How to Open a Business Checking Account: A Complete Guide

Opening a business checking account is one of the first, most crucial steps to setting up your business for long-term success. It’s not just about having somewhere for your business’s cash to sit; a business checking account can offer helpful financial tools from cash flow management to corporate credit cards, merchant services, and more.

The process of opening a business checking account doesn’t have to be complicated. In this guide, we’ll break down what a business checking account really is, why it matters, and how to open one without getting lost in complicated paperwork.

What is a Business Checking Account and Why Do You Need One?

A business checking account, like a personal checking account, is used to house and easily access your company's cash for day-to-day use. While a savings account is designed to earn interest on idle capital, checking accounts are primarily for everyday transactions and can include tools to help you manage spending, automate payments, organize finances, and more.

Whether your business is brand-new or well-established, a business checking account is essential for managing finances confidently.

Importance for Entrepreneurs and Small Businesses

If you’re a sole proprietor or running a lean team of just a few people, a business checking account can offer a lot of help in getting your company moving.

For sole proprietorships, a business checking account will separate your business finances from the personal. The effect of which can ease any overlap, improving the clarity of books and tax prep, helping you minimize risk of inaccurate expense reporting or liability complications.

Business checking accounts can additionally help small business owners grow their business with tools like expense tracking, automated payments (e.g., payroll), ACH and wire transfers, merchant services, and more. Additional services are dependent on the platform you choose, and can include credit cards and debit cards, cash and mobile deposits, loans, and online banking services.

For small business owners and sole proprietors, business checking accounts translate into smoother operations: you don't have to worry about mixing payments with your personal account, you can often process larger invoices with higher transfer limits, and demonstrate professionalism when dealing with clients.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What You Need to Open a Business Checking Account Online

Depending on your type of business and what business checking account you are applying for, you'll need to consider different requirements when opening a business checking account. Generally, you will be expected to provide the following:

Identification & Personal Info

- Social Security Number (SSN) or another government-issued ID such as a passport or Driver’s License

- Personal Contact Details(name, phone, email) of the business owner(s)

Business Entity Information

- Business Name(legal name as registered with the state)

- Business Address(physical or mailing address)

- Type of Business(sole proprietorship, partnership, LLC, corporation, etc.)

- Registration Certificate(dependent on state, showing your business is officially registered with the state)

Federal & Tax Documentation

- Employer Identification Number (EIN) from the IRS (for tax reporting purposes)

- Some banks allow SSN for sole proprietors without employees; requirements vary.

Business Formation & Governing Documents

- Articles of Incorporation(for corporations)

- Corporate Bylaws(if incorporated, to outline governance)

- LLC Operating Agreement(for LLCs, to detail ownership and responsibilities)

- Partnership Agreement(for partnerships, showing who has authority to act on behalf of the business)

- General Business Documentation(any additional supporting paperwork showing business ownership and structure)

Licenses & Certificates

- Business License(required for most businesses to operate legally if applicable in your jurisdiction)

Understanding Terms and Conditions

Every business checking account comes with its own terms and conditions, and understanding them up front can save you from surprise fees and unnecessary headaches later. When reviewing an account, pay attention to:

- FDIC insurance(ensures your deposits are protected up to $250,000 legal limit per depositor).

- Merchant services(whether the account integrates with tools for accepting customer payments).

- ATM fees(what you’ll pay (or save) when withdrawing cash).

- Charge or Debit cards(how many cards you can issue, and what limits apply).

- Credit options(whether the account connects to a business credit card or charge card).

Key Benefits of a Business Checking Account

There are many benefits to opening a business checking account, and, based on the provider you go with, you may have access to extensive financial management tools, access to clients and vendor payments, and additional financial services not immediately available by opening an account alone.

