The Eight Top Ramp Alternatives For Simplifying Payments

Ramp can draw the attention of finance teams for a variety of reasons. Some are wrestling with inconsistent accounting, others may be trying to bring order to scattered invoices, and most are interested in tracking their expenses. Ramp addresses these issues to an extent and consolidates functions that other fintech tools often outsource. Even with its strengths, though, Ramp comes with some notable limitations.

Ramp's shortcomings generally fall into two categories: features that lag behind competitors, or accessibility gaps that exclude a wide range of businesses. These issues can become far more pronounced when compared to other modern finance platforms and expense management solutions that deliver similar functions.

Ramp's middling cash back rate can leave a significant amount of money on the table for teams with heavy card spend. It also doesn’t support crypto payments, which hampers its ability to send fast, low-cost global payments. Perhaps most importantly, its strict approval requirements may prevent many small businesses, international teams, and non-U.S. entities from using the platform at all.

In this guide, we'll break down everything you need to know about Ramp: its core products, its primary use cases, and where its platform shows weaknesses. We'll use Ramp as a benchmark to compare leading alternatives, from platforms that mirror its full-stack approach to management solutions built for specialized workflows or industries. By the end, you'll see why Slash stands out as the strongest competitor. The Slash business banking platform not only resolves each of Ramp's drawbacks, but it delivers features Ramp doesn't match.¹

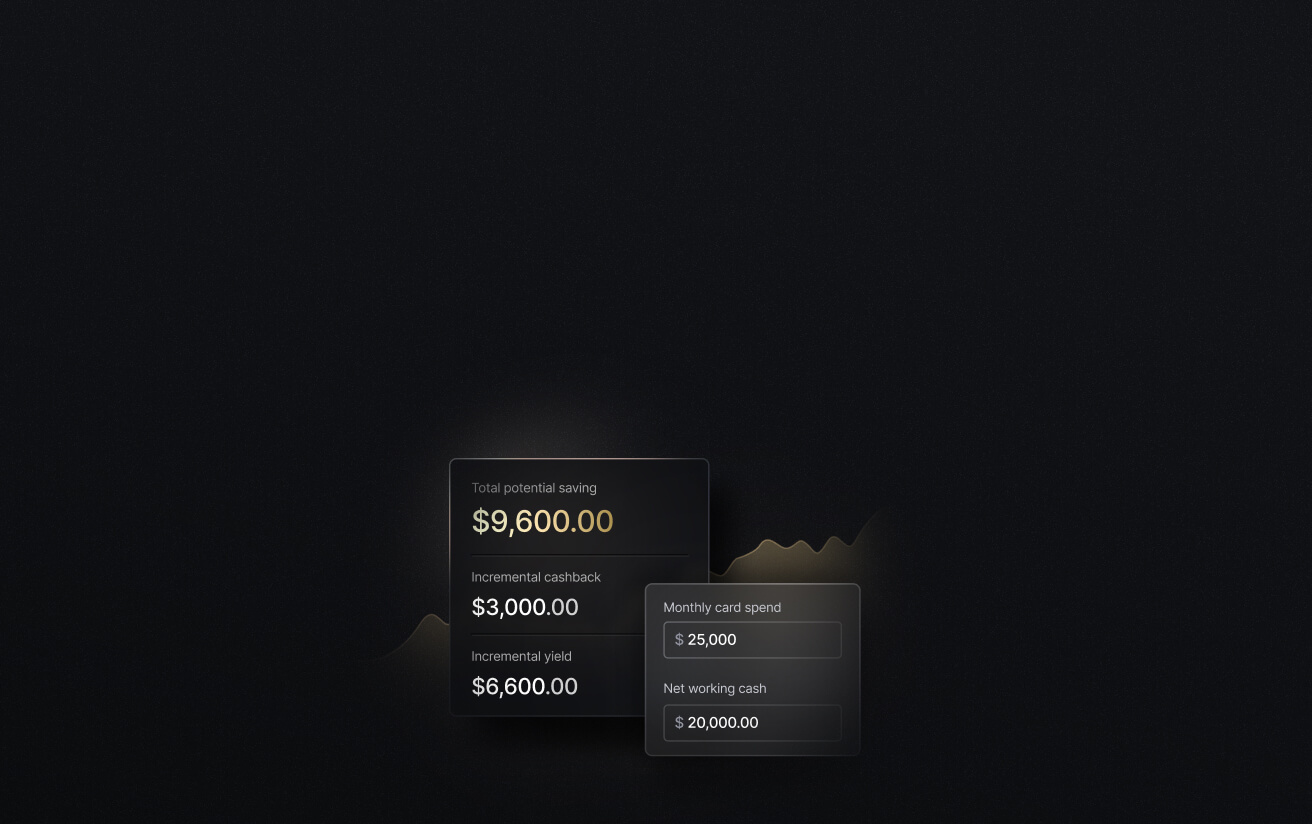

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What is Ramp?

