How Long Do International Payments Take? A Breakdown by Payment Method

Let’s start with the obvious: international payments generally take longer than domestic ones. If you’re used to sending cross border wire transfers or IAT ACH payments, you already know. Not only do they take longer, but they’re often more expensive, come with additional regulatory requirements, and can be more difficult to reconcile in your accounting ledger.

That said, alternative payment rails and modern financial tools have significantly improved how quickly and cost-effectively businesses can move money across borders. In this guide, we’ll walk through the most common methods for international transfers, along with practical guidance on how to time them, track them, and speed them up.

If your business frequently needs to send money internationally, consider Slash, a business banking platform designed to optimize cross border payments.¹ With Slash, you can initiate international wire transfers over the SWIFT network to 180+ countries, send global ACH payments, and use cryptocurrency rails for faster, lower-cost global payments.⁴ All transaction data is also recorded automatically, helping streamline your accounting and financial planning processes, too. Continue reading to learn more.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

International Payment Timelines by Method

Let’s walk through the most common international payment methods and how they compare. For each, we’ll cover typical processing time, fees, and when it makes the most sense to use them:

Wire transfers

Most international wire transfers are facilitated by the SWIFT network, a global interbank messaging system that connects more than 11,000 financial institutions worldwide. Wires are the most widely accepted method for sending money across borders, especially when working with a traditional bank, but that accessibility often comes with higher fees and longer processing times.

Because many transfers rely on intermediary banks and correspondent banking relationships, funds may pass through multiple institutions before reaching the recipient. Each step can introduce additional fees, delays, and compliance checks.

- Processing time: Typically 1-5 business days, depending on the countries involved, intermediary banks, time zones, and bank holidays.

- Fees: Usually $25-$50 per transfer, plus potential intermediary bank fees and FX markups that may be deducted along the way.

- Best for: Large, one-off transfers where global acceptance and reliability matter more than speed or cost.

ACH transfers

Although the ACH network is U.S.-based, some providers allow you to initiate an ACH payment that settles through a foreign clearing network. Examples include SEPA in Europe, BACS in the UK, and BECS in Australia. These transfers are often referred to as global ACH and typically use the IAT SEC code, which is designed for international ACH transactions with additional compliance and reporting requirements.

Because ACH payments are batch processed rather than settled in real time, they are generally more cost-effective than wires but slower.

- Processing time: Typically 2-7+ business days, depending on the destination country, local bank processing hours, and clearing system.

- Fees: Often low or flat, ranging from $1-$10, with more favorable exchange rates than wires in many cases.

- Best for: Recurring payments, payroll, or vendor payouts where low cost matters more than speed.

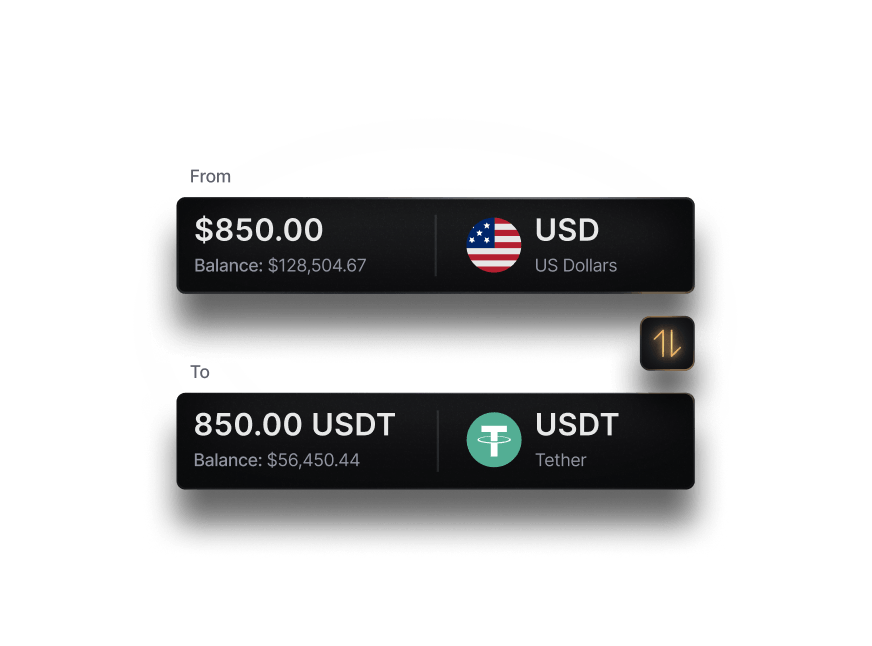

Cryptocurrency

In recent years, cryptocurrency has become a more widely used method for international transfers. With Slash, you can send USDC and USDT, which are stablecoins pegged 1:1 to the U.S. dollar. Unlike traditional cryptocurrencies such as Bitcoin, stablecoins are designed to maintain a consistent value, making them more practical for payments rather than speculation.

