Bookkeeping vs. Accounting: Definitions, Key Differences, and What Modern Teams Need

Early hiring rounds among growing startups often look fairly similar. You might hire a finance controller to manage payroll and bookkeeping, a couple salespeople to pitch their product, and a few engineers to actually build that product. If you followed this exact checklist, though, you’d actually be making a common mistake. Did you spot it?

Accounting and bookkeeping are two different things. While some founders use the terms interchangeably, they’re separate types of work and they each produce distinct outputs. Bookkeeping is about recording every financial transaction that occurs within your business, categorizing them correctly, and keeping the underlying records organized and complete. Accounting builds on those records by analyzing and interpreting the data to produce financial statements, manage tax obligations, and inform business decisions.

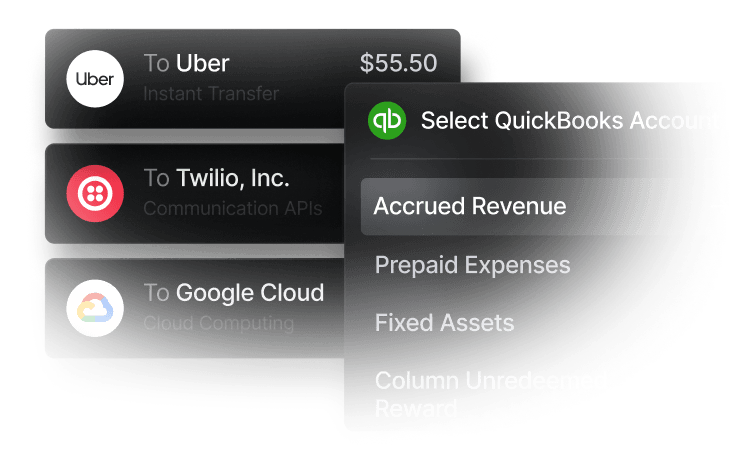

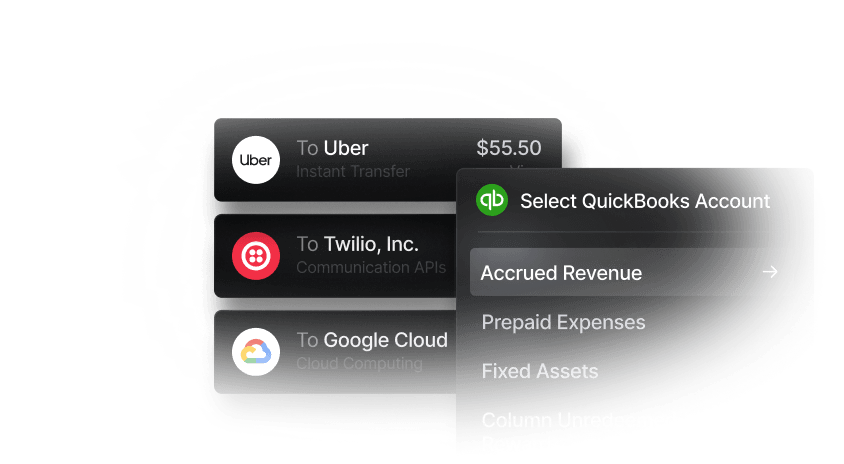

In this guide, we’ll review how bookkeeping works, how accounting works, the differences between the two, and which tasks call for which type of professional. We’ll also take a look at Slash, a neobank that comes with accounting features that can make it easier to manage your books.¹ With Slash, every transaction across your cards and outbound transfers is tracked and automatically categorized; from your dashboard, you can export enriched accounting data to the software you already use, including QuickBooks, Xero, Netsuite, or Sage Intacct.

What Is Bookkeeping?

Bookkeeping is the systematic documenting, organizing, and categorizing of every financial transaction your business makes. Any time money comes in or goes out, it needs to get logged, assigned to the right account, and stored in a way that can be retrieved, reviewed, and reported on later. That’s what bookkeeping is all about.

The focus of bookkeeping leans more towards accuracy and completeness than analysis. A bookkeeper's job is to ensure that their records reflect each transaction that happened in a given time period. When done correctly, you’ll have a trustworthy set of data that can make end-of-month reconciliation a lot more straightforward.

