The Only Constant for Startups Is Change

Starting a company means believing that something about the world isn't good enough. You see a product that could be simpler, a process that could be faster, a market that could be served better. Disruption, iteration, and evolution are all just words for the same thing: in the end, every startup founder wants to create change.

It’s a philosophy we understand at Slash. When Victor and Kevin founded Slash in 2021, the goal was straightforward: sneaker resellers needed a better banking service.¹ But when the sneaker market took a hit, our strategy had to adapt. We expanded our focus to serve more industries and arrived at a broader mission: to end one-size-fits-all banking. Our evolution reflects an enduring principle. If you want to create change, you sometimes have to be willing to rethink your own approach, too.

Now we've recognized something else that needed to change: how Slash serves startups. As a startup ourselves, we know what it takes to run one. We understand why startups prioritize automation, since manual work slows small teams down. We know how powerful it is to build tools for specific industries, because we've felt the pain of using generic software. We ship often not just because we care about improving our product, but because iteration is how startups survive.

After months of refining our platform and expanding what we offer, we're officially launching a new focus: Slash for Startups.

The pitch is simple. Your bank should help you keep more of what you earn. It also should not limit your ability to extend your runway just because you’re just starting out. Industry-leading cashback, accessible treasury, and powerful expense management tools should be available from day one.⁶

If that sounds like a bold claim, it is. So instead of leaving it at that, we want to show you how we've been building with startup founders in mind.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What Should Startups Actually Look for in a Financial Platform?

Every financial platform serves a specific purpose. Some are built for small businesses. Some are designed for large corporations. Some focus on improving a single area in your financial workflow. Some try to handle all of your finances from end-to-end. There are business banking platforms, accounting systems, budgeting tools, digital wallets, financial SaaS products, and plenty of overlap between them.

With enough marketing spin, any of them can look indispensable. It is easy to get sold on a feature you may not actually need, especially when a provider is more focused on closing the deal than delivering lasting value.

For startups, these are the most important factors that should guide your choice of financial provider:

Built-In Treasury, Not Bolted On

Raising a seed round or Series A is exciting, but it immediately raises a question: what do you do with all that cash?

Your startup should be thinking about runway from day one. Money that isn't actively being deployed should still be working for you, without sacrificing flexibility. But many platforms gatekeep treasury access behind significant capital thresholds, or limit your returns if you're not holding enough cash in their accounts.

With Slash Treasury, you can generate steady, low-risk returns on idle funds while keeping them accessible. You shouldn’t need a large reserve to start earning, or lock into terms that make it harder to build runway early. When you can earn up to 3.83% annualized yield from the start, having that extra cash down the line can be the difference between scaling or stalling.

