How to Maximize an Introductory Rate Offer: What Businesses Should Know

Many business owners may not realize that a 0% introductory rate offer is essentially a short-term, interest-free loan that also earns rewards. Buy $20,000 in inventory, pay it down over 12 months, pocket the rewards, and owe nothing in interest. It's one of the better financing tools available to small businesses, but it’s not exactly foolproof.

Like everything related to credit cards, the benefits are there if the card is used and paid down responsibly; put off paying down your balance, however, and the offer can start working against you. The promotional window for an introductory offer has a hard end date, and the rate waiting on the other side is often an APR of 20% or higher. Fail to bring your balance down to $0 by that date, and the interest can start eating away at everything you saved.

For businesses that want a card built for more than just strategic spend timing, the Slash Visa Platinum Card earns up to 2% cash back and connects directly to QuickBooks, Xero, NetSuite, and other accounting platforms.¹ Finance teams get granular controls over every card issued, with spend limits, merchant restrictions, and real-time visibility across the whole team. Receipt matching, expense tracking, and multi-entity support are all built in. Continue reading to learn more.

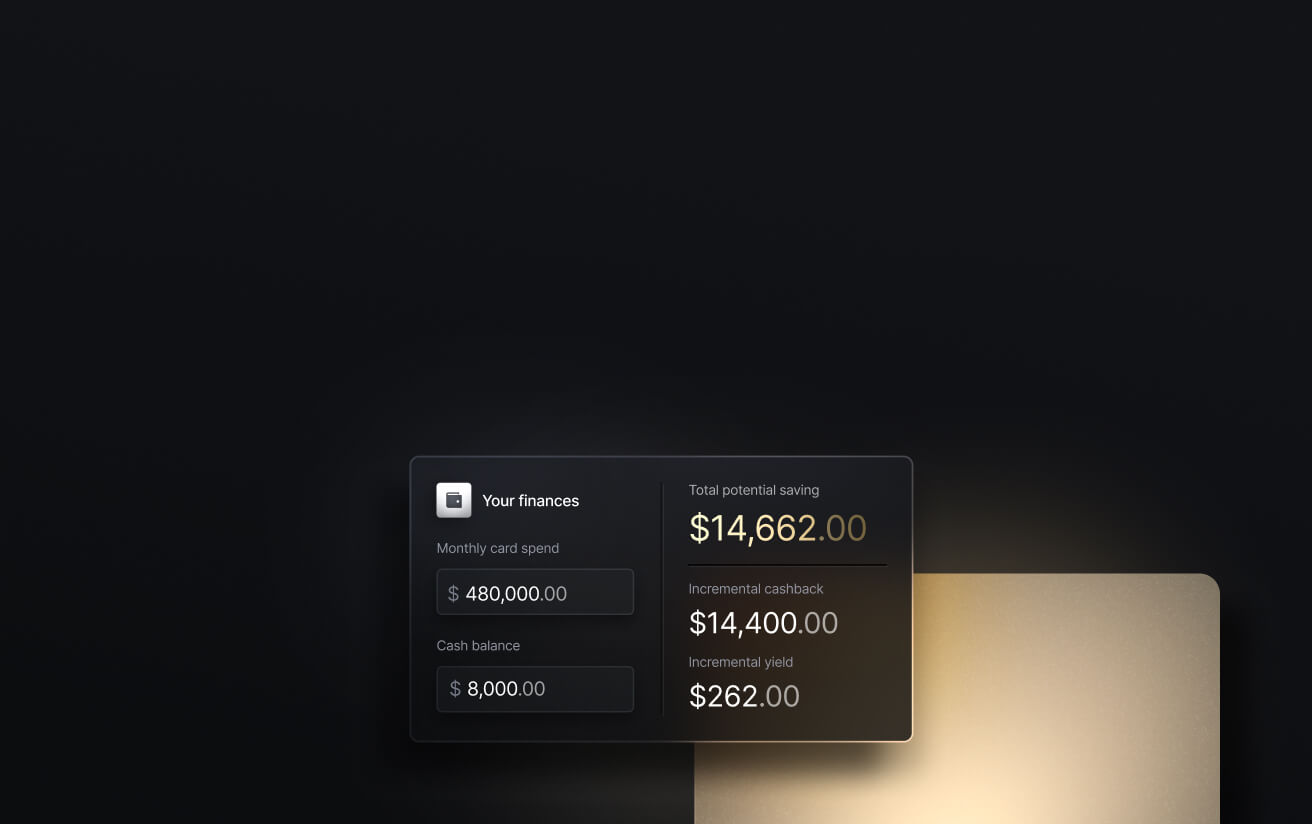

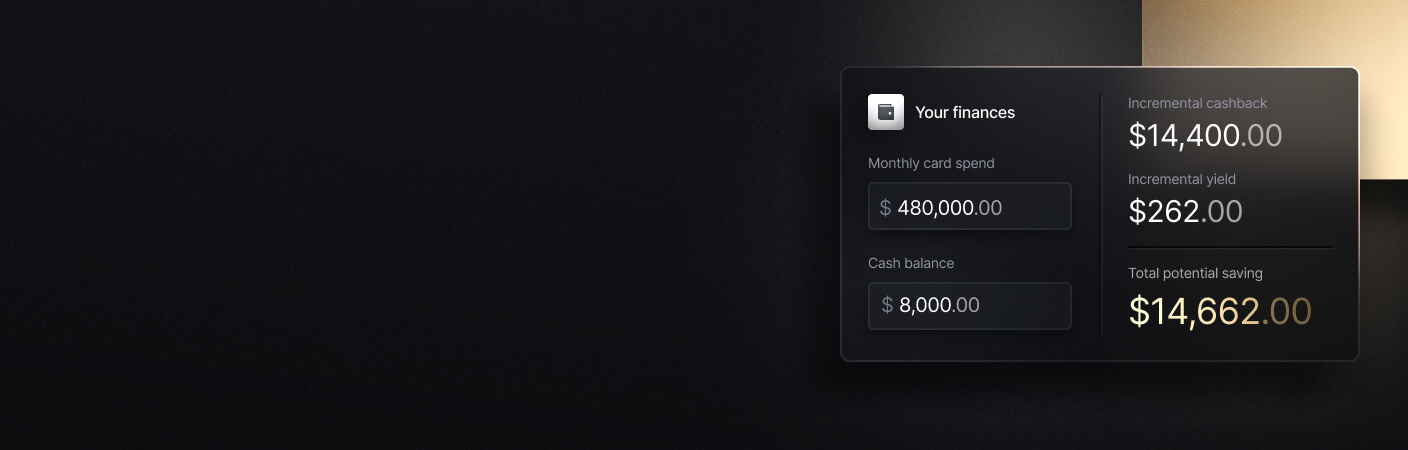

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What is an introductory rate on a credit card?

APR, or annual percentage rate, is the yearly cost of borrowing on a credit card, expressed as a percentage. When you carry a balance from one billing cycle to the next, the issuer charges interest based on that rate. A card with a 20% APR costs you 20% of your outstanding balance per year in interest, calculated daily and billed monthly.

An introductory rate is a temporarily reduced APR, often 0%, that a card issuer offers for a set period after you open an account. During that window, you pay little or no interest on eligible balances. Once the introductory period ends, the standard variable APR kicks in on any remaining balance and on new purchases going forward.

