Bank Routing Numbers

Every ACH payment, wire transfer, and direct deposit relies on a nine-digit routing number to reach the right bank. Use our guide to look up routing numbers for major US banks, understand how they work, and avoid costly payment errors.

What is a routing number?

A routing number - also called an ABA routing number or routing transit number (RTN) - is a nine-digit code that identifies a specific financial institution in the United States. Introduced in 1910 by the American Bankers Association, routing numbers were originally designed to streamline the processing of paper checks. Today they serve as the backbone of electronic funds transfers, enabling banks, payment processors, and clearinghouses to route money to the correct destination. Every federally chartered and state-chartered bank that maintains an account with the Federal Reserve has at least one routing number, and many larger banks use different routing numbers for different states or transaction types.

How routing numbers work

Each routing number is structured according to a precise format. The first four digits identify the Federal Reserve Bank district and the specific processing center. The next four digits identify the individual financial institution. The ninth digit is a checksum - a mathematically derived value that validates the entire number using a formula known as the "modules 10" algorithm. When you initiate an ACH transfer, set up direct deposit, or write a check, your bank's routing number tells the payment network exactly where to send the funds. Without it, there would be no way to distinguish between accounts held at different institutions.

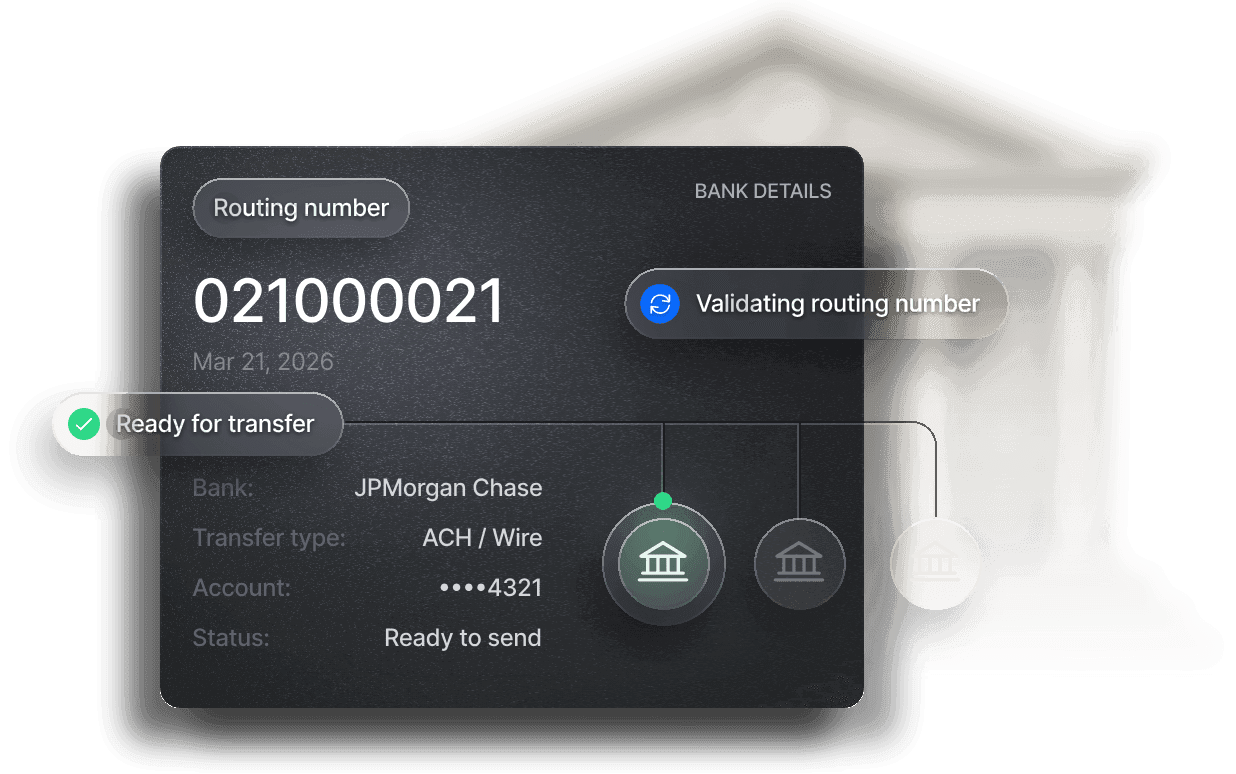

ACH vs. wire transfer routing numbers

Not all routing numbers are interchangeable. Many banks use different routing numbers for ACH transactions (like direct deposits and bill payments) and for domestic wire transfers. ACH routing numbers are used by the Automated Clearing House network, which processes transactions in batches throughout the day. Wire transfer routing numbers route funds through the Fedwire system, which settles transactions individually and in real time. Using an ACH routing number for a wire transfer - or vice versa - can cause your payment to be rejected or significantly delayed. Always confirm which routing number your bank requires for the specific type of transfer you are making.

Where to find your routing number

Your bank's routing number appears in several places. On a personal or business check, the routing number is the first set of nine digits printed along the bottom-left edge, before your account number and check number. You can also find it by logging into your bank's online banking portal or mobile app, where it is typically listed under account details. Your bank's website often publishes routing numbers on a dedicated support page. If you cannot locate it online, calling your bank's customer service line is the most reliable method. For businesses making high-value or time-sensitive payments, verifying the routing number directly with the recipient's bank can prevent costly errors.

Bank Routing Number Lookup

Select a bank for state-by-state routing numbers and transfer guides.

Why banks have multiple routing numbers

Large national banks like Chase, Bank of America, and Wells Fargo maintain dozens of routing numbers - sometimes one for every state where they operate. This dates back to a time when banking was more regionalized: before interstate banking was fully deregulated in the 1990s, banks that expanded into new states often did so by acquiring local banks, each of which already had its own routing number. Rather than consolidate to a single number (which would require every customer to update their direct deposits, autopayments, and vendor relationships), banks kept the legacy routing numbers in place. The result is a patchwork system where the routing number you use depends on where you opened your account, not necessarily where you live today.

Routing number vs. account number

A routing number identifies the bank; an account number identifies you at that bank. Together, these two numbers form the complete address that the banking system uses to direct funds to the right place. Routing numbers are public - anyone can look them up - while account numbers are private and should be shared only with trusted parties. Account numbers vary in length (typically 8 to 17 digits) and are unique within a given bank, though two customers at different banks could theoretically have the same account number. When setting up any payment or transfer, you will always need both your routing number and your account number.

Routing numbers and international transfers

Routing numbers only work within the US domestic banking system. For international wire transfers, banks use SWIFT codes (also called BIC codes) to identify institutions across borders. A SWIFT code is an 8- or 11-character alphanumeric identifier assigned by the Society for Worldwide Interbank Financial Telecommunication. If you're sending money overseas, you'll typically need the recipient's SWIFT code and their local account identifier (such as an IBAN in Europe). If you're receiving an international wire into a US bank account, the sender will need your bank's SWIFT code along with your account number - and sometimes an intermediary bank's routing information as well.

Why Slash?

Trusted by 10,000+ businesses, Slash is reimagining business banking around industry-specific needs. From high treasury yields, integrated stablecoin payments, unlimited virtual cards, and accounting automations, Slash enables business owners to move faster.

Browse routing numbers

Banks grouped by where they operate - nationwide, East Coast, Midwest & South, West & Pacific, or online-only.

Stop looking up routing numbers

Slash handles ACH, wires, and cards from one account — so you can focus on growing your business.

Frequently asked questions

Don't see the answer you're looking for? Get in touch.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.