International Business Payments: Methods, Challenges, and Best Practices

Moving money across borders can be complicated. Behind every international transfer, multiple banks and payment networks may be working together to route the payment to its destination. Depending on the system involved, that process can be relatively simple or incredibly complex. And in most cases, the more complex the route, the more you will pay in fees.

In this guide, we’ll go over every way your business can send money from one country to another. We’ll look at how each payment rail processes an international payment, which fees apply, and the systems that make it all work. We’ll also cover alternative payment methods that you may not be aware of. By the end, you’ll have a clear idea of when to use each payment rail for different situations.

With Slash, you get a range of payment methods that make it easy to choose the right option when you need it.¹ You can send global ACH or wire transfers to over 180 countries and even use cryptocurrency payments to avoid the transaction fees and delays of traditional bank transfers.⁴ And when you’re on the go, you can use your Slash card worldwide anywhere Visa is accepted. Continue reading to learn more.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

How do international business payments work?

Before diving into the process, it helps to understand a few key terms used in international payments:

- SWIFT: Acronym for the Society for Worldwide Interbank Financial Telecommunication, which is a global messaging network that banks use to securely send payment instructions for international wire transfers.

- BIC code: A bank identifier code is used to identify a specific bank in the SWIFT network, similar to a routing number. The term is often used interchangeably with a SWIFT code.

- IBAN: An international bank account number is a standardized format for account numbers used internationally to identify a specific account and bank.

- Intermediary bank: Also called correspondent banks, these are third-party financial institutions that help route payments between the sending and receiving banks when they do not have a direct relationship.

- Payment rail: The underlying network or system that moves money, such as ACH or the blockchain.

- Blockchain: A decentralized digital ledger that records transactions across a distributed network; the blockchain is what facilitates cryptocurrency payments.

Each international transfer moves through a series of steps that can vary depending on the payment method. From the moment a payment is initiated to when funds are finally delivered, different systems, banks, and networks may be involved. Understanding how this process works can help you anticipate timing, fees, and potential delays. Below is a general overview of how a bank-initiated international transfer is processed and settled:

Step 1: Initiate the payment

The process starts when the payer initiates a transfer through a bank or global payment provider. Today, initiation is typically through an online dashboard, though some banks may require phone or in-branch authorization for larger transactions.

To send money internationally, you will need more information than a domestic transfer. This typically includes the recipient’s name, bank account number or IBAN, and the bank’s SWIFT or BIC code. In some cases, you may also need the bank’s address or additional routing details, depending on the country and payment method.

Step 2: Payment processing

Once the payment is submitted, it moves through a network based on the payment method you selected. Each rail processes transactions differently:

International wire transfers (SWIFT)

The sending bank transmits the payment instructions using the SWIFT network. If the sending and receiving banks do not have a direct relationship, the payment is routed through one or more intermediary banks. Each bank in the chain performs its own compliance checks, validates the transaction, and may deduct processing fees before passing the funds along.

Global ACH

The payment originates in a domestic ACH system, such as the U.S. ACH network, and is routed to a corresponding clearing system in the recipient’s country. These payments are typically processed in batches rather than in real time, which can make them slower but more cost-effective than wire transfers. Final settlement occurs within the local clearing network, such as SEPA in Europe or BECS in Australia.

