Working Capital Loans for Startups: How They Work and Where to Apply

Almost all startups, no matter their industry, will struggle to turn a profit for the first year or two of their lifecycles. When your spending is constant but your revenue is irregular, it can be tough to keep your head above water. This cash flow gap can appear even when your startup is financially healthy and growing at a good pace.

Early-stage founders can use working capital loans to bridge these gaps. These loans are meant for short-term operational needs rather than for long-term building or investment. Whether used for product development, rent, or inventory, additional liquidity can help startups push through a period of cash crunch. There are quite a few types of working capital loans, leaving some founders wondering which they should choose and when they should act.

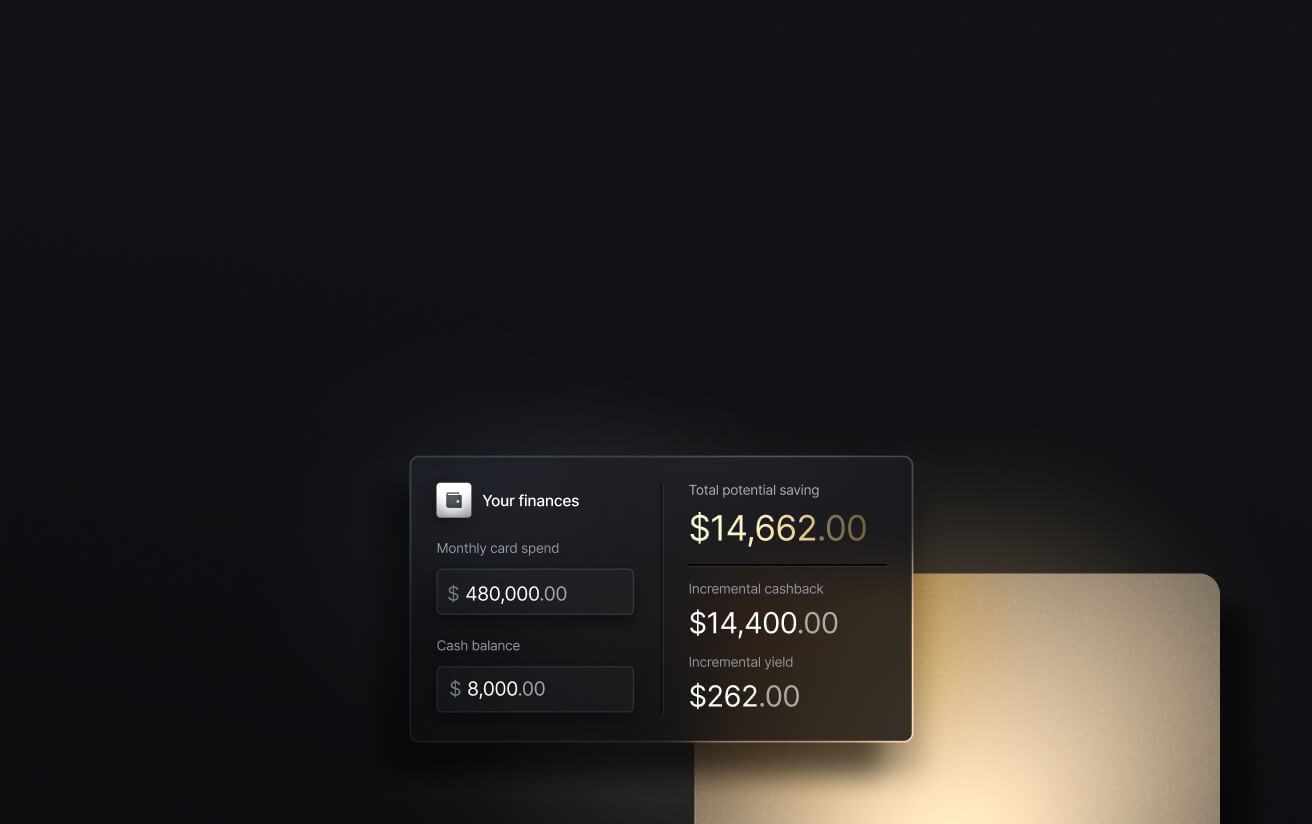

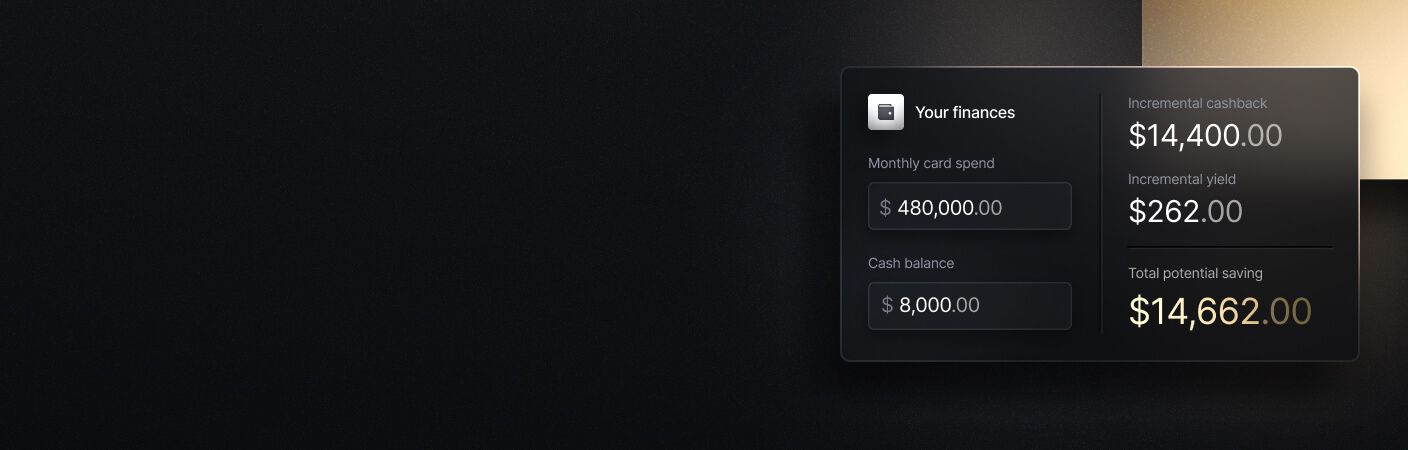

This guide explains what working capital loans are, which types suit different startup situations, what lenders look for, and how to make the right call based on where your business stands today. We’ll also discuss how Slash Working Capital can support your startup’s growth.⁵ Slash offers a line of credit that you can access directly from the Slash dashboard, allowing you to draw funds whenever you need an extra injection of capital. You can choose short-term repayment options that match your cash flow, helping you cover operating expenses and manage timing gaps without taking on long-term debt.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What Is a Working Capital Loan?

A working capital loan is short-term financing designed to cover a business's day-to-day operating expenses. These loans are built for operational needs like payroll, rent, inventory restocking, and closing accounts receivable (AR) gaps when customer payments fall behind. They’re not meant for long-term investments or major asset purchases, as they often carry repayment timelines between 6-18 months.

While a business can operate without a positive cash flow, it cannot operate without capital. The “working capital” in its name is simply a reference to how the money is typically used by the borrower. Working capital is the total of your current assets after subtracting your current liabilities. Calculating this number will reveal the funds you have on hand and the overall liquidity you have to support operations. Without positive capital, businesses can’t pay their employees or source necessary materials.

