Bookkeeping for Startups: Setup and Best Practices

If you’re a first-time founder building a startup for the first time, bookkeeping may be one of the last things on your mind. After all, if your early cash flow is light and you’re not doing much business, your accounting should be easy to catch up on, right? Not exactly.

Clean bookkeeping is just as important during a company’s first few months as it is after its first few decades. By keeping detailed financial records that reflect expenses, assets, liabilities, and income, founders can get an accurate picture of their cash flow and make smarter business decisions based on that data. Without maintaining your books, you may lose sight of your startup’s financial health and leave yourself with a mess once tax season rolls around.

This article aims to give new founders a practical, stage-by-stage guide to setting up and managing their startup's bookkeeping from day one. We’ll discuss the records you should keep, what tasks you should prioritize, and how to avoid the mistakes that cost early-stage startups the most time and money. We’ll also explore Slash, a neobank that connects your banking directly to your books by integrating with QuickBooks Online, Sage Intacct, and Xero.¹

Why Bookkeeping Matters for Early-Stage Companies

Bookkeeping is the process of recording and organizing a business's daily financial transactions, such as expenses, sales, receipts, and payments. By definition, it’s a bit different than accounting, though they often overlap – accounting involves higher-level practices like performing internal audits, forecasting cash flow, and tax filing. Bookkeeping tasks like expense categorization and bank reconciliations help inform accounting processes.

Some early founders may overlook the importance of bookkeeping, as their startup might only have a few sales or clients under their belt. However, it’s an essential part of a company’s financial management processes, regardless of their volume of sales. Accurate bookkeeping helps business owners identify important metrics like burn rate, runway, and profitability. Founders should be able to access detailed insights into their spending and cash reserves, especially early in their startup’s life cycle. Waiting until your first few sales to start organizing your books can leave you playing catch-up.

Your cash flow also matters to potential investors, who often expect clean, organized financials. Whether your startup is preparing for a seed round or a Series A, due diligence checks will likely reveal inconsistencies in your financial records. Founders who have maintained their books can answer questions about revenue growth and operating expenses with confidence. Those who’ve ignored their accounting may be left turning over couch cushions for old receipts.

Lastly, good bookkeeping can take the pain away from year-end tax documentation. Sales tax requirements, payroll tax withholding, quarterly estimated payments, and period-end filings all depend on records being accurate throughout the year. If you’ve kept your books organized, all your financial data will be right where you expect it to be, and you’ll avoid potential penalties and headaches.

How to Set Up Your Startup’s Bookkeeping from Day One

Fully preparing bookkeeping for your startup is a multi-step process, so it’s best to start as soon as you’re able to. This is how to begin:

Open a Dedicated Business Bank Account

Some first-time founders make the mistake of handling their startup’s finances through their personal bank accounts. Mixing the two often creates tax complexity, complicates reconciliation, and undermines the legal separation that a business entity is designed to provide.

It’s a better idea to open a business bank account, as it keeps your personal finances separate from your business finances and can also offer exclusive perks. For example, Slash offers unlimited sub-accounts, giving new founders the ability to sort their finances and create virtual cards dedicated to specific expenses.

Choose a Business Entity

Your business entity type determines how your startup is taxed, how profits are distributed, and what personal liability exposure the founders carry. Startups typically decide between an LLC, S corporation, and C corporation, though some owners may choose a sole proprietorship if they plan on starting small.

LLCs offer flexibility through limited liability protection and profits that pass through to the owner’s tax returns. With an LLC, a founder’s personal assets are protected against outstanding business debts. A corporation is a separate legal entity that provides a more rigid structure that’s suitable for raising capital, though they face stricter compliance rules and can face double taxation (corporate tax + dividend tax). The right choice depends on the specifics of your business and your future plans.

Set Up a Chart of Accounts

A chart of accounts is an organized, numerical index of every financial account in a company's general ledger. It's not meant simply to track your checking and savings accounts; this chart can include categories like undeposited funds, inventory assets, prepaid insurance, and common stock. Maintaining a consistent chart of accounts is especially important to investors and shareholders, as it provides a quick overview of assets and financial health.

Pick an Accounting Method

Companies may either practice cash basis accounting or accrual accounting. Cash basis accounting records income explicitly when money is received or payments are made. Accrual accounting records revenue and expenses when goods are received or services are performed, regardless of when cash changes hands.

While cash basis accounting can be more straightforward, it actually tends to provide a less accurate view of a company’s cash flow in the current moment, since payments can be made long before or long after a service is performed. Because the delivery of a good or service is invariably tied to a payment, even if later or earlier, accrual accounting may provide a better representation of financial health in a startup’s early stages.