Cryptocurrency payments

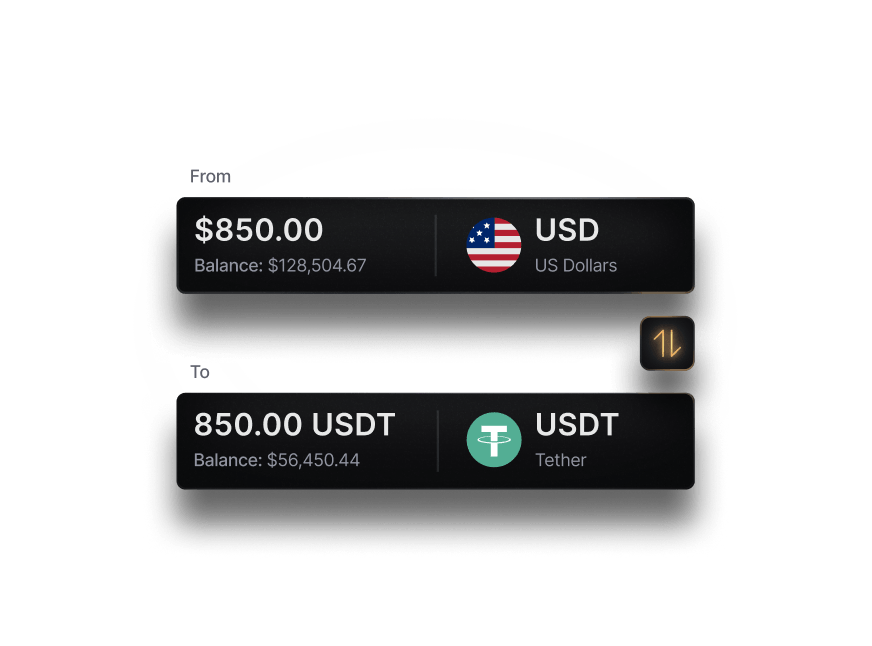

The sender uses a private key to authorize the transaction from their digital wallet. The transaction is broadcast to a blockchain network, where validators confirm it based on the network’s rules. Once verified, it is added to the distributed ledger, and the recipient’s wallet balance updates. This process can happen within minutes, depending on the network and congestion.

Step 3: Currency conversion

If the sender and recipient use different currencies, the payment will need to be converted at some point in the process. Currency conversion can happen at multiple points in the process, whether its at the sending bank, an intermediary, or the receiving bank.

The exchange rate applied is typically not the mid-market rate. Financial institutions often add a markup, which increases the total cost of the transaction. This is also where foreign exchange risk comes into play, since exchange rates can change between the time the payment is initiated and when it is settled in a different currency.

Step 4: Settlement and delivery

Once processing and any currency conversion are complete, the funds are deposited into the recipient’s bank account. Timing varies by payment method. Wire transfers can arrive within one to five business days, while global ACH transfers may take a bit longer depending on the countries and networks involved. Cryptocurrency transactions can settle much faster, though they may require conversion into local currency before being usable in a traditional bank account.

What are the different ways to send money internationally?

Not all international payments move through the same systems. The method you choose determines how the payment is routed, how long it takes to settle, and what costs are involved along the way. Below are six of the most common cross-border payment methods, along with some practical considerations for each one:

Wire transfer

Wire transfers are one of the most common ways to send money internationally, typically processed through the SWIFT network. They are widely supported by traditional banks and can reach most countries, but often involve intermediary banks, which can increase transaction fees and slow delivery times. Wires are generally better suited for larger payments, non-recurring payments.

Global ACH (IAT)

Global ACH transfers, also known as International ACH Transactions (IAT), connect domestic clearing systems across countries. They are generally more cost-effective than wire transfers but take longer to process because payments are settled in batches through local networks like SEPA or BECS. This method works well for recurring payments such as payroll or vendor invoices.

Internationally mailed check

Sending a physical check internationally is still possible, though it is less common today. The recipient must deposit the check with their local bank, which can take several weeks to clear and may involve high fees and unfavorable currency exchange rates. This method is typically only used when digital payment options are not available.

Closed-network digital rails

Closed-network payment systems, such as PayPal or similar online payment platforms, allow users to send money within the same network without relying directly on traditional bank rails. These payments are often faster and easier to initiate, especially for online payments, but can come with higher fees for currency conversion and withdrawals to a bank account. They are commonly used for smaller transactions and cross-border commerce.

International money order

An international money order is a prepaid paper payment used to send money overseas; it functions similarly to a check in that the recipient can deposit it, but it’s paid upfront rather than drawn directly from a bank account. It’s generally more secure than sending cash, but slower and less flexible than digital methods. Fees and processing times vary depending on the issuing institution and destination country.