For a typical SaaS or e-commerce startup today, a month of bookkeeping might include matching card transactions to receipts and expense categories, issuing invoices to customers, applying incoming payments against outstanding receivables, and entering vendor bills for payment. While they can be tough in their own right, these tasks don’t require heavy strategy or analysis. They center around maintaining an accurate, complete, and organized record of what the business did financially.

Core Bookkeeping Tasks and Responsibilities

While the job might sound simple on the surface, most bookkeepers have a lot on their plate. Here’s a rundown of the tasks they commonly have to manage on a day-to-day basis:

- Recording transactions: Each sale, purchase, refund, and bank transfer gets logged into the accounting system with the correct date, amount, and account classification.

- Updating the general ledger: All transactions flow into the correct account in the general ledger, which is the master record of all financial activity. This ensures that account balances always stay current.

- Managing accounts receivable: Issuing invoices to customers, applying payments as they arrive, and tracking overdue balances are AR tasks that give the business a clear view of what it’s owed and when it’s all due.

- Managing accounts payable: On the other hand, AP tasks like entering vendor bills, matching them to purchase orders where applicable, and scheduling payments on time help meet obligations and keep vendor relationships intact.

- Reconciling bank and card statements: Along with recording transactions, bookkeepers also have to make sure they all line up. This means matching accounting records against bank statements, credit card statements, and payment processor reports to catch entry mistakes and duplicate records.

- Recording payroll: As payroll runs are logged, gross wages, tax withholdings, employer contributions, and net pay need to be recorded in the correct accounts.

- Document management: Documents can include receipts, invoices, contracts, payroll records, and more. Bookkeepers store each of these in an organized, auditable format so they’re easily accessible in the future.

What Is Accounting? How It Builds on Bookkeeping

Accounting picks up where bookkeeping leaves off. After bookkeeping produces the raw data, accounting makes sense of it. Accountants use the transaction records maintained by bookkeepers to prepare financial statements, analyze performance, manage tax strategy, and figure out how the business should allocate its capital.

While a bookkeeper produces ledgers and a running transaction history, an accountant produces formally prepared financial statements. These often include balance sheets, income statements, and detailed cash flow statements for defined reporting periods. Those statements are the documents a founder uses to understand the company and what investors evaluate during due diligence. They’re also a key factor that fintechs like Slash evaluate when underwriting businesses for working capital loans.⁵

Accountants can fill quite a few roles across different industries and structures. You may see corporate accountants managing books for a specific entity, controllers overseeing the accounting function across an organization, CPAs handling external audits and tax filings, and small business accountants laying a road map for a busy startup. Each of these cases requires a deeper level of analysis than standard bookkeeping responsibilities.

Key Accounting Tasks and Deliverables

Generally speaking, accounting encompasses a broader and more analytical set of responsibilities than bookkeeping. Here are some of the tasks accountants are typically placed in charge of:

- Adjusting journal entries: At the end of an accounting period, entries should be adjusted to account for accruals, deferrals, prepaid expenses, depreciation, and other items that bookkeepers may not have captured as part of their regular transaction recording.

- Revenue recognition: Accountants ensure that revenue is recorded in the correct period under Generally Accepted Accounting Principles (GAAP). Working with revenue timelines is a process that can be complex for subscription-based businesses or companies that handle a variety of contracts.

- Financial statement preparation: To create a full financial statement, accountants turn general ledger data into a classified balance sheet, multi-step income statement, and statement of cash flows.

- Management reporting: Some accounting teams dive a little deeper and develop budget-versus-actuals analysis, variance explanations, unit economics breakdowns, and scenario models.

- Tax compliance: Staying compliant with the IRS entails preparing and filing income tax returns, sales tax and VAT reports, Form 1099s, and payroll tax filings.

- Forecasting and capital planning: Using recent financial data, accountants can project future cash flows, model capital requirements, and help leadership make informed decisions about hiring and investments.

