Top Fintech Platforms for Multi-Entity Banking in 2026

Multi-entity banking is a way to oversee the finances of multiple legal entities from a single dashboard. It eliminates the need to log into separate banking relationships for each subsidiary or holding company, giving you a consolidated picture of your cash and activity while still honoring the distinct legal boundaries of each business you oversee.

A multi-entity setup can be especially valuable for founders whose growth has added operational complexity over time: an entrepreneur running three brands under separate LLCs, an investor overseeing portfolio companies with independent books, or a business owner who has created subsidiaries for liability protection and tax strategy. If you’ve ever pieced together your cash position across multiple bank logins and spreadsheets, you have likely experienced the frustration multi-entity platforms are built to solve.

In this guide, we break down several of the leading platforms for multi-entity financial management, including Slash. Slash enables you to toggle between dedicated dashboards for each business you oversee. Every subsidiary can maintain its own virtual subaccounts, corporate charge cards, integrated treasury, and cryptocurrency wallets, ensuring clean separation while maintaining centralized oversight.¹, ⁴

The best multi-entity banking platforms for businesses

Not all fintech platforms are built to support businesses operating across multiple legal entities. Below, we compare several leading options, highlighting where each stands out and where limitations may emerge as your organizational structure becomes more complex:

Slash

Slash is a modern financial operations platform that brings corporate cards, expense management, payments, and integrations together under one roof. Slash excels in industry-specific banking solutions, particularly for businesses with diverse spending patterns, web-native businesses, those who need highly compliant financial infrastructure, or those with international operations.

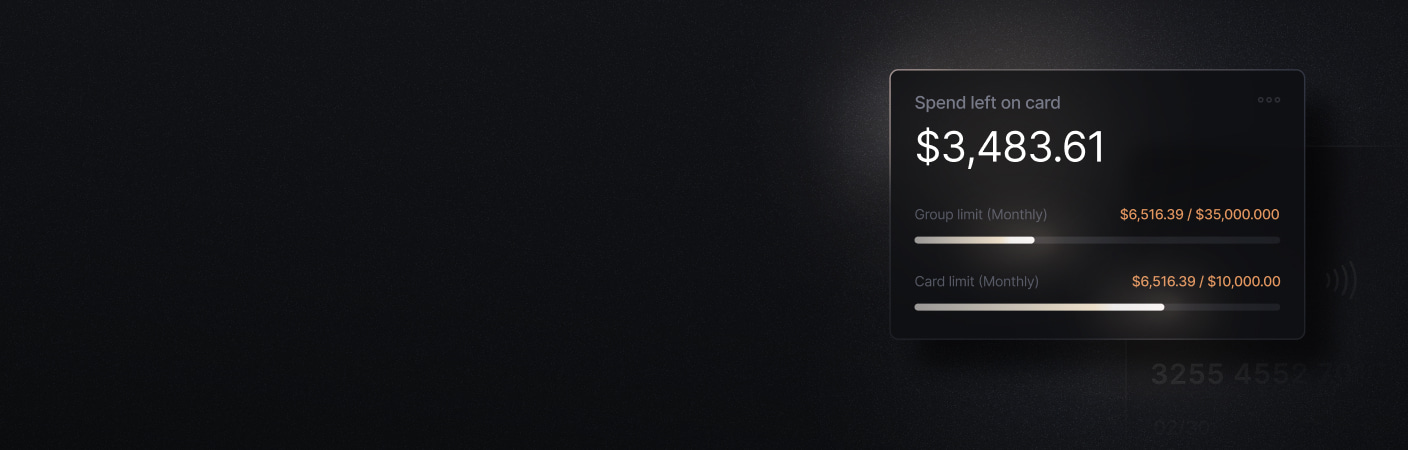

- Configurable virtual accounts: Businesses can spin up unlimited virtual accounts tailored to specific purposes, entities, or revenue streams, making it easy to segment and track cash flows without opening separate bank accounts.

- High-yield treasury: Slash provides treasury accounts powered by money market funds from BlackRock and Morgan Stanley, currently earning a competitive 3.83% annualized yield.⁶

- Unified multi-entity dashboard: A single interface gives teams visibility across all entities, accounts, and transactions, eliminating the need to toggle between platforms or consolidate data manually.

- Third-party perks: Slash offers $1m+ in discounts on popular business tools and services, adding extra value beyond core banking functionality.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Bluevine

Bluevine takes a more conventional approach to business banking, with debit cards and the option to send physical checks. While this familiarity may appeal to some businesses, it comes at the cost of modern capabilities.

- Limited payment methods: All payment activity runs through conventional bank transfers, which can mean slower settlement times compared to platforms offering instant payment rails or cryptocurrency capabilities.

- Limited subaccount creation: Bluevine limits the number of virtual subaccounts users can create based on their pricing tier. Their free plan only enables users to create up to 5 subaccounts; while creating up to 20 can require a fee of $95/month.

