How Long is a Billing Cycle? A Complete Guide for Businesses

Discussing the length of a billing cycle may seem straightforward—maybe even insignificant. Billing cycles determine when your monthly statement shows up, which in turn determines your payment due date. It sounds simple. In practice, however, billing cycles can play a much larger role in how money moves through your company. They can influence when recurring expenses need to be paid, how you manage customer relationships, and how predictable your cash flow may be from month to month.

In this guide, we'll explain the significance of billing cycles to your business operations, starting with what is a billing cycle, how they work, and the typical billing cycle length. You'll also learn how to read a billing statement, how billing cycles can influence credit outcomes, and how finance teams can use billing-cycle timing strategically.

Modern platforms like Slash can improve how you manage payments from month to month; with the Slash financial management dashboard, you can automate payments across multiple rails, generate and manage invoices, improve invoice management, keep an eye on company spending, and maintain corporate charge cards that can earn up to 2% cash back.¹

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What is a billing cycle?

A billing cycle is the recurring time period during which transaction activity is recorded. This activity may include charges made to the account, credits or refunds, and payments that post during the cycle. That activity is then organized and summarized on a billing statement, which is delivered to the account holder ahead of payment.

In most business contexts, billing cycles apply to:

- Credit cards and charge cards

- Recurring vendor invoices and recurring expenses for services

- Rent and utilities

- SaaS platforms and software subscriptions

How do billing cycles work?

A billing cycle follows a predictable pattern. It begins on a set start date, runs for a defined period of time, and closes on a statement date. All transactions that post during that window are included on the statement generated at the end of the cycle. Once a billing cycle closes, any transactions that post afterward are included in the next cycle.

