Best Business Bank Account for International Payments in 2026

If your business frequently sends international transfers through a local bank, you may have run into a few common issues: high FX markups, international wire transfers that take days to settle, and fees that seem to multiply at every stage in the payment chain. The business account you opened on day one may not have been built for cross-border operations, and the cost of that mismatch can become harder to ignore as your international payment volume grows.

Choosing the right business bank account for international payments is not an easy decision. It's a decision that can directly affect your margins, vendor relationships, and how quickly your team can operate in global markets. That's why we're taking a detailed look at some of the best bank accounts for international payments in 2026; we'll break down what to look for in a business account and explain why fintech platforms have become the default for businesses that move money internationally on a regular basis.

We will also show how Slash can support your global payment strategy, with access to global ACH, wire transfers to 180+ countries, and faster, lower-cost transfers with cryptocurrency.¹, ⁴ Slash’s business banking platform combines accessible financial management with flexible cross-border payment capabilities, giving you the tools you need to move money quickly and securely across borders.

The best business bank accounts for international payments at a glance

Here is how the top options stack up:

Best business accounts for international payments

There is no single “best” account for every business. The right choice depends on how often you send international payments, which currencies you work with, and how much complexity your finance team can manage. Some providers focus on low-cost transfers, while others offer a more complete banking setup with payments, cards, and expense management in one place.

Below is a closer look at each option, including where it excels and where it falls short:

Slash

Ideal for: Growth-stage businesses that need full-featured banking, international payments, corporate cards, and more in one platform.

Pros:

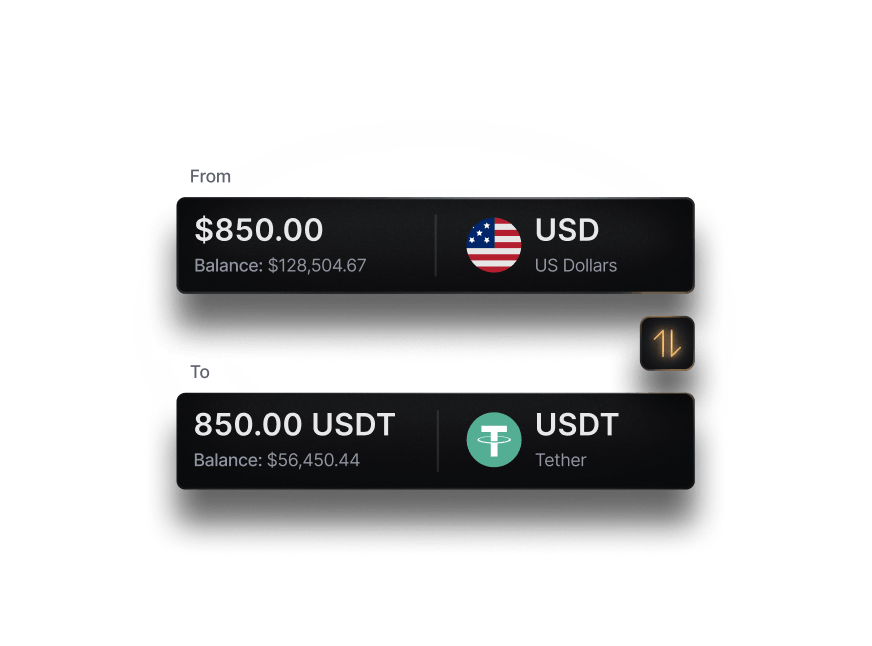

- Supports international wire transfers to 180+ countries in 35+ currencies, with native stablecoin payment rails (USDC and USDT) that can settle cross-border payments in minutes rather than days. This makes Slash a strong option for businesses that need to send money abroad quickly without relying on slow correspondent banking networks.

- FDIC coverage extends into the hundreds of millions through an insured cash sweep network via Column N.A., offering a level of deposit protection that most fintech competitors and traditional banks do not match.²

- Combines banking, card management, expense management, and treasury tools in a single platform, reducing the need to use separate providers for domestic and international financial operations.⁶ Businesses can issue unlimited virtual debit cards with configurable spending limits and controls, and all transactions sync in real time for cleaner reconciliation.