Because these transactions run on blockchain networks rather than traditional banking rails, they avoid intermediary banks, banking hours, and many of the delays tied to the SWIFT network.

- Processing time: Typically a few seconds to a few minutes, depending on the blockchain network and congestion.

- Fees: Network fees are usually low (less than 1%) with gas fees of $1-$2 per transaction.

- Best for: Generally the strongest general-purpose international transfer method; however, both sender and receiver must have access to a crypto wallet.

Checks

While less common today, mailing checks internationally is still an option for certain transactions. Checks are widely understood and don’t require specialized infrastructure, but they come with significant drawbacks.

They can be lost in transit, delayed by postal systems, and subject to long clearing times once deposited. In addition, fluctuations in exchange rates during transit can impact the final value received.

- Processing time: Often 1 to 3 weeks or longer, including mailing and clearing time.

- Fees: Mailing costs plus potential bank processing and conversion fees upon deposit.

- Best for: Low-frequency payments where digital options are not available.

International money orders

International money orders are prepaid paper payment instruments that can be sent across borders. They function similarly to checks but are backed upfront, which can make them slightly more secure for the recipient.

That said, they are increasingly being phased out as faster and more flexible digital payment options become available.

- Processing time: Typically 1 to 3 weeks, depending on delivery and deposit timelines.

- Fees: Purchase fees, mailing costs, and possible conversion fees at the receiving bank.

- Best for: Situations where electronic payments are not possible and a guaranteed paper payment is required.

Closed-network digital wallets

Some digital wallets, such as PayPal and Wise, allow users to send money internationally with relatively fast settlement times and transparent pricing. These platforms operate on closed or semi-closed networks, meaning both the sender and recipient typically need accounts with the same provider.

While convenient, they may not offer the same level of flexibility, control, or scalability that businesses need for larger or more complex payment operations.

- Processing time: Instant to 2 business days, depending on payout method and currency conversion.

- Fees: Vary by provider, often including a percentage-based fee and FX spread.

- Best for: Smaller transfers, P2P payments, and simple cross-border transactions.

Credit cards & charge cards

Credit and charge cards are most commonly used for making purchases in a foreign currency rather than sending direct transfers. A credit card allows you to carry a balance and pay interest over time, while a charge card requires you to pay the full balance each billing cycle.

Many business cards offer low or no foreign transaction fees, though some still charge around 1 to 3 percent per transaction. The Slash card, for example, is a charge card on the Visa network that offers a low 1% FX fee (minimum $0.40).

- Processing time: Transactions are typically authorized instantly, with settlement occurring within 1 to 3 days.

- Fees: Foreign transaction fees, usually between 0% and 3%, plus any applicable currency conversion costs.

- Best for: Business travel, international purchases, and expense management.

Why International Payments Take Longer Than Domestic Transfers

International payments move through a much more complex system than domestic transfers. They may pass through multiple banks, compliance checks, and time zones, which adds time at each step. Here’s where those delays come from:

Intermediary banks and correspondent routing

International payments often rely on intermediary banks to move funds between institutions that do not have direct banking relationships. When you initiate a transfer over the SWIFT network, your provider sends a message through one or more correspondent banks before the funds reach the recipient’s bank. Each intermediary processes the payment, validates details like the account number or IBAN, and may deduct fees along the way, which increases both the processing time and the likelihood of delays compared to a domestic transfer that moves through a single network.

Time zones, banking hours, and bank holidays

Domestic transfers operate within a single country’s banking hours, but international transfers often span multiple time zones. If a payment is initiated outside of business hours, on weekends, or during bank holidays or public holidays, it may not begin processing until the next available window. Because each bank in the chain operates on its own schedule, delays can stack as the transfer moves across regions.

Compliance, KYC, and fraud checks

International transfers are subject to stricter regulatory requirements than domestic payments, including KYC verification, fraud checks, and anti money laundering reviews. If any required information is missing, or if a transaction is flagged for additional review based on the recipient, amount, or corridor, the payment may be paused. These security checks are necessary, but they can extend the overall timeframe.

