A Guide to B2B Cross-Border Payments: What Your Business Needs to Know

Managing cross-border B2B payments can be harder than it looks. Each transfer often involves multiple currencies, banking networks, compliance frameworks, and time zones, all affecting whether payments arrive on time and at their expected cost. For scaling businesses that want to expand internationally, cross-border B2B payments are an equation that needs to be solved.

When finance teams and business owners understand how international payments work, they’ll be able to select cost-effective rails and accurately predict settlement timelines. This can improve vendor relationships, supply chain reliability, and the predictability of cash flow across the organization. On the other hand, unexpectedly long transfer times and surprise fees can interfere with budgeting and harm your organization’s trustworthiness in the eyes of suppliers.

This article covers the main types of international payment, the factors that affect speed and cost, common operational challenges, and practical ways to optimize how your business sends and receives money across borders. We’ll also take a look at Slash, a neobank that supports a wide range of international payment rails, including SWIFT transfers, global ACH payments, low-fee corporate cards, and more.¹

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What Are International B2B Payments?

International B2B payments are financial transactions between companies located in different nations, often coming in the form of purchases, invoices, and repatriations. These transactions are much different than cross-border consumer payments, which tend to be smaller, quicker, and pushed through mobile apps or international money orders.

B2B cross-border payments typically involve larger sums, more counterparties, additional documentation requirements, and exchange rate factors.. They’re the mechanism through which the world’s businesses purchase goods from international suppliers, pay overseas contractors, fund foreign subsidiaries, and more. Per Juniper Research, global B2B payments are projected to reach $124 trillion annually.

When managed efficiently, cross-border B2B payments offer benefits such as:

- Broader market access: Bringing your product or service to other countries unlocks an entirely new segment of customers, offering opportunities for extra profit and wider brand recognition.

- Stronger supplier relationships: Reliable, timely payments often build trust with international vendors and create the foundation for better terms and closer collaboration.

- Predictable cash flow management: Structured payment workflows with known timelines and costs make it possible for businesses to forecast their cash flow more accurately.

- Access to new materials or services: Some vendors may offer specialized products or services that are only found in specific regions. Cross-border payments enable businesses to work with any supplier globally and access niches they may not have in their home country.

Use Cases for B2B Cross-Border Payments

Companies may send and receive money across borders for a wide variety of reasons beyond buying and selling. Some of these use cases include:

- Supply chains and logistics: Companies that manufacture and source different materials often have to make cross-border payments for customs duties, port handling charges, and freight broker bills. Each payment in the chain can affect the overall speed of getting goods from origin to destination.

- Personnel and contractor payments: Paying the wages and benefits of foreign employees and contractors can become complex when they’re spread across multiple countries. These payments often involve specific currency requirements, remittance documentation, and tax withholding obligations.

- Operational purchases: Scaling companies often purchase goods and services from overseas vendors, even if they themselves aren't expanding globally. Whether sourcing inventory from China or contracting a development team from Poland, reliable cross-border payments keep operations running smoothly.

- Investments: Companies growing overseas may need to fund foreign subsidiaries, invest in new assets, or transfer capital to support operations abroad. A cross-border “investment” can also be the acquisition of a new company, which will entail plenty of financial transactions.

- Repatriation: In a business context, repatriation is the act of sending money back to one’s home country. Companies operating across borders routinely will often move profits earned from international subsidiaries back to their original entities.

Common Types of International B2B Payments

Companies have multiple options to weigh when deciding how to make financial transactions across borders. Let’s break down each of them to determine what payment rails make sense in what contexts:

Wire Transfers via the SWIFT Network

International wire transfers are often made through the SWIFT network, which connects more than 11,000 financial institutions across 200+ countries. SWIFT itself isn’t a payment rail, however – it’s a network that tells banks how to process payments.

When a business initiates an international wire transfer, SWIFT routes a secure payment message from the sending bank to the receiving bank. This message may travel directly or it may pass through one or more intermediary banks. Wire transfers are reliable and widely accepted, which makes them a common choice for large or high-stakes B2B payments. Transfers typically take one to five business days, and fees can range from $25-50. With SWIFT, the recipient’s bank may also charge an incoming wire fee of $10-20.