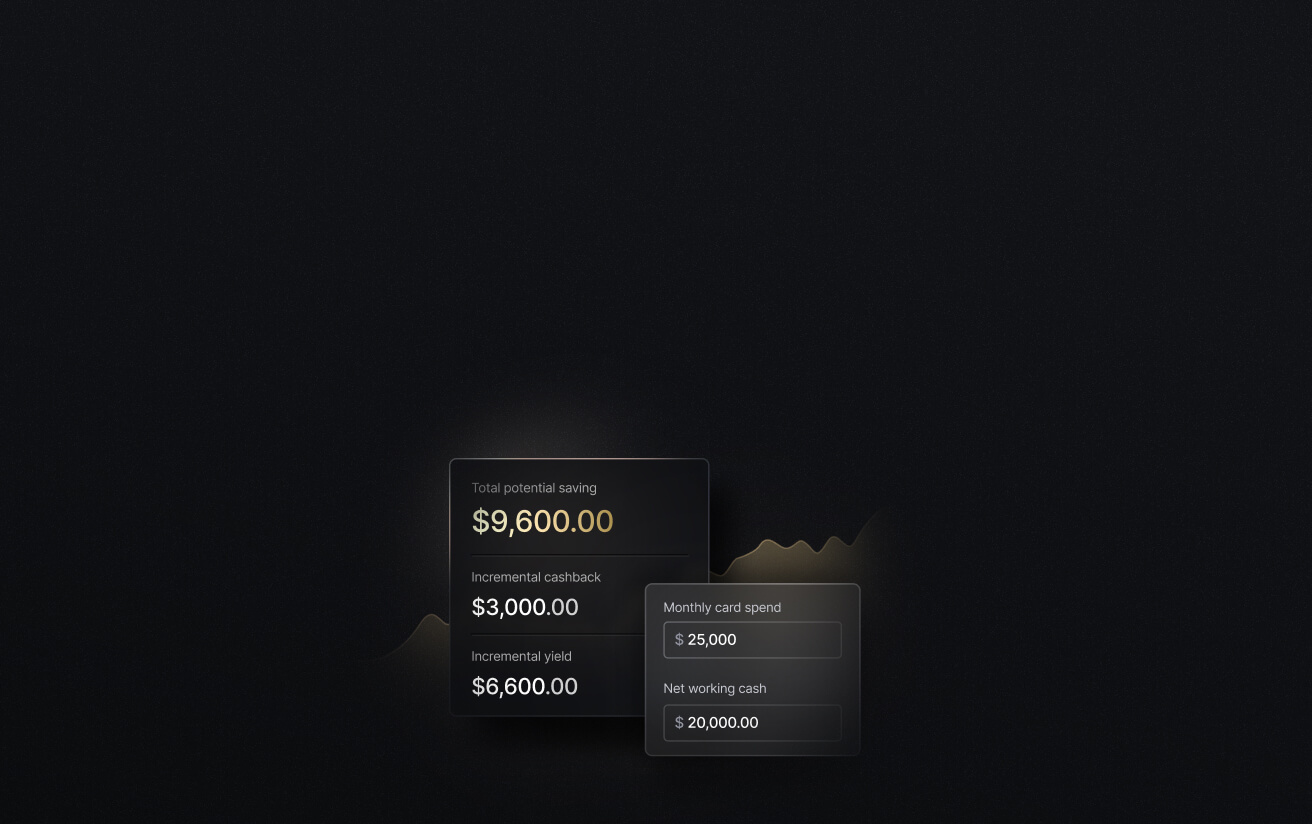

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Bookkeeping vs. Accounting: The Key Differences

In a nutshell, bookkeeping records what happened, and accounting explains what it means.

Bookkeepers work in the present, maintaining records that reflect recently completed transactions. Accountants use those records to produce reports about the past that can help forecast the future. A bookkeeper handles business transactions line by line, while an accountant transforms those transactions into insights that leaders and investors can use. It’s not exactly romantic, but they complete each other.

As distinct as each position is, you’ll often find some overlap at smaller organizations. For example, some bookkeepers at early-stage businesses produce basic monthly financial statements, and accountants at startups might handle most of the bookkeeping tasks. This might work during a business’s first couple years in operation, but it’s usually unsustainable.

While you shouldn’t have one employee that acts as a bookkeeper and accountant, you can adopt a software that does. Modern business banking platforms like Slash can automate parts of both functions. Slash integrates two-ways with QuickBooks Online, Xero, Sage Intacct, and NetSuite, meaning your banking data can flow right from one place to the next without transcription mistakes. Additionally, all business expenses made with the Slash Visa® Platinum Card are intelligently categorized based on your pre-configured rules.

