Online Banking Systems: A Complete Guide to Digital Financial Platforms

Nowadays, a lot of people only interact with their banks digitally. You can now use your phone or laptop to move money, pay bills, check balances, and more without having to set foot in your local branch. Not only is this generally convenient, but it can be a necessary feature for business owners who spend most of their time on the go.

Recognizing the need for online banking features, modern banks have quickly begun expanding the capabilities of their respective platforms. In 2026, online banking systems can have AI assistants, real-time spending insights, credit monitoring, savings tools, and much more. You can do just about everything from your phone except break a $100 bill.

With so much change and innovation in digital banking, choosing the right platform can be challenging. Should you go with a traditional bank, a community bank, or a fintech provider? This guide can help. We’ll explain how online banking systems work, what features matter most, and compare six of today’s leading platforms.

We’ll also examine Slash, a neobank built for modern businesses. Beyond business banking, Slash offers stablecoin support and treasury accounts for companies managing cash across traditional and digital assets.¹, ⁴ Businesses can also access financing, treasury, and other financial tools through a single platform, reducing the need to manage multiple providers.⁵, ⁶

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How Online Banking Systems Work

An online banking platform is the user interface that allows customers online access to a bank's core banking infrastructure. The core, in this context, is the database that actually holds account balances, processes transactions, and maintains the record of truth for deposits and withdrawals. The online platform often connects to that core through a set of APIs, allowing customers to control their accounts with a few buttons on a mobile app.

When you log in, the system almost always authenticates your identity before letting you access your account data. Most major banks now use multi-factor authentication as the default, often coming as some combination of a password, 6 digit code, and biometric fingerprint. As of May 2026, 60-75% of banking platforms use biometrics for logins, per Oloid.

When you initiate a transaction, that processing happens through a combination of the bank's own systems and external payment networks. A bill payment may goes through ACH, a peer-to-peer transfer might work through Zelle, and a wire will probably use SWIFT or Fedwire. Real-time payment rails like RTP and FedNow are also becoming more common on consumer platforms, enabling transfers to settle in minutes rather than hours or days.

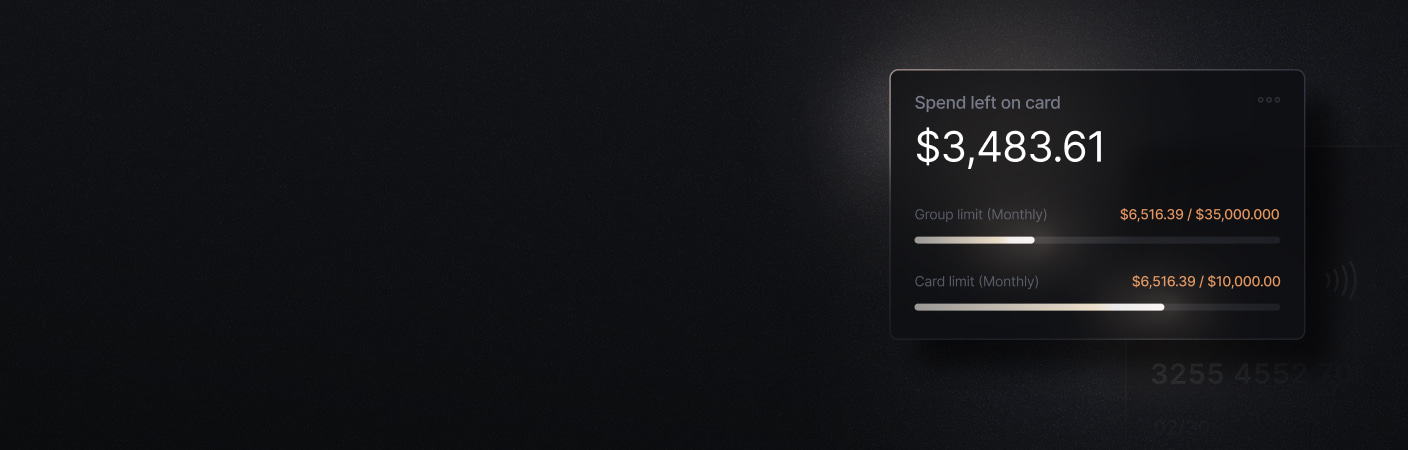

Banking regulators like the FDIC, OCC, and CFPB set strict security and compliance regulations for online banking platforms. For the average system, that often means building out data encryption tools, adopting strict access controls, monitoring activity for fraud detection, and allowing detailed audit logging. Some platforms now also include consumer-facing security tools, such as spending threshold notifications and the ability to view a list of devices that have accessed the account. Slash, for example, comes with a charge card that can be configured with per-employee spend controls, merchant restrictions, and alerts for suspicious activity.

