than a few clicks.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How Does Vendor Payment Automation Work?

While the process may feel like magic, vendor payment automation follows a specific list of steps that saves finance teams time at each turn. Here’s how it works:

Invoice Entry and Data Capture

With automation software, invoices travel from the vendor directly into the payment system instead of clogging up email inboxes and spreadsheets. Once captured, the system extracts key data like vendor identification, invoice number, amount, due date, and line item details. When finance professionals no longer have to manually type invoice information into multiple systems, errors are minimized and time is maximized.

Approval Workflow Execution

With invoice data acquired, the payment progresses through approval workflows without repeated handoffs or additional data entry. Many systems allow you to customize approval paths based on vendor, department, or dollar amount. Approvers then receive notifications with invoice details, purchase order information, vendor history, and budget impact. From there, they can approve or reject directly within the system.

Payment Scheduling and Execution

After an invoice receives all required approvals, the system schedules payment based on invoice due dates or particular preferences configured by finance teams. Whether in the form of ACH, wire transfer, or virtual card, payment methods are selected in advance for each supplier based on their preferences or your policies. Some automation software, such as Slash, even allows near-instant transfers via RTP or stablecoin.⁴

Once a vendor's payment method is configured, every payment to that vendor executes the same way, on time, without requiring setup or intervention for each transaction.

Instant Recordkeeping

Following an executed payment, teams can track transfer status, confirm delivery, and keep records connected with their accounting system. This automatic reconciliation eliminates the manual work of matching bank statements to accounting records, confirming which invoices have been paid, and updating vendor balances. Slash fully integrates with accounting platforms like Quickbooks Online, meaning financial records and invoice data can flow both ways.

Key Benefits of Vendor Payment Automation

Automating supplier payments isn't just about speed (even though that’s one of the best parts). It also helps reduce friction, risk, and inconsistency in the accounts payable process. Here’s a full breakdown of the benefits:

Predictable Vendor Payments and Cash Movement

Cash flow management should be proactive, not reactive. With dedicated software, you can gain clear visibility into upcoming payment obligations and can forecast accurately based on scheduled transactions. When transfers execute automatically, your cash flow becomes more predictable and your vendors will be more pleased with your consistency.

Fewer Manual Touchpoints and Operational Risk

Even for veteran finance teams, each manual step represents an opportunity for mistakes and delays. Physically entering data often results in typos, especially when logging extensive information in multiple systems. Human workflows also have a habit of relying on one or two expert employees, which may go smoothly for a while—until your most valuable team member goes on vacation.

Vendor payment automation software never takes a day off. These systems can also scan and intake invoices, which means errors that used to form between creation and entry will be nearly eliminated.

Stronger Controls, Security, and Audit Readiness

The keys to compliance and security are visibility and consistency. Automated payment systems automatically log every action, providing comprehensive audit trails. Centralized payment execution makes fraud attempts easier to detect and ensures that payment inconsistencies won’t get lost in stacks of spreadsheets.

When everything is systematically maintained and accessible on demand, you’ll be tax compliant and prepared for audits.

Better Vendor Relationships

Streamlined transactions are a win-win for your supplier relationships. When vendors can trust that they’ll receive timely payment, they’ll be more willing to offer favorable terms and treat you as valued customers. Thanks to the fact that payments are consistent and records are clear, you won't often encounter repeated inquiries and disputes.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

When Vendor Payment Automation Becomes Necessary

For a small startup with one or two suppliers, vendor payment automation may initially be a “nice to have”. However, rapid growth may suddenly turn it into a “need to have”. Here’s when automation becomes necessary:

Vendor Volume and Payment Complexity Increase

Quick expansion is great news for any company, but it can come with the breakdown of manual processes. Spreadsheets that track payment status become bloated and out of date, invoices start slipping through cracks, and siloed information hurts visibility. Trying to juggle everything can cost finance teams time that should be spent analyzing performance and forecasting for the future.

Payment Methods Become Too Diverse

As businesses take on new vendors, they’ll find that some request ACH payments, others prefer card transactions, and overseas suppliers require international wire transfers with complex fees and regulations. Each method has different rules, timings, and costs.

Without dedicated systems, accounts payable experts must navigate different portals, remember vendor preferences, and ensure correct methods are used. As you might expect, this commonly leads to errors. The Slash business banking platform centralizes all payments on an all-in-one dashboard that keeps transactions organized, no matter the variety or volume.

Multiple Approval Paths Emerge

When a company takes on a wide range of purchase orders and invoices, approval paths can multiply. Early-stage companies might have single-approver processes, but as organizations grow, approval requirements often branch by amount, department, and purchase type. Managing these paths manually leads to lots of email forwarding, delays, and uncertainty about whether proper approvals were obtained.

Manual Processes Stop Scaling with the Business

As companies grow, finance teams can struggle to keep up with increased payment volume and complexity. Keeping up with endless invoices across fractured systems can quickly turn from “less efficient” to downright impossible.

Approval chains get backed up, errors multiply as processing is rushed, risk increases as shortcuts emerge, and staff frustration rises. It’s not sustainable. When the operational cost of maintaining manual workflows outweighs the effort required to execute them, it becomes time to switch to an automated system.

Best Practices for Implementing Vendor Payment Automation

Adopting vendor payment automation requires thoughtful intent and strategy. Tossing technology onto chaotic processes just automates that chaos. Here are some steps to implementing automation effectively:

- Centralize how vendor payments are executed: When payments happen through one banking portal, another through accounting software, and others through standalone payment services, visibility fragments and controls weaken. Centralizing payment into a single system means all approved payments flow through one place where they're scheduled, executed, and recorded.

- Only review flagged transactions: Design workflows that automatically approve routine payments while flagging reports with unusual patterns for review. The payment process can be accelerated, and your team can still intervene when necessary.