Select an Accounting Tool or Platform

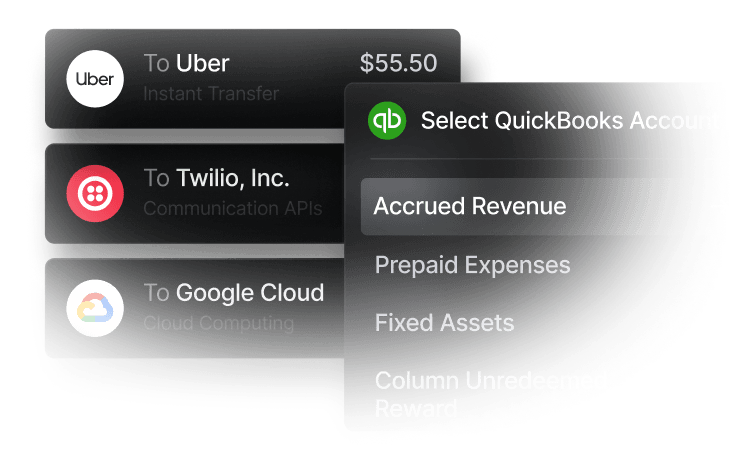

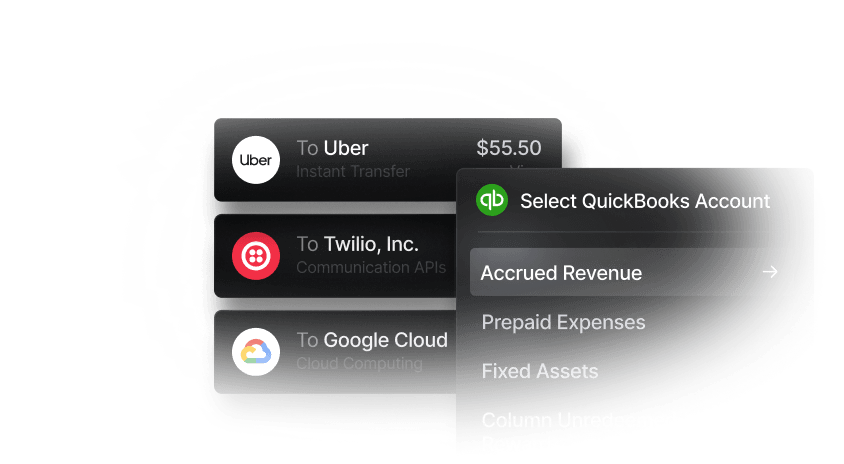

Accounting software automates transaction recording, categorization, and financial reporting in ways that spreadsheets can’t. While there are plenty of options on the market for streamlined accounting, few of them sync with a modern business banking platform. Connecting your bookkeeping and your banking can transform financial tracking for your startup by maintaining accurate records without the time-consuming manual data entry.

QuickBooks, Xero, and Sage Intacct integrate two-ways with Slash, meaning data from one platform can inform the other. Slash imports the structured data that lives in your accounting solution, such as unpaid bills, due dates, payment terms, and vendor info. From there, information about payments made with Slash return to your accounting tool, easing reconciliation and ensuring all numbers match correctly.

Financial Records Every Startup Should Track

When bookkeeping for your startup, you should keep and track everything that documents money moving into or out of the business. “Everything” often means:

- Income and expense records, including all revenue streams and any operating costs

- Bank and credit card statements

- Invoices and receipts that document each transaction on both sides

- Payroll documentation, including wages paid, tax withholdings, benefits, and employer contributions

- Financial statements, including income statement (P&L), balance sheet, and cash flow statement

- Tax filings and supporting documents, including W-2s, 1099s, sales tax records, and quarterly filings

Most of these records should be kept for several years. Investors may want to reference past cash flow to help project future earnings, and the IRS may need some older information for an audit. When it comes to your financial records, there’s no such thing as being too prepared. Proper revenue recognition especially matters for startups using accrual accounting, as the actions that trigger payment matter as much as the payments themselves.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Weekly and Monthly Bookkeeping Tasks to Plan For

Bookkeeping can quickly become overwhelming if you don’t have a clear schedule or priorities. Here’s a quick breakdown of some bookkeeping tasks that should be done weekly, and some that should be done monthly:

Weekly Tasks

- Record transactions and payments: Each time money enters or exits a business account, it should be recorded. Missing a couple transactions here and there can snowball into a reconciliation avalanche at period-end.

