Capital One vs. American Express vs. Slash: Comparing Cards to Find the Best Fit for Your Spending

American Express and Capital One are the second and third largest credit card companies in the U.S., respectively. However, they’re pretty different when you get into the meat of who they are and what they offer. American Express is a long-established corporate card brand known for pioneering charge cards and premium travel rewards that appeal to high-spending cardholders. Capital One came decades later and built its reputation by using information technology and data-driven underwriting to create customized card offers for different customer segments.

For business owners, choosing between Capital One and American Express is ultimately about how well each card supports their day-to-day spending and long-term growth. Corporate cards can allow you to control your team’s expenses, earn rewards, and keep an eye on your overall company spend. While both banks offer helpful cards, their actual value can be diminished by outdated expense management tools and complex redemption options.

Newer banking platforms like Slash represent the next evolution of the corporate card industry, defined by agentic AI tools, unified financial dashboards, and granular card controls.¹ In this guide, we'll compare the top American Express and Capital One cards and evaluate how they stack up against the Slash Visa® Platinum Card. At the same time, we’ll take a look at the features each provider offers surrounding the cards themselves.

What is American Express?

American Express is a legacy financial institution with roots dating all the way back to 1850, when it was an express freight and mail delivery service in Buffalo, New York. Today, it’s played a foundational role in shaping the modern credit card industry. A major milestone came in 1991 with the launch of Membership Rewards, one of America’s first points-based credit card rewards programs. Membership Rewards allowed cardholders to redeem points across a wide range of travel, retail, and lifestyle categories rather than being locked into a single airline or hotel program.

Unlike most issuers, American Express operates as a monoline credit card company, meaning its business is centered almost entirely on card products and payments rather than traditional deposit banking. Amex also runs a closed-loop payment network, handling transaction processing internally instead of relying on shared networks like Visa or Mastercard. One downside of this closed network is its more limited global acceptance compared to typical card networks. Unlike Capital One, Amex doesn’t operate physical bank branches, meaning you’ll have to manage your account digitally or over the phone.

Today, American Express offers a range of business credit cards and charge cards, including:

American Express Business Platinum Card

The Business Platinum Card is American Express's premier business offering, with high rewards-earning potential, expansive perks, and a wide range of statement credits. Cardholders receive access to American Express Travel and concierge services, which can assist with travel booking, dining, and entertainment. The Business Platinum Card is a charge card, not a traditional credit card, meaning balances must be paid in full each billing cycle rather than carried forward with interest. It also carries one of the highest annual fees for card membership in the industry, at $895 a year, and tends to require excellent credit (~690-850) to qualify.

This card’s rewards are points-based rather than cash back based, and they center around certain spending categories. Namely, cardholders can earn 5x points on flights and prepaid hotels using the Amex travel portal. If you’re part of a high-travel business, you can get solid value out of the card, but points redemption can be a little trickier than flat rate cash back.

American Express Blue Business Cash Card

The Blue Business Cash Card is one of Amex's more accessible business credit cards. It has no annual fee, and personal credit requirements aren’t as strict. Instead of earning Membership Rewards points, the card offers cash back: 2% on the first $50,000 in eligible purchases each calendar year, then 1% thereafter. This makes it a more straightforward option for businesses that prefer the ability to rollover balances and earn simple cash back on purchases they don’t have to target towards specific categories.

What is Capital One?

Capital One was founded in 1994 as a monoline credit card company. Unlike many banks at the time, which typically offered uniform pricing and terms across customers, Capital One built its early growth around information technology and risk modeling. They were among the first to use customer data to tailor card products, interest rates, and rewards to different segments. In 2005, the company expanded beyond cards into branch-based banking, marking its transition into a full-service consumer and business bank.

Over time, Capital One has continued to grow through both organic expansion and large acquisitions. They launched Capital One Travel in 2021 as a rival to other travel portals from Amex and Chase. In May 2025, Capital One acquired Discover, which was a move that further strengthened its position in the card industry.

For businesses, Capital One is known for a relatively small but popular lineup of rewards-focused cards, including:

Capital One Spark Business Cards

Capital One offers several Spark cards designed for different credit profiles and spending needs. The Spark 1% Classic is a starter card mainly tailored for applicants with fair credit. As the name indicates, you can earn 1% cash back on all purchases, but you can earn 5% cash back on hotels and rental cards booked through their travel portal.

More competitive options, such as the Spark 1.5% Cash Select and Spark 2% Cash Plus, are geared toward applicants with good to excellent credit. Shrewd readers will correctly guess that these cards earn cash back ranging from 1.5% to 2%.

Capital One Venture X Business Card

The Capital One Venture X Business card is Capital One's flagship business offering. It’s a charge card that earns Capital One Miles on purchases and is designed for businesses with significant travel spend. While it doesn’t match the breadth of premium perks offered by the Amex Business Platinum, it includes valuable benefits such as travel credits and lounge access. The Venture X Business card currently carries an annual fee of $395, which isn’t cheap, but it’s a lower total than some other premium travel cards in the space.