To make this concrete: a card might advertise 0% intro APR for 12 months on purchases, then 19.99% variable APR after that. If you put $10,000 on the card during those 12 months and pay it all off before the promotional period ends, you pay zero interest. If you still owe $4,000 when month 13 starts, that balance begins accruing interest at 19.99%.

Introductory rates apply in a few different forms:

- The most common is an intro APR on purchases, which lets new charges accumulate without interest during the promo period.

- Balance transfer introductory rates apply a low or zero rate to balances you move over from another card.

- Cash advance intro rates are rare, and most cards exclude cash advances from any promotional offer entirely.

For business owners, an introductory APR is a useful short-term tool for managing cash flow during a specific project or growth phase, not a substitute for a longer-term financing strategy.

How long does an introductory rate period typically last?

Introductory APR periods are bounded by both federal rules and card issuer policy. Under the CARD Act, issuers are required to offer introductory periods of at least six months on new accounts. Beyond that floor, the length varies significantly depending on the card and whether it targets consumers or businesses.

Consumer cards tend to offer longer promotional windows, often in the 12 to 21 month range at 0% APR. Business credit cards typically fall in a shorter range, from 6 to 12 billing cycles, though some issuers offer more. The promotional period is stated in the card's terms and conditions and usually starts from the date the account is opened, not the date of your first purchase.

One important caveat: issuers can revoke the introductory rate if you are more than 60 days late on a payment or violate the card's terms. If that happens, the standard variable APR applies to your balance immediately, and you may also face a penalty APR that is higher than the standard rate.