- Free plan available with no monthly commitment, giving businesses access to core banking and payment features without a subscription cost.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Airwallex

Ideal for: Mid-market international businesses that need global payment capabilities and integrated expense management.

Pros:

- Offers local account details in 20+ currencies (including USD, EUR, and GBP), allowing businesses to receive payments as though they had a local bank account in each market. This eliminates the need to open separate accounts at an international bank in every country where you operate.

- FX conversion rates start at 0.5% above interbank for major currencies, which represents meaningful savings compared to the 2–3% typical of traditional banks and most US banks.

Cons:

- Core expense management features such as approval workflows, ERP integrations, and automation are locked behind the Grow plan ($99/month), with multi-entity support reserved for custom-priced enterprise tiers.

- The free Explore plan requires a minimum $5,000 monthly deposit or $10,000 balance; businesses that fall below those thresholds are billed $29/month.

- SWIFT transfers incur fees of $15–$25 per transaction, and FX markups can reach 1–1.5% on less common currency pairs, which erodes cost savings at higher volumes.

Wise Business

Ideal for: Small businesses and freelancers that need to send frequent, low-cost international transfers without full-featured banking.

Pros:

- Uses the mid-market exchange rate with no markup, charging only a transparent currency conversion fee (typically starting around 0.33% for major currency routes) that is displayed before the transfer is confirmed. This transparency stands in contrast to traditional banks that embed hidden spreads in their exchange rates.

- Provides local account details in 10+ currencies (including USD, EUR, and GBP), allowing businesses to receive payments without cross-border fees in supported markets.

- No monthly subscription fee; businesses pay only for the features and transfers they use.

Cons:

- Not a full banking replacement. Wise Business does not offer lending, corporate cards with spend controls, invoicing tools, or advanced cash management, meaning businesses typically need to maintain a separate primary business account.

- SWIFT transfers carry additional flat fees (up to ~$26 depending on the corridor), and receiving USD wires costs a per-transaction fee, which can add up for businesses that regularly receive payments in dollars.

- Limited to payment and transfer functionality. Businesses that need integrated expense management, treasury tools, or working capital financing will need to layer additional providers on top of Wise.

- No support for check deposits or ATM access through dedicated ATM networks, which may matter for businesses that still handle some transactions in cash.

Payoneer

Ideal for: Businesses that receive payments from international marketplaces, freelance platforms, or overseas clients and need to consolidate those funds.

Pros:

- Well integrated with major marketplaces and freelance platforms, making Payoneer a solid choice for online sellers who receive international payments from abroad.

- Supports receiving funds in multiple currencies and provides local receiving accounts in several major markets, reducing wire fees for inbound transactions.

- Offers a working capital advance product for eligible businesses, which can help bridge cash flow gaps tied to international payment cycles.

Cons:

- Receiving funds via card or PayPal costs 3.99% plus $0.49 per transaction, and ACH debits carry a 1% fee, creating overhead for frequent inbound payments outside of marketplace integrations.

- Sending payments to recipients without a Payoneer account adds a 1–4% fee, reducing cost predictability for businesses that pay vendors or contractors outside the Payoneer network.

- No native support for stablecoins or crypto-based payment rails, meaning businesses remain fully exposed to foreign exchange volatility and traditional banking settlement timelines. The platform also lacks the depth of expense management or card issuance features found in more full-featured fintech accounts like Slash or Airwallex.

Revolut Business

Ideal for: Small teams with moderate international payment needs that want an all-in-one digital banking experience.

Pros:

- Offers interbank FX rates on currency exchanges within a monthly free allowance (the size of which depends on plan tier); can be a low-cost option for businesses with predictable, moderate foreign exchange volume.

- Supports global payments to 150+ countries and allows businesses to hold balances in 25+ currencies, including USD, EUR, and GBP.

- Includes business debit cards with spend tracking and team management features. ATM withdrawals are included with plan-dependent limits, though ATM fees apply beyond the free allowance.

Cons:

- US funds are FDIC-insured only up to $250,000 through a partner bank, and UK accounts lack FSCS protection entirely, which may concern businesses holding larger balances.

- Exchange and transfer limits depend on plan tier and are not clearly disclosed. Entry-level plans cap monthly FX volume, and exceeding the free allowance triggers a 0.4–0.6% markup, with a 1% surcharge on weekend exchanges.

