The Top No-Fee Business Checking Accounts for Different Business Needs

Why pay the bank money just to keep it there? Monthly maintenance fees, minimum balance fees, transaction fees, debit card replacement fees, and payment processing fees—traditional business checking accounts have a way of nickel-and-diming small business owners who are just trying to run their companies. A free business checking account can fix most of that, but only if you know what to look for.

Free business checking has become the norm rather than the exception, especially among digital platforms that don’t carry the overhead of physical branches. But "no-fee" means different things across business account providers. Some waive monthly fees but charge for wires. Others bundle in free ACH but cap free transactions or limit cash deposits. Some offer a free business account but charge for the debit card, the savings account, or any feature you actually want to use. That means choosing the right business account depends heavily on how you’ll use it: an outbound wire fee doesn’t matter much if you just need somewhere to park cash, but it matters a lot if you pay vendors weekly.

This guide breaks down the top free business checking accounts and where each fits best, since the right answer for a sole proprietor looks nothing like the right answer for a growing e-commerce business. We’ll also look at Slash, a business banking platform that is free to open and use with no paywalled functionality.¹ That includes unlimited corporate card issuance, invoicing, bill pay, accounting integrations, and more from day one. For businesses doing higher outbound payment volume or significant card spend, Slash’s optional Pro plan unlocks unlimited fee-free domestic payments and elevated rewards, which can pay for itself through everyday activity. Read on to learn more.