How do American Express and Capital One Compare?

Let’s start with an at-a-glance overview of Capital One and American Express’s offerings, then we’ll break down the details:

Rewards

American Express’s Membership Rewards program is a points-based system that allows redemption for travel rewards, statement credits, gift cards, and select perks. Cards like the Amex Platinum earn up to 5x points on airline flights and prepaid hotels booked through Amex Travel, but most everyday business purchases earn just 1x points. As a result, there’s not a lot of reward value for companies that don’t travel much

Capital One's rewards vary by card. The Venture X Business card earns travel miles, with elevated rates of up to 10x on hotels and rental cars and 5x on airline flights booked through Capital One Travel, plus 2x miles on all other purchases. Spark Cards, by contrast, generally focus on straightforward cash back rather than points or miles.

Meanwhile, the Slash Card can earn up to 2% cash back on business spending with no category optimization, travel portals, or redemption tables required. Instead of maximizing rewards points through travel portals or bonus categories, Slash delivers consistent, predictable value across all eligible purchases, making it a valuable option for teams that like earning strong capital without the extra effort.

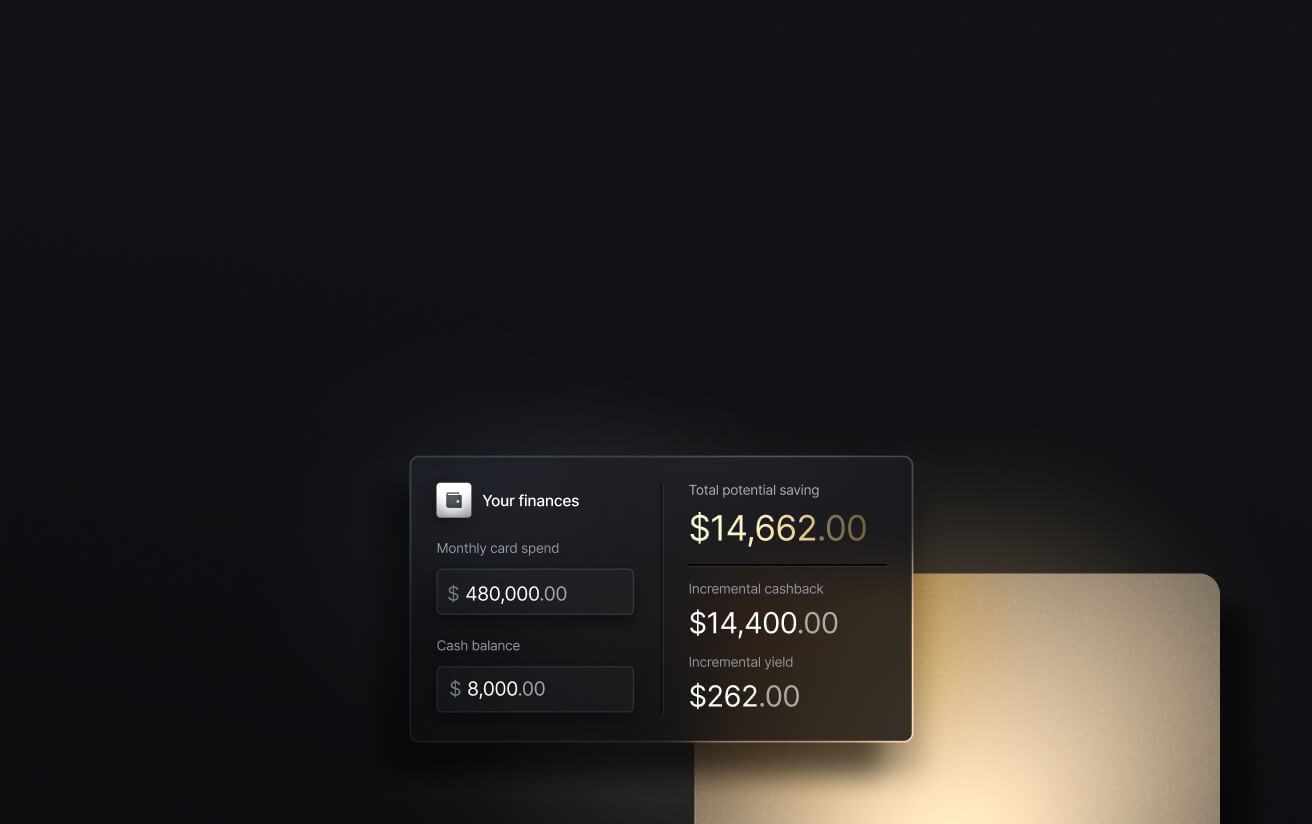

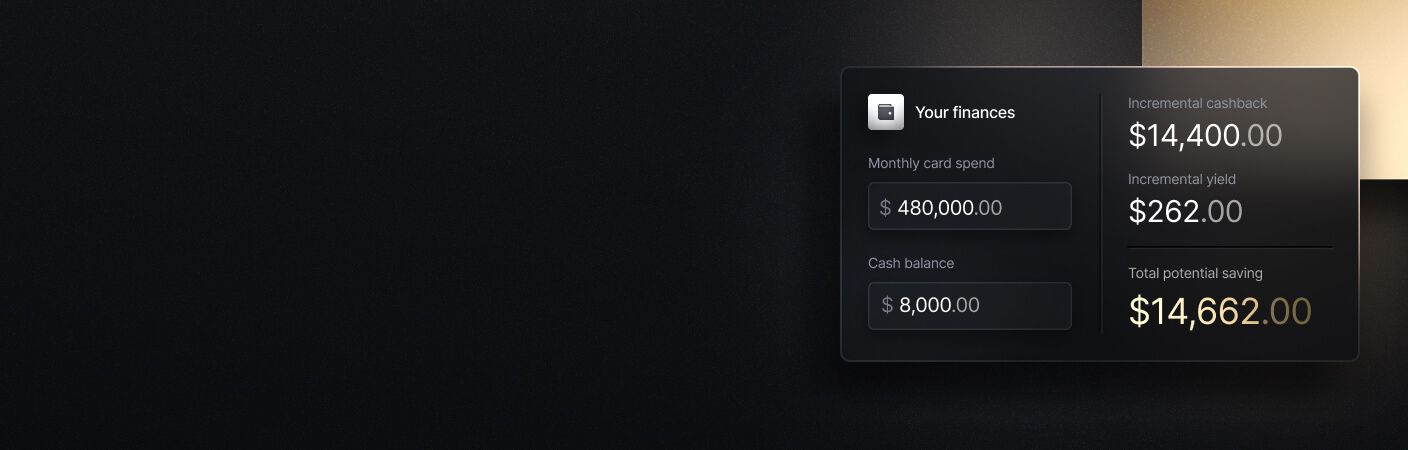

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Annual fees

Amex's premium business cards come with some of the highest annual fees in the industry. The American Express Platinum Card charges $895/year for the main card, with each additional Employee Business Platinum Card costing an extra $400/year. Some of Amex's other non-premium options, like the Blue Business Cash Card, have no annual fee.

Capital One's fees are more mixed. Several Spark cards have no annual fee, while the Spark 2% Cash Plus charges $150/year. As a premium travel-centric card, the Venture X Business Card carries a $395 annual fee for card membership.

Redemption options