Leading Traditional Online Banking Systems in 2026

As we go over our six picks for online banking systems, we’ll look at three that operate between branches and online platforms, and three that more strongly prioritize their online options. Let’s start with the traditional ones:

JPMorgan Chase Online Banking

JPMorgan operates the largest U.S. bank by assets, and its online banking platform reflects that scale. The web and mobile experience, which is Chase-branded, covers checking, savings, credit cards, mortgages, auto financing, and investing. Chase also gives customers access to free credit scores through Credit Journey, which reports from TransUnion.

- Strengths: The JPMorgan investing integration is a big differentiator, as you can move money from a checking account to a brokerage account, track portfolio performance, and work with a financial advisor within the same app. It also has solid bill pay features, with the ability to schedule and track invoice payments to contractors or companies.

- Downsides: Chase’s savings accounts offer a very low APY, coming in at 0.01%-0.02%. You can also get hit with $15 monthly maintenance fees when you don’t hold a certain balance or make monthly deposits.

Bank of America Digital Banking

Two of Bank of America’s key online features are Erica, its mobile-only AI assistant, and an integration with Merrill Lynch investment accounts. Erica can surface spending patterns, flag unusual charges, and connect you to a human specialist. However, it’s not a fully agentic AI, meaning it can’t execute complex tasks from prompts in the same way Slash’s “Twin” can.

If you have a Merrill account, you can get a combined view of your banking and portfolio balances in one place. Their system also comes with a tool called Life Plan, which allows users to set and monitor financial goals as they plan for the future.

- Strengths: Even without agentic abilities, Erica is a useful AI assistant for tasks like spend tracking and locking cards. The Merrill Lynch integration is also key, provided you have an account with them.

- Downside: Some important perks, including card rewards and locked fees, are locked behind a Preferred Rewards status, which requires maintaining a combined balance of at least $30k across Bank of America and Merrill. Erica is also mobile-only, so customers who mainly bank from a desktop don’t get the whole experience.

Wells Fargo Online Banking

Wells Fargo's platform covers account management, bill pay, Zelle, card controls, and mobile deposit. One of its stronger features is its Security Center, which is a dedicated section of the mobile app that consolidates security settings, displays your account's current protection level, and calls out active scam alerts.

FICO score access is available to eligible account holders, and the commercial banking side of the platform has more depth than some of its competitors. In fact, its treasury tools are accessible from the same login as its personal accounts.

- Strengths: The mobile app’s Security Center comes with more options than most online systems allow, giving customers a little more control of their account’s safety. With its healthy business banking features, it’s also particularly useful for founders and small business owners.

- Downside: Wells Fargo’s typical overdraft fee is $35, which is higher than many of its peers. Like JPMorgan Chase, it also comes with rather low savings APY at 0.01%.

Top Digital-Native Banking Platforms

The following three picks are either more known for their online systems than their branches, or don’t have branches at all:

Ally Bank

One entirely digital bank is Ally, which doesn’t have any physical branches or plans to build them. Partly as a result of this business plan, there are no monthly fees or minimum balance requirements to open an account. If you need help at any time, Ally offers 24/7 customer support by phone, chat, or email. The platform also hosts a high yield savings account that currently comes with an APY of 3.00%. With a function called “Buckets” you can also sort your savings into different categories.

- Strengths: Its strong savings rates, lack of fees, and Buckets tool make it helpful for customers who want to save money efficiently. The round-the-clock customer support is also key if you ever have an evening emergency that can’t wait until morning.

- Downside: The lack of physical branches can be a pain, especially if you’re looking to deposit cash. Currently, cash deposits are only possible via Walmart Money Centers using a barcode generated in the Ally app.

Capital One Online Banking

Capital One's online banking system is built with its mobile experience in mind. Their app currently carries a 4.8 star rating on the App Store, which is just about as good as it gets. Its 360 Checking and 360 Performance Savings accounts carry no monthly fees and no minimum balance requirements, and you can even access paychecks two days early through the checking account. Like JPMorgan Chase, you can also check your credit score for free using TransUnion data, but Capital One doesn’t require you to be a customer to do it.

- Strengths: The lack of fees or minimums on its accounts, a highly-rated mobile app, and CreditWise credit monitoring make it a solid choice for everyday consumers. Its early paycheck feature is also a plus for those with low checking balances.

- Downside: Limited physical presence. Capital One's locations are mainly Cafés rather than full-service branches, which matters if you ever need in-person help or regularly deal in cash.

