Receiving International Payments: The Best Methods for Global Businesses

There’s a lot you can do as a sender to optimize international payments, but it may feel like you have fewer levers to pull when you’re on the receiving end. Many businesses default to traditional wire transfers or rely on a small set of payment processors, and just accept the FX fees as unavoidable. These are only a subset of what’s available today, and your setup plays a major role in how efficiently you receive payments.

Advancements in payment infrastructure, including modern payment gateways, fintech platforms, and alternative rails, have expanded how businesses can receive international payments. These solutions can reduce settlement times, improve transparency, and help control costs. In this guide, we’ll break down the most effective ways to receive international payments, from traditional bank transfers to modern payment platforms and stablecoin-based methods.

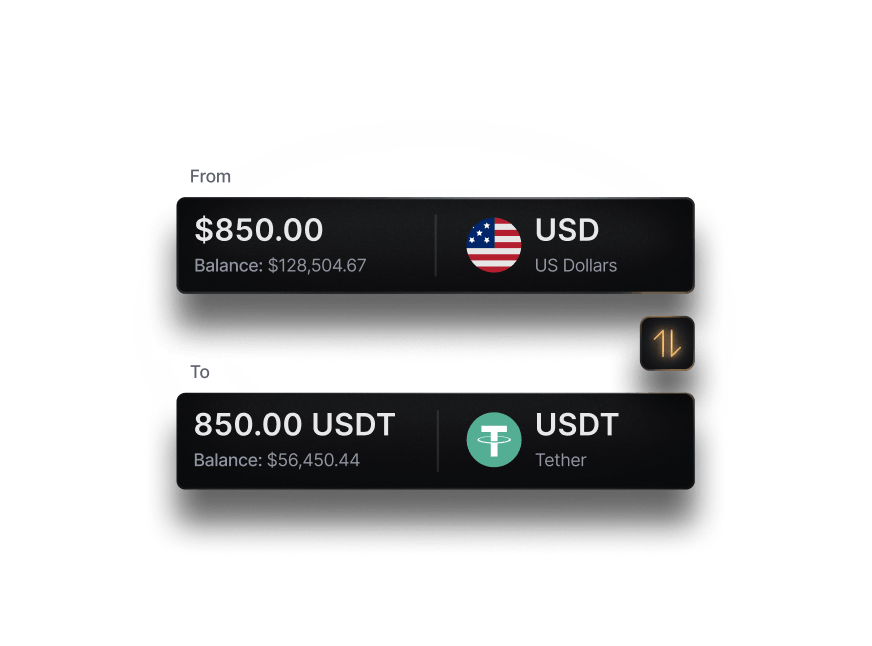

If your business operates globally, the provider you choose plays a major role in how quickly and efficiently you get paid. Slash brings international payment rails, powerful accounting tools, and native crypto support together in a single platform, so you can streamline how your business receives funds end-to-end.¹, ⁴ You can send international wires over the SWIFT network to more than 180 countries in over 135 currencies, leverage global ACH settlement, and move funds with stablecoins like USDC and USDT for faster settlement. You can also connect Slash to your preferred payment processors, giving your customers flexible ways to pay while helping you stay in control of how funds are received.

How International Payments Work

If you’ve worked with international payments before, you know they typically take longer and cost more than domestic transactions. This comes down to how the global banking system is structured. Each country operates its own banking infrastructure; when funds move across borders, they often pass through multiple institutions. Along the way, payments may be validated, routed between banks, and converted into different currencies, all of which can add time and introduce fees.

In some cases, countries with strong financial ties, such as the U.S. and U.K., have more direct banking relationships that help streamline cross-border transactions. Large banks may hold accounts with one another, which allows payments to move more directly between institutions. However, these direct relationships do not exist between every bank globally, which is where correspondent banks come into play.

A correspondent bank facilitates a transaction between two banks that do not have a direct relationship. Depending on the payment route, funds may pass through one or more correspondent banks before reaching the recipient’s bank. At each step, the payment is routed and validated, and fees may be deducted along the way. This process is typically coordinated over the SWIFT network, a global interbank messaging system that connects more than 11,000 financial institutions.

