The Best 0% Introductory APR Credit Cards for 2026

Credit cards with an introductory APR offer can be an incredibly effective short-term financing tool if used correctly. They can work like a reset button, giving you a defined window to pay down existing debt or consolidate balances from multiple accounts without interest charges compounding your problem.

But 0% APR credit cards are not free money. The promotional rate is temporary, balance transfer fees often apply, and any remaining balance after the intro period can be subject to a high variable APR. If you don't have a clear repayment plan before the promotional window closes, the relief can be short-lived. That's why we've compiled some of the best 0% APR credit cards available in 2026 to help you compare terms, evaluate tradeoffs, and choose the offer that aligns with your specific repayment goals.

Once you’ve stabilized your balance and moved past the immediate repayment phase, consider upgrading to a card built for long-term efficiency like the Slash Visa Platinum Card, which earns up to 2% cash back on business spending, offers customizable card controls with merchant and category restrictions, and syncs transaction data directly with accounting tools for streamlined reconciliation and reporting.¹

Our top 9 picks: 0% intro APR credit cards

Here are our top nine picks for 0% intro APR credit cards in 2026, selected based on promotional length, fees, eligibility requirements, and long-term value. Each option stands out for a different reason, so the best choice will depend on whether you’re prioritizing maximum runway, balance transfer flexibility, or ongoing rewards after the intro period ends:

Best for longest intro period: Wells Fargo Reflect® Card

The Reflect's 21-month 0% intro APR ties for the longest on this list, but that's also its only real draw. It earns zero rewards on spending, and once the intro period expires, there's essentially no benefit to continuing to use the card. The included cell phone protection plan is a minor perk, but it doesn't offset the complete absence of cash back or points.

- Usage fees:$0 annual fee

- Balance transfer fees: 5% for each transfer ($5 minimum)

- Variable APR range: 17.49% – 28.24%

- Foreign transaction fees: 3% conversion fee

- Credit score: Good to excellent (670+ FICO)

Best for rewards + intro APR: Chase Freedom Unlimited®

The Freedom Unlimited pairs a 15-month intro APR with a structure that goes beyond a flat rate, offering up to 3–5% cash back on select categories alongside the standard 1.5% on everything else. It's one of the more well-rounded rewards credit cards on this list, though it doesn't lead in any single area. Elevated category rates (including purchases through Chase Travel) require spending at specific merchants to realize, and the card includes access to Chase Credit Journey for free credit monitoring.

- Usage fees:$0 annual fee

- Balance transfer fees: 3% for first 2 months, then 5% for each transfer ($5 minimum)

- Variable APR range: 18.24% - 27.74%

- Foreign transaction fees: 3% conversion fee

- Credit score: Good to excellent (670+ FICO)

Best for cash back match: Discover It® Cash Back

The Discover It's first-year Cashback Match doubles all cash rewards earned in the first year after account opening, delivering strong upfront value for new cardholders. Outside of that first year, the ongoing earn rate drops to a flat 1%, with 5% back only on rotating categories that require quarterly activation and come with spending caps. The bigger structural issue is acceptance: Discover has weaker overseas merchant coverage than Visa or Mastercard.

- Usage fees:$0 annual fee

- Balance transfer fees: 3% for first 2 months, then 5% for each transfer ($5 minimum)

- Variable APR range: 17.49% - 26.49%

- Foreign transaction fees: No FX fee

- Credit score: Good to excellent (670+ FICO)

Best for daily expenses: Blue Cash Everyday® Card from American Express

The Blue Cash Everyday targets common spending categories with a 3% earn rate, making it a reasonable pick for cardholders whose spend aligns with Amex's selected categories. However, that 3% rate is capped at $6,000 per category per year—after which it drops back to 1%—which will limit cash rewards for heavier spenders. Entertainment statement credits and Amex Offers add some supplemental value but don't dramatically raise the card's ceiling.

