Fleet Cards Explained: How They Work, Benefits, and How to Choose the Right One

If your business operates on the road—company cars, logistics and trucking, ground transportation, or rental vehicles—it may be a good fit for a fleet card.

Fleet cards provide a lot more than fuel discounts. They can give fleet managers and finance teams a clearer view into driver spending habits, help track fuel costs in more detail, and reduce the manual work associated with receipts and expense reporting. With the right setup, transportation-heavy businesses can monitor transactions more closely, better control how cards are used, and take measures to prevent fraud across their fleet.

In this guide, we will break down how fleet fuel cards work, the features that matter most, and how to choose the right provider for your business. We’ll also look at where fleet cards can fall short. For many businesses, fuel is only one part of overall spend. With Slash, your business can earn up to 2% cashback on all business expenses, along with real-time visibility, granular card controls, and integrated financial tools that help teams manage spending across every category, not just at the pump.¹

What is a fleet card?

Fleet cards are designed specifically for covering fuel and other vehicle-related costs. You may hear the terms “fleet card,” “fuel card,” and “gas card” used interchangeably, but there are some important differences.

At a high level, all three refer to payment cards used at fuel stations. However, fleet fuel cards are more specialized tools built for businesses that manage multiple vehicles and drivers. In addition to paying for fuel, they are often used for vehicle-related expenses like maintenance, repairs, and other operational purchases tied to a fleet.

Fleet cards are issued by dedicated providers such as Fleetcor and AtoB as well as major fuel companies like ExxonMobil and Fuelman. Many of these providers operate within their own fuel networks, while others offer universal cards that run on payment networks like Visa and are accepted at a wider range of gas stations.

What makes fleet cards different from standard credit cards is the level of control and visibility they provide. Fleet managers can set rules around how cards are used, including time-of-day restrictions, gallon limits, and merchant category controls. These cards are also tied to specific vehicles or drivers through tools like driver IDs and PINs, which makes it easier to track spending and reduce fraud.

Many fleet card providers also bundle their cards with fleet management software, allowing businesses to monitor fuel costs, track expenses, and analyze vehicle performance alongside transaction data. This combination turns a simple payment card into a broader expense management and operational tool.

How does a fleet card work?

Fleet fuel cards are designed to do more than just process payments. They create a structured system for tracking, controlling, and analyzing fuel and vehicle-related expenses across your business.

When a driver uses a fleet card at a gas station, they are typically required to enter a PIN or driver ID. This step links the transaction to a specific individual or vehicle. Once authorized, the purchase is processed through the provider’s network or a broader payment network like Visa, depending on the type of card.

Each transaction captures detailed data, including the number of gallons purchased, fuel costs, time and location, and in some cases vehicle mileage. This information is automatically recorded and made available to fleet managers through a dashboard or reporting system.

Where fleet cards stand apart from standard credit cards is how this data is used. Many providers integrate directly with fleet management software, allowing businesses to monitor fuel usage, track spending patterns, and flag unusual activity in real time. Managers can set controls that limit what drivers can purchase, where they can spend, and how much they can spend per transaction or per day.

This level of integration turns every fuel purchase into a data point. Instead of manually collecting receipts and reconciling expenses, businesses can automate expense tracking, monitor fuel costs more accurately, and make more informed decisions about their fleet operations.

Types of fleet fuel cards: Differences and use cases

The provider behind the card, whether it’s a major fuel brand, a dedicated fleet card issuer, or a newer fintech company, can shape how your company’s fleet cards are accepted, how discounts are applied, and how much control you have over spending. Some cards are designed to maximize fuel savings within a fixed network, while others prioritize flexibility and broader acceptance for drivers on the road.

Understanding these differences is key to choosing the right card for your fleet. Here are the main ways fleet cards are typically categorized:

Open-loop vs. closed-loop cards

Closed-loop fleet cards can only be used within a specific network of fuel stations, such as Shell or Fuelman locations, which allows providers to offer stronger per-gallon fuel discounts. Open-loop cards run on major payment networks like Visa or Mastercard and are accepted at most gas stations, giving drivers more flexibility. These open-loop cards are often referred to as “universal” fleet cards because they are not restricted to a single fuel network.

