How to Choose a Business Banking Platform for Your Small Businesses in 2026

Anyone opening a business bank account today might be surprised by how many choices they face. Traditional banks have expanded what they offer, and recent years have seen neobanks and fintechs fill the landscape with flexible, powerful account features. The competition is fierce, and every business owner has to pick their own winner.

Some platforms serve small businesses that regularly handle physical cash, while others are a better fit for companies planning to expand across borders. Choosing the right one comes down to figuring out where your business fits and which parts of your everyday workflow you want to improve.

This article explains what business banking platforms are, what to look for when evaluating them, and how the top seven options compare for small businesses in 2026. We'll also look at Slash, a neobank that goes a step further with modern tools you won't find everywhere, including stablecoin support and agentic AI purchasing.¹,⁴ With international payment rails, a treasury account with no minimum balance, and working capital loans, Slash is built to support small businesses at every stage of growth.⁵,⁶

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What Are Business Banking Platforms?

Business banking platforms are digital-first companies that offer business checking, payment tools, and built-in financial management, usually without a branch network. Most aren't chartered banks themselves; they partner with FDIC-member banks to hold insured deposits.² Slash, for instance, works with Column N.A., which extends insurance into the hundreds of millions by sweeping funds across multiple FDIC-insured banks.

The practical difference comes down to what's bundled in. Traditional banks tend to charge monthly maintenance fees for basic checking, with financial management sold or handled separately. Platforms tend to fold in accounting integrations, expense tracking, user permissions, and virtual cards. The point is to bring those operations in house and cut out the friction of working through a branch, so more of your financial workflow lives in one place.

What to Look for in a Business Banking Platform

No single platform is best for every business, so the right one depends on how you operate. A company that handles daily cash needs something very different from one paying overseas contractors or managing spend across a team. Before comparing providers, it helps to know which features move the needle for you. Here are the ones worth prioritizing:

- No monthly fees: Some checking accounts charge monthly maintenance fees, often tied to a minimum balance. If you're watching every dollar, look for a platform without them.

- User-friendly mobile and web interfaces: Owners and their teams often manage finances on the go, and a weak mobile app makes it hard to work outside the office.

- Accounting integrations: A platform that syncs transactions with tools like QuickBooks Online and Xero can remove much of the burden of manual reconciliation.

- Expense management and corporate cards: For businesses with multiple team members, having the ability to issue cards with preset limits and tracked expenses inside the platform can cut out the need for a separate tool.

- FDIC insurance and security: Standard coverage is $250,000. Some platforms, including Slash, use deposit sweep programs across multiple partner banks to extend coverage beyond $100 million.

- International capabilities: For businesses paying overseas vendors or earning revenue in foreign currencies, flexible cross-border rails and competitive international rates matter.

The Top 6 Business Banking Platforms for Small Businesses in 2026

1. Slash

Built to centralize financial operations on one integrated dashboard, with no monthly fee or minimum balance requirements to get started.