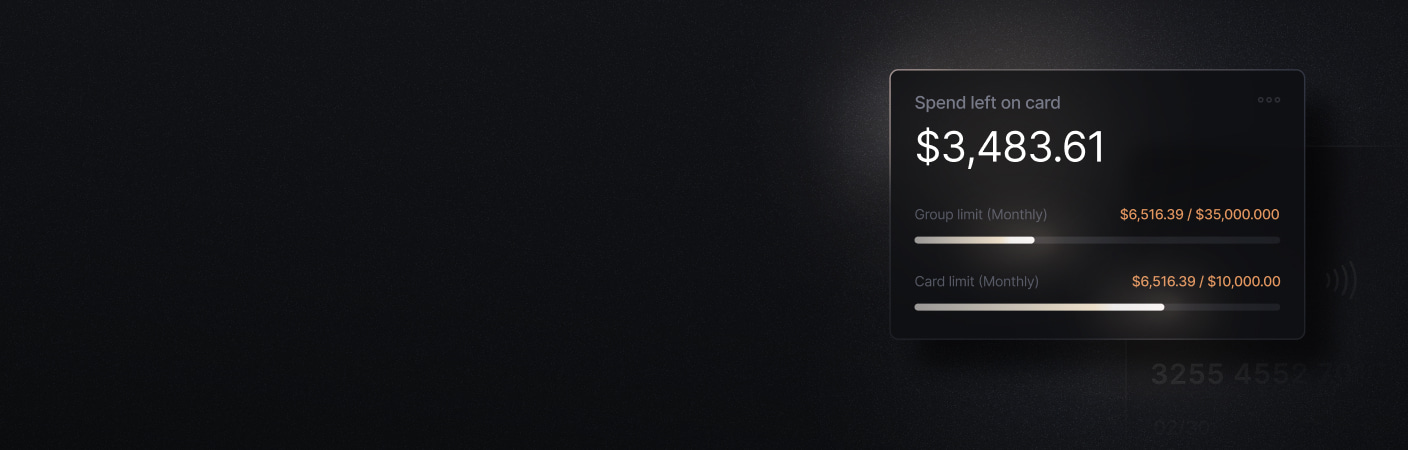

- Categorize each expense: Expense categorization should be fairly granular, extending to segments like research & development, office supplies, utilities, and hiring. Modern banking platforms like Slash offer corporate charge cards that can intelligently categorize expenses the moment they’re made.

- Digitize and file receipts: Since a lot of modern purchases are online-based, many of your receipts will be digital. For business purchases that take place in person, it’s smart to scan and digitize your paper receipts so they’re all kept in the same place. This is important for the sake of both general record keeping and future audits.

Monthly Tasks

- Review outstanding invoices and cash flow: At the end of each month, follow up with any clients that haven’t paid you yet, and do your best to pay off bills and invoices that are nearing their due date. Additionally, it’s good to review your overall cash flow and balance sheet for anything that looks off, like unusual expense trends or revenue that doesn’t match expectations.

- Reconcile bank and credit card accounts: Consistent reconciliation can catch data entry errors, duplicate transactions, missed entries, and unauthorized charges. Compare your accounts against the records in your accounting software and confirm that the two match accordingly.

- Track spending and budgets: Since you’ve been categorizing your expenses, you’ll be able to easily identify what expenses have taken up a larger share of the budget than expected. You can use your monthly review to balance allotments towards certain categories and even out your budget overall.

Common Bookkeeping Mistakes Startups Should Avoid

If you’re a busy founder managing your own early-stage startup, you can expect to make a bookkeeping mistake here and there. Many mistakes are actually easy to avoid, as they’re intentional decisions rather than one-time slip-ups. Here are some to watch out for:

Mixing Personal and Business Finances

Using personal accounts for business transactions creates reconciliation problems and makes cash flow harder for potential investors to review. It also undermines the liability protection that incorporation is meant to provide; an LLC is supposed to protect a founder’s personal assets, but it can’t if the founder pays for all business expenses using those personal assets.

Falling Behind on Transaction Recording

Recording weekly transactions is key to clean bookkeeping, whether the week saw a wave of clients or just a few paid bills. Forgetting to record your sales and expenses may lead to frantic bank statement scrolling at the end of the month.

It’s also possible for a founder to be overwhelmed by the sheer volume of business they’re doing, enough so that they can’t find the time to sit down and log their transactions. If this is you, then first of all, congratulations on your success. We built Slash to make bookkeeping easy for founders like you who need a hand logging their financial activity. Business expenses made with the Slash Visa® Platinum Card are automatically categorized as they upload to our platform the moment they occur. They can then be shared with your integrated accounting solution without any manual work or data entry.