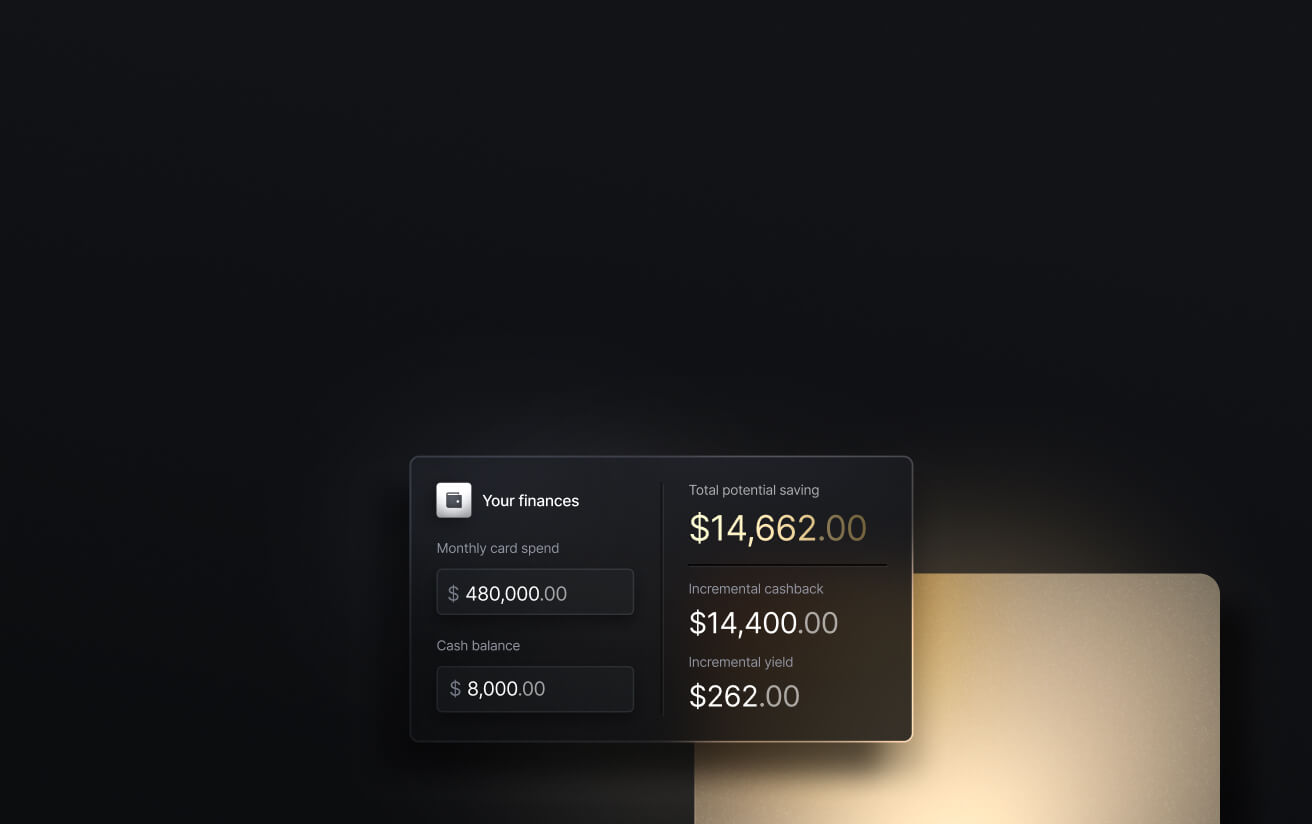

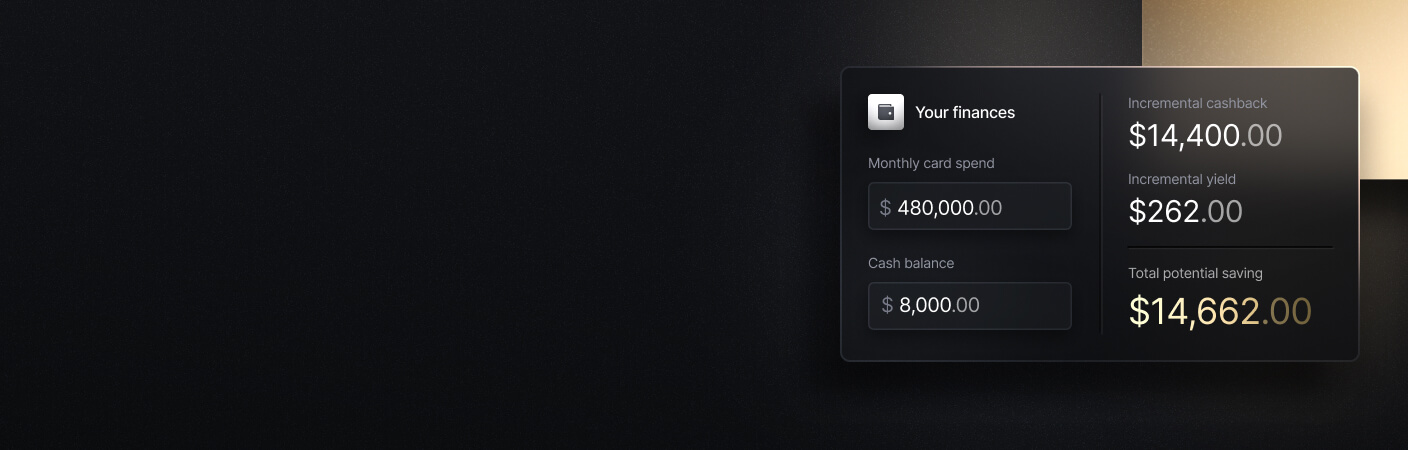

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What free business checking actually means

When a provider advertises a "free business checking account," what they usually mean is no monthly service fee on the account itself. That’s the recurring charge banks tack on for the privilege of holding an account open. But monthly maintenance fees are only the tip of the iceberg. Most banks will still charge different usage fees for all sorts of activities in your business bank account, even if the account itself is technically free.

The fees that tend to stick around on a "free" business account include:

- Wire fees on outgoing domestic and international transfers

- Overdraft fees, which can run $30 or more per incident at major banks

- Cash deposit fees once you exceed monthly limits

- ATM fees at out-of-network ATMs

- Foreign transaction fees on debit card spend abroad

- Surcharges for expedited or international payments

- Fees to move money from your business checking to a linked savings account at another bank

None of these fees tend to show up in the advertised "no-fee" claim. They show up on your monthly statement after you’ve already opened the business account and started using it. Even providers that are aggressive about cutting fees rarely eliminate all of them, because some operational fees correspond to real expenses. A domestic wire actually costs the sending bank money to process, and that cost gets passed through to the accountholder.

The same caveat applies to high-APY offers on a business savings account. A provider advertising 4% or higher yield usually has conditions attached: a minimum balance requirement, management fees, direct deposit activity thresholds, or some combination of all three. If your savings account doesn’t qualify in a given month, the rate tends to drop to offset the bank’s costs of managing the account.

So when you’re comparing free business accounts, you still should check where the fees exist. They do, at every business account provider. The real question is which operational costs are still in play and how that lines up with how your business operates. A free business checking account with no monthly fee but high wire fees is a great deal for a business that rarely wires money; it's a bad deal for one that wires constantly. The fit matters more than the marketing.