- Usage fees:$0 annual fee

- Balance transfer fees: 3% for each transfer ($5 minimum)

- Variable APR range: 19.49% - 28.49%

- Foreign transaction fees: 2.7% conversion fee

- Credit score: Good to excellent (670+ FICO)

Best for extended payoff timelines: U.S. Bank Shield Visa® Card

The Shield Visa offers the longest 0% intro APR window on this list at 24 billing cycles. However, the card offers little else. Cash back is limited to travel purchases made through U.S. Bank's own Travel Center, and the only other ongoing perk is a $20 annual statement credit. This is a card to open with a specific payoff goal in mind and little expectation of value beyond it.

- Usage fees:$0 annual fee

- Balance transfer fees: 5% for each transfer ($5 minimum)

- Variable APR range: 16.99% - 27.99%

- Foreign transaction fees: 3% conversion fee

- Credit score: Good to excellent (FICO 670+)

Best for fee-averse balance transfers: Citi Simplicity Card

The Citi Simplicity Card makes a narrow case for itself: no late fees, no penalty APR, and a 21-month 0% intro period that ties for the longest on this list. For someone managing a balance transfer who's worried about missing a payment, that forgiveness structure has practical value. But the Citi Simplicity earns zero rewards and offers little beyond those baseline protections. It's worth having during the intro period, but easy to outgrow after it.

- Usage fees:$0 annual fee

- Balance transfer fee: 3% for first 4 months, then 5% for each transfer ($5 minimum)

- Variable APR range: 17.49% - 28.24%

- Foreign transaction fees: 3% conversion fee

- Credit score: Good to excellent (670+ FICO)

Best for simple business cash back: Chase Ink Business Unlimited® Card

The Ink Business Unlimited is a no-frills business card that keeps things simple with unlimited 1.5% cash back on all purchases and no annual fee. The main drawbacks are a relatively short 12-month intro APR window (one of the shortest on this list), which gives business owners less runway to finance larger purchases interest-free. The 3% foreign transaction fee may make this card a poor fit for businesses with significant international spend.

- Usage fees:$0 annual fee

- Balance transfer fees: 5% for each transfer ($5 minimum)

- Variable APR range: 16.74% – 24.74%

- Foreign transaction fees: 3% conversion fee

- Credit score: Good to excellent (670+ FICO)

Best for flexible everyday rewards: Bank of America Customized Cash Rewards Card

The Bank of America Customized Cash Rewards gives cardholders the ability to choose their highest-earning category, which can be useful for businesses with predictable, concentrated spending. The critical limitation in this context is the intro APR: at just 7 billing cycles, it's the shortest window on this list. Plus, the flat rate cash back of 1% on non-category purchases leaves something to be desired for more varied day-to-day spending.

- Usage fees:$0 annual fee

- Balance transfer fee: 5% of each transfer

- Variable APR range: 16.74% - 26.74%

- Foreign transaction fees: 3% conversion fee

- Credit score: Good to excellent (670+ FICO)

Best alternative to intro APR cards: Slash Visa® Platinum Card

A business charge card rather than a credit card, Slash stands apart from every other card on this list with up to 2% cash back — the highest flat rate here — and no credit check requirement. Beyond the earn rate, it's the only card on this list built with spend management in mind: you can issue unlimited virtual cards, set granular controls by merchant or category, and sync transaction data directly to QuickBooks through the Slash dashboard.

- Usage fees:$0 - $25/month for Pro

- APR: N/A (charge card)