Virtual Payment Cards

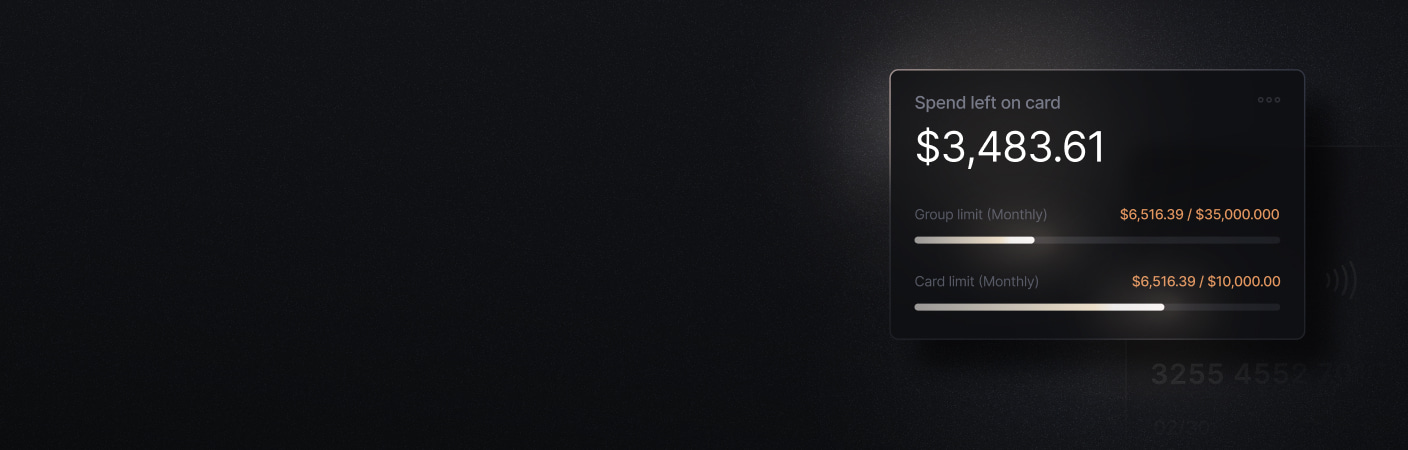

Virtual cards are individual corporate cards generated for specific transactions or spending categories. Each card typically carries a unique 16-digit number, spending limit, and expiration date. They can be especially useful for sending one-time payments to vendors or overseas hotels.

As these cards are often connected to an ERP or financial platform, they can offer an extra layer of control and visibility. Slash takes this a step further with the Slash Visa® Platinum Card, which comes with granular spending controls and real-time spending data and analytics. Your business also gets up to 2% cash back with every purchase.

International ACH Transfers

While many payment rails connect individual bank accounts, global ACH transfers send funds to the recipient country’s equivalent clearing network. These transfers are processed in batches rather than individually, which means the network can handle large volumes of requests quickly and efficiently. Global ACH payments can take anywhere from 1-5 business days to complete, and typically come with fees of around $5. However, not all U.S. banks support global ACH, so it’s important to determine whether your bank does and what your recipient’s bank offers.

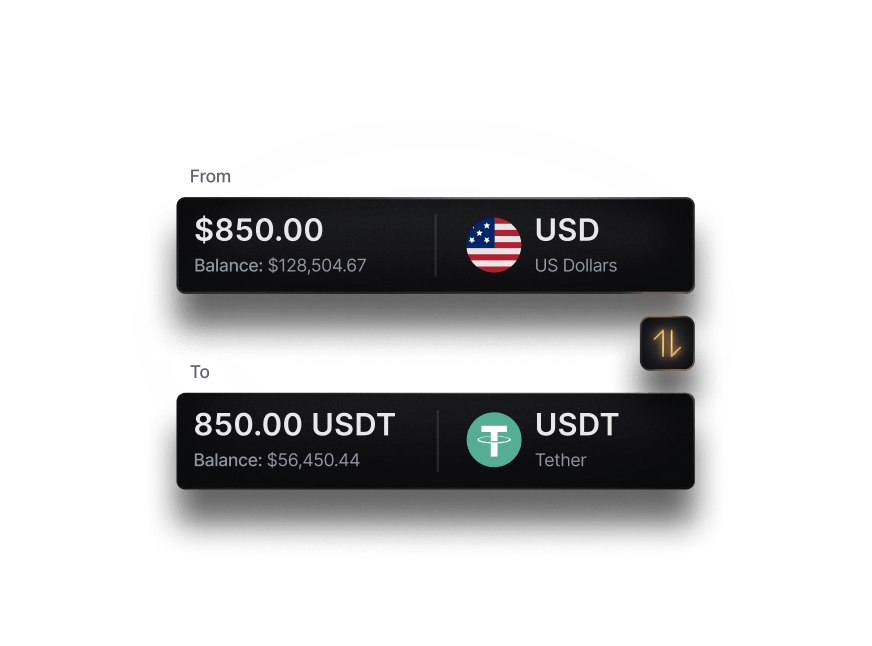

Cryptocurrency and Stablecoins

Cryptocurrencies are an emerging tool for cross-border B2B transactions, particularly for businesses operating in markets with limited banking infrastructure or high wire costs. These payments are often made with stablecoins, which are digital assets pegged to fiat currencies like the U.S. dollar. Some modern payment platforms like Slash have support for stablecoins like USDC and USDT.⁴ Slash makes it easier for businesses to work with crypto by offering built-in on/off ramps that convert it into your local currency.