Credit-based vs. prepaid fleet cards

Credit-based fleet cards extend a line of credit, allowing businesses to pay for fuel and expenses upfront and settle the balance later. Prepaid fleet cards require businesses to fund the account in advance, which can help control spending and reduce risk. Some providers offer both options, giving fleets flexibility depending on their cash flow and credit profile.

For businesses with smaller fleets or mixed spending needs, a dedicated fleet fuel card is not always the most practical option. If your drivers are not consistently fueling within a single network, or if vehicle expenses are only one part of your overall spend, a more flexible payment solution can offer better coverage. Cards like the Slash Visa® Platinum Card provide broad acceptance wherever Visa is accepted, allowing teams to pay for fuel, maintenance, software, and operational expenses all in one place.

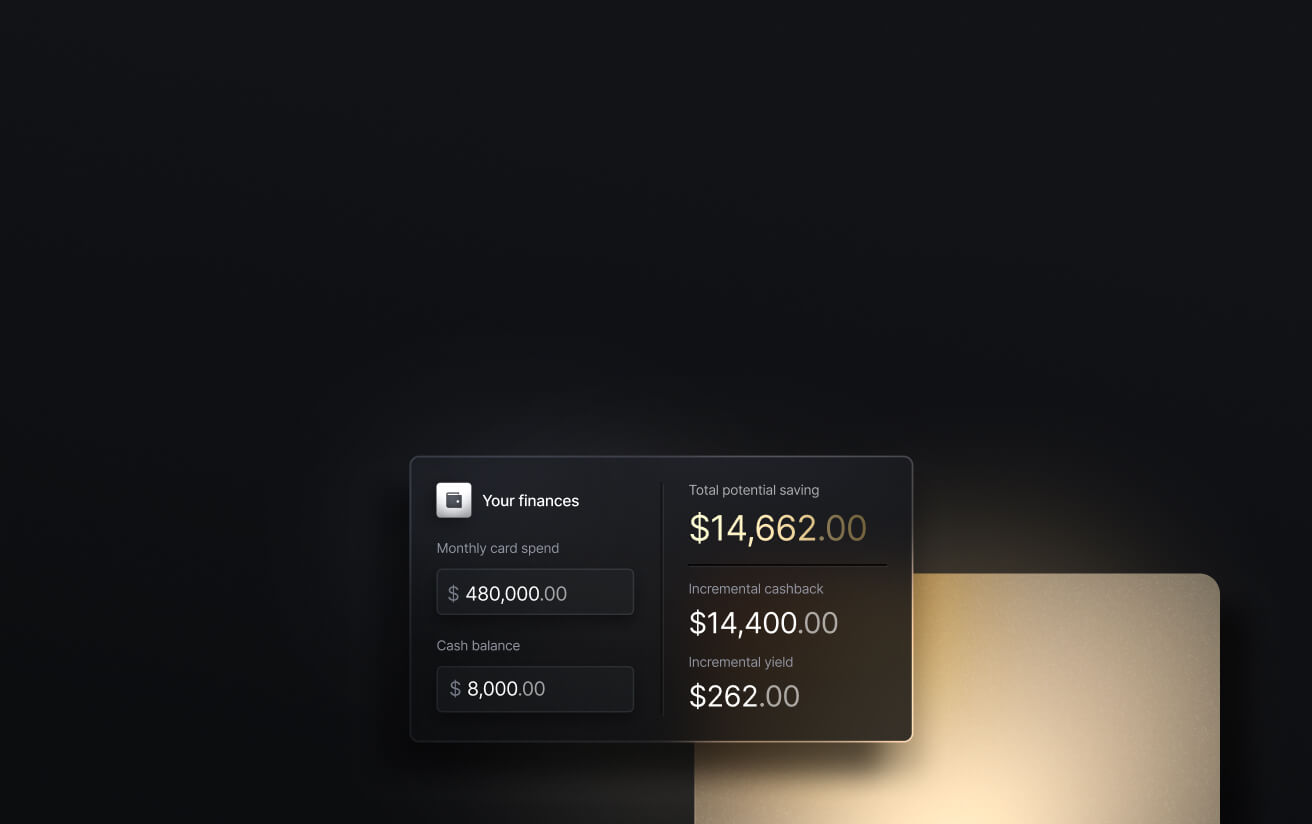

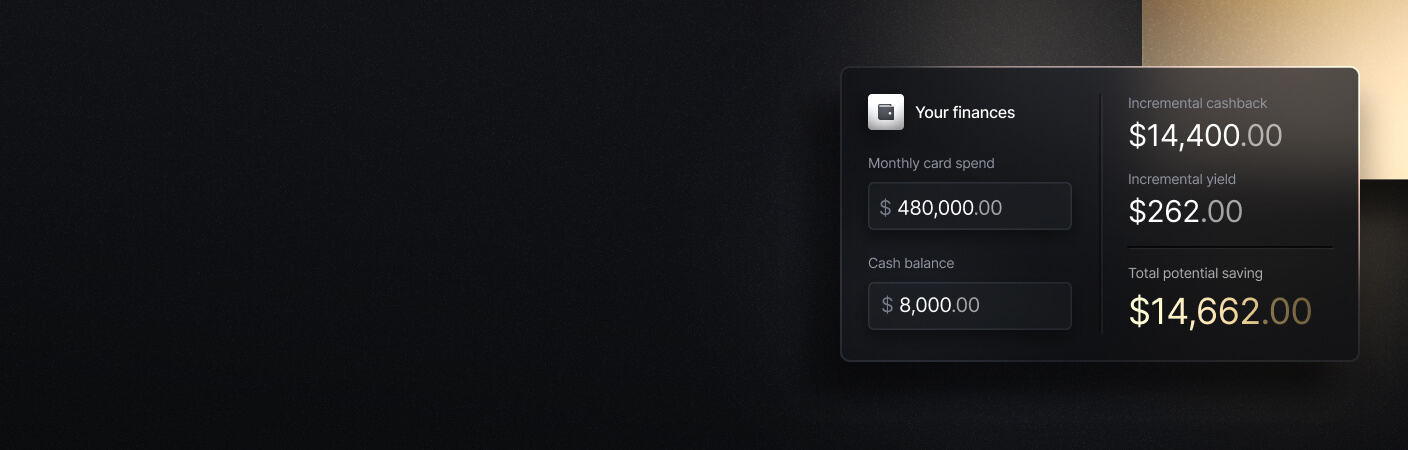

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Key features of fleet fuel cards

Fleet fuel cards work alongside fleet management systems to give businesses more control, visibility, and efficiency across fuel and vehicle-related expenses. Instead of treating each transaction as a standalone purchase, fleet cards turn spending into structured, trackable data that can be monitored and optimized over time. Here are some of the practical advantages of using fleet fuel cards:

Real-time spending controls

Fleet fuel cards allow managers to set detailed rules around how each card can be used. These controls can include limits on gallon purchases, restrictions on certain fuel stations, time-of-day usage windows, and merchant category blocks.