- Feature availability varies significantly by region, particularly for US customers, making it difficult to evaluate the account without testing it in your specific market.

Fintech accounts vs. traditional banks: what's the difference?

Many US businesses default to using their existing bank to handle international payments. It seems like a reasonable choice: the relationship is already in place, the business account is active, and the bank supports international wire transfers. However, the cross-border payment infrastructure at many banks lags behind leading fintech alternatives, which can lead to higher costs and longer settlement times.

A typical international wire transfer through a US bank includes a flat sending fee, often $25 to $50, an FX markup on the exchange rate that may not be disclosed upfront, and potential intermediary bank charges that are deducted from the payment while it is in transit. The sender may not know the total cost of currency conversion until the transfer settles, and the recipient may receive less than expected.

In addition, many banks have not adopted newer payment rails such as cryptocurrency or built strong integrations with modern payment processors. This can limit how businesses send and receive funds, especially when working with partners that expect more flexible payment options. While banks continue to rely heavily on wires and correspondent networks, fintech platforms often support multiple rails within a single account, including local payment methods, wallet-based transfers, and stablecoin payments.

Why fintech-native accounts suit international-first businesses

The gap between fintech and traditional banking for international payments shows up in three areas:

- Pricing: fintech platforms generally offer tighter FX spreads and more transparent fee structures, whether that means mid-market rates with no markup (as with Wise Business) or clearly disclosed fees (as with Slash).

- Speed: Access to local payment rails and stablecoin-based transfers means cross-border payments can settle in minutes rather than days.

- Tooling: Integrated dashboards, real-time payment tracking, and automated reconciliation reduce the manual work that finance teams absorb when managing international payments through a bank portal that was designed primarily for domestic transactions.

None of this means traditional banks are unsuitable for every international payment. For businesses that send one or two international wire transfers per quarter, the cost difference may be marginal. But for companies where cross-border payments are a regular part of operations, the structural advantages of a purpose-built fintech account are hard to ignore.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What to look for in a business account for international payments

Choosing the right account comes down to a few practical factors that directly impact cost, speed, and day-to-day operations. Rather than relying on generic advice, it helps to evaluate each provider using a consistent set of questions. The criteria below are framed to help you do exactly that as you compare your options:

FX fees and exchange rates

The most significant cost driver for international payments is often the exchange rate, not the transfer fee. Some providers may advertise low or zero wire fees while embedding a large spread in the FX rate.

When evaluating business bank accounts, compare the rate you are offered against the mid-market rate at the time of the transaction. Even a 0.5% spread on a $50,000 payment represents $250 in additional cost, and those fees compound with every payment cycle.

Transfer speed and payment rails

Local payment rails (such as SEPA in Europe for EUR transfers or Faster Payments in the UK for GBP) typically settle same-day and cost less than SWIFT-routed international wire transfers. Look for providers like Slash with global ACH settlement, which allows you to send low-fee local transfers.

Providers that support stablecoin or crypto-based transfers offer an additional rail that can bypass traditional banking intermediaries entirely, settling in minutes regardless of the destination country. Speed matters not just for operational convenience but for managing foreign exchange risk: the longer a payment takes to settle, the more exposure your business has to currency fluctuation between initiation and delivery.

Card and expense management

Look for corporate cards with low or no foreign transaction fees, real-time transaction visibility, and configurable spending limits. These features can help control costs and give finance teams better oversight into transactions happening across different currencies and regions. The ability to issue virtual cards for specific projects can also simplify how your international expenses are managed.

The Slash Visa Platinum Card can be used worldwide anywhere Visa is accepted with a low 1% foreign transaction fee ($0.40 minimum). You can issue unlimited virtual cards to your team, adjust spending controls by region, and track all expenses in real-time from across the globe.

Integrations and API access

Handling payments across multiple currencies adds complexity when it comes time to close the books. Differences between expected and settled amounts, along with shifting exchange rates, can make reconciliation more time-consuming and harder to track as volume grows.

A business account that integrates directly with your accounting software helps reduce that friction. Look for native integrations with platforms like QuickBooks, Xero, or Sage Intacct that sync transaction data automatically, so your records reflect the correct amounts without manual cleanup at the end of each period.

