Tracking Cross-Border Payments: What Businesses Need to Know to Streamline Global Payments

Sending a payment overseas—often grouped under international money transfers—is a bit more complex than sending one domestically. For businesses sending money overseas, a common concern is whether the money will arrive on time. When payments are delayed, products can be held up, vendor relationships can feel strained, and cash flow can get tighter than expected. So how can businesses keep a closer eye on their cross-border payments using clear payment tracking methods while they're in transit?

There's no one-size-fits-all way to track international transfers. Different payment methods rely on different systems, move at different speeds, and offer varying levels of visibility along the way. In this guide, we'll break down how to track the most common cross-border B2B payment methods, including international wire transfers, global ACH transfers, and cryptocurrency transactions. Along with practical ways to shorten timelines and avoid common delays.

In the current landscape, businesses are in need of fast and cost-effective cross-border payment platforms. This is where modern unified banking platforms like us come in and help you send, receive, and manage international payments.¹ With Slash, your business can access all the payment rails you need in one place, alongside fast payment options that many providers don't support, like native cryptocurrency support, advanced low-fee corporate cards, and USD payment access worldwide through the Slash Global USD account.³ ⁴

Leveraging unified banking systems, like Slash, empowers your business to track cross-border payments seamlessly across multiple countries and currencies, ensuring timely transactions to enhance your global operations.

What are cross-border payments, and how do they work?

A cross-border payment is any financial transaction in which the sender and recipient are located in different countries. These payments can take many forms, including international bank transfers, cryptocurrency transactions, credit card payments, and more.

The global cross-border payments market has experienced exponential growth in recent years. As reported by FXC Intelligence, the global cross-border payments market reached $195 trillion in 2025 and is expected to reach $320 trillion by 2032. This trend is a direct reflection of the growing volume of international trade and demand for cross-border payment processing like international wire transfers, digital wallets, and cryptocurrency transactions.

When a business initiates a cross-border payment through traditional banking networks, several steps occur before funds reach the recipient. The payment provider must verify regulatory compliance in both jurisdictions, route funds through one or more financial institutions, and convert currency if needed. Each added step in the process can introduce additional cross-border transaction fees and processing time.

Alternative payment methods rely on different infrastructure, which changes how payments move and how they're tracked. Cryptocurrency transactions settle on the blockchain, bypassing banking networks altogether. Digital wallets operate on closed networks with internal settlement systems. Traditional methods like wires, ACH, or paper checks depend on banking rails and, in some cases, international mail. These structural differences directly affect cost, speed, and visibility.

The most common cross-border payment methods

Below, we take a closer look at the most widely used international payment methods, including details about how they're processed and what businesses should consider when choosing between them:

Global ACH transfers

Global ACH payments originate in the U.S. automated clearing house system and settle through a recipient country's equivalent clearing network. Examples include SEPA in the European Union, BACS in the United Kingdom, and BECS in Australia. Among banking transfers, Global ACH can be one of the most cost-effective international payment processing options. However, the trade-off for lower fees is extended processing time; settlements can take anywhere from a few business days to over one week to complete. These are sometimes referred to as global ach transfers in provider documentation.

International Wire Transfers

International wire transfers are often facilitated through the SWIFT network, which connects more than 11,000 financial institutions worldwide. Slash utilizes SWIFT for its wire transfers, enabling businesses to send wires to over 180 countries in 135+ different currencies. While wire transfers generally process faster than ACH, they often can come with higher fees to cover expedited payment processing. Foreign transaction fees, intermediary bank charges, and currency conversion costs can add up quickly, especially for smaller transfers.

Digital wallets and money transfer services

Digital wallets like PayPal and Wise move funds through closed-network rails, often offering faster delivery and lower fees for smaller transfers. These tools are commonly used for remittances, cross border remittance, and smaller international payments. For heavy B2B use, however, limitations may arise. Low transfer limits and reduced compliance measures can make digital wallets less suitable for high-value or more formalized B2B payments.

