SWIFT Cross-Border Payments Guide: Optimizing Efficiency for Your Global Payments

If you’ve ever sent money overseas, you already know that it’s a bit different from sending money within the U.S. The U.S.’s interconnected banking systems, like ACH, wire, and RTP, obscure the more complex and less connected global banking system. Without a shared language binding the world’s banks together, we wouldn’t know how to move money across borders, how to route payments between institutions, or when and how to convert currencies.

That’s where SWIFT comes in. The SWIFT network connects banks across countries and serves as a reliable and efficient system for international payments. However, although SWIFT is widely used and well trusted, it comes with tradeoffs. High processing fees, payment delays, and FX swings can make cross-border payments more expensive and less predictable.

In this guide, we’ll show you how to best use the SWIFT network when sending international payments. We’ll break down how it works, explain which types of transactions are best suited for SWIFT, and highlight alternative cross-border payment methods that can unlock faster, lower-cost transfers. For a more dynamic global payment stack, you can use Slash, a business banking solution with global ACH settlement, international wires via the SWIFT network to 180+ countries, and cryptocurrency payment options that can help reduce the fees and delays of traditional banks.¹, ⁴

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

What are SWIFT cross border payments, and how do they work?

There’s a common misconception that SWIFT is a payment rail like ACH or SEPA, but this is not the case. SWIFT is an interbank messaging network; it communicates standardized instructions that tell banks how to process payments between financial institutions. In other words, SWIFT doesn’t actually move money, it tells banks how to move it.

Prior to the SWIFT network, cross-border payments relied on Telex, a manual and error-prone messaging system that required banks to send payment instructions in unstructured formats. In 1977, SWIFT modernized cross-border payments by introducing a secure, standardized messaging network. Over time, it has continued to evolve with updates like SWIFT GPI, which brought improvements to speed, transparency, and tracking for international transactions.

When you send a SWIFT payment, your bank sends a SWIFT message (often an MT103) that contains all the payment instructions to the receiving bank. The message includes information about the sender, beneficiary, amount, currency, and destination account number. These messages rely on BIC (Bank Identifier Codes) to route payments to the correct financial institutions. Each bank in the SWIFT network has a unique code that ensures the message is delivered accurately.

If the sending and receiving banks don’t have a direct relationship, intermediary banks (also called correspondent banks) are used to complete the transaction. These banks hold correspondent accounts, often referred to as nostro and vostro accounts, which allow them to settle funds on behalf of each other. As the payment moves through this chain, each institution follows the instructions in the SWIFT message to debit and credit accounts accordingly. This process is known as correspondent banking, and it forms the backbone of today’s global payment systems.

Because each bank in the SWIFT payment chain performs its own validation, processing, and currency conversion (if needed), SWIFT payments can be expensive. Intermediary fees are often added along the way, and costs can increase depending on how many banks are involved in a given transaction. For example, sending a SWIFT payment between the U.S. and Great Britain will typically involve lower fees due to strong correspondent banking relationships, while sending a payment from the U.S. to a country like Kosovo may require more intermediaries, resulting in higher costs.

How do you send SWIFT cross-border payments?

Initiating a SWIFT payment differs among financial services providers. It can be as simple as entering a few details in your online banking dashboard, or it may involve additional steps like calling your bank to initiate the transaction. Instead of covering every method, let’s walk through how to send a SWIFT payment using Slash:

Step 1: Initiate the transfer

In Slash, begin by navigating to the “Move Money” button in your dashboard. Clicking it opens a window where you can start entering the transfer details.