Since stablecoins are linked to fiat currency, they don’t experience the volatility of tokens like Bitcoin or Ethereum. Compared to many traditional B2B payment methods, crypto transfers can settle much faster and may incur fees of less than 1% of the transaction value.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

International B2B Payment Challenges Companies Face

Depending on the payment rail companies choose, the location they’re sending to, and the currencies at play, companies may run into a number of obstacles when making cross-border transfers. Here are some of the most common:

Slow Speeds and Payment Processing Delays

Cross-border payments are famously sluggish, especially with traditional methods. SWIFT transfers and ACH payments can take up to five business days, and don’t offer visibility into overall progress. For businesses with supply chains that depend on predictable payment receipt, this volatility can be disruptive. A transaction delayed by several days can hold up customs clearances, interfere with manufacturing, or frustrate vendors.

Compliance and Laws

Every country has its own financial regulations meant to enforce security and guard against fraud. Payments may be held to AML (anti-money laundering) requirements, Know Your Business (KYB) verification procedures, and even counter-terrorism financing (CTF) standards. It can be difficult to keep track of all these guidelines, and as a result, innocent B2B transfers may trigger due diligence requirements that delay processing significantly. Failure to comply with applicable regulations can result in frozen transactions and/or legal penalties.

Costs and Bank Fees

Between initial fees and intermediary bank charges, international wire transfers can sometimes charge senders upwards of $50. Since not all of these costs are visible upfront, the recipient may end up with a slightly different amount than expected, which can create reconciliation problems. Businesses that prefer methods with lower fees have the option of utilizing global ACH, virtual cards, or stablecoins.

Foreign Exchange Rates

Many international transfers include an extra processing step for converting currencies. Currency conversion introduces foreign exchange (FX) risk for transfers that take multiple days to settle, as exchange rates can fluctuate during the multi-day journey. This means the value of the transfer when initiated may be different from the value upon settlement.

For example, a transfer to Rio de Janeiro might be initiated from the United States on a Wednesday when 1 Brazilian real (R$) equals $0.19 USD. If the payment takes several days to settle and the exchange rate moves to $0.21 by Saturday, the final converted amount will differ from what was expected at the time of sending. This fluctuation can lead to unpredictable costs or shortfalls, especially for larger payments.

Faster payment methods reduce this exposure by shortening the time between initiation and settlement. Cryptocurrency payments, which can settle in minutes, largely eliminate this timing gap, locking in value at the moment of transfer and minimizing the impact of exchange rate movements.

Best Practices for Efficient B2B Cross-Border Payments

While some of those challenges are just “part of the game” when it comes to international payments, others can be minimized with smart business practices. Here are a few tips:

- Consolidate global payments: Some teams make the mistake of managing workflows for different regions and currencies across several fragmented systems. Instead, it’s best to run international payments through a single solution to reduce the burden of extra coordination and reconciliation. Slash tracks SWIFT payments, ACH transfers, stablecoins, and virtual cards on the same platform, allowing for easy comparison and analysis.

- Verify vendor banking information: Incorrect bank account information and codes can cause payment failures and delays between business partners. When beginning a relationship with a supplier, it’s very important to make sure you transcribe their banking details correctly and double-check them before each transfer. It’s also wise to ask if they’re planning on switching banks or moving locations in the future, as you don’t want to be caught off guard by a change in information.

- Plan payments around time zones and banking schedules: Weekends, local holidays, or far-apart time zones can add multiple days to a transaction. You may think it’s all right to send a payment on a Thursday morning rather than a Wednesday afternoon, but that Thursday payment could stay pending through a long weekend with a foreign holiday you didn’t plan for.

- Keep clear records for reconciliation: Each cross-border payment should generate an audit trail that logs details like the amount sent, the fees deducted, the amount received, the exchange rate applied, and the date of settlement. This documentation helps maintain accurate financial reporting, resolve discrepancies with vendors, and satisfy compliance requirements.

- Use platforms that integrate with accounting systems: Businesses can organize their vendor payments and streamline their month-end close by connecting their banking processes with their accounting software. Platforms like Slash can pull invoice and vendor information directly from QuickBooks Online, Xero, and Sage Intacct. After payment is complete, Slash then pushes that updated information back to your accounting app, ensuring everything is aligned.