Physical payment methods

Sending paper checks or purchasing international money orders are highly accessible, but they are generally the least safe and slowest transfer methods available. Checks may be lost or stolen during transit, and money orders can take weeks or even months to arrive at their destination. Furthermore, tracking can be minimal or nonexistent, leaving businesses with incredibly limited visibility into whether funds will reach the intended recipient on time.

Blockchain and cryptocurrency transfers

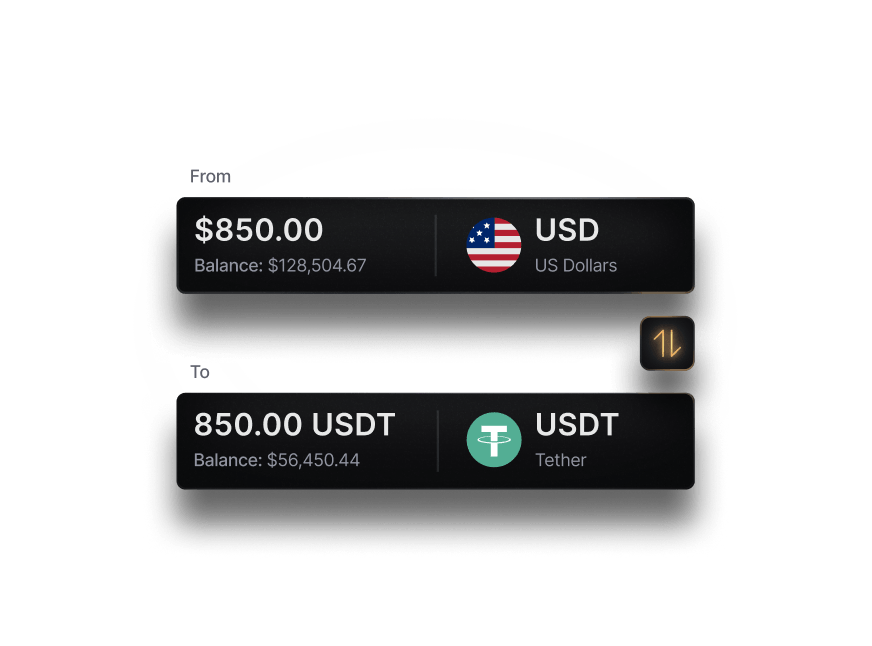

Blockchain-based payments are increasingly used in cross-border commerce due to faster settlement and lower infrastructure costs. These cryptocurrency transactions can settle in minutes rather than days, bypass traditional banking networks entirely, and can significantly reduce costs compared to conventional payment methods. Most cryptocurrency transfers only require a small conversion fee when converting between fiat currency and digital assets (which is called on-ramping and off-ramping).

Slash natively supports sending and receiving stablecoins like USDC and USDT, which are USD-denominated coins that can be on/off ramped into USD for less than a 1% conversion fee.

Credit card payments

Card networks such as Visa, Mastercard, and American Express operate globally, making them convenient for international travel expenses, subscriptions, and low recurring charges. For businesses, cards can simplify foreign spending without requiring separate payment workflows. Costs can often be the primary drawback.

Foreign transaction fees often average around 3%, along with additional merchant processing fees. The Slash Card offers a comparatively low foreign transaction fee of 1% or $0.40. In addition, the Slash Card comes with dynamic spend control features like configurable card groupings, customizable spend limits, and unlimited virtual card issuance.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

8 benefits and drawbacks of cross-border payments

Managing cross-border payments can add complexity, but they also offer meaningful benefits for growing businesses. Here are some of the advantages and disadvantages associated with conducting cross-border transactions:

Benefits

- Cost-savings opportunities: Working with overseas vendors can lower production or service costs. Choosing the right payment provider can further reduce fees and FX markups compared to traditional banks.

- Access to unique materials: Some materials, products, or specialized services are only available in specific regions. Cross-border payments enable businesses to work with the best suppliers globally, regardless of location.

- Expansion into global markets: Cross-border payments enable you to work with business partners around the globe, which can help you build relationships with new international customers, partners, and vendors.

- Management of foreign subsidiaries: Reliable payment systems can make it easier to send and receive payments from foreign subsidiaries, manage overseas payroll, and move capital across entities while maintaining accurate reporting across jurisdictions.