Step 2: Input the recipient’s banking details

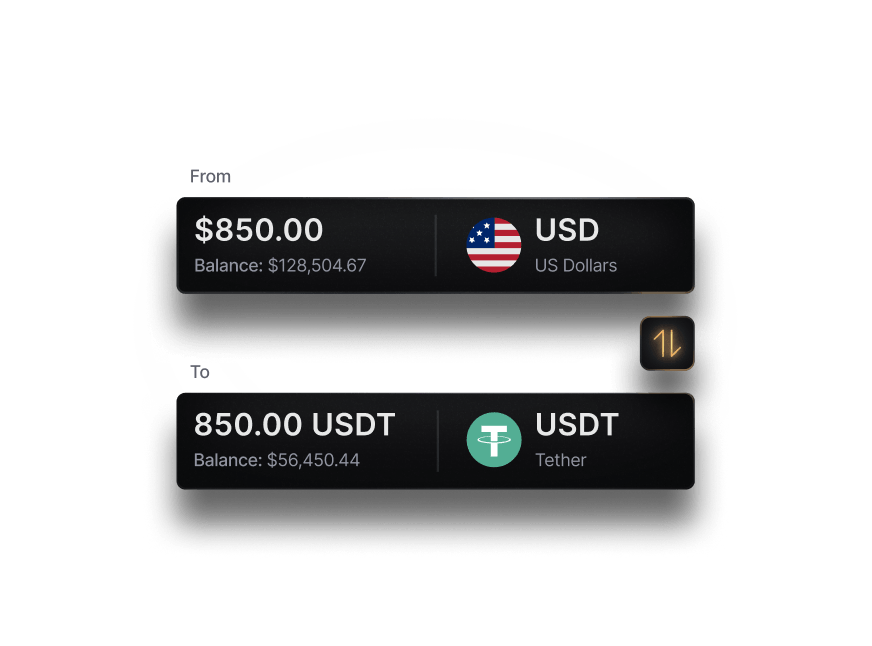

You’ll need several pieces of information to ensure the funds are routed correctly. This includes the recipient’s account number and their bank’s routing details. For international payments, you’ll also need a SWIFT code, also known as a BIC, which identifies the recipient’s bank within the SWIFT network. If your recipient doesn’t know their SWIFT code, they can request it from their bank.

Step 3: Calculate the transfer amount

Depending on how you were invoiced, you may need to do some math to figure out how much money to send. If you were invoiced in your home currency, then no worries. If it’s in the recipient’s currency, you’ll need to calculate the conversion using the current exchange rate.

In any cross-border transaction, there is always some FX exposure. Between the time you initiate the payment and when it settles, exchange rates can fluctuate, which may result in a slight overpayment or underpayment. To manage this, some businesses use risk-sharing clauses, which split the difference if exchange rates move beyond a set threshold, or forward contracts, which lock in an exchange rate for a future transaction.

Step 4: Verify payment details

Once you’ve entered the payment amount and recipient details, double check everything before sending. Incorrect information can delay the payment or require manual recovery, which is not always guaranteed. Slash helps reduce errors by saving and organizing verified banking details for your contacts, giving you a reliable record for future transfers.

Step 5: Send and track the payment:

After confirming the details, click ‘Send payment.’ Once sent, Slash will transmit a SWIFT message with the payment instructions through the SWIFT network. You can track the payment as it moves through intermediary banks to the beneficiary’s account by using SWIFT’s Basic Tracker tool. Input the UETR code (listed under ‘Advanced transaction details’ on Slash) into Basic Tracker to check the status, processing steps, and estimated settlement time.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Why should you use SWIFT for cross-border payments? N benefits

SWIFT remains the backbone of global payments, and for good reason. Despite newer alternatives, it continues to be one of the most reliable and widely used ways to send money internationally. Here’s why:

Global reach

SWIFT is the default cross-border payment method at over 11,000 banks in nearly every country on Earth. That level of global reach is hard to beat. Since SWIFT works directly with bank accounts, senders and recipients don’t need to configure any niche third-party services for handling their payments.

Trusted and widely accepted

As the standard global payment messaging system, SWIFT implements some of the most sophisticated controls and protections of any payment system. It uses advanced encryption and authentication measures to prevent unauthorized access to banking details and transaction data.

Suitable for high-value transactions

There is no strict network-imposed limit on the amount you can send through SWIFT. Individual banks and providers may set their own caps, often around $10,000 and sometimes up to $1M or more per transaction, making SWIFT well suited for large international transfers.

