How to Open a Company Bank Account in Only 3 Steps

Opening a company bank account is one of the first steps you should take after launching your business. While you may be excited to buy supplies, start working on a website, and hire employees, you shouldn’t manage any of it with your personal account. A dedicated company bank account separates your professional expenses from your home expenses, keeping your tax returns simple and helping you look clean in the eyes of the IRS.

The actual act of opening a company bank account can be trickier than you might expect. You’ll need quite a few pieces of documentation to start, and if you want an account with certain features, you should dive in and do some research. A company account that earns high yield and helps you track your spending can be completely different from one that just acts like a steel safe in your closet.

If you want to know why a company bank account matters, what to look for when choosing a bank, how to open the account, and how to manage it once it's up and running, you’ve come to the right place. We’ll also take a look at Slash, a business banking platform checking, treasury, and corporate cards in one place.¹, ⁶ Slash offers a level of financial control that you’ll rarely get anywhere else, with automated accounting sync and built in AP & AR tools. Continue reading to learn more.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

The Importance of Having a Company Bank Account

A company bank account, otherwise known as a business bank account, is simply a bank account meant for non-personal, business-related purchases and transfers. About 96% of small businesses maintain dedicated business bank accounts, according to recent data compiled by B2BReviews. Let’s take a look at some reasons these accounts have become near-universal:

Separation of personal and business finances

Keeping your company finances separate from your personal finances is both a good practical decision and a good legal decision. If your business expenses run through the same account as your personal expenses, you’ll have to manually sort through every transaction to figure out how much you’ve been spending and how much runway you have left in the short term. Not only is that inconvenient, but it can make claiming tax deductions on business expenses at the end of the year very difficult.

This isn’t a problem with a dedicated company account. Everything within it is business-related by default, which makes tracking, reporting, and reconciling way simpler. If you own an LLC or corporation, that distinction also reinforces the separation between personal and business assets. The owner of an LLC isn’t supposed to be entirely liable if their business goes under, but if they ran that business with a personal bank account, their own assets won’t be shielded against creditors and audits.

Getting more control over your cash flow

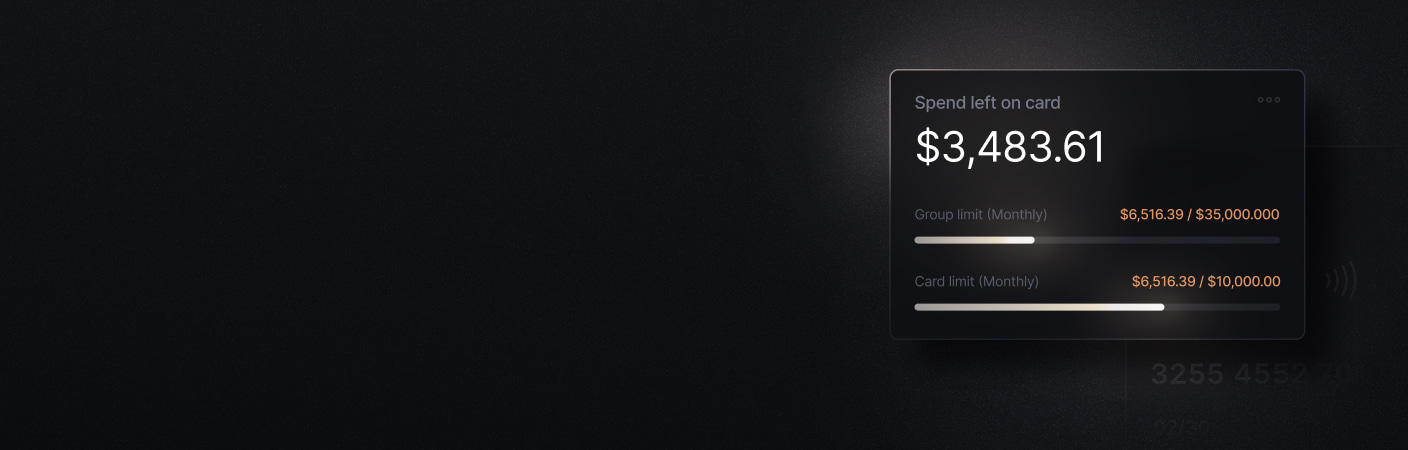

Company bank accounts usually come with a variety of features that personal accounts rarely support. Expense tracking, bill pay, and cash flow analytics can all be game-changers for small businesses, especially given the lack of time owners have to manage it all. Some platforms, including Slash, offer corporate card programs that give users cash back on business purchases and come with expense management tools. Without these features, you’re essentially paying an opportunity cost, meaning the decision to ignore them is actively costing you money.