Outside of traditional bank transfers, there are a few ways to reduce reliance on the global banking system and potentially improve speed and cost:

- Cryptocurrency & the blockchain: Blockchain networks enable transactions to be sent directly between digital wallets without relying on intermediary banks. While often associated with cryptocurrencies like bitcoin, stablecoins such as USDC and USDT are commonly used for payments because they are designed to maintain a stable value relative to fiat currencies like the U.S. dollar. These transactions can settle in minutes and often have lower fees than international wires.

- Closed-network digital rails: Digital wallet providers such as PayPal or Wise process cross-border payments within their own networks. This can reduce settlement times compared to traditional bank transfers, though fees and foreign exchange costs vary by provider. Furthermore, not all platforms are designed for full-scale business payment operations.

Who pays for currency conversion?

In international payments, currency conversion costs do not always fall cleanly on the sender or the recipient. It depends on how the payment is sent and which currency is used.

If the sender converts funds before sending, for example from euros to dollars, they typically pay the foreign exchange cost upfront. However, if a payment is sent in a foreign currency and your bank or payment provider converts it upon arrival, the cost is effectively passed to you through the exchange rate spread or conversion fee.

With payment processors, currency conversion is handled automatically when the customer pays in a different currency than your pricing. The processor applies its own exchange rate and charges a foreign exchange fee, typically as a percentage on top of standard transaction fees. This cost is usually deducted from your payout rather than charged separately to the customer, so the recipient ends up absorbing the impact unless pricing is adjusted to account for it.

How to Receive Payments from International Clients: Common Methods

Businesses today have more options than ever when it comes to receiving international payments. The challenge is understanding how each method works and choosing the right mix based on cost, settlement speed, and how your customers prefer to pay. Here are some of the most common methods used today:

International wire transfers (SWIFT)

Wire transfers over the SWIFT network are one of the most widely used methods for receiving international payments. Your client sends funds from their bank, which are routed to your bank, sometimes through intermediary institutions. This method is reliable and supports a wide range of currencies, but it can come with higher fees, slower settlement times, and limited visibility into deductions along the way.

Global ACH and local bank transfers

In some regions, international payments can be routed through local bank networks, often referred to as global ACH. These transfers typically cost less than wires and can be faster when both banks support the same regional system. However, availability depends on the countries and currencies involved, and not all businesses or banks support these rails.

Payment processors and gateways

Payment processors like Stripe, PayPal, or Adyen allow businesses to accept international payments through cards, bank debits, and digital wallets. These platforms handle currency conversion and settlement, making them easy to integrate into checkout flows. While convenient, they often charge their own processing and FX fees, and funds may take a few days to settle into your account.

Multi-currency accounts

Multi-currency accounts let you receive, hold, and manage funds in different currencies without immediately converting them, which can reduce unnecessary FX conversions and give you more control over timing. However, they add accounting complexity, as you need to track balances, revaluations, and gains or losses across currencies, and they expose you to FX risk since exchange rate movements can reduce the value of funds before conversion.

Stablecoin and cryptocurrency payments

Some businesses accept payments in cryptocurrency through dedicated crypto payment processors embedded in their checkout flow. These payments can settle quickly and bypass traditional banking intermediaries, which may reduce costs and delays. Stablecoins like USDC and USDT are commonly used for this purpose since they are designed to track the value of the U.S. dollar, making them more practical for commerce than more volatile cryptocurrencies.

If you choose to accept stablecoins at checkout, Slash natively supports on- and off-ramps for USDC and USDT. This allows you to receive funds in crypto, convert to dollars when needed, and manage both fiat and digital assets within the same account without relying on separate providers.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

What Affects How You Receive International Payments?

If you’ve ever received an international payment that took longer than expected or arrived short of the original amount, you’ve seen how variable these transactions can be. Those differences aren’t random; they’re driven by how the payment is structured and processed. Here are some of the variables that can impact how you ultimately receive a payment from overseas:

- Payment methods used: The way a sender chooses to send money, whether through international wire transfers, bank transfers, debit or card payments, or an online payment gateway like Stripe or PayPal, directly impacts how you receive payments, including speed, fees, and settlement.