- Foreign transaction fees: 1% FX fee

- Credit score: No credit check required

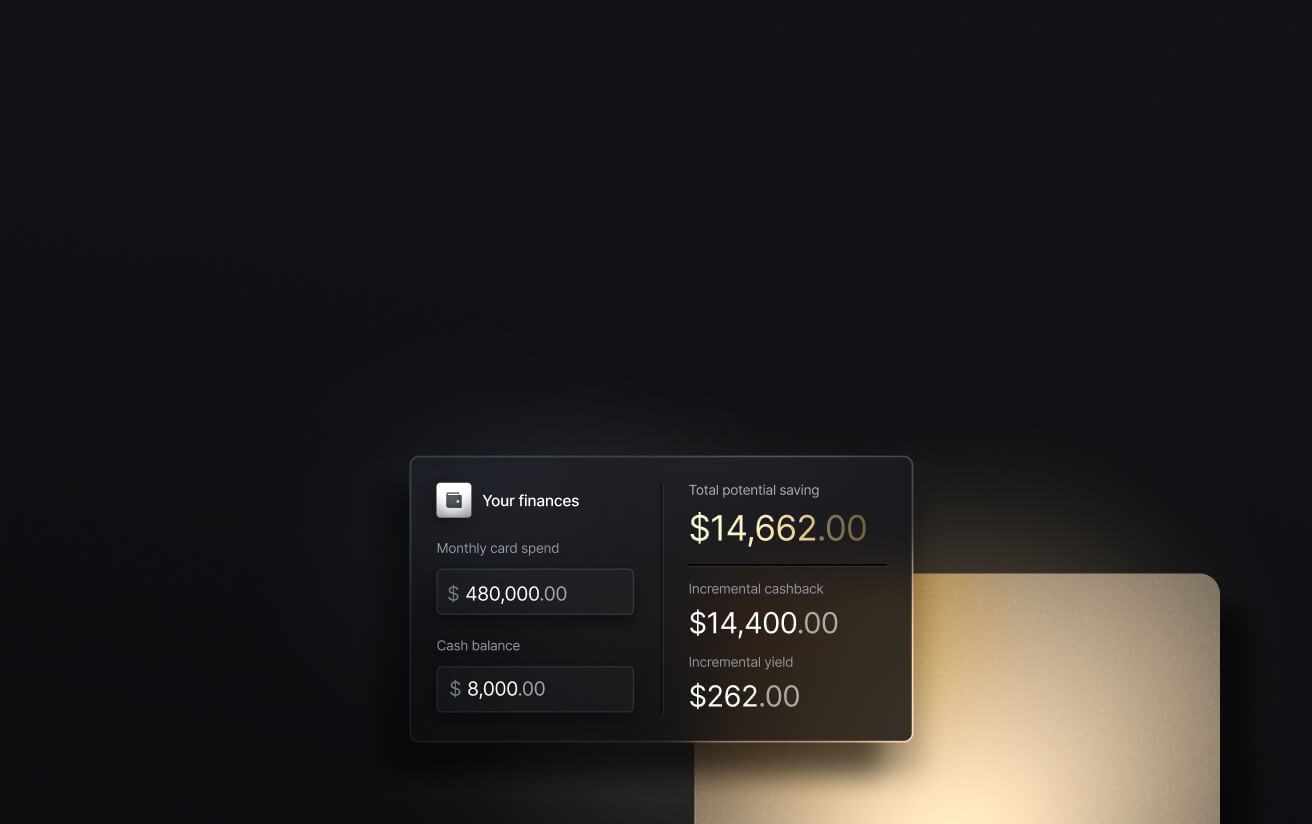

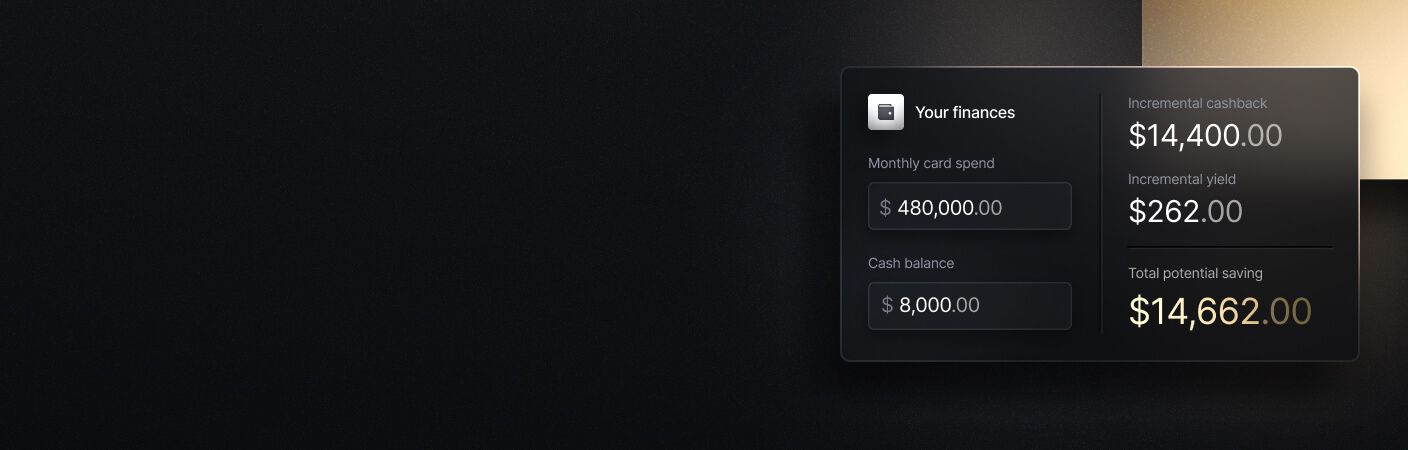

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

How to decide which 0% intro APR card is right for you

Not every balance transfer offer is structured the same way. Some balance transfer cards apply the promotional rate only to new purchases, others only to transferred balances, and the length of the introductory period can range from 12 billing cycles to 21 or more. Before applying, be clear about whether you're consolidating debt, financing a purchase, or creating short-term breathing room, because the right card for one goal may be the wrong fit for another.

Here are some common scenarios where introductory offers may make sense for applicants:

- Consolidating outstanding balances: A 0% APR balance transfer card can simplify repayment by combining multiple balances into one monthly payment, potentially reducing the total interest you'd otherwise accrue. Just make sure the balance transfer fee doesn't outweigh the interest savings.

- Paying off a high-rate balance: If one card is charging a high purchase APR, transferring that balance can immediately stop interest from compounding in the short term. However, it’s important to commit to paying it down aggressively before the standard variable APR applies.

- Making a large one-time purchase: A 0% APR card can function as short-term financing, letting you spread payments out without paying interest, as long as you stay within the promotional window from account opening.

- Short-term cash flow relief: Temporary income gaps or unexpected costs can strain your budget. A 0% intro APR card can provide breathing room, but it's a bridge strategy; the balance still needs to be repaid before regular interest kicks in.

How 0% intro APR actually works