Within a fleet management system, these controls are enforced at the point of transaction. That means if a driver attempts to make a purchase outside of approved parameters, the transaction is automatically declined. This reduces unauthorized spending and ensures that fuel costs stay within policy without requiring manual oversight.

Driver accountability

Fleet cards tie every transaction to a specific driver or vehicle using tools like driver IDs and PINs. Before completing a purchase, drivers are often required to enter identifying information, which links the transaction directly to them.

This creates a clear record of who made each purchase, when, and where. Fleet managers can use this data to monitor driver behavior, identify inefficiencies, and address issues like excessive fuel consumption or unauthorized purchases. It also simplifies internal accountability by removing ambiguity around shared cards.

Fraud protection

Because fleet cards operate within controlled environments, they offer stronger fraud protection than standard credit cards in many fleet use cases. Restrictions on purchase types, fuel-only limits, and required driver authentication all reduce the likelihood of misuse.

In addition, fleet management systems can continuously monitor transaction data for unusual patterns, such as purchases outside normal locations or abnormal fuel volumes. These signals can trigger alerts or automatic declines, helping businesses catch fraud early and limit financial exposure.

Savings on fuel and operating costs

One of the primary benefits of fleet fuel cards is access to fuel discounts, often calculated on a per-gallon basis within a provider’s network. These discounts can add up quickly for fleets with high fuel consumption.