Ramp is a modern finance platform that bundles corporate card management, expense tracking, banking, and accounts payable automation into a single system. Some of Ramp's most heavily used tools include:

- Ramp Card: Offers up to 1.5% cash back with customizable spending limits and built-in compliance guardrails.

- Expense management: Automatically matches receipts to transactions, sends real-time spending alerts, and enforces travel and expense policies. Ramp also offers some travel booking features that enhance visibility into purchases made through third-party travel platforms.

- AP automation: Extracts invoice data via OCR, matches purchase orders, and routes approvals without manual intervention, effectively serving as AP automation software.

- Banking & payments: Provides business and treasury accounts, domestic ACH transfers, international wires through the SWIFT network, and multi-currency capabilities.

- Integrations: Connects with accounting software like QuickBooks, Xero, and a range of ERP systems.

While Ramp's suite of features might appear healthy at first glance, a closer look shows that many of its capabilities fall short of what competing platforms now provide.

Why You Should Consider a Ramp Alternative

While Ramp has established a solid footing in spend management, several limitations prevent it from functioning as a truly comprehensive financial management solution. Underwhelming rewards, missing financial products, and narrow eligibility requirements can all be a pain for prospective customers. Here are the areas where Ramp falls behind:

Lower cash back than competition

Ramp's 1.5% cash back ceiling leaves money on the table compared to alternatives like the Slash Visa® Platinum Card, which earn up to 2%. Teams that use Slash Cards to spend into the tens of thousands can unlock hundreds more in returns without any extra effort.

No crypto support

Ramp doesn't support cryptocurrency or stablecoin transfers, which means you miss out on crypto payments for businesses that bypass the delays and fees associated with traditional banking networks. Platforms like Slash, by contrast, let you send, receive, and convert USD-pegged stablecoins directly within the app.⁴

Narrow approval criteria

Ramp only accepts U.S.-registered businesses, excludes sole proprietors and individuals entirely, and requires at least $25,000 sitting in a single bank account at the time of application. Quite a few competitors allow users to sign up for their services without any money in a bank account.

International access is another element to consider. You can’t use Ramp if you don’t have a physical entity located within the United States or Canada. With Slash, on the other hand, you can qualify for a Global USD account without a U.S.-registered LLC, making it far more accessible for businesses operating outside American borders.³

No credit or financing instruments

Unlike quite a few competitors, Ramp doesn’t offer any loan tools or working capital financing. Given its high barrier to entry and its lack of funding access, it’s clear that Ramp isn’t necessarily the best option for new founders or small businesses who are looking to kickstart their operations.

Who Are Ramp’s Main Competitors?

Since Ramp bundles a wide range of products and management solutions into one platform, we've selected eight competitors that either match Ramp's breadth or match some of their features. Some excel at travel booking, others focus on procurement or AP/AR automation, while a few offer more accessible, all-in-one solutions that work for businesses of any size or structure. Below are our picks for the best Ramp alternatives out there in 2026:

Slash

Slash is the only all-around solution that directly addresses every one of Ramp's pain points. It combines business banking, global payments, powerful corporate cards, and deep integrations into a single platform designed to centralize your entire cash flow. Not to mention – you need $0 in a business bank account to qualify, not $25,000.

Here are some specific places where Slash stands out the most:

- Flexible financing:Slash Working Capital gives you a tailored line of credit you can tap whenever cash is tight.⁵ Choose between 30-, 60-, or 90-day repayment terms to inject liquidity exactly when you need it.

- An agentic AI assistant: Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Native crypto support: Slash lets you send, receive, and convert USD-pegged stablecoins USDC and USDT without leaving the platform. Built-in on/off ramps make it easy to convert your currency and push payments globally across eight supported blockchains.

- Industry-leading cashback: With the Slash Visa® Platinum Card, you can earn up to 2% cashback on company spending. You can also get real time visibility into each purchase, customizable spending controls, and the ability to issue unlimited virtual cards for handling employee expenses.

- High-yield treasury accounts: Slash users can earn up to 3.84% annualized yield on idle funds with money market investments from Morgan Stanley and Blackrock, managed directly within your Slash account.⁶

- Accessibility: Slash's application process can be more forgiving than competitors. You can qualify for the full platform without an SSN, EIN, or U.S.-based entity.