A 0% intro APR card is best viewed as a structured financing strategy. It can be highly effective for paying down debt, consolidating balances, or smoothing short-term cash flow, but only if paired with a disciplined repayment plan. Carrying a large balance past the promotional deadline can result in substantial interest charges and may negatively impact your credit score if utilization remains high.

Used strategically, these offers create breathing room and reduce interest costs. Used carelessly, they can delay the problem rather than solve it. Here are some important things to consider:

Key distinction: Using 0% APR for purchases or balance transfers

Not all 0% APR offers apply to the same types of transactions. Some cards offer 0% APR on new purchases only, others apply it strictly to balance transfers, and a few extend the promotional rate to both. If your goal is debt consolidation, you'll want to confirm that balance transfers qualify and review any associated transfer fees, which are typically 3% to 5% of the amount moved.

Key things to confirm before applying:

- Whether the 0% rate applies to purchases, balance transfers, or both.

- Transfer fees, which are typically 3% to 5% of the amount moved.

- Many issuers require balance transfers to be completed within the first 60 days of account opening to qualify for the introductory rate. Missing that window could mean losing access to the promotion entirely.

What happens after the promotional period ends?

After the intro period expires, the card reverts to its standard variable APR, which is often significantly higher. Any remaining balance will begin accruing interest immediately at that rate. That’s why it’s critical to calculate whether you can realistically pay off the balance before the promotional window closes

You should also evaluate the card’s long-term usability. Does it offer competitive rewards, reasonable fees, and benefits that align with your spending habits? If not, it may serve purely as a short-term tool rather than a card you plan to keep in regular rotation.

