Reduce Costs on International Payments: Cross-Border and International Payment Fees Explained

Imagine this: you've just sent a payment to one of your suppliers in Europe. After switching to a new local bank that promised transparent international payment fees for international transfers and lower wire transfer costs, you're eager to see if their service lives up to the claims—especially since you work with many different overseas partners. You initiate a wire transfer and execute the payment. Then, the wait begins.

Five days later, the wire finally arrives, but not without a problem. Your supplier contacts you because the amount received isn't enough to cover the full invoice. After investigating, you discover the issue: your bank routed the payment through multiple intermediary banks, each deducting their own intermediary bank fees along the chain. By the time the payment reached its destination, over $500 in value had been lost to various bank charges you never anticipated.

This frustrating scenario of hidden cross-border fees occurs daily for businesses managing international transactions. Hidden fees, unclear currency conversion fees, markups, and lengthy processing times can create a payment experience that's both expensive and confusing. In this guide, you'll learn exactly what cross-border fees entail, how they compare to other international payment fees, and the critical factors behind these costs. Most importantly, we will equip you with proven strategies to dramatically reduce your international transfer fees, ensuring more cost-effective global payments.

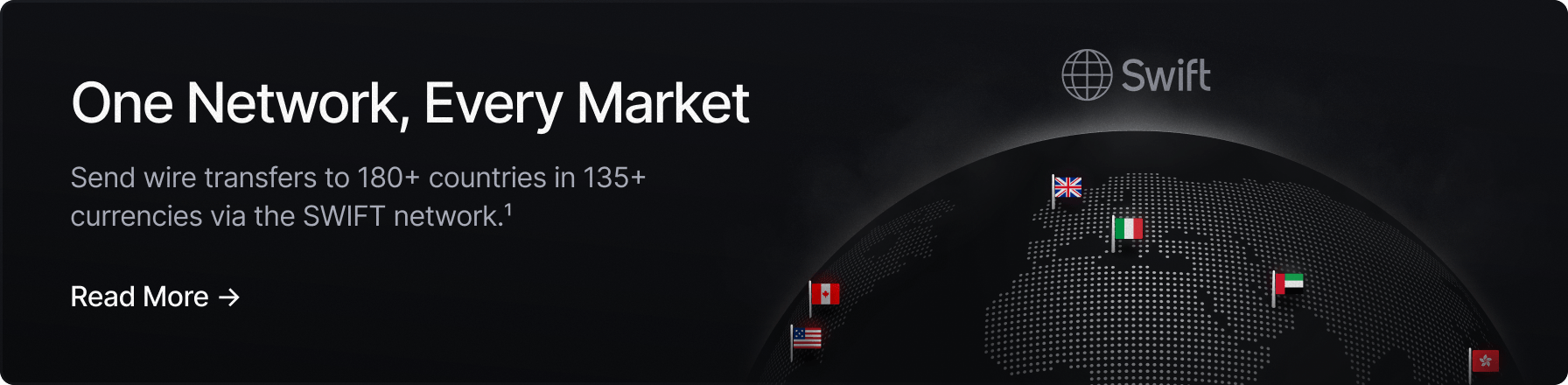

This is where we come in: Slash is a revolutionary banking platform and global payment solution designed to eliminate complexities and high costs of traditional international payments.¹ With Slash, you can effortlessly conduct cross-border transactions in over 180 countries in 135+ currencies, including cryptocurrencies. Slash's integrated platform allows businesses to deliver fast and efficient international payments, drastically reducing the time and fees usually associated with international bank transfers.⁴

What is a cross-border fee?

A cross-border fee is an additional charge applied when a payment involves parties in different countries or when a transaction is processed across international borders. These fees come into effect whenever money moves between different nations, regardless of whether currency conversion is involved. Cross-border fees apply across various payment methods and situations, including:

- Credit card transactions: When you use a credit card issued in one country to make a purchase from a merchant in another country, credit card companies typically charge a cross-border fee on top of the usual interchange fee—often labeled as foreign transaction fees by issuers. This happens even if both parties use the same currency. For example, a USD credit card used at a USD-accepting merchant in Canada would still incur cross-border charges.

- Wire transfer fees: International wire transfers through the SWIFT network or other payment rails can involve international wire transfer fees from your local bank, intermediary bank fees, and the recipient's bank. Depending on the provider, costs can be a flat fee or vary depending on the amount and destination.

- ACH payments: While domestic ACH transfers are typically low-cost, international service extensions may involve additional processing charges or ACH payment fees when sending payments to bank accounts in different countries.