Upcoming Trends in International B2B Payments

The infrastructure that supports international payments is far from perfect, and new developments are constantly in the works to make these transfers faster, easier, and safer. Here are some trends we may see in the near future:

Cryptocurrency Adoption

Stablecoins are turning from a niche digital asset into a mainstream B2B payment tool; about $35 billion in stablecoins were sent and received in 2025 alone, according to Artemis Analytics. Because stablecoin transactions settle on blockchain networks, they can move faster and with greater transparency than traditional payment methods. Additionally, blockchains support smart contracts, which are self-executing contracts that automatically enforce agreements when predetermined conditions are met, such as terms agreed upon by buyers and sellers. Smart contracts are evolving in usage by the day, and may play a large part in future financial transactions.

AI and automation in compliance and fraud detection

AI can analyze existing financial data to detect unusual spending activity and make smarter authorization decisions on the spot. When it comes to international B2B payments, AI-powered screening tools can assess transactions against sanctions lists, flag suspicious patterns, and even produce compliance documentation. This reduces the manual burden on finance and legal teams while often improving the accuracy and speed of compliance review.

Real-time payment network expansion

Real-time payment networks are country-specific infrastructures that can carry funds to domestic recipients in less than a minute. These payments cannot travel internationally, and are almost exclusively limited to a nation’s own borders. However, that won’t always be the case – some countries are developing ways to connect their real-time networks with outside systems. In 2021, Singapore’s PayNow broke this barrier by linking with Thailand’s PromptPay. While this sort of progress hasn’t started among the two U.S. real-time networks, FedNow and the RTP network, overseas expansion has been named a long-term goal.

Manage Global Payments in One Place with Slash

Optimizing one B2B cross-border method can be tough on its own, but juggling several payment rails, vendors, timelines, and delays can be an immense challenge. Instead of adopting multiple solutions that cover specific parts of the international payment process, it’s better to choose one business banking platform that can handle it all independently.

Slash is a neobank that offers a unified platform allowing companies to initiate and track almost any method of payment from a single dashboard. Whether SWIFT transfer, ACH payment, or stablecoin, we enable businesses to select the payment rail of their choice based on timing needs and recipient requests. For those who prefer cards, businesses can make global purchases with the Slash Visa® Platinum Card, which incurs an FX fee of just 1% per transaction (min. $0.40).

For those who are ready to work with crypto, our platform supports dedicated on/off ramps for both USDT and USDC, allowing businesses to convert their digital token of choice into fiat currency with fees of less than 1% per transaction.

Here are some other Slash features that can help expanding businesses:

- Accounting software integrations: Slash integrates with QuickBooks Online, Xero, and Sage Intacct, helping finance teams work faster and with greater accuracy. Streamline your reconciliation with automated workflows for expense reporting, tax preparation, and more using financial data from your Slash account.

- Global USD accounts: With access to Slash’s Global USD account, founders in 130+ countries can hold dollar-based funds, send & receive ACH/wire, and make stablecoin payments without a U.S.-incorporated LLC.³

- Working capital financing: Slash users can choose between flexible 30, 60, or 90 day repayment terms, allowing their businesses to continue to scale while still supporting liquidity for daily operations.⁵

- Expense management features: Streamline your expense reporting with end-to-end SMS receipt collection for Slash cards, streamlined reimbursement flows, and automatic accounting updates.

Slash brings global payments into a single workflow, letting businesses send international transfers and manage vendor payouts across 180+ countries. Check out our platform if you’re interested in taking financial shortcuts across borders.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What risks should companies consider when sending large international payments, and how can they mitigate them?

Large international payments carry extra FX risk, as exchange rate fluctuations can change the value of a transfer significantly. Additionally, sizable transactions can warrant extra scrutiny due to AML frameworks and various regulations.

What is SEPA?

The Single Euro Payments Area (SEPA) is a European infrastructure that connects cross-border electronic euro payments between correspondent banking systems, making them as fast, secure, and easy as domestic transfers.

Do all traditional banks support SWIFT transfers and global ACH payments?

While over 11,000 banks around the world support SWIFT transfers, some smaller banks and credit unions may not. Global ACH payments are a bit more limited, as only certain U.S. financial institutions support the service. We recommend researching your current or prospective bank's capabilities.

What is a letter of credit?

A letter of credit is a financial document issued by a bank that guarantees a seller will receive payment on time and for the full amount, provided they meet specific delivery and documentation conditions. In the context of international B2B payments, they’re often used as a form of agreement between vendor and purchaser.

Read more from us