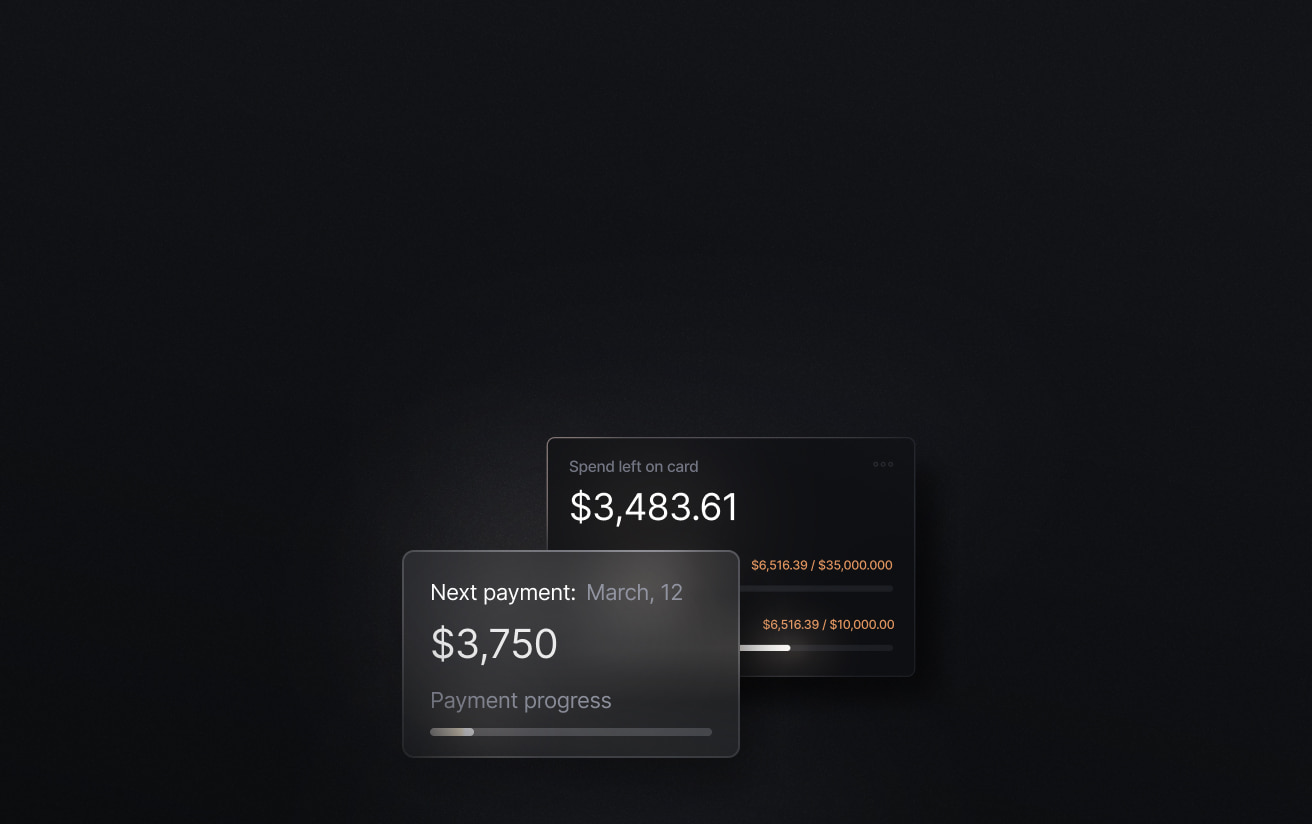

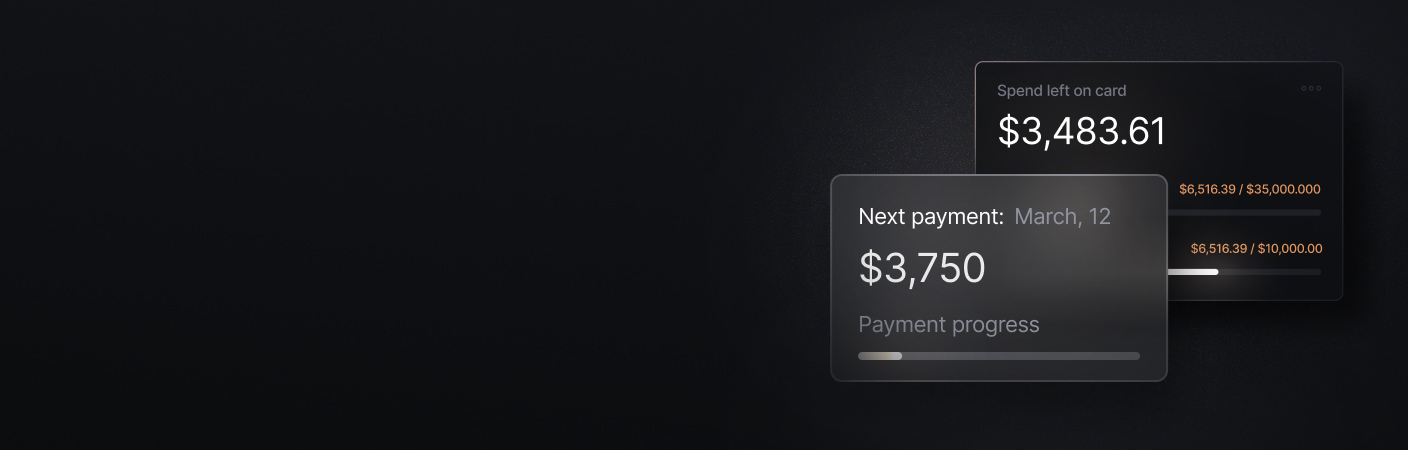

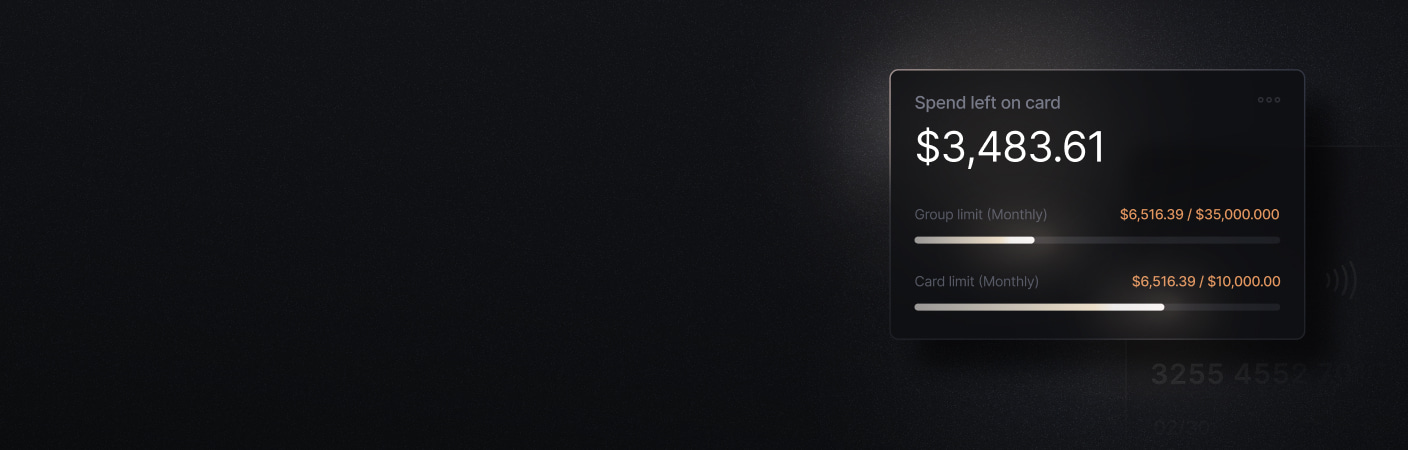

After the statement posts, a payment due date follows. This often includes a grace period that allows businesses time to review the statement and schedule payment. While the billing cycle determines when statements post and which transactions appear on them, it does not necessarily determine when payment is due. This is the essential billing cycle vs due date distinction.

This distinction can become important when using different corporate card payment structures. For example, the Slash Visa Platinum Card is a charge card that requires balances to be paid down daily. Even so, the account can still produce periodic statements that summarize activity for review, reconciliation, and recordkeeping.

How long is a billing cycle?

In most cases, the billing cycle length is one month, reflecting a typical monthly billing cycle. This is true for the majority of credit cards, rent payments, utilities, and recurring business services. While the length is generally consistent, the exact closing date can vary. Some billing cycles close on a fixed calendar date, such as the first or fifteenth of every month. Others operate on a rolling basis, meaning the cycle closes on the same day every month based on when the account or service was first activated.

Certain services may have longer or shorter billing cycles, which can change how they affect your cash flow. For example, many software providers offer annual subscriptions that bill once per year. These plans often come at a lower effective annual cost than paying month to month, but they require planning for a larger, less frequent outflow. Other billing arrangements may run weekly, biweekly, or quarterly, depending on the service and the terms you negotiate.

Sometimes, billing cycle adjustments can be negotiated with your provider. Changing a billing cycle may help align large expenses with revenue inflows or spread payments more evenly across the month to reduce cash strain. Ultimately, the right billing cycle structure depends on how your business typically earns and spends money. Companies with predictable monthly revenue may prefer a single consolidated billing date, while companies with more variable inflows may benefit from staggered cycles.

Understanding your billing statement