- Digital payments: Payment processors like PayPal or Wise charge cross-border fees and other international payment fees when facilitating international transactions, often combining these with currency conversion fees and markups.

The charge structure for cross-border fees can vary depending on the payment method and provider used. Some traditional banks impose a flat fee or a percentage-based charge, while others may use tiered pricing based on transaction volume.

Cross-border fees v. foreign transaction fees

Though the difference is subtle, cross-border fees and foreign transaction fees are not exactly the same thing. Recognizing this distinction can help you better evaluate payment options and identify where costs are actually coming from.

A "cross-border fee" is a broad umbrella term that encompasses all extra charges on international purchases or transfers. The term can refer to multiple cost components bundled together, including foreign exchange fees, currency conversion fees, and interchange fees.

Foreign transaction fees usually refer to the network processing fees and service charges for handling transactions across international borders. This applies to both banking transfers and credit card networks like Visa and Mastercard. You may also see related costs itemized as FX fees (sometimes written as fx fees) for currency conversion or network processing.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Other international transaction fees

Currency conversion fees, also called foreign exchange (FX) fees, refer to the markup your bank, currency exchange service, or payment processor adds when converting between different currencies. Currency conversion fees may appear as a separate line item on your statement, or they may be embedded directly into the exchange rate provided by your bank. When embedded in the rate, the fee is added to the mid-market conversion rate, which is the real-time wholesale exchange rate banks use when trading foreign currencies with each other.

Cryptocurrency presents an alternative payment method that can bypass this fee-heavy structure entirely. Because cryptocurrencies are transferred and settled on the blockchain, a decentralized and heavily-encrypted informational network, they don't rely on banks to manually process and convert each cross-border transfer. As a result, cryptocurrency payments can move much faster and cost much less in fees than institutional bank transfers.

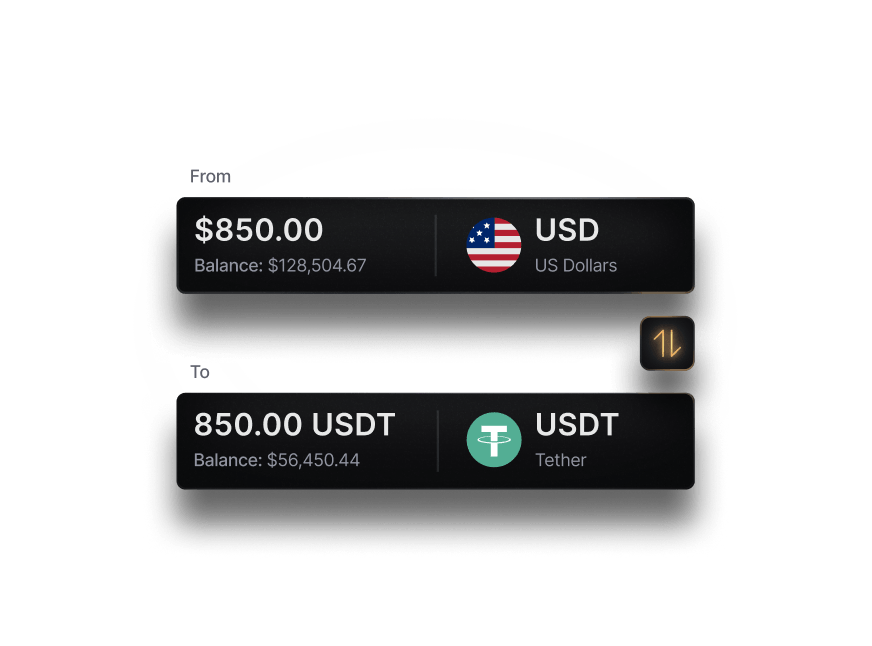

With Slash, you can send and receive two different USD-pegged stablecoins natively within the platform: USDT and USDC. Crypto transfers do not incur foreign transaction or processing fees, and you can on- and off-ramp each stablecoin for less than a 1% conversion fee. Plus, for foreign businesses unable to open a business bank account in the U.S., Slash's Global USD account allows you to hold, send, and receive USD payments using crypto rails or bank transfer networks.³

Cross-border transactions: 5 key factors that influence costs and efficiency

Managing international payments requires understanding the complex ecosystem that determines how much you pay and how quickly your money moves. Here are the five factors that can impact your cross-border transaction costs and efficiency:

Banking networks and transaction processing

Correspondent and intermediary banking relationships uphold the network that facilitates traditional international payments. When you send money from your issuing bank to a recipient in another country, your payment often passes through a chain of correspondent banks that maintain relationships across borders. Each intermediary bank in this chain may deduct their own processing charges (intermediary bank fees), which can add up significantly as the processing becomes more complex.