The 8 best free business checking accounts for modern companies

The free business checking label gets attached to a lot of accounts, but there's still some places where fees can sneak in or functional limitations can show up. Below is a list of 8 no-fee business account providers, including details on where the fees don't match the claims and how each stacks up as a daily driver for your finances:

Slash

A digital-first business banking platform that consolidates checking, treasury, corporate cards, and finance tooling into one dashboard. The Free plan has no paywalled functionality, which separates Slash from other competitors that gate features behind paid tiers.

- No monthly fees, no minimum balance

- Unlimited virtual and physical corporate cards, up to 2% cash back

- Invoicing (AR) and bill pay (AP) included on the free plan

- Xero, Sage Intacct, NetSuite, and Quickbooks integrations

- SWIFT wires to 180+ countries and USDC/USDT stablecoin transfers

- Treasury accounts earning up to 3.79% annualized yield through Morgan Stanley and BlackRock money market funds, with no minimum balance to open⁶

- FDIC insurance coverage over $100M via Column N.A., Member FDIC, and Column’s Sweep Program Network Banks.²

The Pro plan ($25/month flat, not per user) adds unlimited fee-free domestic transfers and up to 2% cashback.

Bluevine

Bluevine business checking offers tiered pricing aimed at domestic businesses that keep large cash balances and want to earn interest on their business's checking account without opening a separate savings account at another bank.

- No monthly fee, no minimum balance on the Standard plan

- 1.3% APY on business account balances up to $250,000 on the Standard plan (requires meeting a monthly activity goal)

- 5 sub-accounts on Standard that function like a built-in savings account; 10 on Plus, 20 on Premier

- Built-in invoicing and Stripe-powered payment links

- Bluevine business debit card from Mastercard

Tradeoff: The headline 3.0% APY requires the $95/month Premier plan, and the Standard plan’s 1.3% APY caps at $250,000.

Novo

A basic free business checking account for freelancers, sole proprietors, and small businesses with simple needs. Novo is a member FDIC partner through Middlesex Federal Savings.

- No monthly fees, no minimum balance, no overdraft fees

- Up to $7/month in ATM fee refunds across network ATMs when using the business debit card

- Built-in invoicing and bill pay

- Novo Boost speeds up Stripe payouts

- Free mobile deposits for paper checks

Tradeoff: No yield, no business savings account, no treasury product. Novo is checking-only with no way to earn interest and doesn’t accept cash deposits.

Relay

A free business checking platform designed for small businesses that want to split their cash across multiple sub-accounts, popular with operators using the Profit First budgeting method.

- No monthly fee, no minimum balance on the Starter business account

- Up to 50 business debit cards with spend controls

- QuickBooks integration and Xero on all plans

- Free incoming wires and free ATM withdrawals at Allpoint ATMs

Tradeoff: Automated bill pay is gated behind the $30/month Grow plan, which means businesses managing recurring vendor payments need to upgrade or handle payables manually.

Mercury

A bank + financial platform built for venture-backed startups and software companies, with strong developer tools and API access.

- No monthly fees, no minimum balance

- Up to $5M in FDIC insurance through multi-bank insured cash sweep

- Mercury IO corporate credit card, up to 1.5% cash back

- Mainly U.S. only, limited international support

Tradeoff: No treasury or yield product on the free business account. Idle cash sits flat unless you opt into Mercury Treasury, which requires a $250,000 minimum balance across all Mercury accounts.

American Express Business Checking

The American Express business checking account earns Membership Rewards points on debit card spend, best for businesses already in the Amex ecosystem.

- No monthly fees, no minimum balance

- 1 Membership Rewards point per $2 spent on the business debit card

- Fee-free withdrawals at 70,000+ Allpoint ATMs and MoneyPass ATMs nationwide

- 24/7 customer support for accountholders

Tradeoff: Limited to just a QuickBooks integration for accounting. No native invoicing, bill pay, or AR/AP tooling on the business account; you’d need to layer those in through other software.

U.S. Bank Business Essentials

A free business checking account from a major national bank, useful for businesses that want branch access along with a no-fee business account. A reasonable alternative to a local credit union if you want a brick-and-mortar relationship.

- No monthly maintenance fee, no minimum balance

- Unlimited digital transactions (ACH, debit card purchases, transfers, mobile deposits)

- Free mobile card reader for new accounts

- 24/7 live customer support

- Access to a separate U.S. Bank business savings account through the same login

Tradeoff: ACH transfers to external payees cost $1 each, and outgoing international wire fees run up to $70.