Simplifying tax preparation

If you want to earn money back at the end of the year by deducting legitimate business expenses, you’ll need organized documentation. A company bank account is built to provide that clear, complete record of what your business spent. When everything’s mixed up in a personal account, identifying which charges were business-related means you’ll have to go line by line and sift through groceries, streaming subscriptions, and everything else.

A separate company account can also let your accountant or bookkeeper work directly from a clean record of business activity. Because everything’s arranged where it belongs, you get a chronological list of your income and expenses throughout the year that acts as an automatic audit trail.

Choosing the Right Bank: Key Considerations

Not all small business owners spend time doing research before choosing a company bank account. In fact, 56% of them open their company account at the same bank they hold their personal account with, according to data from the NFIB. While there’s something to be said about the convenience of working with a familiar bank, this often means they left better options on the table.

It’s usually best to consider a wide range of company bank accounts and narrow them down to those that most closely fit your needs. Here’s what you’ll want to keep in mind as you choose your bank:

Features and perks

An account’s features may make or break your decision from the start. One of the most important things to consider is whether the bank supports the payment types your business relies on. ACH transfers, domestic and international wires, and real-time payments are standard at most banks, but the fees they each come with can make a big impact. If you’re looking for a more modern rail with faster transfer times, Slash allows users to send and receive stablecoins like USDC and USDT and on/off ramp them into fiat currency natively.⁴

Once you’ve examined their payment methods, you’ll also want to learn about their card program, tools for tracking and managing expenses, and any integrations they have with accounting solutions or ERP systems. As you compare and contrast the features different company bank accounts offer, it helps to picture the ways you’ll use them on a day-to-day basis.

Interest rates

It’s likely a bad move to keep your cash sitting in a non-interest-bearing account, especially if you have a lot of it. Even a little bit of interest on those funds adds up over time. Banks often offer interest-bearing checking or business savings options that pay more than a standard operating account. Some come in the form of high-yield savings accounts, while others are treasury accounts backed by the full faith and credit of the US government. For example, eligible Slash users can access a Treasury account backed by BlackRock and Morgan Stanley that earns up to 3.82% annualized yield on idle cash.

Customer service

If and when something goes wrong with a payment, the quality of your bank’s support can instantly become a big deal. You don’t want a declined wire, a flagged card, or an account access issue to take days to fix. Some banks have support channels dedicated to company account problems and tool-related troubleshooting. If you’re interested in sticking with your personal bank because you’ve had good experiences with their customer support, doublecheck to see if they offer help lines tailored for companies as well.

Accessibility

Accessibility can mean different things to different business owners. Online-only banks that offer strong rates and features can work well for businesses that rarely need in-person banking. Traditional branch-based banks make more sense if you regularly deposit cash, want access to physical banking services, or simply prefer in-person assistance. Digital options are quickly becoming the norm, however; the American Bankers Association found that 76% of banking customers primarily use mobile and online apps to manage their banking, while only 9% prioritize visiting local branches.

3 Steps: How to Open a Company Bank Account

Opening a company bank account isn’t the same as opening a personal one, even if you use the same bank for both. While the process will look a bit different from institution to institution, you’ll typically follow these three steps:

Step 1: Gather your documentation

Most banks require similar documentation, though the specific list can vary slightly based on your business structure and state of residence. You’ll want to have these ready before you apply:

- Government-issued photo ID for all owners and authorized signers

- Employer Identification Number (EIN), or Social Security Number (SSN) if you're a sole proprietor without an EIN

- Business formation documents (Articles of Organization for an LLC, Articles of Incorporation for a corporation)

- Operating agreement, if your LLC has multiple members

- Business license or permits, if required by your city or state

- DBA registration certificate, if you operate under a trade name other than your legal business name

- Business name and physical address

If you're not sure what your specific bank requires, it’s a good idea to call ahead or check their website before applying. This can also be a good test run for their customer service; if you have a tough time getting in touch with someone to ask about documentation now, an emergency scenario down the road could be even worse.

Step 2: Complete the application process

Most major banks and digital banking platforms let you apply online, though some still require an in-person visit to verify your identity. Modern online applications are usually quick, sometimes taking less than 30 minutes to complete when you’re prepared with your documentation. Approval typically comes within a few business days for straightforward cases, especially with digital-first banks that can move more nimbly.

During the application, you'll provide your legal business name, structure, EIN, and the other paperwork and information listed above. If there are multiple owners with significant stakes in the business, they may need to verify their identity separately. Once the bank gives you their stamp of approval, they’ll send you your account details and you can set up online access.

Step 3: Deposit funds and get set up

Before you fully get started, check to see if your account requires a minimum opening deposit. Not all company bank accounts do, but some need a small starting balance of around $200-$500. Once the account is open, connect it to your accounting software, configure your online banking settings and security parameters, and order any cards you need. If you were previously using your personal accounts to manage business purchases and vendor payments, it’s best to update your partners and suppliers with your new account information as soon as possible.