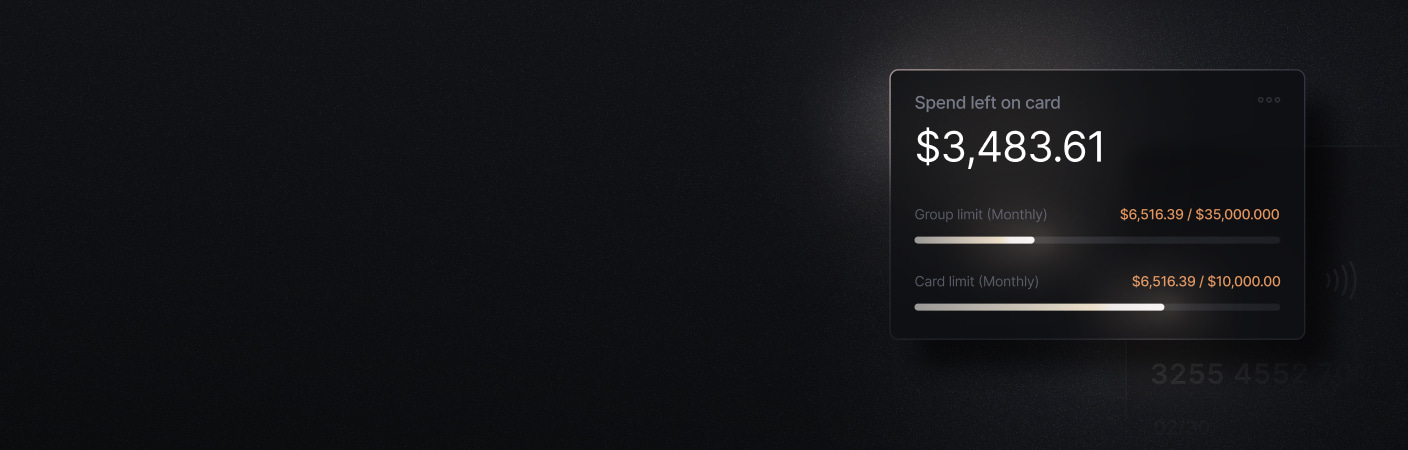

- Slash Visa Platinum Card: Earns up to 2% cashback with unlimited issuance, per-card spend controls, and real-time visibility across every card and transfer. No personal guarantee required in an EIN-only application.

- Diverse payment methods: SWIFT wires to 180+ countries, global ACH, and real-time domestic transfers via RTP and FedNow, plus stablecoin on/off ramps for cross-border USD.⁴ Pro users pay no per-transaction fees on domestic transfers.

- Built-in treasury: Earn up to 3.76% annualized on idle funds through BlackRock and Morgan Stanley money market funds

- AI-powered finance: Chat with Twin to manage your accounts, make purchases online, and give detailed insights into your financial metrics.

2. Mercury

A digital banking platform for tech founders, built around API access and a clean interface.

- Accounts and cards: Business checking and savings, corporate debit cards, and venture debt for funded startups, with FDIC coverage up to $5M through its partner-bank sweep network.

- Yield: Accounts don't earn interest on their own; yield requires Mercury Treasury, a separate product needing at least $250,000 held across Mercury accounts.

- Limitations: International payments reach a limited set of countries, and recurring invoices and reimbursements sit behind the paid Plus plan.

3. Novo

A zero-fee checking platform for freelancers, solopreneurs, and very small businesses.

- Cost: No monthly fees, no minimum balance, and ATM fee refunds up to $7/month.

- Built-in tools: Invoicing included.

- Limitations: No interest on deposits, no outbound international wires, weaker QuickBooks integration than competitors, and FDIC coverage only up to the standard $250k.

4. Relay

A multi-account platform for segmenting cash, commonly used for Profit First budgeting.

- Account structure: Up to 20 checking accounts and two savings accounts under one login, with FDIC coverage up to $3M through Thread Bank's sweep network.

- Integrations: QuickBooks Online and Xero sync on every tier, including the free plan.

- Limitations: Card cashback, free wires, and automated bill pay require paid plans ($30/month Grow, $90/month Scale), and there's no built-in lending or cash advance.

5. Bluevine

A checking account paired with lending, aimed at businesses that want both from one provider.

- Lending: Line of credit up to $250,000, available to businesses with at least six months of operating history and $10,000/month in revenue.

- Limitations: No real-time payments through FedNow or RTP.

- Cash handling: Cash deposits run up to $4.95 per transaction through Green Dot locations.

6. Airwallex

A cross-border platform for businesses with multi-currency operations.

- Multi-currency: Holds 20+ currencies and sends to 150+ countries through local rails and SWIFT, with employee corporate cards that charge no fee on same-currency spend.

- FX pricing: Conversions carry a markup of roughly 0.4% to 0.6% over the interbank rate, not pure interbank pricing.

- Limitations: No lines of credit, and limited transaction history visibility can make reconciliation a chore.