Your billing statement is a summary of everything that happened during a specific billing cycle. For businesses, understanding how to read a billing statement can be a useful skill for accurate expense tracking, cash flow planning, and on-time payments. Each section of the statement serves a specific purpose and directly affects how much you need to pay and when:

Starting balance

The statement typically begins with the balance carried over from the previous cycle. This number reflects any unpaid amount that remained when the last billing period closed. If the account was paid in full, the starting balance will be zero. If not, that balance carries forward and contributes to the current total.

Activity during the current cycle

Next, the statement lists all activity posted during the current billing cycle. This can include purchases made with the card or account, recurring subscription charges, fees (such as late fees or service charges), and interest charges. Only transactions that post before the billing cycle's closing date will appear on your statement. Charges made after the closing date will roll into the next cycle, even if they occur just one day later.

Payments and credits applied

This section shows any payments or credits that reduced the balance during the billing cycle. These may include manual payments, automatic payments, refunds, or statement credits. Payments made before the closing date reduce the balance shown on the statement, while payments made afterward appear on the next one. This timing is important for planning cash outflows and understanding what will be due.

Statement balance at the closing date

The statement finishes by showing the balance as of the closing date. This amount reflects everything owed for the billing cycle and is typically the figure businesses use to review charges, reconcile accounts, and prepare payments.

Minimum payment and due date

Finally, the statement lists the minimum payment required and the due date. This applies most specifically to credit card statements. Paying at least the minimum by the due date helps avoid late fees and negative payment history.

If your business uses charge cards, you will not have a minimum payment, since they require cardholders to pay the full balance rather than a minimum. Understanding this section ensures you know exactly how much must be paid and by when, allowing your finance team to plan payments without disrupting cash flow.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How does a billing cycle impact your credit score?