As valuable as high rewards points are, the way you redeem them can also be important. American Express allows points to be redeemed through Amex Travel, converted to statement credits or cash back, or used to purchase gift cards. Redemption values vary widely, typically ranging from roughly $0.007 to $0.02 per point depending on how they’re used.

Capital One Miles can be redeemed through Capital One Travel, used to cover recent travel purchases on your statement, or redeemed for cash back and gift cards. Cash-back redemptions generally convert at a lower rate, often between $0.005 and $0.016 per mile, depending on the method.

Slash, on the other hand, eliminates the guesswork and calculations around rewards. Cash back is earned directly, so businesses don't have to navigate portals or pick specific purchases to get their full value.

Card-related benefits

Premium Amex cards, such as the Business Platinum, include extensive travel perks like credits for TSA PreCheck, monthly Uber Cash credits, access to Amex's Delta Sky Clubs, a Hertz Gold Plus membership, and much more. Many of these benefits are delivered through a patchwork of statement credits and partner programs.

The Capital One Venture X Business Card includes a similar lineup of perks. Cardholders get access to Capital One Lounges, a $300 annual travel credit, credits for TSA PreCheck, a Hertz Gold Plus membership, and more. In both of these cases, you’ll only get a large lineup of perks with their premium cards, which come with annual fees to offset their costs.

Account-related benefits

American Express comes with an “@ Work” account that allows admins to manage employee cards centrally, assign individual spending limits, review transaction data, and export to QuickBooks and other accounting platforms. Some Capital One cards, including the Venture X Business and Spark Cash Plus, include a built-in Expense Management feature that lets employees attach receipts, add notes, and auto-submit reports directly from the app. It also comes with an Accounts Payable tool that lets businesses send payments via card, ACH, or check to vendors from the Capital One dashboard.