Differences in Outputs: From Ledger to Financial Statements

Bookkeepers own the general ledger, the AR and AP subledgers, and the transactions that connect to them. Their output is a set of records that’s been reconciled against external statements and accurately reflects every financial event that happened within a given period.

Accountants can then use that ledger data to adjust entries for accruals and prepare reviewed financial statements. Oftentimes, they’ll also analyze KPIs, trends, margin ratios, burn rate, and forward-looking metrics to help management understand what to do next.

When Your Business Needs a Bookkeeper, an Accountant, or Both

While large companies will probably employ both accountants and bookkeepers, an early-stage business with tight margins may have a tougher time deciding who to hire. Your choice may depend on factors like transaction volume, revenue scale, and how much strategic financial guidance you’re looking for. Here are a few scenarios to consider:

- Solo consultant or single-person business: A one-person business with predictable revenue and simple expenses may be able to manage basic bookkeeping with accounting software and an occasional call to a CPA. A dedicated bookkeeper may not be necessary at this stage, since your accounting need is primarily compliance-focused.

- 10-person agency at roughly $2M in annual revenue: A business at this level is likely generating enough transaction volume and payroll complexity to benefit from a bookkeeper. You may also use a part-time accountant for tax compliance, financial statement review, and strategic planning conversations as the business makes hiring and investment decisions.

- Company with fiat and crypto operations: Even if it’s small, a Web3 or fintech company operating across currencies and processing stablecoin payments may want a senior bookkeeper and an accountant with knowledge of the industry. Crypto can be tricky, so it’s smart to arm yourself with employees that have relevant experience.

- Mid-sized corporation with a 200+ headcount: Once your company grows past its Series C funding stage and approaches 200 employees, you should be able to find room for both bookkeepers and accountants. Trying to assign all the tasks we’ve talked about to one type of employee is a recipe for delays and mistakes.

How Slash Can Help Your Bookkeeping and Accounting Processes

If you’re running a business with tight liquidity, it can be tough to decide what positions to hire for. You might want both a bookkeeper and accountant, but you may not be able to afford both. Slash can help delay this decision by reducing the manual work involved in both processes.

Using OCR technology, Slash can scan receipts and invoices and instantly populate fields that bookkeepers would have previously spent time filling themselves. As employees spend with the Slash Visa® Platinum Card, purchases are automatically categorized based on pre-defined rules, meaning no one has to squint at receipt details and make decisions on the spot. Eligible purchases also earn up to 2% cash back. Our platform is also built to help automate some of the more complex tasks accountants are in charge of. Twin, Slash’s AI agent, can be prompted to forecast future cash flow and create sophisticated charts based on your business’s current data. Twin can pore through all your company’s transactions and fully analyze your cash flow in minutes. Along with our accounting and bookkeeping tools, Slash also comes with the following features:

- High-yield treasury: Earn up to 3.80% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

- Native cryptocurrency support: Send and receive USD-pegged stablecoins USDC and USDT across eight supported blockchains for faster, lower-cost global payments.⁴

- Diverse payment methods: Slash supports a wide range of payments, including card spend, global ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- Reimbursements: Instead of managing reimbursements across multiple tools, teams can now submit, review, and approve reimbursements directly inside the Slash dashboard. Connect your bank account, upload your receipt, and let Slash capture the details.

When your company grows from a startup to a mid-sized business, you’ll likely need to onboard both an accountant and a bookkeeper. In the meantime, Slash can help you automate and manage some of their most essential responsibilities.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Is end-of-month reconciliation a job for a bookkeeper or an accountant?

It’s a job for both, in a way. After bookkeepers process and log transactions, they deliver all that data from a given month to the accountant. The accountant then reviews that material and adjusts it. The bookkeeper is the one that arranges the information used in reconciliation, while the accountant delivers the finished report.

Bank Reconciliation Made Easy: Prevent Errors & Simplify Accounting

What is a CPA?

A CPA (Certified Public Accountant) is a licensed accounting expert that holds a license given by the state to practice public accounting. They often operate independently, and businesses can hire them temporarily or as consultants.

How far out should I forecast my cash flow?

It depends on what you’re looking to prepare for. If your focus is on the short term, a 13 week cash flow forecast is a popular template. For the long term, you can forecast a full year into the future.

How to Build a 13-Week Cash Flow Forecast

Read more from us