Clear visibility

SWIFT provides tools like the Basic Tracker to give insight into payment status. Each bank in the chain maintains records, allowing you to track your payment as it moves through the network, similar to tracking a package in the mail.

4 limitations of SWIFT cross-border payments

SWIFT is slightly hindered by the inefficiencies and business models of the global banking system. When you send a payment, you’ll typically be responsible for multiple processing fees. On top of that, delays can slow down your operations and increase the risk of currency fluctuations against you. Below, we explain these limitations in more detail:

- Intermediary fees: SWIFT payments often pass through one or more intermediary banks, each of which may charge a handling fee. These fees are not always disclosed upfront, which can make the total cost of a transaction unpredictable.

- Processing delays: Because multiple banks are involved in validating and settling the transaction, SWIFT payments can take anywhere from one to five business days to complete. Delays can be longer if there are compliance checks, time zone differences, or errors in the payment instructions.

- FX risk: Exchange rates can fluctuate between the time a payment is initiated and when it is settled. This creates a risk that the final amount received may differ slightly from what was expected, especially in volatile currency pairs. The longer the delay, the greater the risk for fluctuation.

- Currency conversion fees: In addition to FX rate fluctuations, banks often apply a markup on the exchange rate when converting currencies. These spreads can increase the total cost of the transaction beyond standard transfer or intermediary fees.

An increasingly popular alternative for getting around these downsides is cryptocurrency. Crypto payments bypass the traditional banking system and move funds across the blockchain, a secure and fast digital payment infrastructure. With Slash, you can send global payments in USDC and USDT, two stablecoins that are pegged to the value of the U.S. dollar. Funds can be converted from fiat into crypto automatically with a built-in on-ramp, transactions can settle in minutes, and there are no intermediary processing fees along the way.

Common uses of SWIFT cross-border payments

SWIFT is typically used in situations where reliability, global reach, and bank-level trust matter more than speed or cost. While newer payment methods can be faster or cheaper, SWIFT remains the standard for many types of international transactions, especially those involving large sums or less accessible regions. Here are some common use-case scenarios:

High-value international payments

A U.S.-based manufacturing company needs to pay a supplier in Germany $250,000 for a bulk equipment order. Because of the high transaction value, both parties want the payment to be processed through established banking channels with clear documentation. The company uses a SWIFT wire transfer to ensure the funds are delivered securely, with a full record of the transaction for accounting and compliance purposes.

Payments to countries without local rails

A startup in the U.S. hires a contractor in a country where modern payment systems, like local ACH equivalents or widely accepted digital wallets, are limited or unavailable. Because there’s no reliable local infrastructure for receiving payments, the company uses SWIFT to send funds directly to the contractor’s bank account.

Similarly, a nonprofit organization sending funds to a partner in a developing country may rely on SWIFT because it’s one of the only globally supported payment systems that can reach local banks. Even if the payment takes a few days, SWIFT ensures the funds can be delivered where alternative methods cannot.

Transactions requiring bank-to-bank trust

A financial services firm is transferring funds to a partner bank in another country as part of an investment deal. Both sides require a high level of trust, regulatory compliance, and traceability. By using SWIFT, the payment instructions are transmitted securely between banks, with standardized messaging and clear audit trails.

Make global payments easier to manage at scale with Slash

With Slash, you can send payments via the SWIFT network to 180+ countries in more than 135 different currencies. For those keeping track, that’s more than 90% of every country on the globe.

You also get access to a range of payment methods to fit different use cases. Global ACH settlement enables low-cost, reliable bank transfers on clearing networks like SEPA, BACS, BECS, and others. RTP and FedNow access allow you to send near-instant payments within the U.S. for minimal fees. And native cryptocurrency support provides a fast, low-cost option for global transfers.