- Exchange rates and currency conversion: When accepting payments in a foreign currency, exchange rates and foreign exchange spreads determine how much you ultimately receive in dollars. Timing and provider rates can significantly affect the final amount after currency conversion.

- Payment provider and processing setup: Your payment processor or bank plays a major role in global payment outcomes. Different providers offer varying payment options, transaction fees, and payment processing speeds for cross-border transactions.

- Banking relationships: If your bank and the sender’s bank do not have a direct relationship, an intermediary bank may be required to complete the international transfer. Each intermediary can add fees and processing time.

- Recipient account setup: Whether you’re using a standard bank account, a multicurrency account, or a local bank setup in different countries affects how easily you can accept and hold foreign currency.

- Transaction fees and hidden costs: International payments often incur multiple layers of fees, including wire transfer fees, payment gateway charges, intermediary bank deductions, and foreign exchange costs.

- Country and regulatory factors: Cross-border payments are subject to regulatory requirements that vary by country. These rules can affect how payments are processed, what information is required, and how long a transaction takes.

Challenges Businesses Face When Receiving International Payments

Getting paid internationally isn’t just about receiving funds, it’s about managing everything that comes with it. Payments can take longer, cost more, and be harder to track than domestic transactions. Knowing what to expect can help you choose a setup that works more reliably for your business;

- High transaction fees: International payments often include multiple layers of fees, from wire transfer and payment processing charges to deductions by intermediary banks, which can reduce the total amount received.

- Unpredictable exchange rates: Changes in foreign exchange rates can impact how much you receive after currency conversion, especially if there’s a delay between when a payment is sent and when it settles.

- Slow settlement times: Cross-border payments, particularly international wire transfers, can take several business days due to intermediary banks, time zones, and banking cut-off times.

- Reconciliation and accounting challenges: Matching incoming payments to invoices can be more difficult with international transactions, especially when fees are deducted mid-transfer or when amounts are converted between currencies.

How to Choose the Right Setup to Receive International Payments

The best way to choose a setup is to start by evaluating how your business actually gets paid. These questions will help you evaluate your needs and narrow down the providers and features that make the most sense:

How often do you receive international payments?

The volume and frequency of your transactions should shape your setup. Businesses receiving frequent or high-volume payments can benefit from optimized rails, negotiated fees, or dedicated payment infrastructure, while occasional payments may not justify more complex solutions.

Which countries are you operating in?

The countries you work with determine what payment methods are available and how efficiently funds can move. Some regions support faster local bank transfers or global ACH, while others rely more heavily on international wire transfers and intermediary banks.

What currencies do you need to support?

If you regularly receive payments in multiple currencies, a multicurrency setup can help you avoid unnecessary conversions and manage foreign exchange more strategically. If not, it may be simpler to standardize on a single currency like USD.

How will this integrate with your accounting systems?

Your payment setup should align with how you track and reconcile transactions. Some payment processors and banking platforms integrate directly with accounting tools, which can reduce manual work and improve visibility across international payments.

How do you prioritize speed vs. cost?

Different payment methods offer different trade-offs. International wire transfers are widely supported but can be slower and more expensive, while alternatives like stablecoins may offer faster settlement or lower fees.

How do you invoice or request payments from clients?

The way you bill clients influences how they pay. If you rely on invoices, integrating payment links for bank transfers, cards, or payment gateways that connect with your banking stack can make it easier for clients to pay you internationally by reducing friction in the payment process.

Bringing International Payments into One System with Slash

At a high level, receiving international payments comes down to flexibility and control. You need to support the ways your customers prefer to pay, manage when and how currency conversion happens, and avoid unnecessary delays as funds move across borders. When those pieces are handled well, payments become more predictable and easier to manage.