Many working capital loans come with rigid repayment schedules that can restrict a startup’s movement, even with the extra liquidity. Slash Working Capital, on the other hand, offers flexible repayment terms of 30, 60, or 90 days. Our working capital financing functions as a line of revolving credit, meaning users have access to a pre-approved amount of funding rather than an upfront lump sum. This enables first-time founders to align repayments with their revenue cycles and only pay for the capital they actually use.

Why Startups Need Working Capital Loans

If revenue slows but spending doesn’t, you may be approaching a gap in capital. Here are some scenarios where an otherwise healthy startup may need a working capital loan:

- Fluctuating or seasonal revenue: Some businesses may see annual spikes and slowdowns that inherently come with the product or service they offer. For example, a tax e-filing service will see most of its activity in Q1, and a camping supply company may see slower business in the winter. Working capital loans may be called upon to help continue growth during revenue offseasons.

- Slow-paying customers: Some B2B transactions take anywhere from 1-3 months to be fully paid off. As open invoices sit idly in another company’s accounts payable (AP) department, working capital may be growing thin at the business that’s waiting to receive the payment. This can be especially problematic when these delays occur among a startup’s first few clients, as early customers bring key income.

- Rapid growth that outpaces current assets: Quick growth can create sudden cash flow crises. A surge in orders may require you to double your inventory investment and boost hiring before revenue actually hits your account. While a spike in activity is generally great news for a startup, they may need short-term financing to catch up to demand.

- Time-sensitive business opportunities: Some of the best moves a startup can make are unplanned. Perhaps bulk inventory suddenly becomes available at a discounted price, or you want to boost marketing to match a viral trend. Maybe a competitor just went under and their customers are available. Working capital financing gives you the ability to act when the window is open.

Types of Working Capital Loans for Startups

There are eight main types of short-term business loan, each with different timelines and refinancing options. These types include:

Line of Credit

A business line of credit gives you access to a set pool of funds that you draw on as needed and repay on a revolving basis. You only pay interest on what you use, which makes it efficient for businesses whose cash needs fluctuate. The flexibility that a working capital line of credit offers makes it well-suited for startups with recurring but unpredictable liquidity needs. Slash Working Capital is built around this structure, giving users on-demand access to money without the lump sum loan.