While these tools are pretty respectable for legacy banks, they don’t stack up to what a modern platform like Slash offers. Slash allows business owners to issue unlimited virtual cards to their employees from both their desktop and mobile app. Admins can set spending limits, apply category-based rules, and manage controls at the individual or team level. All transaction data is captured automatically in the Slash dashboard, where businesses can view real-time spending analytics, receive alerts, and export clean data directly into several accounting solutions. Slash also supports payment rails like same-day ACH, RTP/FedNow, and stablecoins alongside traditional methods.⁴

Drawbacks

American Express and Capital One cards can struggle to match the effective cash value offered by Slash. Points-based rewards can be difficult to optimize, redemption values vary, and high annual fees may outweigh the benefits for many businesses. Lower-tier cash back cards usually cap earnings below Slash's up to 2% rate.

Applying in the first place can also be an issue. Capital One and American Express require excellent credit to open an account with their premium cards, which can be a barrier for some applicants. Outside of their rewards and accessibility, both institutions overall lack the modern card controls and centralized financial infrastructure that platforms like Slash are built around.

How to Choose the Right Corporate Card

American Express’s Business Platinum and Capital One’s Venture X Business are both premium, points-earning charge cards designed for frequent travelers. Each offers a broad set of travel-focused perks, including lounge access, credits for expedited security programs, and elevated rewards for bookings made through their respective travel portals. For businesses with regular air travel, these cards can make time spent in airports more convenient and comfortable.

The American Express Blue Business Cash is a solid option for businesses that prefer cash back over points. It earns 2% cash back (up to $50,000) and comes with some modern features like accounting integrations. However, Slash offers more cutting-edge features and up to 2% cash back with no earnings cap. For businesses spending more than $50,000 per year across their cards, which is common for mid-sized and larger teams, the Blue Business Cash can leave meaningful rewards on the table.

In the end, managing employee spending is easiest with the Slash card. It’s designed to save your business time and money by automating compliance checks, streamlining expense reporting, and giving you detailed analytics about spending across your company.

Make the Right Financial Move With Slash

While the Slash Visa® Platinum Card can be a game-changing perk for high-spend teams, Slash does a lot more than issue corporate cards. Slash is a unified business banking platform built to simplify how your company manages its finances. Rather than juggling separate systems for cards, payments, and expense tracking, Slash brings these workflows together on a single dashboard, reducing overhead and improving visibility.

The Slash Visa® Platinum Card is a charge card that can support businesses at every stage, from early growth to large-scale enterprises. The EIN-only application process doesn’t rely on a traditional personal credit check for account opening. Instead, Slash evaluates your company’s current financial position to determine eligibility and spending limits, making access to modern financial tools more practical for fast-growing teams that may not fit traditional underwriting models.

With a flat rate cash back structure, cardholders can earn up to 2% cash back on eligible expenses without having to worry about redeeming rewards points.

Alongside its corporate cards, Slash offers a full suite of business banking features, including:

- AI-powered finance: Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Native cryptocurrency support: Send and receive USD-pegged stablecoins USDC and USDT across eight supported blockchains for faster, lower-cost global payments.

- Diverse payment methods: Slash supports a wide range of payments designed for global entry, including card spend, global ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- Accounting integrations: Sync transaction data with QuickBooks Online, Xero, NetSuite, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Expense Management: Use the Slash Action Center as a one-stop spot for employees to see pending tasks assigned to them. These may include card requests, expense submissions, reimbursement reviews, and more.

If you're looking for a modern alternative to legacy business cards, explore Slash today to see how a single dashboard can overhaul your financial processes.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Are American Express cards hard to get?

Some American Express cards are tough to qualify for, especially premium options that require strong credit profiles and higher spending capacity. Entry-level Amex cards, however, can be more accessible.

What are the Easiest Business Credit Cards to Get? Top Picks and How to Get Yours Approved

Can I use American Express cards as easily as Capital One?

Capital One cards generally have broader global acceptance because they run on the Visa or Mastercard networks. American Express's global entry has improved over time, but may still be more limited in certain regions or with smaller merchants.

Who are Amex and Capital One's hotel and airline partners?

Amex Platinum cardholders get hotel perks like complimentary membership with Hilton Honors Gold, Marriott Bonvoy Gold Elite, and access to Amex's partner hotel collection. For flights, Amex cardholders have access to Centurion Lounges, Plaza Premium access, Priority Pass membership, and statement credits for security expediting services.

Capital One Venture X cardholders don’t get elevated hotel status, but they do get access to Premier and Lifestyle hotel collections along with Capital One Lounges. The Capital One Venture X card lets you transfer Capital One Miles to the Air Canada Aeroplan program, allowing you to book Air Canada flights and Star Alliance partners.

A Complete Guide to Travel Expense Reimbursement Policies

Are charge cards better than credit cards for businesses?

It depends on your spending habits, but the answer is often yes. Charge cards can work well for businesses that pay their balances in full each month and want higher spending flexibility. Credit cards may be a better fit for companies that prefer the option to carry a balance or need more predictable monthly payments.

Business Charge Card vs Credit Card: 6 Key Differences You Should Know

Read more from us