Cryptocurrency

Cryptocurrency allows businesses to send money and accept payments internationally without relying on traditional banks or intermediaries. Transactions are processed on a blockchain network and can settle quickly, often within minutes, depending on the currency and network conditions. However, not all cryptocurrencies are supported in each region, so sending cryptocurrency across borders requires some additional research and compliance considerations.

Challenges businesses face with international payments

Each global payment method comes with its own benefits and tradeoffs. One option may work well for recurring, low-cost transfers but take longer to settle, while another may be faster but unavailable in the region you are sending to. Below are some of challenges your business should be aware of before sending international payments:

- FX fees: Foreign exchange fees are separate from processing fees. A payment provider might advertise a low transfer fee while still adding a sizable markup to the exchange rate, which means the real cost of the payment can be higher than it first appears.

- Processing delays: International payments often move more slowly than expected because the payment is not always processed continuously from start to finish. Cutoff times, weekends, local banking holidays, time zone differences, batch processing schedules, and compliance reviews can all add delays, even before the funds begin moving through the network.

- Intermediary banks: Each intermediary bank in the payment chain may deduct its own fees, introduce additional review steps, and reduce both the speed of delivery and the predictability of the final amount received.

- Lack of visibility: Some payment methods are much easier to track than others. Traditional GPI SWIFT wires offer detailed tracking, but other methods like mailed checks, money orders, and certain closed-network payment methods can provide limited status updates, making it harder to tell whether a payment is still processing, delayed, or missing.

- Reconciliation issues: International payments do not always arrive in the exact amount the sender expected. Exchange rate movements, intermediary deductions, bank fees, and partial invoice payments can create mismatches between what was sent, what was received, and what appears in your accounting system.

How to choose the right international payment method

Choosing the right method is less about picking a single “best” option and more about matching the payment to your specific situation. Here are four questions you can ask before sending a cross-border payment that can help narrow down the best option:

1. What’s the purpose of the payment?

Identifying the reason you are transferring funds should be the first act when choosing a method of payment. For example, paying a foreign suppliers may require a payment method that deposits funds directly into a bank account, making wires or global ACH more practical. For online transactions through a payment gateway, a credit card may be easier to use. You should also consider whether the recipient can accept the payment method. Not every business is set up to receive cryptocurrency or digital wallet payments, and some may require traditional bank transfers for compliance or accounting reasons.

2. What’s your level of urgency?

If speed is critical, you will want a payment method that settles quickly and avoids multi-step bank routing. Cryptocurrency and closed-network digital rails can often process transactions within minutes or hours, making them a strong fit for time-sensitive payments. Traditional bank wires can also be relatively fast, but timing still depends on cutoff hours, time zones, and whether intermediary banks are involved.

Best for quick settlement: Cryptocurrency, closed-network digital rails

3. What’s your cost sensitivity?

Costs are not always structured the same way across payment methods. Some charge higher upfront transaction fees, while others embed costs in exchange rate markups or intermediary deductions.

Wire transfers often involve multiple layers of fees, from sending charges to intermediary bank costs and FX markups, while global ACH tends to be cheaper upfront but can still include currency conversion costs. Cryptocurrency can bypass many of these bank fees altogether; with Slash, you can send and receive cross-border crypto payments for under 1%, giving you a lower-cost option than traditional banking rails.

Best for low-cost international transfers: Cryptocurrency, global ACH

4. How often will you send the payment, and what’s its size?

Some rails are optimized for recurring, lower-value transactions, while others are better suited for large, one-time transfers.

Batch-based systems like ACH are often used for recurring payments because they can process multiple transactions efficiently, while wire transfers are typically used for higher-value payments that require direct bank-to-bank delivery. With Slash, you can schedule outbound ACH, wire, and cryptocurrency payments so you stay on top of recurring payment terms without having to manage each transfer manually.