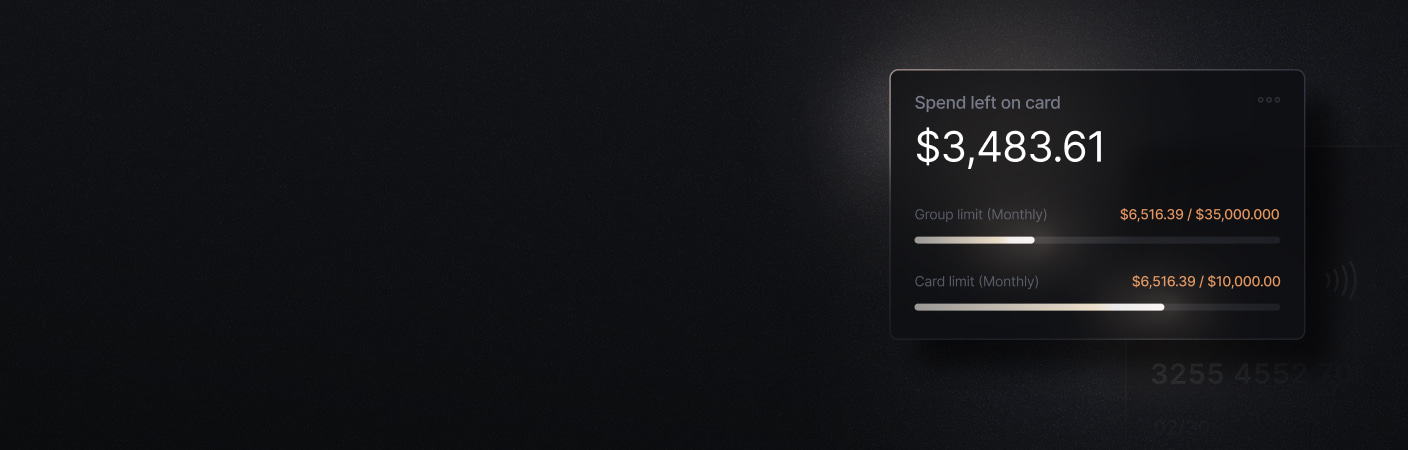

- Financial Management and Organization. A business checking account itself can help keep business finances organized and bookkeeping simplified. Tools on platforms such as Slash can provide you with accounting features, detailed vendor payments, and more, all within reach of one (or more) business checking accounts¹.

- Credibility with Clients and Vendors. Having a dedicated business account makes it not only easier for your business, but also for those you do business with. For professional reasons, having a business checking account can help you maintain credibility and professionalism with your partners. It can also improve your transactional cash flow, with ACH and wire transfers sometimes available through your account.

- Additional Financial Services Having a business checking account can consolidate your finances and can provide you with further services related to detailed transaction history, payroll, accounting, and more.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Choosing the Right Business Bank for Your Needs

When choosing the right business banking platform with which to open a checking account, it’s important to factor in key features of the offered service, like accessibility and technology, fee structures, balance requirements, and whether or not the platform supports your business-specific needs.

How to Open a Business Checking Account Online with Slash: Step-by-Step Guide

Slash is an online banking platform built to support modern businesses' financial needs. Here's a step-by-step look at how you can open a business account with Slash today:

Step 1: Choose Slash as your business banking platform

Most business bank accounts give you the basics — a place to hold money and move it around. Slash starts there and builds up: cards, expense management, treasury, and more, all native to the platform

Your Slash account comes with full payment rails (ACH, wires, RTP, FedNow) and multi‑million‑dollar FDIC insurance through the Column N.A. sweep network². From there, you can issue virtual and physical Visa Platinum cards with up to 2% cashback, manage expenses and invoicing without a separate platform, and put idle cash to work in Treasury through money market funds managed by BlackRock and Morgan Stanley⁶.

Step 2: Gather your documentation

Slash offers a streamlined application and approval process. For US-incorporated entities (LLCs, C Corps, S Corps, Limited Partnerships), you'll need:

- Business name, address, phone number, and date of incorporation

- Government-issued ID for all beneficial owners

- Articles of incorporation

- Two recent bank or credit card statements

- Proof of operating activity (invoices, contracts, or revenue statements)

- Certificate of Good Standing (if incorporated in DE or NJ)

International businesses can apply for a Global USD Account with similar documentation — no US incorporation required.

Step 3: Submit your application online

Head to slash.com/register to get started. You'll answer a few questions about your business, then either schedule a product demo with the sales team or skip straight to the full application.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Can you open a business bank account without an SSN?

In some cases, yes. To do so, you’ll typically need to provide government-issued identification (like a Social Security Number (SSN) or passport). For U.S.-based businesses, most banks will require either an SSN or an Employer Identification Number (EIN), depending on your business structure. Some financial platforms, including Slash, allow you to open an account using an EIN rather than SSN, which can be especially useful for international founders.

Open a US Business Bank Account as a Non-Resident: Requirements and Benefits

How to Start a Business in the USA: A Step-by-Step Guide for Foreigners

What’s the difference between a business checking account and a business savings account?

A business savings account is typically used to store excess cash that will accrue interest for your business. A business checking account lets you handle daily business operations with tools to manage cash flow, payroll, business spending, and more.

Do I need a business account for each LLC?

Separate accounts for each LLC is best practice, though not required. If you have multiple LLCs and bank accounts, platforms such as Slash offer multi-entity support that will help you manage each entity in one dashboard.

Top Fintech Platforms for Multi‐Entity Banking in 2026