Currency conversion

When you send money internationally, the transfer often involves converting between currencies. Depending on the provider and routing path, this conversion can happen at the sending bank, an intermediary, or the recipient’s local bank. Each step can introduce additional processing time, and exchange rates or FX spreads may result in part of the total amount being deducted before the funds are delivered.

Differences in local banking infrastructure

International transfers ultimately depend on how efficiently the recipient’s local bank can receive and settle funds. In some countries, banks rely on batch-based clearing systems with limited processing windows, while others may require additional manual review before funds are credited. Local regulations, cutoff hours, and how well the receiving bank integrates with global networks like SWIFT all affect how quickly the recipient can access the funds after they arrive in-country.

How to Speed Up International Payments for Your Business

International payments don’t have to take days. In many cases, delays come down to a few avoidable mistakes or timing issues. These simple tips can help you move money faster and with fewer surprises:

- Double check recipient banking details: Confirm the recipient name, account number, IBAN, and SWIFT BIC code. Even small errors can cause a transfer to fail validation or be returned, adding days to the timeframe.

- Choose providers with strong banking relationships: Providers with direct connections in key corridors can reduce reliance on intermediary banks, leading to faster processing, fewer fees deducted, and fewer delays.

- Send payments on Tuesdays when possible: Avoid weekends and common bank holidays, which often fall on Mondays. Sending earlier in the week, especially Tuesday, helps ensure your transfer begins processing without delay.

- Be mindful of time zones: Each bank operates on its own schedule. A transfer sent during U.S. hours may arrive after hours for the recipient, delaying the next processing step.

- Track transfers and communicate with your recipient: Use tracking tools to monitor progress and quickly identify delays, whether at an intermediary bank or the recipient’s local bank.

The most efficient way to send money across borders: cryptocurrency

As adoption expands, the benefits of using cryptocurrency for fast, low-cost international payments is becoming harder to ignore. There are no intermediary banks, no waiting for each institution to process the transfer, and no delays because one bank in the chain is closed for a holiday. You initiate the payment, and it settles, 24/7/365.

It also cuts out a lot of the unpredictability around fees. With wires, you might see amounts deducted along the way or get hit with exchange rate markups you didn’t expect. Crypto is much more straightforward. What you send is generally what arrives, aside from a small network fee. If you’re moving money frequently or operating in slower corridors, that consistency and speed can make a noticeable difference.

How Slash Helps Finance Teams Move Money Faster Across Borders

Speeding up international payments starts with having options. Most delays happen when you’re locked into a single rail, whether that’s wire transfers with multiple intermediary banks or slower batch-based systems. Slash gives finance teams the flexibility to choose how they send money based on the situation, so you’re not forced into unnecessary delays, fees, or processing constraints.

With Slash, you can use SWIFT wire transfers to reach 180+ countries in 135+ currencies when coverage matters most, global ACH to access local clearing networks for more predictable and cost-effective settlement, or USDC and USDT when you need speed and want to avoid traditional banking delays entirely. Built-in on and off ramps make it easy to move between fiat and crypto without added complexity. Instead of relying on a single approach, you can choose the fastest or most cost-effective option for each transfer, giving you more control and far fewer surprises.

Once your payments are running efficiently, the next step is making sure the rest of your financial operations are just as streamlined. Here’s what else Slash offers:

- Dynamic business banking: Open unlimited virtual accounts to separate operational funds to give teams clearer visibility into cash flow. Manage multiple business entities from a single dashboard, with consolidated reporting and clear visibility across accounts.

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Slash Visa® Platinum Card: A corporate charge card that earns up to 2% cash back on company spending (U.S. only), with configurable spending rules, card controls, and real-time visibility into spending.

- High-yield treasury: Earn up to 3.83% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, all managed directly from your Slash account.⁶

- Flexible financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to bridge cash flow gaps when needed.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Can international payments be reversed once sent?

Yes, but only in certain cases. You can request a recall or cancellation, especially if the transfer has not yet been fully processed, though success depends on the banks involved and whether the funds have already been credited to the recipient.

Can international payments be scheduled in advance?

Yes, many providers (including Slash) allow you to schedule international transfers ahead of time. This can help you align payments with vendor terms, avoid weekends or bank holidays, and better control timing across different time zones.

Payment Automation Explained for Businesses in 2026

Can payments be tracked in real-time after being sent?

Tracking capabilities depend on the provider and payment method. SWIFT transfers may offer status updates through the online Basic Tracker tool, and cryptocurrency transfers can be tracked using the block explorer for the blockchain used.

Tracking Cross-Border Payments: Sending Money Overseas