The challenge is that many businesses don’t have a single system that can handle all of this. Payments might come in through a processor, settle into a bank account, and then require separate tools for reconciliation or currency management. Bringing these pieces together can make a meaningful difference in how efficiently your business operates.

Slash is designed to centralize that experience, giving you a single platform to manage international payments end to end:

- Send international wire transfers over the SWIFT network to 180+ countries in 135+ currencies.

- Send low-cost international ACH transfers through local clearing networks like SEPA, BACs, Zengin, and more.

- Hold, send, and receive USD-backed stablecoins like USDC and USDT, with built-in on- and off-ramps across networks like Ethereum, Solana, and Base.

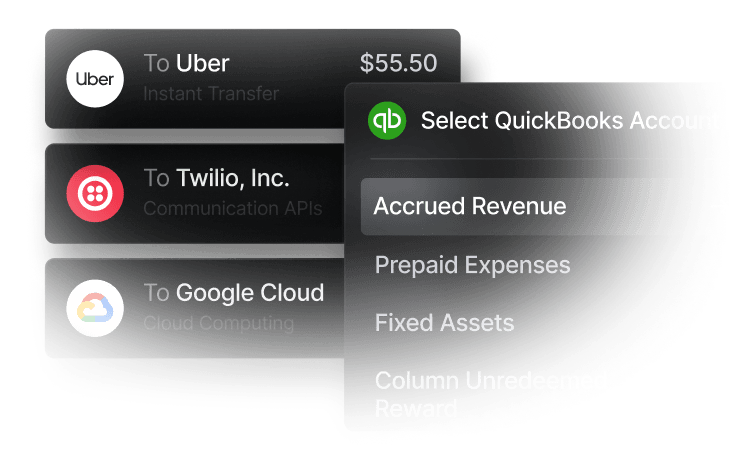

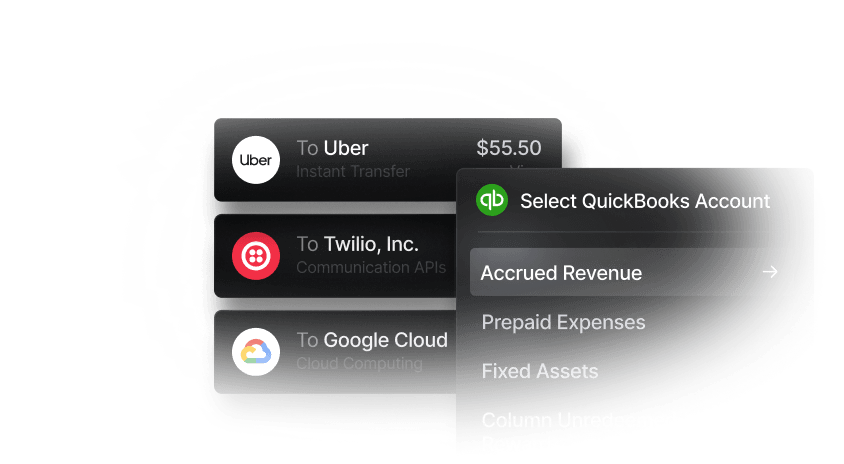

- Connect directly with accounting platforms like QuickBooks, Xero, and Sage Intacct to simplify reconciliation and reporting.

- Use Slash cards globally with a low 1% FX fee (minimum $0.40) anywhere Visa is accepted.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

What type of provider is usually the fastest for accepting payments globally?

Usually, card payments through an international payment processor are the fastest way to accept payments globally at the point of payment, because the customer can pay immediately online and the transaction is authorized in real time. Stablecoin payments can settle faster in actual fund movement, often within minutes, but they are only practical when both sides are set up to use crypto.

How to Receive International Payments: Comparing Different Methods

Crypto Payment Processors: Compare Top Platforms for Businesses

Can you receive international payments in multiple currencies without converting them immediately?

If you use a multicurrency account, you can receive payments in foreign currency without immediate conversion. This gives you control over when to convert, but you also take on the risk that exchange rates may move against you before you do.

Discover How Multi-Currency Business Accounts Work: Benefits and Top Alternatives

Read more from us