Brex

Brex is a well-known option for VC-backed startups seeking unified business banking and expense management. It offers AP automation, travel and expense tracking, and treasury accounts with a yield of up to 3.67%. However, many of Brex's more sophisticated features, like multi-entity support, ERP integrations, and enhanced expense tools, are locked behind pricier subscription tiers.

Where Brex falls short:

- Low effective rewards value: Brex’s cards use a points-based system where redemption values often fall well below straightforward cash back rates. You can earn 7x points on rideshare purchases and 4x on travel, but most other purchases earn only 1x. It’s not impossible to get good value out of points systems, but it takes specific spending patterns and some extra math.

- Limited accessibility: Small and medium-sized businesses without venture backing will struggle to qualify. Brex typically expects either VC funding or over $1 million in annual revenue, putting it out of reach for many growing companies. Plus, if you thought Ramp’s $25,000 minimum was high, Brex requires at least $50,000 in a business account to apply for their corporate card.

Spendesk

Spendesk primarily caters to European companies and leans heavily into procurement and AP workflows. Its spend controls and purchasing visibility are solid, but the platform lacks many features teams have come to expect from modern finance tools. In fact, while it does offer corporate cards, they come with no cash back rewards whatsoever. Because Spendesk settles primarily in the EU and relies on partners like Wise for payments, its global coverage can be inconsistent.

Where Spendesk falls short:

- Zero card rewards: Unlike nearly every competitor, Spendesk offers no cash back or points on its corporate cards.

- Heavy European focus: The platform's regional orientation limits its usefulness for U.S.-based and globally distributed teams, particularly when it comes to payment coverage and currency flexibility.

- Expensive international fees: If you make an international card payment or a reimbursement in a foreign currency, you’ll be hit with a 2.99% markup.

Navan

Navan excels as a travel booking and management solution, but it ultimately doesn't pretend to be a comprehensive financial operations platform. Its intuitive booking engine can be a big advantage for those interested in travel policy enforcement and employee trip management. Step outside T&E, however, and the offering thins out considerably.

Where Navan falls short:

- Narrow T&E focus: Navan's travel booking comes first, and everything else is an afterthought. If you need invoice processing, vendor management, or business banking, Navan won't cut it.

- International payment coverage: Even though Navan’s all about travel, it supports payments in just 49 countries and about 25 currencies, which is far below the 150+ countries most competitors handle. This can easily be a dealbreaker for globally distributed teams.

BILL.com

BILL.com, otherwise known as BILL and formerly known as Divvy, is an AP/AR management software with invoice and receipt automation capabilities. You can customize invoices, automate approval routing, simplify vendor management, and generate general ledger codes without much effort. It also comes with a charge card known as the BILL Divvy Card. However, BILL's narrower focus on payables and receivables comes at the expense of some of its secondary functions, which underperforms when matched up against competitors.

Where BILL falls short:

- Points-based rewards program: Like Brex, BILL's rewards structure through its BILL Divvy Card is points-based, and can underperform compared to straightforward cash back if your spending doesn't align with point multipliers.

- No business banking: You'll still need separate accounts to handle treasury functions, financing, and day-to-day banking operations.

- Expensive monthly costs: Despite not being one of the more robust solutions in its class, it’s one of the most expensive. BILL costs $49 per user per month on its base plan, and $89 per user on its corporate plan.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Expensify

As you might guess from its name, Expensify specializes in expense management. Its SmartScan feature captures receipts effectively, and the Expensify Card delivers the day-to-day expense tracking that you would expect from this type of financial management solution. Expensify is also pretty accessible for many business types, and even has plans for individuals, sole-proprietors, and SMBs.

Where Expensify falls short:

- Misleading cashback: As you do your research, you might see that Expensify offers up to 2% cash back. However, reaching that rate requires extremely high monthly spending of at least $250k across cards. Otherwise, you’ll only earn 1% cashback on spending.

- No banking infrastructure: Without treasury accounts or dedicated business banking, Expensify works best as a supplement to your existing financial stack rather than a replacement.

SAP Concur

SAP Concur is similar to Expensify, but it tilts even more heavily toward travel and expense management. The platform is built to slot into enterprise software ecosystems (namely ones owned by SAP), handling expense approvals and AP workflows while leaving banking, payments, and card management to other providers.

Where SAP Concur falls short:

- No corporate card offering: If you want to manage card spend, you’ll need a separate provider entirely.

- Designed as middleware: Concur assumes you'll maintain dedicated banking and payment solutions elsewhere, making it a coordination challenge for teams hoping to consolidate their finance stack.