The SWIFT network remains the dominant infrastructure for international wire transfers, connecting over 11,000 financial institutions worldwide. Slash leverages the SWIFT network to provide reliable international wire transfer capabilities, enabling businesses to reach merchant bank accounts in 180+ countries. While SWIFT transfers may take 3-5 business days and involve international wire transfer fees and bank charges along the payment chain, they remain a practical option for destinations where alternative payment rails aren't available.

Foreign exchange rates and currency conversion

Foreign exchange rates fluctuate constantly based on market conditions, but the rate you actually receive is typically not the mid-market rate. The mid-market rate(also called the interbank rate) is the midpoint between the buying and selling prices of two currencies in the global foreign exchange market. This is the "real" exchange rate you see on financial websites and news reports, representing what large institutions pay when trading currencies with each other. However, when you convert currency through your bank or payment processor, they can add a markup to this mid-market rate in the form of currency conversion fees and spreads.

Payment provider fee structures

International fee structures vary significantly across payment providers, from flat fees to percentage-based charges. Traditional banks can charge up to $40-50 per international wire transfer in international wire transfer fees regardless of the amount, plus currency conversion fees and markups can add another 3-5%.

Cryptocurrency transfers bypass traditional bank foreign transaction and processing fees, charging only a small conversion fee when moving between fiat currency and crypto. Slash's conversion fee, for instance, is just 0.5% for USDC. Plus, you can send international wires to 180+ countries for only $25—wire transfer costs far lower than other banks—or use the Slash Card for international purchases with just a 1% or $0.40 foreign transaction fee, reducing FX fees (fx fees) overall.

How to reduce cross-border fees: 4 strategies you need to know

Businesses no longer need to accept heavy cross-border and FX fees as a cost of doing business internationally. Modern alternatives to traditional banking systems unlock access to faster payment processing and cost-effective international payments that move money more efficiently and for less added cost. Here are some strategies to leverage these cost-saving opportunities.

Utilize cryptocurrency and stablecoins

Crypto rails offer a fundamentally different approach to international payments, capable of dramatically reducing costs and accelerating settlement times. Cryptocurrency bypasses the bank network infrastructure by settling transactions directly on the blockchain, eliminating the middlemen and their associated charges. Stablecoins are particularly powerful for business payments because they eliminate the volatility associated with exchange-traded cryptocurrencies. By pegging their value to fiat currency (typically USD), stablecoins like USDC, USDT, and USDSL maintain stable value while providing all the benefits of blockchain technology.³

With Slash, you can send and accept payments in USDT and USDC across 8 supported blockchains, giving you the flexibility to choose the optimal network based on speed, cost, and your counterparty's preferences. On-ramping and off-ramping between traditional currency and cryptocurrency come at a fee of less than 1%, often much lower than the currency conversion fees charged by institutional banks, and transfers on the blockchain can settle in a matter of minutes, not days.