Beyond direct fuel savings, the data collected through fleet cards can also highlight inefficiencies in routes, driver behavior, or vehicle performance. Over time, this visibility helps businesses reduce overall operating costs, not just at the pump but across their entire fleet.

Centralized reporting without spreadsheets

Fleet fuel cards automatically capture transaction data and organize it into centralized dashboards and reports. This eliminates the need to collect paper receipts or manually reconcile expenses in spreadsheets.

Instead, fleet managers and finance teams can access real-time reporting on fuel costs, spending patterns, and transaction history across all drivers and vehicles. Many providers also integrate with accounting and expense management systems, making it easier to sync data, streamline reconciliation, and maintain accurate financial records without manual data entry.

Best practices for using fleet cards

Fleet fuel cards are most effective when they are paired with clear policies and consistent oversight. Here are some common ways that fleet managers get the most from their fleet cards:

- Assign individual cards instead of sharing: Issue a dedicated card to each driver or vehicle rather than using shared cards across your team. This makes every transaction traceable, improves accountability, and gives you cleaner data when tracking fuel costs and driver behavior.

- Set spending controls up front: Configure limits on gallon purchases, transaction amounts, fuel stations, and time-of-day usage before cards are distributed. Establishing these rules early prevents misuse and reduces the need for reactive enforcement later.

- Review reports from your FMS regularly: Make it a habit to monitor transaction reports, fuel usage trends, and spending patterns within your fleet management software. Regular reviews help you catch anomalies, identify inefficiencies, and adjust policies before small issues become costly problems.

- Require driver ID and PIN authentication on every transaction: Ensure that drivers must enter a driver ID and PIN for every purchase to link transactions to specific individuals. This adds a layer of security, deters fraud, and strengthens your ability to audit and enforce spending policies.

Earn rewards outside the truck: Choosing Slash as your company card solution

Fleet fuel cards are designed to optimize fuel costs, but they can be limiting when your business expenses extend beyond the pump. Many transportation and service businesses also spend heavily on tools, subscriptions, and day-to-day operating costs that fall outside of fuel networks. A general-purpose card like the Slash Visa Platinum card can allow you to capture value across all of that spend, with up to 2% cashback on purchases, while still maintaining control through customizable spending limits and real-time tracking.

Another consideration is how your payment tools fit into your broader financial stack. Fleet cards often operate as standalone systems focused only on fuel and vehicle expenses. In contrast, platforms like Slash combine corporate cards with integrated banking, expense management, and accounting integrations. This allows businesses to manage cash flow, track spending, and reconcile transactions across all categories, not just fleet-related costs, within a single system.

Here are a few additional ways Slash can support both your fleet on the road and your business behind the scenes:

- Diverse payment methods: Access global ACH settlement, wire transfers to 180+ countries, and real-time payment rails like RTP and FedNow. Pro users pay no additional domestic per-transaction fees.

- High-yield treasury: Earn 3.82% Yield on your idle cash through treasury accounts backed by Morgan Stanley and BlackRock money market funds.⁶

- Accounting & ERP integrations: Sync transaction data directly with QuickBooks, Xero, or Sage Intacct for simplified reconciliation and reporting.

- Capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to bridge temporary cash flow gaps when needed.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What’s the minimum fleet size to qualify for fleet cards?

There is usually no strict minimum fleet size, and many providers offer fleet fuel cards to businesses with just one or two vehicles. However, larger fleets tend to unlock better fuel discounts, higher limits, and more advanced reporting features.

Do fleet cards work internationally?

Most fleet cards are designed for use within a specific country or fuel network, so international acceptance can be limited. Some universal fleet cards that run on Visa or Mastercard may work abroad, but fees, acceptance, and controls can vary by provider.

What's an FX Fee? Everything You Need to Know to Save on International Payments

Can you withdraw money from a fleet card?

Fleet fuel cards are not designed for cash withdrawals and typically block ATM access. They are restricted to approved purchases like fuel, maintenance, and vehicle-related expenses to maintain control and reduce fraud risk.

Prepaid Business Cards: How to Manage Employee Expenses and Maximize Control with Slash