- Traditional feature set only: Debit card access and check mailing may suit straightforward operations, but businesses needing charge cards or credit cards may need an additional provider.

Brex

Brex positions itself as a financial platform for high-growth companies, but its rewards structure and eligibility requirements can be limiting for many businesses.

- Points-based rewards model: Brex assigns a set value to its rewards points, with redemption rates that can differ based on usage. In some cases, this may result in lower effective returns compared to flat-rate cashback cards.

- High barrier to entry: Eligibility is restricted to venture-backed startups or businesses generating at least $1 million in annual revenue, excluding a large portion of the SMB market.

- Feature gating by plan tier: Several key capabilities are locked behind premium subscription levels, which can make the platform cost-prohibitive for smaller or leaner teams.

Mercury

Mercury is a popular digital banking option for startups, particularly those formed in the United States. However, its structure and eligibility criteria can create friction for globally distributed or multi-entity organizations.

- Selective approval criteria: Mercury primarily serves U.S.-registered businesses with domestic operations. Founders operating non-U.S. entities or international holding structures may face additional hurdles or be unable to open accounts.

- No cryptocurrency or stablecoin support: The platform does not offer native crypto or stablecoin capabilities, limiting flexibility for businesses that transact in digital assets or operate on blockchain-based payment rails.

- Limited multi-entity depth: While you can open separate accounts for different entities, Mercury does not provide the same consolidated, cross-entity financial controls and treasury tooling found in more purpose-built multi-entity platforms.

Wise Business

Wise Business is best known for its transparent foreign exchange pricing, but it operates more as a payments layer than a standalone bank. Businesses still need to maintain separate primary accounts and assemble additional tools to fill operational gaps.

- Not a full banking replacement: Wise does not offer lending, corporate cards, or advanced cash management features. It requires external bank or card accounts to function, adding operational complexity.

- Limited currency and payment scope: Despite its global reputation, business accounts support just 21 currencies and can accept payments in only 18, even with local account details such as U.K. sort codes or EU IBANs.

- Fees can add up quickly: Wise promotes mid-market exchange rates, but still layers on transfer and conversion fees starting around 0.57%, plus SWIFT surcharges for non-SEPA transfers. Inbound USD wires and SWIFT payments cost $6.11 each.

Venn

Venn is built with Canadian businesses in mind, offering multi-currency account holding (including USD) but not designed to serve U.S.-based companies as a primary banking platform.

- Modest rewards and yield: Cashback tops out at just 1%, and treasury interest on idle balances falls below the 3% mark, trailing the rates offered by other alternatives.

- Narrower feature depth: Beyond payments and currency management, Venn doesn't yet match the breadth of tools (such as advanced analytics, treasury products, or deep integrations) found on more mature platforms.

Key features to look for in a multi-entity banking platform

Not all multi-entity platforms function exactly the same. Some simply allow you to open multiple accounts; others give complete entity separation. Some offer dedicated treasury accounts and global payment capabilities; others do not. Knowing which features actually improve visibility, control, and efficiency can help you choose a platform that fits your business’s structure as it scales:

Consolidated dashboards and account switching

The whole point of multi-entity banking is unified visibility. Look for platforms that let you see balances, transactions, and pending approvals across all entities from a single view, with the ability to switch between entities quickly. If toggling between accounts requires logging out and back in, or navigating through multiple screens, the platform isn't solving the core problem.

Intercompany transfers and automation

Moving money between entities is one of the most common pain points for multi-entity businesses. The strongest platforms let you automate intercompany transfers with preset rules, reducing manual work and ensuring accurate records. This matters especially at month-end when reconciliation across entities can consume hours of finance team time.

Role-based access and approval workflows

As your organization grows, you need granular control over who can see and do what across each entity. Look for platforms like Slash that offer role-based permissions, multi-level approval workflows, and the ability to set different policies for different entities. This is especially important for businesses where different entities have different spending patterns or compliance requirements.

FDIC coverage and deposit safety

Most fintech platforms are not banks themselves. They partner with FDIC-member institutions (often called sponsor banks or partner banks) to hold your deposits. This means FDIC insurance comes from the partner bank, not the fintech's digital interface. Slash, for instance, uses Column N.A.’s insured cash sweep networks to extend coverage well beyond the standard $250,000 per depositor, with FDIC coverage into the hundreds of millions per account.²

API access and integrations

If your finance team relies on accounting software, ERPs, or custom internal tools, API access is non-negotiable. Slash’s API capabilities let you automate data flows between your banking platform and the rest of your tech stack, as well as giving you the ability to automate virtual account and card creation, and sync with QuickBooks Online.