Billing cycles can directly affect the credit reporting process. During each credit card billing cycle, charges accumulate until the cycle closes and a credit card statement is issued. The balance shown on that statement is typically what credit card companies report to credit bureaus.

That reported balance is compared to the card's credit limit to calculate your credit utilization ratio. If a high balance appears on the statement, your available credit may look lower, even if you pay the balance off shortly afterward. As a result, utilization can temporarily increase simply due to the timing of credit card billing.

Credit utilization is one of the most influential factors in credit scoring. Using a large portion of your available credit can negatively affect scores, especially if high balances appear consistently on credit card statements. This can happen even when businesses pay in full every month.

Payment history is also tied to billing cycles. Each credit card statement includes a due date set by the card issuer, and missing that deadline can lead to late fees and negative credit reporting. Knowing when billing cycles close and when payments are due helps businesses manage utilization, preserve available credit, and maintain strong standing with credit bureaus. Timing therefore contributes to the billing cycle impact on credit score, primarily through utilization and payment history.

Why billing cycles matter for your finances and how to use them effectively

Billing cycles play an important role in cash flow management. By tracking when expenses post and when payments are due, finance teams can better anticipate short-term cash needs and avoid situations where multiple large payments hit at once. This is particularly important when monitoring accounts receivable; delays in your business's incoming payments can compound the negative impact of large, outgoing billing obligations.

Another common use of billing cycle management is addressing late-paying customers or partners. If a customer regularly pays invoices a week or more after the due date, shortening the billing cycle can help offset that delay. Instead of reacting to late payments after the fact, businesses can proactively adjust timelines to protect cash flow without immediately resorting to penalties or stricter enforcement.

Shortened or adjusted billing cycles can also be useful when working with high-value clients, managing credit exposure, or transitioning a customer to tighter payment terms. While these approaches are not necessary for every relationship, they can help finance teams adapt customers' billing structures to real-world payment behavior.

Discover smarter capital management solutions with Slash

Managing billing cycles becomes significantly easier with the right tools in place. Slash gives you clear visibility into your company's entire financial workflow from a single dashboard—corporate cards, business accounts, payments, invoices, and more. With a more complete picture of your financial standing, finance teams can make better-informed decisions about how to structure and manage billing cycles for both operating expenses and revenue collection.

Unlike traditional credit cards, the Slash Visa Platinum Card is repaid daily, helping businesses maintain tighter control over balances while still earning up to 2% in cashback rewards. Slash also makes it easier to manage employee spending by allowing you to set individualized spending rules by category or transaction, create card groupings by team, and automatically incorporate card activity into your broader analytics dashboard so spending stays aligned with your overall financial position.

Additional ways Slash helps optimize financial management include:

- Multi-entity support: Consolidate statements across multiple entities, subsidiaries, or storefronts into a single dashboard for easier oversight.

- Invoice management: Coming soon, manage accounts receivable through an intuitive invoice management dashboard. Generate invoices from stored contact and banking data, track payment status, and accept payments across multiple rails—including cryptocurrency.

- Diverse payment methods: Choose payment options that match your speed and cost needs, including Global ACH, international wires to more than 180 countries, and real-time rails like RTP and FedNow.

- Flexible financing: Address short-term liquidity needs with Slash's Working Capital Financing, a tailored line of credit that supports on-demand drawdowns with flexible 30-, 60-, or 90-day repayment terms.⁵

- Native crypto support: Hold, send, and receive USD-denominated stablecoins such as USDC and USDT, with easy on- and off-ramps and near-instant global transfers that bypass traditional banking delays and foreign transaction fees.⁴

If you want clearer visibility into spending and fewer surprises at the end of each billing cycle, Slash gives you greater control over your company's finances. Learn more at slash.com.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What does double-cycle billing mean?

Double-cycle billing is a method where interest is calculated using balances from both the current and previous billing cycles, which can result in higher interest charges. To avoid paying more interest than you anticipated, consider using a charge card like the Slash Visa Platinum Card.

Is a billing cycle the same as a due date?

No. A billing cycle defines the period of activity summarized on a statement, while the due date is the deadline for payment. Think of this as a billing cycle vs. a due date.

What's a Billing Cycle? Everything You Need to Know

What is the 15-3 rule?

The 15-3 rule is a credit card payment strategy. It aims to lower the reported credit utilization by making a payment before the billing cycle closes and another before the due date.

Can Businesses Deduct Bad Debt on Their Taxes?