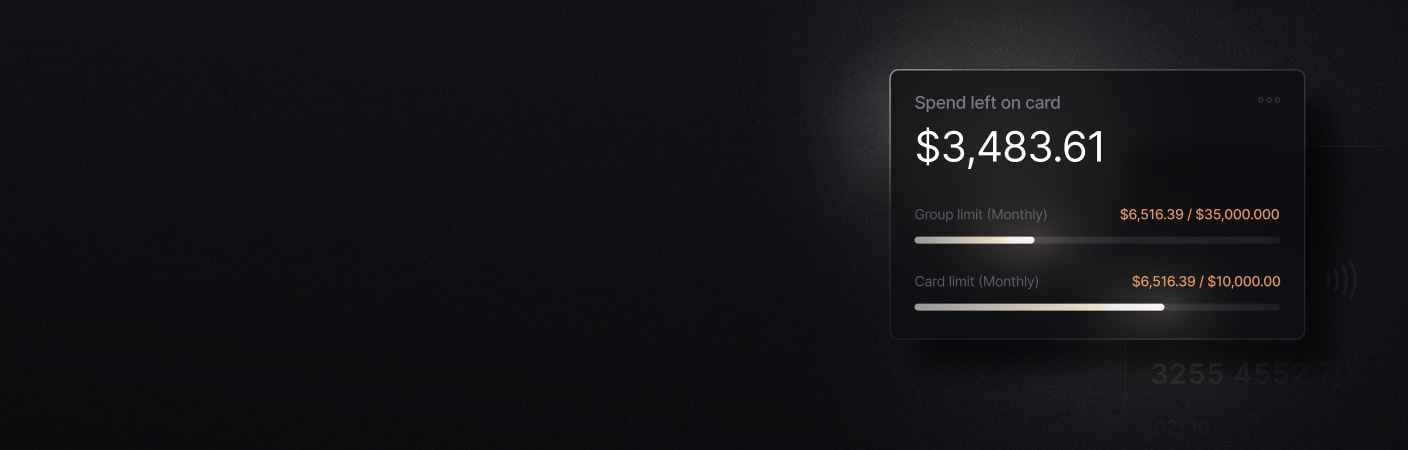

Scale Spend Without Chaos

As you start hiring and scaling, you need a simple way to deploy company funds across the team. Speed matters, but so does control. The best platforms make it easy to issue cards, configure spend limits, and enforce policies without slowing anyone down.

Think about what it looks like when a startup goes from five people to twenty. Suddenly you have team leads buying software subscriptions, a marketing hire running paid campaigns on a personal card waiting for reimbursement, and an office manager expensing supplies with no clear approval workflow. Without the right system, finance becomes a game of catch-up. At the speed startups operate, falling behind on spend visibility can mean burning through runway a lot faster than you may have predicted.

When those cards also generate cashback, your operating expenses start working for you instead of just flowing out the door. It is a small margin on any individual transaction, but across hundreds or thousands of monthly charges, it can compound into serious savings.

Automation as Leverage

The name of the game with startups is to do more with less. Your financial platform should reflect that.

A survey by Time Etc found that entrepreneurs spend more than a third of their working hours on administrative tasks. The most common time-waster? Logging expenses. Modern financial systems can automate transaction recording across cards and payments, apply AI-powered fraud detection, integrate with accounting and ERP software for reconciliation and reporting, streamline approval routing, simplify invoice management, and much more.

The right platform reduces manual work, limits errors, and delays the need to build out a large finance team as you scale. When your founding team is already stretched thin, the last thing you need is someone spending ten hours a week categorizing transactions and tracking down receipts. Every manual financial process you can eliminate is an hour your team gets back for the work that actually moves the needle.

Infrastructure That Adapts

As your company grows, the systems you use will evolve. API access allows you to integrate financial data into your broader tech stack, build custom workflows, and maintain flexibility as new tools come online. A platform that locks you into a rigid structure today will become a liability tomorrow, especially if migration means re-establishing banking relationships, reissuing cards, or rebuilding integrations from scratch.

“Having 50 employees means that when a customer tells me something, I can raise it up directly to our engineering team, our CTO, our CEO,” explained Nico Gutierrez, a member of Slash’s Startups team. “We actually listen. Someone we onboarded recently needed a specific feature in invoicing. I brought it up to our team, and now it’s in the pipeline.”

The best financial infrastructure is the kind you never have to think about replacing. It should be flexible enough to support you at ten employees and powerful enough to scale with you at two hundred. That’s why we don’t build our roadmap in a vacuum at Slash. We listen to our users, adjust our priorities based on their feedback, and deliver the tools startups need at every stage of growth.

What Your Startup Needs to Know About Slash

The Slash proposition is simple: we will save your startup more time and money than any other platform. It’s a bold claim, but we’re comfortable making it. Here’s why:

Leading Cash Back Rewards

The Slash Visa Platinum Card earns up to 2%+ cash back on your spending, with no cap on how much you can earn. Other providers either don’t match our rate, make it difficult to access the highest rate, or structure rewards in ways that reduce what you ultimately earn.