Treasury management and multi-currency support

For businesses with significant cash reserves or international operations, treasury features matter. This includes the ability to earn yield on idle balances, manage liquidity across entities, and hold or transact in multiple currencies. Platforms vary widely here: some offer high-yield treasury accounts with institutional-grade investment options, while others focus primarily on competitive FX rates for cross-border payments.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How to choose the right multi-entity platform for your business

Not every multi-entity setup looks the same. A holding company with three domestic LLCs has very different needs than an ecommerce seller operating across multiple countries. The right platform depends less on brand recognition and more on how well the product aligns with your operational complexity. Here are the key factors to evaluate:

1. Entity Separation Without Fragmentation

At a minimum, each legal entity should have clean financial separation. That means distinct accounts, cards, transaction histories, and reporting. The real differentiator is whether you can maintain that separation while still viewing everything centrally. Look for:

- A unified dashboard across entities

- Consolidated reporting

- Role-based permissions by entity

- The ability to move funds between entities cleanly when appropriate

If you still need spreadsheets to understand your total cash position, the platform is not solving the full problem.

2. Treasury and Yield on Idle Cash

Multi-entity businesses often hold meaningful idle balances across subsidiaries. Small yield differences compound quickly when spread across multiple accounts. To assess your treasury needs, consider questions like:

- Are funds sitting in low-yield checking accounts?

- Is there access to treasury products or money market funds?

- Can you manage liquidity across entities efficiently?

A platform that optimizes cash across your structure can materially improve returns without increasing risk.

3. Card Infrastructure and Spend Controls

If multiple teams operate under different entities, card management becomes critical. Strong spend controls reduce cross-entity confusion and simplify accounting at month-end. Here are some questions to ask about a multi-entity platform’s card management:

- Are corporate charge cards or credit cards available, or only debit?

- Can you issue cards per entity?

- Do spend limits and approval workflows operate independently per subsidiary?

- Is expense tracking built in, or does it require another tool?

4. International Capabilities

Many multi-entity structures exist specifically for international operations, and platforms that only support domestic entities may limit your growth plans. If that applies to you, confirm:

- Are non-U.S. entities supported?

- Can you hold and move funds in multiple currencies?

- Are there stablecoin or crypto payment options if relevant to your business model?

- What are the FX and wire fees?

5. Eligibility Requirements and Scaling Flexibility

Some platforms restrict access based on revenue thresholds, venture backing, or geography. Others lock core features behind premium pricing tiers. Before committing, ask:

- Will this platform still work if we add more entities?

- Are there revenue minimums or structural limitations?

- Does pricing scale predictably as we grow?

Switching financial infrastructure later is painful. It’s better to choose a system that can grow with your structure.

How Slash supports multi-entity businesses

From a single login, you can switch between dedicated dashboards for each company, with full visibility into balances, transactions, and card activity in real time. Every entity maintains its own bank account structure, allowing for clean legal and accounting separation while still giving leadership a consolidated view across the entire organization. This eliminates the need to work with multiple institutions or manually assemble data just to understand your overall cash position.

Each entity can also operate with its own financial stack inside Slash. You can create virtual subaccounts to segment revenue streams and allocate budgets, all without opening additional external bank accounts. Intercompany transfers make it simple to move funds between subsidiaries when appropriate, with clear records for reconciliation. Deposits are held with Slash’s partner bank, Column N.A., and are backed by millions in FDIC-insurance, providing the stability of traditional banking with cutting-edge protection.

Beyond core multi-entity banking, Slash also offers:

- Unlimited virtual cards per entity: Issue cards for team members, vendors, and subscriptions with customizable spend controls and up to 2% cashback.

- High-yield treasury: Earn up to 3.83% annualized yield on idle funds through money market investments from BlackRock and Morgan Stanley.

- Streamlined integrations: Native QuickBooks sync keeps each entity’s books accurate, while Plaid connectivity enables secure integration with external banks and financial services across your organization.

- Global payments: Send wires to more than 180 countries with support for ACH, RTP, and FedNow. On and off ramp funds into USD-pegged stablecoins for fast, low-cost transfers outside of traditional banking channels. Pro users pay no additional per-transaction fees.3

- Enterprise-grade compliance: SOC 2 Type II and PCI DSS certified security for every Slash account across all your entities.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What features are essential for managing multiple entities efficiently?

At a minimum, you should look for a unified dashboard with real-time visibility across entities and the ability to easily switch between them.

How do fintech platforms handle FDIC insurance across multiple entities?

Fintech platforms partner with FDIC-member banks to hold deposits. Coverage is provided through the partner bank under FDIC pass-through rules, meaning insurance applies to each eligible depositor's balances. Some platforms like Slash use sweep networks to distribute deposits across multiple banks, extending coverage beyond the standard $250,000 limit.

How do I know if a platform's multi-entity support is mature?

Look for dedicated product pages and documentation around multi-entity features, ask during demos how long they've offered multi-entity management, and request references from current customers with a similar entity structure.

Read more from us