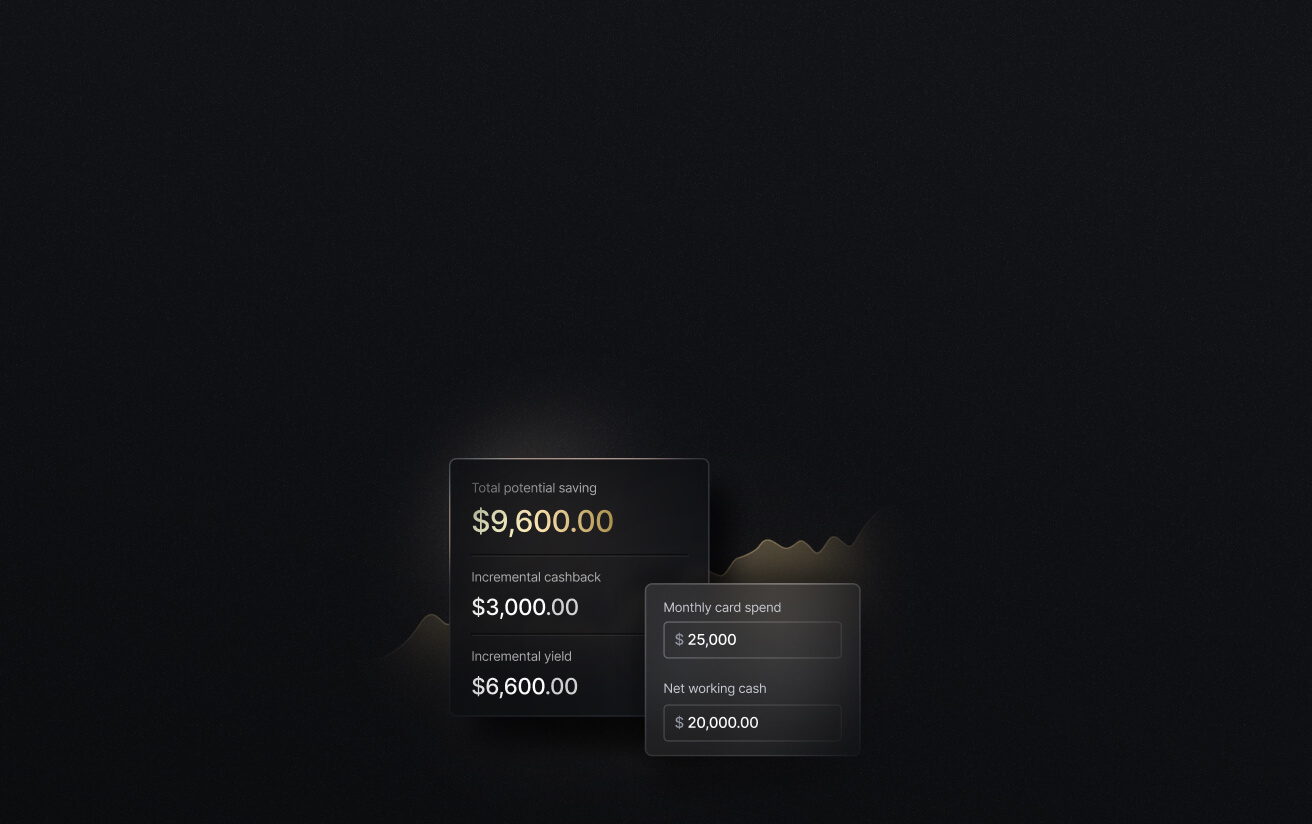

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

How to Choose the Best Business Banking Platform for Your Small Business

The right platform depends less on which has the longest feature list and more on how your business runs day to day. Here's how the options above sort out by the kind of operator you are:

If Your Small Business Handles Cash

Take a salon, a food truck, or a corner retail shop that rings up a big share of sales in cash. That cash has to get deposited somewhere, and most platforms on this list are digital-first with no way to accept cash deposits. A cash-heavy business is the one case where a neobank may fall short. A traditional bank with branches, or a platform with retail deposit partnerships through networks like Green Dot, will handle the deposits better than anything built purely for digital workflows.