Short-Term Loans

Short-term loans provide a lump sum upfront that’s repaid over a fixed schedule over a short period of time. Funds are released quickly compared to traditional bank loans, sometimes within 24 hours through alternative lenders. However, they often come with high fees that add up as time passes, so startups should be ready to repay the loan sooner rather than later. Short-term loans are a practical choice when you have a specific, time-sensitive expense and need cash fast.

Invoice Factoring and Financing

If your startup is sitting on a large pile of unpaid invoices owed from other businesses, invoice factoring lets you convert that future cash into present cash. You sell your open invoices to a factoring company for a percentage of the invoice value upfront (typically 70–90%), and the company collects from your clients directly. Invoice financing is a similar tactic that allows businesses to use invoices as collateral for a loan.

Merchant Cash Advance

A merchant cash advance (MCA) allows businesses to quickly take out a loan that’s based around their volume of sales. That loan is then repaid with a part of their weekly revenue. MCA providers often take portions of incoming payments via credit card transactions, so they primarily partner with B2C companies. While MCAs can fund quickly with minimal documentation, they often come with high fees and a strict repayment schedule.

SBA 7(a) and SBA Express Loans

Many financial institutions offer Small Business Administration (SBA) loans that are partially guaranteed by the federal government. This allows lenders to offer favorable terms like lower interest rates, longer repayment periods, and more flexibility on collateral. For startups with a brief credit history, SBA loans can be a great working capital financing option.

The catch, however, is the application process; it can take up to three months to be approved for a loan. SBA Express loans were created as a faster alternative, with a response time as quick as 36 hours. These loans carry lower maximum amounts, capping at $500k as opposed to a standard SBA loan’s max amount of $5 million.

Revenue-Based Financing

Revenue-based financing provides a lump sum in exchange for a fixed percentage of monthly revenue that lasts until the total repayment amount is reached. Unlike an MCA, which consistently draws from online transactions, revenue-based financing takes from all sources of revenue at the end of each month. Since it’s percentage-based, slower months mean smaller payments. This sort of structure can be ideal for B2B companies with a reliable cash flow.

Equipment Financing

Equipment financing is the process of getting a loan to acquire business equipment such as company vehicles, medical supplies, technology, and even office furniture. With this type of loan, companies can spread the cost of purchasing out over time using the equipment itself as collateral. This allows businesses to acquire the service and production-related supplies they need without running out of capital reserves. Equipment financing is best suited for startups that heavily rely on physical appliances.

Business Credit Cards

While business credit cards aren’t technically loans, they function as revolving working capital when used strategically. They're easy to access, provide immediate liquidity, and often come with perks and rewards. For startups in early stages, a business credit card may be the most accessible first step toward building a working capital cushion.

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What Lenders Look For When Approving Startups

Your choice between financing options may end up being influenced by each loan’s individual qualification criteria. Lenders keep different factors in mind when approving startups, such as:

Minimum Time in Business

Lenders want to know that they can trust the stability of your business, so they often prioritize startups that have been in operation for a healthy period of time. Traditional banks and SBA lenders can require at least two years of business history, while some fintechs and alternative lenders may approve companies less than a year old.

If your startup is pre-revenue or in a very early stage, your realistic borrowing options narrow considerably. The first place new founders should turn is Slash. Slope Bank, our lending partner, considers your complete financial picture across multiple platforms and accounts. Our Working Capital Financing can then be tailored specifically to your startup and its industry, meaning you won’t have to build several years of credit history to get a loan that works for you.

Monthly Revenue Thresholds

Lenders will often use monthly revenue to assess your repayment ability and set your loan size. Minimum thresholds vary widely, and can be adjusted based on what the borrower seeks and when they plan on repaying. SBA loans require at least $100k in annual revenue to qualify, which means your monthly revenue minimum is essentially $8,333. Before applying for any loan, make sure you have financial reports and bank statements that can prove your income.

Credit Score

For startups without an established business credit profile, lenders often look at the founder's personal credit score as a proxy for creditworthiness. Different lenders come with a variety of credit score requirements, but we can again identify the Small Business Administration’s standards: you must have a personal credit score of 600+ to apply for an SBA loan. No matter the financing option, lenders will usually offer better repayment terms to borrowers with higher credit scores.

Collateral or Personal Guarantee Requirements

Secured working capital loans are loans that require the inclusion of either collateral or a personal guarantee. In this context, collateral may consist of equipment, real estate, or accounts receivable that secure the loan through value. If your business can't repay, your collateral may be seized. A personal guarantee means your own money and possessions are the assets at stake. Secured loans can be risky, so it’s smart to consider them only when you’re confident in the consistency of your future cash flow.