Axos Bank

Axos Bank offers a free online-only business checking account from a chartered digital bank.

- No monthly fees, no minimum balance

- Unlimited domestic ATM fee reimbursements when using the business debit card

- Free incoming wires (domestic and international)

- Expanded FDIC insurance via IntraFi insured cash sweep network

Tradeoff: No native invoicing, bill pay, or accounting integrations on the free tier. Businesses would need to add separate software to manage their bookkeeping.

Get more from your business checking account with Slash

It’s easy to compare business checking accounts on the monthly fee alone and call it done. But once you start running a business through one of these accounts, the costs show up elsewhere: in wire fees, in features locked behind a paid tier, and in the third-party software you have to add on because the bank doesn’t include it. With Slash, there’s no paywall between you and what you need to get done.

Slash’s free plan includes the full scope of the platform’s functionality: accounts payable and receivable tools, real-time cash flow metrics, accounting integrations, merchant services for major online marketplaces, an integrated treasury account, and unlimited cashback-earning corporate cards. Here’s the full breakdown of what you get when you switch your business account to Slash:

- Slash Visa® Platinum Card: Set customizable spending controls and issue unlimited virtual cards for team expenses, vendor payments, and subscriptions. Earn up to 2% cashback on business card purchases.⁷

- Native cryptocurrency support: Hold, send, and receive USDC and USDT across eight supported blockchains for faster, lower-cost global payments.⁴

- Diverse payment methods: Virtual card payments, global ACH, international wires to 180+ countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- AI-powered finance: Twin, our built-in AI agent, handles complex tasks from natural-language prompts like issuing cards, paying invoices, reviewing cash flow, and more.

- Global USD: The Slash Global USD Account gives foreign founders access to USD without forming a US entity.³ Balances are backed by Slash’s USDSL stablecoin, matched one-to-one with the US dollar.

- Working capital financing: Access short-term financing with 30-, 60-, or 90-day repayment terms to bridge cash flow gaps.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What services can still trigger fees on a free business checking account?

Most free business checking accounts only waive the monthly service fee on the business account itself. Wires, overdraft fees, cash deposits, out-of-network ATM withdrawals, debit card foreign transaction fees, expedited payments, and same-day ACH can all still carry charges depending on the provider. The exact list varies, so it’s worth reviewing the full fee schedule on any business account before opening it.

What's an FX Fee? Everything You Need to Know to Save on International Payments

How Wire Transfer Fees Work (and How to Lower Them)

Do free business checking accounts limit transfers or payment volume?

Some do. A few business account providers cap free ACH transfers, wire transfers, debit card transactions, or teller transactions per month and charge per-item transaction fees once you hit the limit. Others offer unlimited transactions but draw the line elsewhere, like wire counts or mobile deposits. If your small business processes meaningful volume, the per-transaction structure usually matters more than the monthly fee on the business account.

Why do some free business checking accounts advertise high APY?

High APY is often used as a hook to make a free business checking account look more competitive against a dedicated business savings account. The advertised rate usually comes with conditions (minimum balances, monthly debit card activity requirements, or paid plan tiers), and the rate you actually earn can be significantly lower if you don’t meet them. Read the fine print to see what qualifies before assuming the headline number applies to your business account.

The Top 7 Platforms for Integrated Treasury, Forecasting, and High-Yield Accounts

Can sole proprietors open a free business checking account?

Yes. Most free business checking providers accept sole proprietors, though some require an EIN while others let you apply with an SSN. Bluevine business checking and Novo support sole proprietors with a free business account, as do most traditional bank business checking accounts. Slash currently does not support sole proprietors.

The 5 Best Business Bank Accounts if You're Self-Employed

Are free business checking accounts FDIC insured?

Yes. Even when the business account provider is a fintech rather than a chartered bank, deposits are held at a member FDIC partner bank and protected up to $250,000 per depositor. Many free business checking providers go further by using insured cash sweep networks that extend FDIC insurance coverage into the millions across multiple partner banks.

FDIC Insurance Guide: Limits, Protection Strategies, and How to Elevate Your Coverage

What’s the difference between a free business checking account and a business savings account?

A free business checking account is built for day-to-day operations: paying vendors, running payroll, accepting debit card payments. A business savings account is built to hold reserve cash you don’t need immediately, and typically pays interest in exchange for some withdrawal limits. Some modern business checking account providers blur this line by paying yield on the checking balance itself, reducing the need for a separate savings account at another bank.