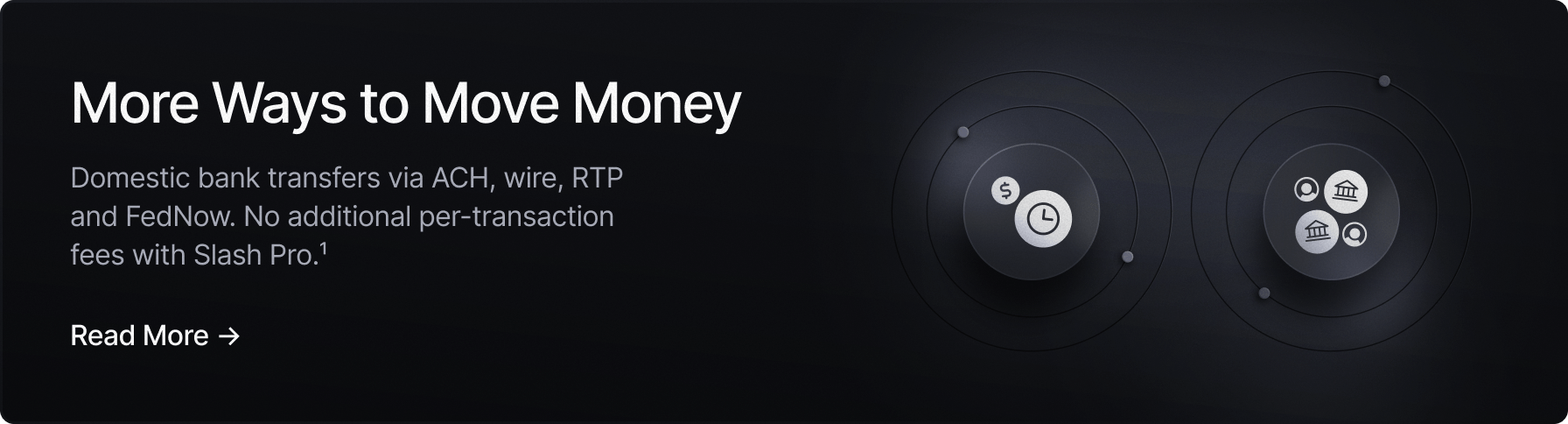

Leverage multiple payment methods

Access to a variety of different payment methods grants flexibility when you need a low-cost or quick transfer. Global ACH transfers originate from U.S. automated clearing house networks connected to your issuing bank and settle on foreign equivalents like SEPA (European Union), BACS (United Kingdom), or BECS (Australia). These transfers can be a low-cost bank transfer option with ACH payment fees typically under 1%, but may take several business days to complete. Wire transfers via the SWIFT network generally process faster than ACH, though they come with higher foreign transaction fees—sometimes $40--50 plus any intermediary bank charges and currency conversion markups.

Opt for a low-fee corporate card

If you or your employees frequently make purchases overseas, you may be paying far more than necessary to cover foreign transaction fees. Many credit cards charge fees in excess of 3% on all international purchases, but low-fee alternatives are available.

The Slash Visa® Platinum Card charges only a 1% foreign transaction fee or $0.40 on international transactions. Beyond the lower fees, the Slash card provides comprehensive spend management capabilities that are particularly valuable for businesses with international operations. You can issue unlimited physical and virtual cards from within the dashboard, group cards and controls by team, set individual spending limits for each employee, and more.

Start optimizing your global payments with Slash

Cross-border fees don't have to be an unavoidable cost of doing business internationally. Understanding the factors that drive international payment costs can empower your business to make smarter decisions about how to move money across borders. Whether you're dealing with traditional wire transfers, credit card transactions, or exploring cryptocurrency alternatives, the right payment infrastructure can save thousands of dollars annually while dramatically improving transaction speed and transparency.

Slash provides a comprehensive solution designed specifically to address the pain points of international payments. With access to multiple payment rails including cost-effective Global ACH transfers, reliable SWIFT wires to 180+ countries in 135+ currencies, and cutting-edge cryptocurrency capabilities across 8 blockchains, you can choose the optimal method for each transaction.

Combined with Slash's complete suite of banking and payment solutions, you can optimize payments around the world or streamline operations in-office. Here's what else Slash has to offer:

- Native cryptocurrency support: On-ramp and off-ramp with USDC, USDT, and USDSL at conversion fees under 1%. Send and receive stablecoins across 8 supported blockchains for settlement in minutes instead of days.

- Recurring and scheduled payments: Automate regular vendor payments, subscriptions, and retainers without manual intervention for consistent timing and reduced administrative burden.

- Slash Visa® Platinum Card: Issue unlimited physical and virtual cards, group cards by team, set individual spending limits, and prevent spending in unapproved categories—all with only 1% or $0.40 FX fees and up to 2% cashback (in the U.S.).

- Real-time analytics dashboard: Track company expenses and cash flow as they happen, with detailed breakdowns by payment method, contact, recipient, and currency to identify optimization opportunities.

- Global USD Account: Enables non-U.S. business entities to access Slash's full payment and crypto rails without requiring a U.S.-registered LLC, making efficient USD-denominated payments accessible worldwide.

Get started with Slash today and discover how much you can save on your global transactions.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What are cross-border processing fees?

Cross-border processing fees are charges applied by payment networks and financial institutions when processing transactions between parties in different countries. They are a form of international payment fees. These fees apply to credit card transactions on networks like Visa and Mastercard and on payments from banks and payment providers.

Interchange Fees Explained: What They Are and When They Appear

Do cross-border fees apply to cryptocurrency transactions or stablecoins?

Cryptocurrency transactions bypass traditional cross-border fee structures because they settle directly on blockchain networks. While you'll pay a small conversion fee when converting between traditional currency and crypto (called on/off ramping), the blockchain transfer itself costs nothing. Using Slash to send stablecoins like USDC and USDT can be particularly cost-effective for international payments.

Stablecoin Transaction Fees: A Complete Guide for Businesses

How are intermediary banks and correspondent banks different?

Correspondent banks are financial institutions that have established direct relationships to facilitate international transactions on behalf of other banks, while intermediary banks are any banks that sit in the middle of a payment chain between the sender and recipient.

Tracking Cross-Border Payments: Sending Money Overseas

Read more from us