For instance, Rho requires you to join its Platinum program to get its maximum earn rate, which in turn requires you to keep at least 50% of your company’s assets on the platform. While not inherently bad, it adds needless complexity. Or consider Brex. Their points-to-cash redemption rate is $0.006 per point; even with heavily optimized category spending, it can be difficult to match the effective value of flat-rate cashback.

With Slash, you can access up to 2%+ cash back on card spend and fee-free domestic transfers for just $25 per month.

Card providers generally fall into one of two categories: they either cap rewards at 1.5%, or they offer points-based programs instead of direct cash back. Mercury and Ramp fall into the first group, while Brex and BILL fall into the second. If your goal is maximizing the returns on your spending, 2%+ cash back with no ceiling is hard to beat.

Treasury Without Fees or Minimums

Many integrated treasury products are only accessible once your startup is already well-established. Mercury, for example, requires at least $250,000 in checking balances before you can access its treasury product. Minimum balance requirements can also limit flexibility. Moving funds out may trigger fees or force you to close and reopen accounts, which is far from ideal when you need liquidity.

With Slash, you can access treasury from day one and earn the maximum rate without meeting a minimum balance requirement. That means you do not have to tie up excess capital just to qualify for better returns. Slash Treasury invests in money market funds from Morgan Stanley and BlackRock, delivering institutional-grade yield without institutional-style barriers.

For a startup that just closed its seed round, this can be particularly impactful. You might have $500K in the bank and eighteen months to prove your model. Even a modest yield increase on that capital can extend your runway by weeks. Weeks that, at the right moment, can make the difference between closing your next round or running out of time.

Protection That Grants Peace of Mind

For early-stage startups, cash on hand can increase quickly after a fundraise hits your account. Once balances exceed $250,000 in a standard bank account, funds above that limit may not be fully covered by FDIC insurance.

Many startups may not think about deposit insurance until they need to. But as balances move into the seven figures, concentration risk becomes part of the equation—when you’re raising $10 million, $250,000 is not much of a cushion. With Slash, you can ensure your entire balance is protected without needing to manage multiple banking relationships yourself.

Slash accounts are provided through Column N.A.’s sweep network, which automatically distributes deposits across multiple FDIC-insured banks while keeping your funds consolidated in a single account.² Column’s network offers expanded FDIC coverage up to $150 million, compared to $50 million through a sweep network like IntraFi.

Dedicated Customer Support

Our support team is available 24/7, and they know the product inside and out. When you reach out, you are not routed to a bot or an outsourced call center. You are communicating with people who understand how Slash works and can resolve issues quickly.

“At the end of the day, it’s a relationship business,” Gutierrez said. “At Slash, you’re going to get a banking experience where you’re heard and where you have a direct line to the people behind the product.”

If something is not working the way it should, or if a key feature is missing from your financial stack, we do not just log a ticket. We route that feedback to the right team internally and use it to improve the platform. In fact, many of our product updates start with customer conversations. “A lot of the time, if you’re having a problem, that means someone else is having that problem,” Gutierrez said. “And we have the ability to change that.”

Built-In Cryptocurrency Capabilities

Slash allows you to hold, send, and receive USDC and USDT natively within the platform.⁴ We handle the technical complexity so it feels like traditional banking, even though private keys, gas fees, blockchain connectivity, and transaction validation are all managed behind the scenes.

Native crypto payment support is especially useful for startups working with international suppliers or customers. Because blockchain networks operate outside traditional banking rails, crypto transfers can avoid many of the fees, delays, and time restrictions associated with cross-border wires. Even if you are not running a global operation, B2B payments on stablecoin rails can be fast, secure, and cost-effective.

For startups building in web3, this is expected. For everyone else, it is optional leverage. Having the ability to move funds through stablecoins gives you an alternative when traditional banking infrastructure is slow, expensive, or unavailable outside normal hours.