But Slash is more than just a payment solution. It’s a comprehensive business banking platform with built-in tools for managing spend, tracking expenses, and handling financial operations end to end. Here’s what else you get with Slash:

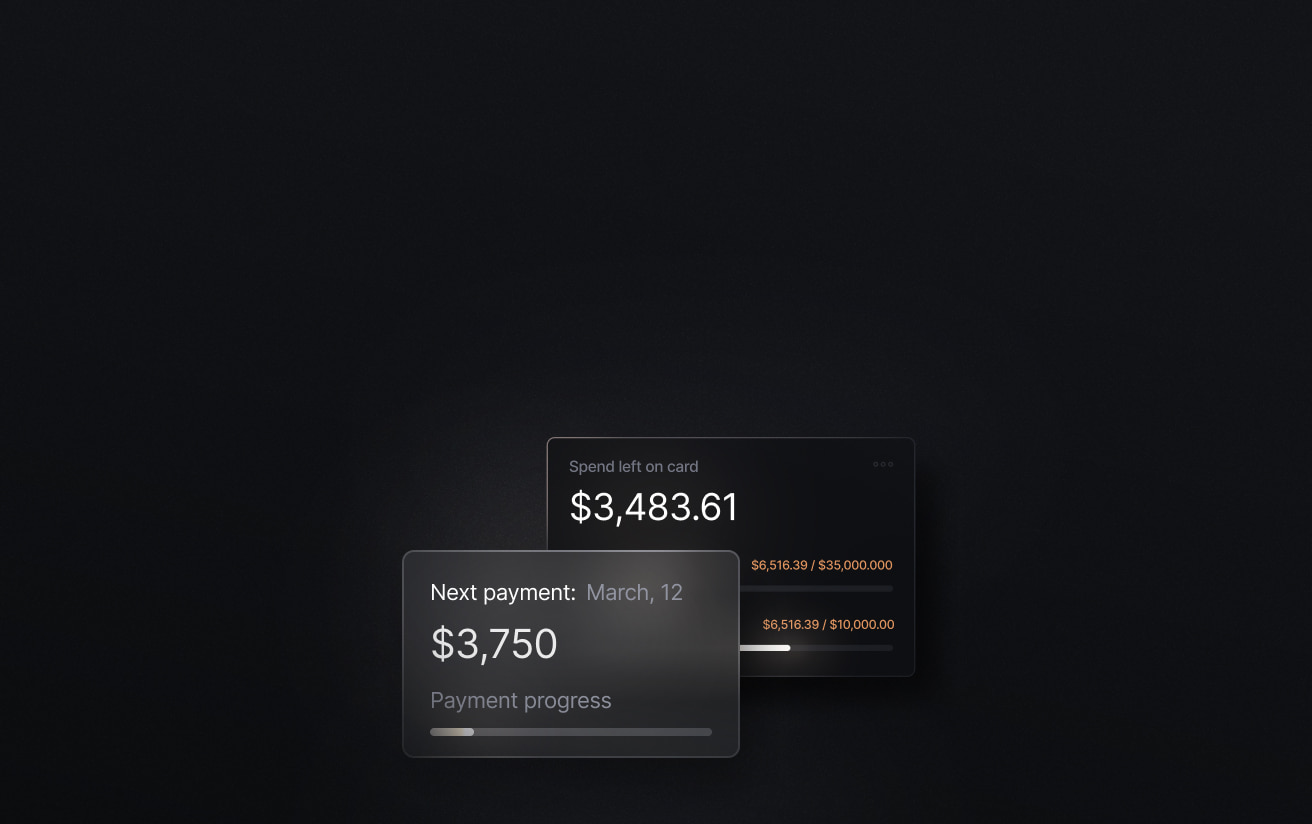

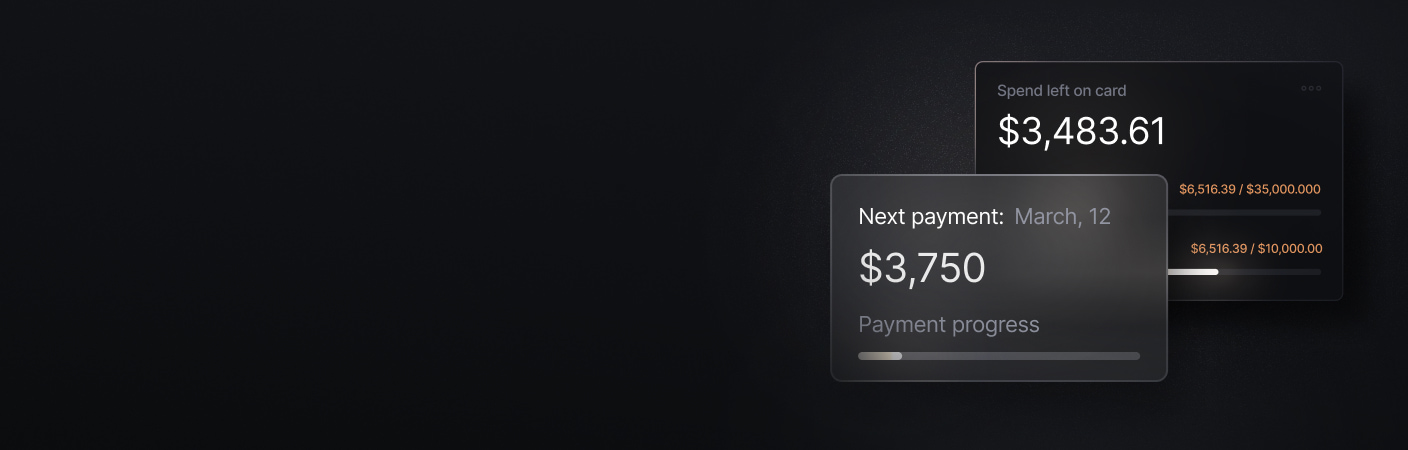

- Slash Visa® Platinum Card: A corporate charge card that earns up to 2% cash back on company spending, with configurable controls, spending limits, and strong fraud protection.

- Dynamic business banking: Open unlimited virtual accounts to separate operational funds and give teams clearer visibility into cash flow. Manage multiple business entities from a single dashboard with consolidated reporting.

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- High-yield treasury: Earn 3.82% yield on idle cash through treasury accounts backed by Morgan Stanley and BlackRock money market funds.⁶

- Capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge temporary cash flow gaps when needed.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What is a SWIFT GPI payment, and how is it different from a standard SWIFT transfer?

A SWIFT GPI payment is an enhanced version of a standard SWIFT transfer that offers faster processing, end-to-end tracking, and greater transparency on fees and FX rates. Unlike traditional SWIFT payments, GPI allows you to track your payment in real time as it moves through intermediary banks.

SWIFT Cross-Border Payments: How They Work and Key Uses

Can a SWIFT payment be canceled or recalled after it’s sent?

In some cases, yes, but it depends on how far along the payment is in the process. If the funds have not yet been credited to the recipient’s account, your bank may be able to request a recall, though success is not guaranteed and additional fees may apply.

ACH vs Wire Transfer: Key Differences, Costs, Limits & Use Cases

Why do intermediary banks charge fees for SWIFT transfers?

Intermediary banks charge fees because they help route, process, and settle the payment between the sending and receiving banks. Each bank in the chain performs its own validation and may handle currency conversion, which is why multiple fees can be applied to a single transaction.

Mastering Cross-Border Fees: Essential Insights and Strategies for Reducing International Payment Fees

Do all banks support SWIFT payments globally?

Most major banks worldwide are part of the SWIFT network, but not every financial institution participates directly. Smaller or regional banks may rely on partner or correspondent banks with SWIFT access to send and receive international payments.

What kind of messages does SWIFT send between banks?

SWIFT sends standardized financial messages, known as MT messages, that include detailed payment instructions. For example, an MT103 is used for customer payments, while an MT940 is used for account statements, ensuring consistent communication between banks.

Read more from us