Account protection

FDIC coverage can vary depending on how the account is structured, especially with fintech platforms that hold funds through partner banks. Some offer standard FDIC insurance up to applicable limits, while others extend coverage through sweep networks that distribute funds across multiple banks.

It is worth confirming where your funds are held, how coverage is applied, and whether your full balance is insured. For example, Slash provides FDIC coverage into the hundreds of millions through Column N.A.’s sweep network, while other providers like Revolut Business and Wise Business may offer more limited coverage depending on how accounts are set up.

Benefits of using a dedicated international business account

- Lower FX costs: Traditional banks often bundle FX markups with wire and intermediary bank fees, which can add up quickly. Many fintech platforms offer alternative payment rails that reduce or bypass these layers, helping lower total costs on international transfers.

- Faster settlement: International bank transfers can take several days to arrive. Modern platforms can reduce settlement times with access to cryptocurrency, which can be especially useful when paying vendors on tight timelines or acting on favorable exchange rates.

- Centralized visibility: Managing payments across multiple systems can make tracking international spend difficult. A dedicated account brings transactions into a single view, making it easier to monitor activity and reconcile accounts.

- Simplified accounting: With fewer systems to manage, finance teams spend less time resolving discrepancies and more time closing the books accurately and on schedule.

- Stronger vendor relationships: Paying the correct amount, on time, and in the expected currency builds trust with international partners and reduces back-and-forth over payment issues.

Is Slash the right account for your international payments?

International payments introduce a different set of constraints than domestic ones. Costs are less predictable, settlement times vary by method, and the way funds move can depend on where your counterparties are located and what they can accept. Over time, those variables start to shape how your finance team operates.

Having multiple payment options in one account can simplify that. Slash supports SWIFT transfers to 180+ countries in 35+ currencies, along with stablecoin payments like USDC and USDT. This gives you the flexibility to choose how you send money based on cost, speed, or what the recipient can accept. Access to USD banking can also be a limitation for international teams. Many providers require a US entity to open an account. Slash’s Global USD Account removes that requirement, making it easier to send, receive, and hold USD.³

At a certain point, the focus shifts from saving on fees to how your entire financial setup supports international operations. With Slash, you get more than just ways to move money. Here’s what else you get:

- Slash Visa® Platinum Card: Earn up to 2% cash back (U.S. only), set customizable spending controls and limits, and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more.

- Expense management: Streamline expense reporting with end-to-end SMS receipt collection for Slash cards, simple reimbursement flows, and automatic accounting updates.

- Accounting integrations: Connect Slash with QuickBooks, Xero, or Sage Intacct so your transaction data flows directly into your books, already categorized and ready for reconciliation.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury accounts: Earn up to 3.83% annualized yield on idle funds through money market investments from BlackRock and Morgan Stanley, managed directly in your Slash account.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What are the fees for international payments?

Slash charges $25 for SWIFT wire transfers and a 1% foreign transaction fee on international card payments. Stablecoin transfers use volume-based pricing, which can be more cost-effective for frequent cross-border payments.

Mastering Cross-Border Fees: Essential Insights and Strategies for Reducing International Payment Fees

Can I use Slash to pay international contractors?

Yes. You can pay contractors via international wire, global ACH, or stablecoin transfer, depending on speed and cost preferences.

How to Pay International Contractors in 2026

What is the difference between a wire transfer and a local transfer?

Wire transfers move funds across countries through bank networks and can take several days with added fees. Local transfers use domestic rails in the destination country, making them typically faster and cheaper.

ACH vs Wire Transfer: Key Differences, Costs, Limits & Use Cases

Do I need a separate account for each currency?

Not necessarily. Some providers offer multi-currency accounts, while others, like Slash, focus on USD and crypto rails to simplify operations while still supporting payments in 35+ currencies.

Discover How Multi-Currency Business Accounts Work: Benefits and Top Alternatives

Can I use Slash if my business is outside the US?

Yes. The Global USD Account allows non-US businesses to access USD banking and crypto payments without a US entity or bank account. Or, you can access Slash's full-featured platform if you have a qualifying U.S.-registered LLC.

Open a US Business Bank Account as a Non-Resident: Requirements and Benefits

Read more from us