Working Capital Ratio

Lenders may evaluate your working capital ratio, which is the number that represents your current assets divided by your current liabilities. A ratio above 1.0 means you have more short-term assets than short-term obligations, while one below 1.0 suggests you may already be in a liquidity crunch. For a startup, a realistically healthy working capital ratio is often between 1.5 and 2.0. A high ratio shows that you have sufficient liquidity to cover short-term debts while holding enough cash to operate efficiently.

How to Choose the Right Working Capital Loan

While some startups may only have a couple loans to choose from based on their financial standing, more established small businesses can choose any of the seven we’ve discussed. The right option depends on your answer to a few questions:

- How urgent is your need? Some financing options, such as short-term loans and merchant cash advances, can get funds to your business account within 72 hours. If you have a couple months of runway before cash gets particularly tight, the long approval period of an SBA loan can align with your timeline.

- What's the money actually for? Do you need quick cash to address a sudden expense, or are you looking for extra liquidity for recurring needs like upkeep and payroll? Different financing types match different use cases. Revolving products like lines of credit and business credit cards work well for ongoing, variable needs. Lump sum options may be better for one-time, specific payments.

- What does capital actually cost you? Using interest rates and factor rates, calculate your total repayment amount across the estimated loan term to figure out how much extra money you could end up paying. While certain metrics between lenders may seem similar on the surface, different schedules and fees can lead to surprising totals at the end of the period.

- Are you comfortable with the guarantee requirements? To access the lower interest rates of a secured loan, you have to be ready to put your personal assets on the line. If you’re not confident enough in your startup’s solvency to be comfortable with this arrangement, then you should instead consider borrowing via an unsecured loan. Before signing any contracts, make sure you know whether the loan you’re receiving comes with any kind of personal guarantee.

For many early-stage startups, a business line of credit can be the right first move, as it provides flexibility and doesn't require in-depth cash forecasting. Lump sum loans may be a better fit for situations with a defined, near-term funding requirement.

How Slash Helps Startups Manage Working Capital

It can be tough to find a financial institution or lender that quickly approves early-stage businesses without requesting an extended financial history or a personal guarantee that puts your assets at risk. With the help of our partner bank, Slope, our Working Capital is built for first-time founders looking for exactly that.

Slash offers flexible term loans with 30, 60, or 90-day repayment windows without personal guarantees, early repayment penalties, or hidden fees. This allows startups to align their repayments with their revenue cycles and only pay for the capital they actually take advantage of.

In order to apply, businesses are asked to provide an estimate of annual revenue as well as banking information in order to verify income. Approval can come in less than three business days and financing amounts can be up to $250k (or more, with additional qualification steps). Eligibility is solely determined by Slope, and may be determined based on factors such as business requirements, revenue thresholds, and credit review. Slope performs a soft credit check as a part of your application that does not affect your credit score.

Our working capital loans are only a small part of our overall business banking platform.¹ Slash can help startups manage cash flow with features such as:

- The Slash dashboard: Our platform comes with an integrated dashboard that displays all payments, employee spend, virtual accounts, financial analytics, and more in the same place.

- Connected AI agents: With support for Model Context Protocol (MCP), users can now connect AI agents directly to their business finances. Create cards, send payments, manage invoices, and query your transaction data, all through Claude, ChatGPT, and other MCP-compatible agents.

- Cryptocurrency payments: With built-in on/off ramps, businesses can send and receive USD-pegged stablecoins like USDC and USDT.⁴ This allows companies to access potential benefits like faster settlement and lower processing costs, while avoiding the price volatility associated with many other cryptocurrencies.

- Accounting integrations: Automatically sync transaction data with QuickBooks Online, Xero, and Sage Intacct for simplified reconciliation and reporting.

- Slash Visa® Platinum Card: A corporate charge card that earns up to 2% cash back on company spending, with configurable controls, spending limits, and strong fraud protection.

If you're an early-stage founder looking for additional liquidity, our Working Capital can help you access quick funds – and the Slash platform can help you with just about everything else.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What personal credit score do you need for a working capital loan?

A good credit score is generally above 670, but lender requirements vary. As is true with all things credit score, the higher your score, the better terms you'll likely be offered.

How to Get a Working Capital Loan: Key Insights for Small Business Owners

What are CAPlines?

CAPLines are a series of loan programs offered by the SBA that allow small business owners to take out loans specifically for seasonal or cyclical needs.

Why would my business not qualify for a loan?

There's a host of reasons a startup may not qualify for a loan, including poor cash flow/revenue, a low credit score, or outstanding debt. Different loan options assess different factors, so getting rejected by one lender doesn't exclude you from getting approved by another.

What is the Accion Opportunity Fund?

The Accion Opportunity Fund is a nonprofit small business lender that specifically helps businesses from underserved communities. To do this, they consider factors beyond credit score, such as cash flows and tax returns, and lend based on business needs.