Marcus by Goldman Sachs

“Marcus” is the name of Goldman Sachs's consumer savings brand, which is focused narrowly on savings accounts and CDs. In other words, it doesn’t have a checking account. However, the online savings account offers 3.40% APY with no minimum balance and no monthly fees, which is one of the highest-yield options you’ll find in the space. CD options include a promotional 14-month term at 4.00% APY and a No-Penalty CD at 3.80% APY, both with a $500 minimum. Goldman Sachs comes with institutional credibility, which means Marcus’s rates are consistently competitive without much risk of fluctuation.

- Strengths: Marcus comes with some of the most competitive savings rates in the consumer market with no fees and no minimum balance. If you’re looking for a savings account, it’s a great choice.

- Downside: If you’re looking for a checking account, on the other hand, you won’t find it here.. Marcus is a savings and CD platform only, so you’ll have to manage a separate checking account elsewhere for everyday spending.

How to Choose the Right Online Banking System

The right choice of platform depends on whether you’re an individual or business, and what you intend on using the platform for. Here are the factors that separate a strong online banking system from a weak one:

- Savings rates: Online-only platforms usually offer higher yields than traditional banks because they don't carry the overhead of branch networks. If earning a competitive APY on idle cash is a priority, digital-native platforms will often beat the big traditional banks on this metric. Some business banking platforms, such as Slash, come with treasury accounts that offer a higher annualized yield than many high-yield savings accounts.

- Fee structure: Each platform comes with different monthly maintenance fees, minimum balance requirements, and overdraft fees. Some institutions waive fees conditionally, while others have eliminated them entirely. Take a look at the full fee list of any system you’re interested in.

- Mobile experience: For many people, the mobile app is the most important banking interface. While not professionally endorsed, app store ratings and user reviews are a good indicator of day-to-day usability. You’ll also want to keep an eye out for certain standout features, such as AI assistants and automation tools.

- Physical access: Some online banking platforms are committed to never building real branches, which can work for their sakes. However, if you handle cash regularly, need to visit a branch occasionally, or prefer resolving issues in person, the availability of ATMs and branch locations is pretty important.

- Security features: Beyond multi-factor authentication, you should look for features like the ability to generate virtual card numbers for online purchases, card freeze controls, and a clear security dashboard that makes it easy to review and update your protection settings.

Make the Right Financial Move with Slash

Most online banking systems are built primarily for personal finance. They can handle everyday spending and saving well. If you’re a business managing spend across borders, multiple entities, or high corporate card volume, you often won’t get everything you need from a legacy online banking account.

As a neobank tailored for business financial management, Slash offers access to payment rails including SWIFT wires, real-time payment networks, global ACH, virtual cards, and stablecoin transfers across eight different blockchains. The Slash Visa® Platinum Card is a charge card custom-built for employee spend. Issue unlimited virtual cards, apply granular spend limits or team controls, and earn up to 2% cash back on eligible business spend.

If you run a multi-entity business, everything from accounts to cards to analytics consolidates under one login, each with separate views per entity. At the same time, accounting integrations with QuickBooks, Xero, NetSuite, and Sage Intacct sync automatically, meaning all expenses can sort cleanly without manual reconciliation or accidental data entry typos.

Slash’s online banking system also comes with the following features:

- Agentic AI: Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.

- High-yield treasury: Earn up to 3.80% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.

- Global USD: The Slash Global USD Account is designed as an alternative for foreign founders who want access to USD without forming a US entity.³

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Are digital-only banks like Ally safe?

Yes, digital-only banks that are FDIC members (which Ally is) carry the same deposit insurance as traditional banks, up to $250,000 per depositor, per ownership category. The absence of physical branches doesn't affect the safety of deposits. Slash accounts are FDIC-insured up to $150M through the Column N.A. insured cash sweep network.²

The Top 5 Recommended Crypto-Friendly Banks for Businesses in 2026

Top Online Banking Platforms in 2026

Can I use multiple online banking platforms at the same time?

Yes, and many people do. You might hold a high-yield savings account at a digital-only bank like Marcus, plus a full-service checking account at Chase or Bank of America for everyday transactions.

Top Fintech Platforms for Multi‐Entity Banking in 2026

What should business owners look for in online banking systems?

Businesses generally need more from their banking platform, including multi-user access with different permission levels, the ability to issue cards to employees with individual controls, strong accounting software integrations, international payment options, and support for multiple entities or accounts under one login. Consumer platforms often lack these features entirely, which is why purpose-built business banking platforms like Slash exist in their own category.

What Business Banking Platform Should You Choose in 2026?

AI Solutions for Banking: Use Cases, Insights, and Benefits