What types of transactions does an introductory rate apply to?

Not all transactions carry the same APR, even during a promotional period. Most card disclosures list purchase APR, balance transfer APR, and cash advance APR as three separate rates, and an introductory offer may cover only one of them. Assuming an intro rate applies to everything on the card can end up being a costly mistake. Here’s what to know:

- Intro APR on purchases: Covers new charges you make to the card during the promotional window. This is the most direct application for businesses: a planned equipment purchase, marketing campaign spend, or a new software plan can be charged to the card and paid off in installments over the intro window without accruing interest costs.

- Balance transfer introductory rates: Lets you move existing balances from other cards to the new card at a low or 0% rate. This can reduce the cost of carrying debt that was already accruing interest at a higher rate elsewhere. Most balance transfer offers charge a one-time fee of 3% to 5% of the transferred amount, which reduces the savings but is often still worth it compared to paying 20% or more in ongoing interest.

- Cash advances: Almost always excluded from intro offers. When you take a cash advance, the higher cash advance APR (often 25% or more) typically applies from the day of the transaction, with no grace period. This applies even if your card has an active 0% purchase intro rate. Card disclosures will specify this separately.

Before relying on an introductory offer for any part of your financing plan, read the full card terms carefully to confirm which transaction types are covered. The headline "0% intro APR" in the marketing materials may apply only to purchases but not balance transfers, or vice versa.

When it makes sense to use an introductory rate for your business

Introductory APR offers work best as tactical tools for businesses managing growth initiatives, seasonal swings, or short-term projects with predictable payoff timelines (key word: predictable). If you can map out a clear repayment plan that zeros the balance before the intro APR period ends, it can essentially act as a short term, interest free loan. Here are some of the most common ways businesses will use introductory rate offers:

Large planned purchases

The clearest use case is using the credit card for a large, planned purchase that would otherwise come out of operating cash. A marketing campaign budget, a batch of software licenses, a significant inventory order before a busy season: these are the kinds of expenses where a 0% intro period for 12 months can help, especially early on. You buy what the business needs, spread the payments over the promotional window, and pay no interest if you execute the plan.

Consolidating existing debt

Balance transfer offers usually serve a different purpose: debt consolidation. If you have existing credit card balances accruing at 20% or 25%, moving them to a card with a 0% intro balance transfer rate can reduce your carrying cost during the promotional period. The balance transfer fee (typically 3% to 5%) is usually unavoidable, but it is often far lower than the interest you'd pay over 12 months at a high rate. Keep in mind that your eligibility for opening a new line of credit depends on your creditworthiness, so taking steps to strengthen your credit score ahead of time can help get you a credit card that better fits your needs.

When the approach breaks down

Rolling balances from promotional card to promotional card as each offer expires can work for a short period, but it adds risk: it affects your credit profile, requires constant management, and eventually runs out of road when you no longer qualify for new promotional offers. Inevitably, the damage it does to your credit will far outweigh the benefit of using the offer as an interest-free loan. Intro APR is a bridge, not a financing structure.

A charge card can run alongside your broader financing stack without adding any interest rate risk. The Slash Visa Platinum Card is a charge card that earns up to 2% cash back and carries no APR, because balances are paid in full each billing cycle. That structure eliminates the risk of a balance rolling into a high-rate environment after a promotional window closes.

Pros and cons of introductory APR offers

Used well, a 0% introductory APR offer is one of the cheaper ways a business can access short-term financing. Used carelessly, it's a setup for an expensive surprise when month 13 arrives and the standard rate kicks in on whatever's left. Below are what your business should weigh before opening a new account:

Advantages:

- Zero or reduced interest costs: A 0% intro period eliminates interest on purchases or transferred balances for the duration of the promo window. On a $10,000 purchase carried for 12 months at a typical 22% APR, that's roughly $1,200 in interest you don't pay.

- Cash flow flexibility: Spreading a large expense across 12 or more billing cycles without accruing interest lets the business preserve cash for payroll, operations, and growth instead of paying down debt faster than the timing requires.

- Debt consolidation savings: A balance transfer offer can cut the cost of existing high-rate debt significantly during the promo period.

- Ability to earn cash back or rewards: Most rewards cards with intro offers still pay cash rewards, cash back, or statement credit rewards on purchases made during the promo. You're effectively earning money on interest-free spending.