- Stronger vendor relationships: Reliable, timely international payments can strengthen business relationships. When you can consistently pay foreign vendors on time using their preferred payment method, you can build trust and may receive opportunities to negotiate better terms.

Drawbacks

- FX risk: Exchange rates fluctuate constantly based on market conditions, economic indicators, and geopolitical events. A payment initiated when rates are favorable might be processed days later at a less favorable rate, impacting the actual amount received.

- Cross-border transaction fees and hidden costs: Cross-border payments involve multiple layers of fees: processing fees, FX markups, intermediary charges, and recipient bank deductions can obscure the true cost of a payment. These fees can be opaque and difficult to predict, making it challenging to calculate the true cost of international transfers.

- Regulatory complexity: Cross-border payments must comply with AML rules, sanctions screening, due-diligence requirements such as KYC and KYB, and tax regulations across multiple jurisdictions. Slash follows applicable major international transfer regulations to help you avoid penalties, delayed transfers, or frozen accounts.

5 key issues that can slow down cross-border payments

Understanding what causes payment processing delays while international payments are processing can help businesses anticipate potential issues and choose payment methods that minimize disruptions. Here are the most common factors that may extend processing times for different payment methods:

Intermediate bank processing delays

When your bank doesn't have a direct relationship with the recipient's bank, funds must route through one or more intermediary banks. Each intermediary adds processing time and additional fees as they verify the transaction, check for compliance issues, and execute the next leg of the transfer. Intermediate processing delays primarily affect ACH and wire transfers.

Compliance and regulatory checks

Financial institutions must screen all international transfers against applicable sanctions lists, as well as perform transaction monitoring to identify potential fraud, money laundering, and sanctions violations. These compliance processes involve cross-referencing payment details against watchlists and verifying that transactions don't violate regulations in any involved jurisdiction. High-value transfers or payments to certain countries may require more in-depth screening, adding even more processing time while banks conduct additional reviews.

Bank processing cut-off times

Banks process international transfers in batches at specific times each day. If your payment misses the cut-off time, it won't be processed until the next business day. Cut-off times vary by institution and may be surprisingly early, sometimes in the late morning or early afternoon. Additionally, banks in different countries operate on different schedules and holidays, potentially adding several days if your payment is submitted before a long weekend in either country.

Limited infrastructure in emerging markets

Some regions may not participate in global payment networks like SWIFT, making transfers slower and more expensive. In these markets, correspondent banking relationships may be limited, requiring funds to route through more intermediaries. Additionally, adoption of crypto payment infrastructure is still evolving; some partnerships may limit your ability to leverage the benefits of blockchain-based payments.

Incomplete or incorrect payment information

Errors in payment details such as incorrect account numbers, missing SWIFT codes, incomplete recipient names, or wrong bank information can cause immediate delays. Financial institutions must halt processing to request corrections, and the back-and-forth communication can add days or even weeks to the transfer. Some errors may result in payments being returned to the sender, requiring the entire process to start over with correct information.

How to track cross-border payments: Step-by-step guide

How you track an international payment depends on which payment method you used. Below, we break down some standard payment tracking methods for major payment types:

Tracking global ACH transfers

- Obtain your transaction reference number from your payment provider when initiating the transfer.

- Search for the transfer in your banking portal using the reference number or date range for the transaction.

- Check the transaction status, which typically shows stages like 'Initiated,' 'Processing,' 'Sent to Recipient Bank,' and 'Completed.' Some banks may provide estimated delivery dates based on the destination country.

- Wait for the transaction status to update as 'Completed.'If the recipient has not received payment after the expected settlement date, reach out to your banking provider.

Tracking international wires via SWIFT

- Request a SWIFT UETR number when initiating a wire transfer. This 36-character code is used to uniquely identify your payment in the global banking network.

- Enter the UETR number into your bank's tracker, the SWIFT GPI Tracker service, or the online SWIFT Basic Tracker for real-time status updates.