How to Choose the Best Ramp Alternative For Your Business

Not all expense management platforms are created equal, from their features to their target audience. What works for a venture-backed startup won't necessarily fit a mom-and-pop shop or a globally distributed team. The right Ramp alternative depends on your specific business needs, growth stage, and where your current setup creates the most friction. Here are the key factors to weigh when evaluating your options:

Transaction syncing and automation capabilities

Look for platforms that automatically match receipts to transactions, sync data to your accounting software in real time, and eliminate manual entry wherever possible. The best solutions categorize transactions intelligently, flag anomalies, and push updates to your general ledger through a configurable API. Slash excels here with integrations across QuickBooks Online, Xero, Sage Intacct, and NetSuite.

User accessibility

A powerful platform can still be inadequate if your team can't figure out how to use it. Keep an eye out for clean, intuitive interfaces that deliver enterprise-grade functionality without needing extensive training or constant IT support. This is where demos can come in handy.

Accessibility is also important during the application process; restrictive qualification criteria can lock out otherwise qualified businesses. Slash hits both these marks, since their interface is straightforward enough for new hires to navigate, and the approval process accepts non-U.S. companies and growing small businesses.

Strong spending controls and policy enforcement

A platform that allows you to extend spending privileges to the rest of your team isn’t very useful if you can’t customize those privileges. Look for platforms that let you set spend limits by department, vendor category, or individual cardholder, and that automatically enforce travel and expense policies at the point of transaction. That way, you can prevent policy violations before they happen and save quite a bit of time on manual approvals.

Unified dashboard with wide-ranging features

You might have all the tools you need for cards, payments, invoices, and banking, but they may not be particularly helpful if you have to juggle a bunch of logins and windows for each one. With a unified dashboard, you can get a single source for all your financial activity, from card transactions and wire transfers to invoice approvals and account balances. Platforms that consolidate these functions save time, reduce context-switching, and make it easier to spot patterns or problems.

Clear expense reporting

If you’re working with old-fashioned systems, it’s easy to waste a lot of time hunting for old receipts and fixing discrepancies at the end of the month. Look for platforms that capture transaction data at the point of spend, match receipts, and generate reports automatically. Reporting tools should give finance real-time visibility into what's been spent, by whom, and against which budget, without waiting for employees to submit anything.

Start Optimizing Your Business Banking Now With Slash

Ramp laid important groundwork in modernizing corporate finance, but it's far from the only option. For many businesses, it's not the best one either. Between its restrictive approval criteria, limited rewards, and the absence of financing or crypto capabilities, Ramp leaves gaps that can hamper growth and flexibility.

As an all-in-one business banking platform, Slash eliminates those gaps entirely. You can get strong cash back, flexible financing through Slash Working Capital, native crypto support across eight blockchains, and a platform accessible to both U.S. and international companies without onerous requirements.

Slash also allows you to create and send invoices, track which ones have been paid, and follow up on the ones that haven't, all from the same place you bank. If you want a deeper look into the way cash moves in and out of your business, prompt our AI agent, Twin, to dive into the data. Twin can generate charts and cash flow forecasts that come filled with insights you may never have discovered yourself.

There are even more Slash features we haven’t touched on, including:

- Action Center: A one-stop spot for employees to see pending tasks assigned to them. These may include card requests, expense submissions, reimbursement reviews, and more.

- Separate virtual accounts: Create multiple business bank accounts to silo cash flows by project, department, or client with real-time analytics across each of them.

- Multi-entity support: Slash offers multi-entity account management tools without separate logins, allowing businesses to track spending, manage accounts, and download statements across all subsidiaries in one place.

- The Slash Mobile App: Our app allows users to send money, add funds, switch between entities, create cards, and much more while on the go.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Which solutions are best suited for mid-market versus enterprise companies?

Mid-market companies generally do well with platforms that balance features and simplicity, while enterprises often need deeper ERP integrations and multi-entity support. Slash’s scalability, customizability, and powerful account management tools fit well within any team, no matter your growth stage.

Which Ramp alternatives support invoice scanning?

As a matter of fact, each of the platforms we've discussed allow you to scan invoices. However, it's the workflow after that counts. For example, after an invoice is scanned/uploaded, Slash can turn it into a structured bill. From there, it can create a payable, route it by policy, and automate payment execution.

Automated Invoice Scanning: How It Works in Accounts Payable

Which alternatives offer the fastest setup and easiest user experience?

Platforms with streamlined applications and intuitive interfaces like Slash can get you up and running pretty quickly. Look for solutions that minimize documentation requirements and don't require extensive training for your team to start using effectively.

Which platforms are best for expense tracking?

Generally speaking, each of these platforms come with some expense tracking features. For the most full-fledged tools, consider Slash, Expensify, and Brex.

Best Expense Management Tools for Startups in 2026

Read more from us