Bespoke Software Discounts

One of the overlooked advantages of choosing the right financial platform is what comes with it. Slash Perks gives users access to more than $1M in discounts on the software tools startups rely on every day. From cloud infrastructure and design tools to CRM platforms and analytics suites, these savings can heavily lower the cost of your core tech stack.

If your company relies on AWS, Google Cloud, Figma, HubSpot, or similar tools, Slash Perks helps reduce costs across more than 100 SaaS platforms and cloud services. Combined with up to 2%+ cash back on card spend, the total savings available to Slash users can be difficult to match elsewhere.

More Than a Platform: The Slash Founders Community

Building a startup can be isolating. You are making high-stakes decisions every week, often without a large advisory network or an experienced finance team to rely on. Most financial providers keep that outside their scope. They provide a dashboard, offer a support line, and leave the rest to you.

Slash takes a different approach. Beyond the product, startups that use Slash gain access to a community of founders facing similar challenges. Our Founders Series brings leaders together in person, giving us the opportunity to hear feedback directly and build real relationships with the teams we support.

Simar Boparai from our Startups team described the goal of a Founders Series event this way: “The immediate sign up isn’t what’s important to me,” she said. “What’s important is building a really strong community. A month down the line, I want people to work with Slash because they think ‘wow, Simar, or Shaan, or whoever at Slash is so cool.”

Not only is our team cool, but so are our events. Last month, we invited founders from around the Bay Area to Sonoma Raceway for a hot lap on the track. We hosted a Michelin-starred dinner where founders had candid conversations about the realities of building their businesses. And we regularly welcome industry leaders to the Slash office to speak with our team and community, helping us better understand the challenges they face and how we can support them.

“I want [our community] to be an actual resource for people,” Boparai said. “These are people who are building companies at the intersection of culture and technology—literally rewriting the human experience. That's revolutionary work, and more than anything I want Slash to be a part of their story.”

Where the Differences Matter

It is easy to build a comparison table and declare yourself the winner. Every fintech company does it. Instead, let’s be honest about where the real differences show up in day-to-day operations.

Cash back: Slash’s up to 2%+ uncapped cashback rate is the highest in the space for a straightforward monthly fee. Mercury and Ramp cap out at 1.5%. Brex offers points that can be converted, but the effective return depends on how you redeem them. Rho can match the rate, but only if you commit half your assets to the platform.

Treasury: Slash stands alone in offering our best treasury yields to every account holder with no reserve minimums and near-immediate withdrawal liquidity. Mercury’s $250K minimum threshold means that many seed-stage startups likely cannot even access their treasury product. Brex and Ramp offer yield-bearing options, but they come with conditions and restrictions that can limit returns for smaller reserve balances, particularly when you need to move money quickly.

Support: When a wire transfer does not go through on a Friday afternoon before a critical vendor payment is due, the quality of your support experience stops being a nice-to-have. Slash’s 24/7 team with direct product knowledge means you are not waiting until Monday for someone to read a script and escalate your ticket.

Crypto: Most fintech platforms either do not yet support crypto or just treat it as an afterthought. Slash’s native stablecoin capabilities are integrated directly into the platform, which means you can move between fiat and crypto without switching tools or managing separate wallets. For startups that operate globally or pay contractors internationally, this is a genuine competitive advantage.