Best for recurring payments: Corporate cards, global ACH, wire transfers

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

5 best practices for sending international payments

Once you understand how different payment methods work and where issues tend to arise, the next step is improving how your business manages those payments day to day. Small adjustments to your process can make a noticeable difference in cost, visibility, and overall efficiency. Below are some practical, low-effort ways to improve how you move money across borders:

- Keep all your payment activity in one place instead of using multiple different services. Splitting activity across bank dashboards, crypto exchange platforms, and third-party digital wallets can make it significantly harder to keep a close eye on all your transactions. With Slash, you can manage ACH, wire, card, and cryptocurrency payments in one place, so all records stay centralized.

- Know how to track your transfers. Figuring out if your payments are processing, delayed, or cancelled can be much easier if you know how to use transaction tracking tools. SWIFT wire transfers can often be tracked using services like the SWIFT Basic Tracker, while cryptocurrency payments can be followed on a block explorer for the relevant network. It’s also important to bear in mind that some methods, like checks and money orders, offer little to no tracking once they are sent.

- Keep accounting records aligned with how payments settle. International payments rarely arrive in the exact amount that was sent due to FX swings, fees, and exchange rate markups. Building processes that account for these differences helps avoid discrepancies and reduces manual work during reconciliation.

- Understand jurisdictional regulations before sending payments. Different countries have different rules around cross-border transfers, especially for non-bank methods like cryptocurrency. Being aware of local requirements, reporting obligations, and restrictions ahead of time can help you avoid delays, rejected payments, or compliance issues.

- Implement FX hedging strategies by negotiating forward contracts to lock in exchange rates ahead of time or using options to protect against unfavorable currency shifts. You can also reduce exposure by aligning revenue and expenses in the same currency wherever possible.

Start optimizing your global payments with Slash

When you’re working with a limited set of international payment options, you’re at a disadvantage. You pay more in fees when you don’t have the right alternatives, wait longer than necessary for settlements, and take on more FX risk when you can’t control how and when funds are converted. Over time, those losses add up.

Slash helps you optimize how you send global payments. From a single dashboard, you can move money via ACH, wires, crypto, or cards depending on what makes sense in the moment. Some payments need to be fast; some need to be cheap; some need to land in a specific currency. With Slash, you choose instead of working around limitations.

Slash supports outbound payments to 180+ countries in over 135 currencies, with everything in one place. No switching between crypto dashboards, banking portals, or card platforms to track activity. Every transaction is recorded, organized, and ready for accounting as soon as it hits your dashboard.

Here are some additional features that can elevate how your business manages its finances:

- Slash Visa® Platinum Card: Earn up to 2% cash back, set customizable spending controls and limits, and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more.

- Expense management: Streamline expense reporting with end-to-end SMS receipt collection for Slash cards, simple reimbursement flows, and automatic accounting updates.

- Accounting integrations: Connect Slash with QuickBooks, Xero, or Sage Intacct so your transaction data flows directly into your books, already categorized and ready for reconciliation.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury accounts: Earn up to 3.82% annualized yield on idle funds through money market investments from BlackRock and Morgan Stanley, managed directly in your Slash account.⁶

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What are intermediary banks, and how do they affect transfer?

Intermediary banks route funds between the sending and receiving banks when no direct relationship exists. Each intermediary in the chain can add processing time and may charge additional fees, increasing both the cost and duration of the transfer.

Mastering Cross-Border Fees: Essential Insights and Strategies for Reducing International Payment Fees

Are international payments reversible once sent?

Most international payments are difficult to reverse once they’ve been processed, especially wire transfers and cryptocurrency transactions. If a payment needs to be canceled, it usually must be caught early. Once it hits the recipient’s bank account, you’ll need to contact the recipient about recovering funds.

Tracking Cross-Border Payments: Sending Money Overseas

What should businesses check before adding a new international payee?

Businesses should verify the payee’s banking details: account numbers, SWIFT/BIC codes, and currency preferences. It’s also important to confirm the recipient’s identity and ensure the payment complies with any relevant regulations or internal approval processes.

SWIFT Cross-Border Payments: How They Work and Key Uses

Read more from us