If You Make International Payments

Picture an ecommerce brand buying inventory from suppliers in three countries and paying overseas contractors every month. FX markups are the cost that quietly eats margin, so conversion pricing and cross-border rails should drive the decision. Airwallex specializes here, holding 20+ currencies and pricing conversions within about half a percent of interbank rates; however, holding multiple currencies at once can expose your business to FX rate swings. Slash suits the same brand if it would rather skip a separate FX tool, with SWIFT wires to 180+ countries and stablecoin rails that settle cross-border USD in minutes from one account.

If You Need Credit Alongside Your Account

Consider an agency that fronts media spend for clients before invoices clear, or a wholesaler paying for a large inventory order months ahead of revenue. Both need a credit line next to the operating account rather than a separate loan application at another lender. Bluevine builds around this pairing, with checking plus a revolving line of credit up to $250,000. Slash offers working capital financing on 30-, 60-, or 90-day terms inside the platform, so the same operator can draw on short-term capital without leaving their account.

If You Manage Spending Across a Team

Think of a 25-person startup where a dozen people carry cards and expenses stack up by Friday. Card controls and expense tracking start to matter more than the checking account, so unlimited card issuance, per-card limits, approval workflows, and accounting sync become the priorities. A bare-bones account like Novo runs out of room fast here. With Slash, you can issue unlimited virtual cards, set spend limits and merchant controls per card, and view every transaction in real time.

Make the Right Financial Move with Slash

Each platform here does something well. Some are strong on international payments but offer no line of credit. Others have plenty of payment rails but a thin corporate card. A few cover almost everything, but lock the useful parts behind paid tiers and per-transaction fees. Slash brings these capabilities together on one platform at a low cost.

Slash also covers the parts of running a business that usually mean another subscription. You can create and send invoices, track which ones have been paid, and follow up on the ones that haven't, all from the same place you bank. Bill pay works the same way, with scheduled payments and approval steps so money doesn't go out the door without a check. Both tie directly into your accounts and sync back to your accounting software, so receivables and payables stay current without manual entry.

Here’s what else when you get when you make the switch to Slash:

- Slash Visa® Platinum Card: Set customizable spending controls and issue unlimited virtual cards for team expenses, vendor payments, and subscriptions, with up to 2% cash back on business purchases.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to bridge cash flow gaps.

- High-yield treasury: Earn up to 3.76% annualized on idle funds through BlackRock and Morgan Stanley money market funds, managed directly within your Slash account.

- Diverse payment methods: Card spend, global ACH, international wires to 180+ countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- Global USD: The Slash Global USD Account gives foreign founders access to USD without forming a US entity.³ Balances are backed by Slash's USDSL stablecoin, matched one-to-one with the US dollar.

Reach out today to see how Slash can serve as the all-in-one banking platform for your small business.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Business Banking Platform FAQs

What is the difference between a business banking platform and a traditional bank?

Business banking platforms are digital-first and typically operate without branches, partnering with chartered banks to hold deposits. They're built around the workflows of running a business, with accounting integrations, multi-user access, expense tracking, and API access that traditional banks have been slower to prioritize.

Fintech’s Second Wave: How Silicon Valley Rebuilt Banking

Are business banking platforms FDIC insured?

Most are, through partner-bank relationships. Standard FDIC coverage is $250,000 per depositor, per bank. Many neobanks extend this well beyond the standard limit by sweeping deposits across multiple partner banks, in some cases into the hundreds of millions.

Can I connect a business banking platform to my accounting software?

In most cases, yes. Nearly all of these platforms integrate with QuickBooks Online and Xero, and some also connect with NetSuite, Sage Intacct, and other mid-market ERPs.

The Best Accounting Automation Software Tools in 2026

Read more from us