Tips for Managing Your Company Bank Account

Even if you have access to automated financial tools, your business bank account can’t manage itself. As your company gets busier, you’re responsible for staying on top of every one of those incoming and outgoing payments. It may seem overwhelming, but ideally, your company bank account comes with tools built to make it all a little easier. To manage everything cleanly, you may want to:

Track your transactions

Try reviewing your account activity every couple of days instead of scanning through your bank statements at the end of each month. Duplicate charges and fraudulent transactions can be much easier to dispute when they're recent. As you stay up to date on your spending, you’ll also have your finger on the pulse of your cash flow. You may notice if revenue is slowing, if a vendor is paying inconsistently, or if you’re spending more on inventory than expected. A few minutes of inspection every couple days can help you avoid hours of stress at the end of the month.

Utilize online banking features

What’s the point of a tool if you don’t use it? While something like working capital financing might only be used situationally, quite a few features can come in handy on a daily basis. Most platforms let you set up 24/7 alerts for low balances, large outgoing transactions, or unusual activity patterns. You may also be able to automate recurring payments or schedule transfers, saving you time and lowering the risk of missed payments. Each tool on a company bank account’s belt is meant to make your life easier, so it’s smart to take advantage of them when you can.

Conduct full account reviews

While you may track your transactions several times a week, it’s also helpful to review your account activity overall every month or two. Ask yourself questions like:

- Is my liquidity in a better spot than it was last month?

- Are my operating costs staying consistent?

- Are clients paying us on time, and are we paying our vendors on time?

- How are my employees using their corporate cards, and do I need to adjust their spend limits?

- Do I have excess cash that belongs in a high-yield account?

Ideally, this isn’t the time where you catch suspicious transactions or categorize miscellaneous purchases. You should instead use these reviews to make larger-scale strategic decisions and shift priorities if you see something heading in the wrong direction.

Make the Right Financial Move with Slash

Gathering the documentation you need to open a company bank account can be cumbersome, but it’s straightforward overall. Actually choosing an institution to open that account with, however, is another story. Do you want to choose an option that comes with a bounty of features, or one with a strong customer support team? Is it better to pick an account that gives you more control over money movement, or one that allows you to earn high interest on money that doesn’t move?

If you partner with Slash, you can have it all on the same account. Slash is a financial platform that puts corporate cards, diverse payment rails, accounting integrations, and more alongside a company checking account on a real-time dashboard.

Business owners that rely on their employees to spend money can issue unlimited virtual Slash Visa® Platinum Cards, each with uniquely configured spend controls and the ability to earn up to 2% cash back on company purchases. If you’re looking to break into crypto, you can send and receive stablecoins and on/off ramp them with conversion fees of up to 1.5%. No worries if you’re not on the Web3 train – we also support traditional rails like domestic and global ACH payments, wire transfers, FedNow/RTP, and virtual cards.

All deposits into Slash accounts are insured into the hundreds of millions with the help of our partner bank, Column N.A.² Column works with a network of FDIC-insured banks through the IntraFi sweep program to distribute your funds across multiple institutions, meaning your coverage can be extended far beyond the common $250k limit.

Slash’s company bank account comes with quite a few other features, including:

- AI-powered finance: Twin is a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- Global USD Account: The Slash Global USD Account is designed as an alternative for foreign founders who want access to USD without forming a US entity.³ Balances are backed by Slash’s USDSL stablecoin, which is designed to maintain a one-to-one value with the US dollar.

- Accounts payable & receivable: With Slash’s invoicing and bill pay features, users can send customized invoices, collect payments, and manage vendor bills all in the same place.

- Slash Mobile App: Bank on the go with the Slash app; issue cards, check balances, check items in your action center, and move money from your phone. Learn more about our app’s capabilities here.

Slash can give your company complete control over its finances from the comfort of your computer chair (if it’s comfortable, that is). To learn more, reach out today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

How long does it take to get approved for a company bank account?

Approval timelines can vary by institution and your company’s structure. Many online banks and digital-first banking platforms can review and approve a complete business account application within a few days. If you forget about certain pieces of documentation or additional verification is needed, though, the process can take longer.

What are the Easiest Business Credit Cards to Get? Top Picks and How to Get Yours Approved

How much does it cost to open a company bank account?

The actual act of opening a company bank account is typically free, but there are other types of costs to watch out for. Some accounts require an opening minimum deposit, while others come with monthly maintenance fees and per-transaction costs. Banks can occasionally waive monthly fees if you maintain a certain average balance or meet activity thresholds.

The 8 Best Free Business Bank Accounts in 2026

Can I open a company bank account online?

Definitely, even with many traditional brick-and mortar banks. Most banks and banking platforms offer online applications that don't require a branch visit.

Online Banking Systems: Guide to Digital Banking Platforms

Read more from us