- Building credit history: On-time payments during the promotional period contribute positively to your credit history, both personal (if the issuer reports to consumer bureaus) and business.

Drawbacks:

- High standard APR afterward: When the intro APR offer ends, standard variable APRs on business cards typically range from 16% to 26%. A $5,000 balance that wasn't paid off in time can generate $1,000 or more in interest in its first year at that rate.

- Fees reduce savings: Balance transfer fees, annual fees, and late payment fees still factor in. A 5% balance transfer fee on a $20,000 move is $1,000 upfront, for instance. Worth it if the debt is paid off, a bad deal if it isn’t zeroed.

- Overspending risk: The psychological effect of "0%" is real. It can make it easier to charge purchases the business couldn't comfortably repay on a normal timeline, which defeats the purpose of using the offer as a financing tool.

- Penalty APR exposure: Often, if you’re more than 60 days late on a payment, the issuer may pull the promotional rate and replace it with the standard APR or a higher penalty rate.

- Credit utilization impact: Carrying large balances on a card, even at 0%, increases your credit utilization ratio. If the issuer reports to personal credit bureaus (many business cards require a personal guarantee), this can temporarily lower your credit score.

The drawbacks can be easier to avoid with a clear plan at the start. Calculate the monthly payment needed to zero the balance before the promotional period ends, confirm the business can sustain those payments, and set up automatic minimum payments as a backstop. Treating it as structured short-term financing rather than a low-cost credit line helps keep the math working in your favor.

Maximize the Value of Your Card Spend with Slash

A 0% intro APR card can be a useful tool, but qualifying for one usually means a hard credit pull, a strong personal credit score, and often an EIN. Slash takes a different approach: eligibility for the Slash Visa Platinum Card is based on your business's financial metrics, not a hard credit inquiry, and you don't need an SSN to apply. That matters for non-U.S. applicants or owners who'd rather not take a credit hit just to access a business card.

The Slash Card keeps up with the needs of your team, too. You can issue unlimited virtual cards to employees and contractors, each with its own spend limits, merchant category restrictions, and real-time visibility in the dashboard. Instead of funneling everything through one card and reconciling it manually at month end, every dollar of team spend is tracked, controlled, and categorized as it happens. There's no preset spending limit, so you're not managing against an arbitrary cap. And across eligible business spend, the Slash card earns up to 2% cash back, which can add up once your whole team is running through it.

Here’s what else you get when you get started with Slash:

- Invoicing and bill pay: Create professional invoices, manage outstanding receivables, scan invoices you’ve received with OCR, and more. Your receivables and payables sit alongside everything else.

- High-yield treasury: Earn up to 3.80% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, Sage Intacct, or NetSuite to streamline reconciliation, reporting, and month-end close.

- Native cryptocurrency support: Send and receive USD-pegged stablecoins USDC and USDT across eight supported blockchains for faster, lower-cost global payments.⁴

- Diverse payment methods: Slash supports a wide range of rails, including same-day ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Do I still have to make minimum payments with a 0% intro APR?

Yes. The 0% rate means no interest, not no payments. Missing a minimum can trigger late fees and, if you fall more than 60 days behind, it gives the issuer grounds to cancel the promotional rate and apply the standard APR to your balance.

How Long is a Billing Cycle? Managing Business Cards and Expense Billing

Can my introductory rate be canceled?

Yes. Most issuers can revoke the intro rate if you are more than 60 days late on a payment or otherwise violate the card's terms. If that happens, the standard or penalty APR applies to your full balance immediately.

The 8 Best No-Fee Business Bank Accounts in 2026

Does 0% intro APR apply to cash advances?

Generally no. Cash advances are almost always excluded from introductory offers, and the cash advance APR (often 25% to 30% or more) applies from the day the advance is taken, with no grace period.

Will a 0% intro APR card help my credit?

It can. Paying on time and keeping utilization low are both positive for your credit profile. Note that some business credit cards still report to personal credit bureaus, so late payments can affect your personal credit as well.

What happens to my remaining balance when the intro period ends?

It starts accruing interest at the card's standard variable APR from that day forward, with no grace period.

Is an annual fee worth it for an introductory-rate card?

Add up the interest you expect to save during the promo period plus any cash back or rewards, then subtract the annual fee. If that number is positive, the fee pays for itself. It's also worth considering charge cards like the Slash Visa Platinum Card, which carries no APR and earns up to 2% cash back.

American Express vs. Capital One vs Slash: A Card Comparison