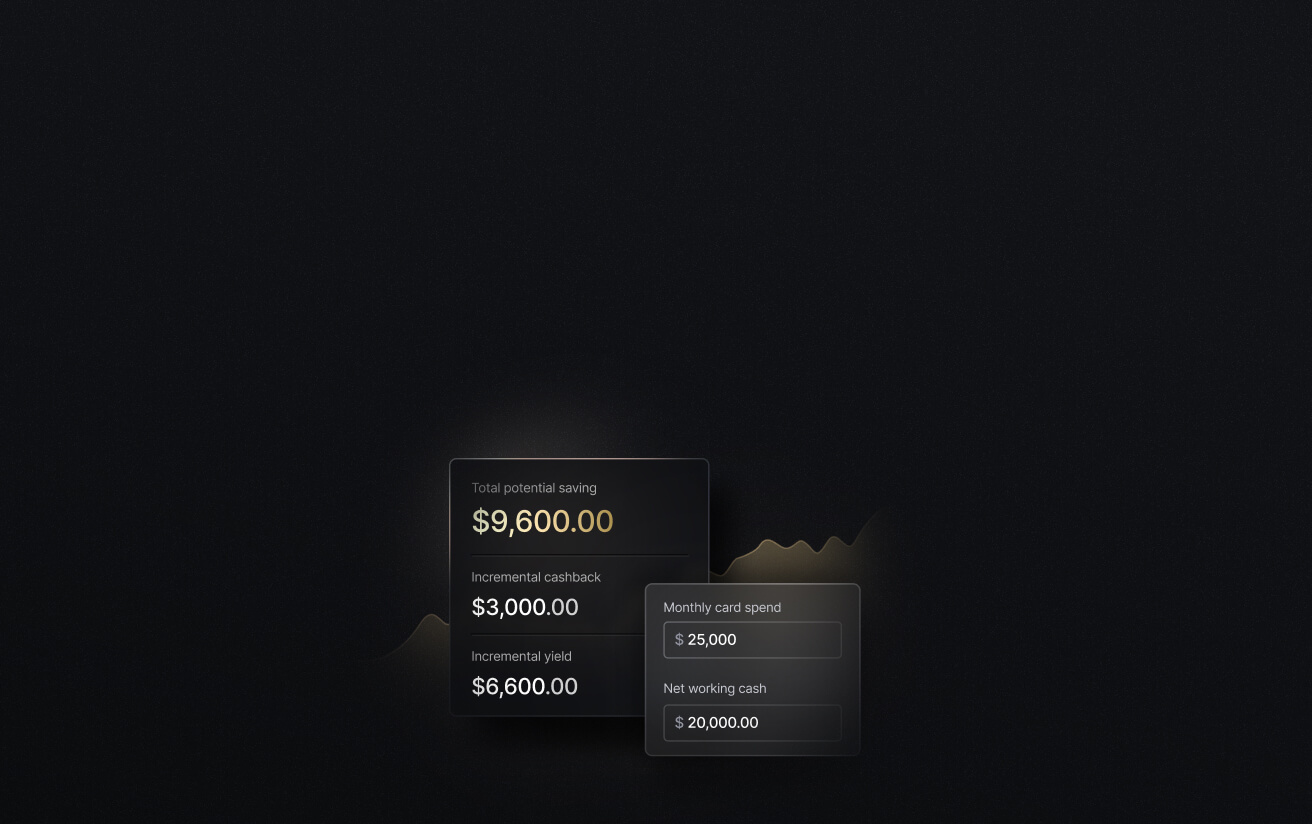

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

The Slash Philosophy: From the People, Product Follows

The fintech space is noisy. Every platform is going to tell you it is the best, the fastest, the most innovative. We get it. We’re doing it right now.

The difference between Slash and the rest of the field isn’t just about the features. It’s about philosophy. We believe that a startup’s financial platform should grow with the company, not around it. We believe that earning the best possible return on your spend should not require navigating tiered programs or meeting arbitrary asset thresholds. We believe that treasury should be available the moment you have capital to manage, not after you have hit a quarter-million-dollar balance. And we believe that the people building your tools should know your name.

That is the Slash thesis. It is simple, and it guides everything we build. If you are a startup founder choosing a financial platform right now, we would encourage you to look past the feature matrices and the marketing pages. Ask yourself: which platform is actually built for where I am today, and where I plan to be in two years?

We think the answer is Slash. But don’t just take our word for it. Try it and see for yourself.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Related posts

Best Startup Credit Cards 2026: Top Picks & Features

Treasury Management for Startups: A Complete Guide to Cash Flow, Liquidity & Risk