Miscategorizing Expenses

Expense categorization is key to clean bookkeeping practices, but making mistakes along the way counteracts the benefits it offers. For example, you may accidentally label a trip to the office supply store “marketing”, or a monthly software subscription “insurance”. Poor categorization can distort financial reports, complicate tax preparation, and confuse you as you sort through your cash flow.

Skipping Monthly Bank Reconciliation

Business owners typically find missed transactions and mis-categorized expenses during their monthly reconciliation process. If they’re skipping reconciliation, then these oversights are only going to compound over time. Undiscovered financial errors will often resurface as earlier records are investigated, whether the person doing that investigation is you or an auditor.

Missing Tax Obligations

Tax obligations can be tough for startups to keep up with, especially with the variety of state-specific requirements found in the U.S.. Corporations call for different taxes than LLCs, sales taxes can vary by structure and entity, and your first hiring round will introduce you to payroll tax laws. If you formed your business in a different state than it operates out of, you also have to know which state’s taxes apply to you in which situations. Doing all this research beforehand can help you stay ahead of surprise regulations.

Waiting Until Tax Season to Organize Records

It’s one thing to postpone your bookkeeping for a couple weeks or a month, but you never want to procrastinate all the way until tax season. Cobbling together a year’s worth of financial data is extremely difficult, even with the help of specialized software. It’s a mistake that some inexperienced founders end up dealing with every spring. Take our advice: don’t be one of them.

How Slash Helps Startups With Bookkeeping and Accounting

Bookkeeping is easiest when first-time founders stay dedicated to logging their transactions and categorizing their expenses. However, even the most organized business owners may struggle to keep up when their accounting software is disconnected from their banking solution. Fractured systems can lead to misaligned data and errors during manual transposition, costing busy founders time that should be dedicated to building their startups. This is where Slash can help.

Slash is a business banking platform that introduces real-time transaction data to your accounting workflows, providing greater transparency and allowing a deeper level of automation. Our system integrates with QuickBooks Online, Sage Intacct, and Xero, allowing your financial information to sync together and work in harmony.

All incoming and outgoing payments are easily accessible on the Slash dashboard, enabling accurate financial forecasting and cash flow assessment. The Slash dashboard also displays employee spend, virtual accounts, financial analytics, and more in one spot. Other Slash features that can help startups better manage their finances include:

- Slash Visa® Platinum Card: The Slash card is a corporate charge card that earns up to 2% cash back on company spend, with configurable spending rules, card controls, and encryption-grade fraud protection.

- Diverse payment methods: Our platform supports global ACH, international wires to 180+ countries, and real-time rails like RTP and FedNow.

- Stablecoins: With built-in on/off ramps, businesses can send and receive USD-pegged stablecoins like USDC and USDT.⁴ This allows companies to access potential benefits like faster settlement and lower processing costs, while avoiding the price volatility associated with many other cryptocurrencies.

- Reimbursements: Our reimbursements tool allows teams to submit, review, and approve reimbursements directly inside the Slash dashboard.

- High-yield treasury: Slash offers treasury accounts that earn up to 3.83% annualized yield on idle funds through money market investments from BlackRock and Morgan Stanley.⁶

When Slash’s banking tools are integrated with your current accounting system, you’ll finally be able to streamline your bookkeeping and open up breathing room to focus on what matters: the performance of your startup.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

How much should a startup spend on accounting?

Bookkeeping and accounting don't inherently come with their own costs. However, some startups use specialized software or freelance bookkeepers. Check the pricing tiers of solutions like QuickBooks Live to see what plans are right for you. Once you've selected a solution, you can add Slash to your stack for no additional cost.

The Best Multi-Entity Accounting Software: Comparison, Features, and Benefits

What are some SaaS metrics I should track when bookkeeping?

Some common SaaS metrics include recurring revenue, customer acquisition cost (CAC), lifetime value (LTV), and churn. Since these companies are often internet-based or cloud-based platforms, most of their expenses will come with digital receipts. These receipts can be easy to miss, so make sure to identify any attached documents or PDFs from online purchases or recurring subscriptions.

Should I consider outsourcing accounting to bookkeeping services?

Some startups may outsource accounting to bookkeeping services if they feel overwhelmed by reconciliation and tax preparation. However, these full service solutions can be expensive, and may not be well suited for your startup's exact needs. Pairing Slash with a solution like QuickBooks allows more flexibility and automation at a lower price.

Accounts Payable Outsourcing: Is It the Right Option for Your Business?

Read more from us