- Contact your bank's wire transfer department if tracking shows unexpected delays or if the payment appears stuck at an intermediary bank. They can initiate traces and communicate directly with other banks in the payment chain to resolve issues.

Tracking cryptocurrency transfers

- Save the transaction hash (TxID) provided when you initiate the crypto transfer. This string is a unique identifier for your transaction on the blockchain.

- Visit a blockchain explorer website appropriate for the blockchain you used to send the payment (such as Etherscan for Ethereum or Solscan for Solana). Enter the transaction hash into the search field.

- Most crypto payments are considered final after a certain number of network confirmations. This depends on the blockchain used and the type of asset sent, but usual confirmation counts can be found with a quick online search.

- Verify receipt with the payee once confirmations are complete. Since crypto transactions can settle in minutes, tracking may not be necessary beyond verifying that the transaction appears on the blockchain. If the recipient doesn't see the funds within an hour, there may be an issue with their wallet or the recipient address.

Money orders

- Request a receipt with a serial number when purchasing the money order.

- Contact the issuing provider with this serial number to check if the money order has been cashed. However, this only confirms whether funds have been claimed, not whether they're en route to the recipient.

- Once the issuer confirms that the money order has been cashed, confirm with the intended recipient that the payment was received.

Additional payment methods, like mailed checks or digital wallet services, have a wide range of different tracking methods depending on your service provider. In general, if a payment does not reach your intended recipient within a reasonable amount of time, you should contact your payment provider to receive details about locating your payment.

Start optimizing your global payments today with Slash

When your global ACH transfers are tracked through one bank portal, your cryptocurrency transactions through a separate crypto exchange, and your international wire transfers through another banking interface, maintaining a comprehensive view of all outstanding payments can be unnecessarily complicated.

Slash removes this fragmentation by offering a unified cross border payments platform where businesses can initiate, track, and manage all cross-border payments from a single dashboard. Whether you're sending an international wire, processing a crypto transfer, or executing a global ACH payment, everything moves through one system with consistent tracking and visibility. The result is less manual oversight, fewer gaps in reporting, and greater control over global cash flow. Additional Slash features that support international operations include:

- Slash Global USD: Enables foreign businesses to hold, send, and receive USD globally without requiring a U.S. bank account or LLC. Combine Slash's diverse payment rails and native crypto support to operate internationally with fewer barriers.

- Slash Visa Platinum Card: A corporate charge card with advanced spend controls, including configurable card groupings, unlimited virtual cards, and customizable limits. Businesses can also earn up to 2% cash back on U.S. purchases, delivering consistent value on everyday spending.

- Powerful integrations: Clean integration with QuickBooks can help finance teams work faster and with greater accuracy. Streamline your month-end close with automated workflows for expense reporting, tax preparation, reconciliation, and more using financial data from your Slash account.

- Invoice management: Rolling out now, Slash's invoice management tools help track outstanding payments, monitor invoice status, and accept multiple payment options—all using saved contact information directly from your Slash account.

Slash is the modern platform for global banking, combining real-time international payments with intelligent tools designed for growing businesses. Learn how Slash can simplify the way you send and manage payments today at slash.com.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What are the main types of cross-border payment methods?

Common options include global ACH transfers, international wire transfers, digital wallets, cryptocurrency payments, and credit cards. Platforms like Slash support multiple payment rails in one place, making it easier to choose the right method for each transaction.

International Business Payments: Methods, Fees, and Best Options

What to look for when choosing a payment provider?

Key factors include transparent fees, strong compliance coverage, reliable tracking, and support for multiple payment methods. Slash offers lower fees than many traditional banks and simplifies international payment management by centralizing initiation, tracking, and reporting.

Cross-Border Payments Guide: Choosing the Right Solutions

How long do cross-border payments typically take?

Settlement times vary widely depending on the method, ranging from minutes for crypto transfers to several business days for ACH or wire payments. Using modern platforms like Slash can help reduce delays and improve visibility into payment timelines.

According to Worldpay’s 2024 Global Payments Report, cross-border online purchases now account for ~18% of global e-commerce volume.

How Long Do International Payments Take? A Guide for Streamlining Global Operations