- Standardize vendor onboarding: Proper onboarding can ensure regulatory compliance, reduce financial risk, improve payment accuracy, and create clear accountability across teams. This process includes collecting banking details and confirming preferred payment methods up front, which streamlines transactions right away.

- Keep accounting and payment data in sync: Ensure payment systems integrate with your accounting software so transaction data matches seamlessly. When transfers execute, accounting records should update simultaneously without requiring manual entries or reconciliation. Slash fully integrates with accounting platforms like Quickbooks Online, meaning financial data flows both ways.

- Monitor and tweak results: With automation, you’ll likely see improvements in metrics like cost per transaction, processing times, and overall accuracy. If any results fall below your expectations, determine what needs to change and how.

Choosing the Right Vendor Payment Automation Approach for Your Business

The final step is choosing the right type of platform. Three common approaches exist for implementing vendor payment automation:

- Standalone tools focus specifically on payment processing, scheduling, execution, and recording. For invoice management and accounting, they require integration with other systems.

- Platforms that combine spend management and payments offer features like integrated invoice management, approval workflows, payment execution, and expense management on unified platforms.

- Custom or internal systems built on banking APIs and payment rails provide maximum flexibility and control -- but they require development resources and ongoing maintenance.

The right choice depends on your existing workflow, integrations, and goals. Standalone tools work well when you already have a solid accounts payable system and only need to automate payment execution. Custom systems make sense for companies with unique developmental requirements (and spare time).

Platforms that combine vendor payments with other features like expense management and international payment support are best for teams that plan on modernizing their entire accounts payable process. Companies looking for this kind of solution may consider turning to Slash.

How Slash Enables Smarter Vendor Payment Automation

Slash is a business banking platform that provides the payment infrastructure finance teams need to fully automate vendor payments. Rather than requiring finance professionals to navigate multiple banking portals and manually trigger individual payments, Slash centralizes payment execution on an integrated dashboard.

Our platform helps teams automate and streamline the payment process by supporting multiple payment method options, including ACH payments, wire transfers, virtual cards, and crypto. This way, vendors receive payment through their preferred methods without human errors or delays. With our tools, you also get real-time visibility into the payment journey, revealing what transactions are scheduled and which have executed.

Slash also syncs payment activity with accounting systems like Quickbooks Online, reducing reconciliation work and ensuring accounting records stay current as payments execute. Outside of the accounts payable process, we also offer:

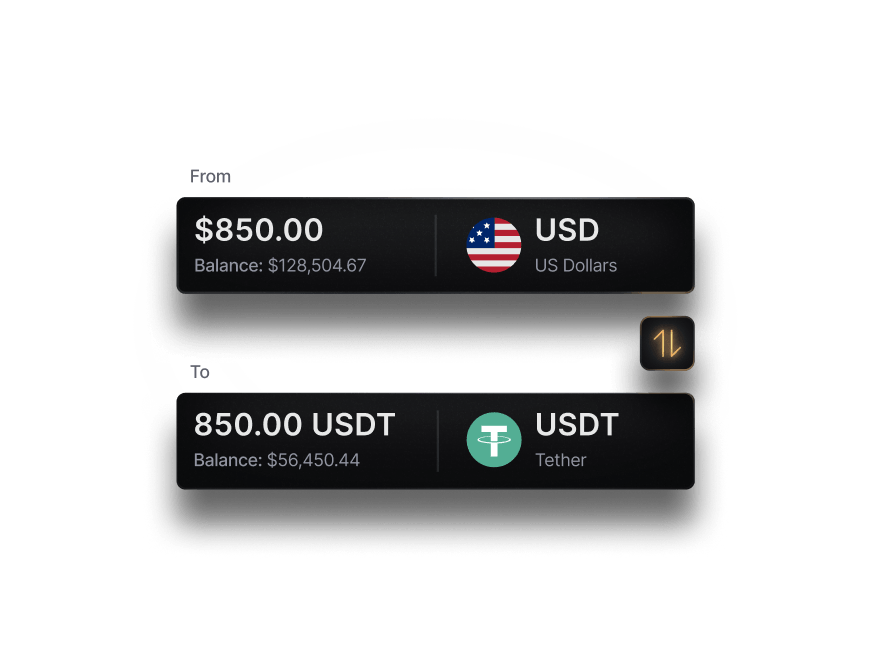

- Native cryptocurrency support: On our platform, you can on- and off-ramp USDC, USDT, and USDSL with conversion fees under 1%. Send or receive stablecoins across 8 blockchains with processing that can take less than 10 minutes.

- Slash Visa® Platinum Card: Our corporate charge cards earns users up to 2% cash back across all company card spend. Set spending rules by category, merchant, or team, and issue unlimited virtual cards for recurring vendor payments or controlled employee access.

- High-yield treasury: Slash offers treasury accounts that allocate funds into securities powered by BlackRock and Morgan Stanley, with yields up to 3.83% annualized.⁶

Slash helps finance teams execute vendor payments in a controlled and visible way as complexity grows, without increasing manual overhead or weakening guardrails against fraud. Learn how we can streamline your accounts payable process today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

How is AP automation different from vendor payment automation?

Vendor payments are a step within the AP automation cycle. AP automation includes invoice processing, validation, approval, and settlement. Vendor payment automation concerns the details, scheduling, and execution of outgoing payments to suppliers.

Accounts Payable Automation: 6 Best Practices to Streamline Your AP Process

What is the invoice processing journey?

The invoice processing journey includes intake & verification, data extraction and validation against purchase orders, approval routing (automated or manual), payment scheduling, payment execution, and recording/archiving.

Invoice Management: Streamline Processes, Reduce Errors, and Optimize Cash Flow

Read more from us