What is a billing cycle, and why does it matter?

A billing cycle is the period of time, typically about 28 to 31 days, during which your credit card transactions are recorded and grouped into a statement. At the end of each billing cycle, your issuer generates a statement showing your balance, minimum payment due, and payment deadline. Even with a 0% intro APR, you must still make at least the minimum payment by the due date to maintain the promotional rate.

Payment timing also affects how your balance appears on your credit report. Your statement balance is often what gets reported to credit bureaus, and a high reported balance can increase your credit utilization ratio. Paying down your balance before the statement closing date can help manage utilization and protect your FICO score while you're using the promotional offer.

Using a 0% intro APR card for business spending

A 0% intro APR card can be especially useful in a business context. If you're making a large one-time purchase, such as equipment, inventory, or a software implementation, the promotional period can function like short-term, interest-free financing. It can also provide temporary cash flow relief during slower revenue months or while waiting on receivables to clear.

The key is to treat the offer as a structured plan, not a flexible safety net. Before you even open the account, decide which specific business expense will go on the card, what your monthly payoff target will be, and the exact date by which you intend to have the balance at zero. Reverse-engineering the math from the end of the promotional period can help you determine whether the strategy is realistic based on your projected revenue.

Tracking spending during the intro period matters even more for businesses than for personal use. Charges can quickly spread across software subscriptions, travel, advertising platforms, contractors, and recurring vendor payments, making it easy to lose visibility into your true balance. Reviewing transactions consistently and reconciling them against your accounting system helps ensure the promotional balance does not quietly grow beyond your payoff plan.

Here are some additional considerations to keep in mind when using a 0% APR business card:

- If the card offers rewards in the form of a statement credit, understand that it reduces what you owe but does not replace disciplined repayment.

- Approval terms, promotional periods, and credit limits may vary based on your credit profile, so the advertised headline offer is not guaranteed.

- Have a backup financing plan in place in case you do not qualify for the 0% APR offer or receive a lower limit than expected.

Thinking beyond the intro offer: Managing business finances with Slash

If you’re a business owner using a 0% intro APR card to pay down balances or finance a major purchase, it can be a powerful short-term lever. But promotional financing is temporary by design, and most 0% APR cards are not built to serve as a long-term operating backbone for your business. Once your balance is under control, it often makes sense to transition to a dedicated business card that supports daily spend management, employee controls, and financial visibility.

That’s where the Slash Visa Platinum Card fits in. You earn industry-leading cash back on business spending, can issue unlimited cards to employees with customizable controls, benefit from low foreign transaction fees, and manage everything inside the broader Slash financial dashboard. Instead of juggling separate tools for payments, cards, and reporting, you operate from one unified system.

With Slash, you get infrastructure that extends well beyond a single credit line:

- Diverse payment methods: Send global ACH and wires to 180+ countries and move money domestically in real time via RTP and FedNow. Pro users pay no added per-transaction fees.

- High-yield treasury: Earn 3.86% APY on idle cash through treasury accounts backed by Morgan Stanley and BlackRock money market funds.⁶

- Native cryptocurrency support: Hold, send, and receive USD-pegged stablecoins like USDC and USDT across eight supported blockchains for fast, low-cost global payments.⁴

- Separate virtual accounts: Create multiple accounts to silo cash by project, department, or client, with real-time visibility across all balances.

- Accounting integrations: Sync transactions directly with QuickBooks to keep your books automatically updated.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What happens when the intro APR period ends?

When the introductory period expires, any remaining balance begins accruing interest at the card’s standard variable APR. If you have not paid off the balance, your monthly interest charges can increase significantly, so it’s important to have a payoff plan in place before the promotional rate ends.

Can a 0% intro APR card affect my credit score?

Yes. Applying for a new card may cause a small, temporary dip due to a hard inquiry, and carrying a high balance can increase your credit utilization ratio. However, making on-time payments and lowering your overall debt during the intro period can positively impact your credit profile over time.

How to Build Business Credit: A Complete Guide for Businesses