How Do Merchant Discount Rates Work?

Every time a customer taps their card or enters their details at your storefront’s checkout, you lose a small percentage of that sale. This 1.5%-3.5% charge is known as the merchant discount rate (MDR). For many small business owners, this is a fee that’s worth absorbing in order to accept payment via cards. However, that doesn't mean it should be overlooked.

Even though a couple of percentage points may not feel like a lot, they can add up quickly for businesses whose customers routinely use credit and debit cards. According to the Merchants Payments Coalition, American businesses paid $198.25 billion in payment processing fees in 2025. If you can’t easily look through your cash flow, you may not know exactly how much your company contributes to that total.

This article breaks down what the merchant discount rate is, which fee components make it up, how it flows through a transaction, and what factors push your rate higher or lower. By the end, you'll have a better idea of what you pay to accept cards and how to evaluate those costs as your business grows. We’ll also take a look at Slash, a business banking platform that displays incoming and outgoing transactions on an integrated financial dashboard.¹ From there, you can use Slash's forecasting tools to visualize how changes to your payment processor could affect your cash flow going forward.

What Is a Merchant Discount Rate?

The merchant discount rate is the percentage of each card transaction that merchants pay to process a payment. Rather than a single charge from a single source, MDR is typically a number that covers a bunch of different fees collected by participants in the payment ecosystem.

MDRs usually apply to credit and debit card purchases processed through merchant acquirers or payment service providers. Most business owners see it as a line item on their payout statements, representing the difference between what a customer paid and what actually settled in the merchant's bank account. Across providers and pricing structures, MDR rates are typically around 2-3%, but they can vary more widely depending on a business's setup and processing agreement.

What Costs Are Included in the Merchant Discount Rate?

The MDR is made up of several distinct fee categories, each coming from a different member of the payment processing chain. You can think of it like a highway with multiple toll booths, where each party takes a small cut before the funds reach you. If you want to know where your costs are coming from and which parts you can actually influence, it’s important to know what fees build the MDR:

Interchange Fees

Interchange fees represent the largest piece of the MDR pie for many merchants. These fees are paid to the issuing bank, which is the institution that issued the card your customer used to make the purchase. When a customer pays with a card, the issuing bank essentially fronts the transaction amount to the merchant on behalf of the cardholder. Interchange is how the bank gets compensated for taking on that risk, funding its fraud prevention operations, and supporting cardholder rewards programs.

Interchange rates are established by the card networks, such as Mastercard and Visa. Because each network sets their own rates, they aren't the same across all transactions. For example, a debit purchase at a retail store often carries lower interchange rates than an online purchase made with a premium travel rewards credit card. Card type, transaction method, and risk level can all influence the final number.

Assessment or Card Network Fees

Just as card networks set their own interchange rates, they also charge separate fees to fund their global infrastructure and operations. These assessment fees are typically the smallest of the bunch, often around 0.1-0.2% of the transaction amount. Even though they don’t seem significant, they’re still a consistent cost of doing business that shouldn’t be overlooked.

Payment Processor or Acquirer Fees

The third cost is what your payment processor or acquirer charges for facilitating the transaction. These costs can cover authorization, settlement, fraud monitoring, and any reporting or support tools they provide. Unlike interchange and network fees, the processor markup is the one portion of the MDR that can sometimes be negotiated, particularly for businesses with higher transaction volumes or a strong, low-risk payment history. If you feel that your storefront provides a level of traffic that’s valuable to your payment provider, you may be able to work out a lower rate.

How the Merchant Discount Rate Works

When a customer pays by card, a few financial parties work in the background to complete the transaction. The MDR is the combined cost of coordinating all of them. Here's how the process typically works:

- A customer initiates a card payment: The customer's card details are captured at checkout, either in person via a terminal or online through a payment gateway. Afterwards, the transaction request is sent out for processing.

- The payment routes through a processor or network: The request travels from the merchant's payment setup through the acquiring bank and into the card network, which then passes it along to the issuing bank for approval.

- The issuing bank approves or declines the transaction: The customer's bank reviews the request and makes sure funds are available in the account. When that’s confirmed, it runs fraud checks and approves or declines the purchase. This all happens within a few seconds, meaning the customer doesn’t have to spend time waiting at the terminal or checkout page.

- The merchant receives payment after processing fees are deducted: Once approved, the transaction heads for settlement. By the time funds reach the merchant's account, the interchange fee, assessment fee, and processor markup have already been automatically deducted. The merchant receives the net amount after all parties have taken their share.

Factors That Affect the Merchant Discount Rate

Your merchant discount rate depends on how you accept payments, what your customers pay with, and how your business is classified by acquirers and networks. Here are the variables that can lead to increases or decreases in your MDR:

- Card type: Premium, rewards, or travel cards typically carry higher rates than standard consumer cards, since extra fees pay for extra features. Generally speaking, credit cards tend to come with higher interchange rates than debit cards overall.

- Transaction volume: If your business sees high processing volumes, you may have leverage to negotiate lower processor markups. Some pricing agreements also include volume-based discounts that reduce your effective rate as your business grows. It’s sort of like a “bulk discount” in the eyes of the provider.

- Industry or business category: Each business is assigned a Merchant Category Code (MCC) that tells acquirers and networks what type of business it operates. Industries associated with higher chargeback rates or fraud risk, such as travel or subscription services, may face higher MDRs than lower-risk categories like grocery or retail.

- Online vs. in-person transactions: Card-present transactions, where a card is tapped, inserted, or swiped in person, generally carry lower interchange because the fraud risk is lower. Due to the chances of hacking or PAN (Primary Account Number) enumeration attacks, card-not-present transactions within online purchases usually come with higher prices because they’re vulnerable to fraud.

- International transactions: Cross-border payments may come with additional fees, including foreign currency conversion charges, international network fees, and settlement costs that vary by country.

- Chargeback history: A high ratio of chargebacks signals risk to processors and acquirers. Businesses that commonly experience disputed transactions may be moved into higher-risk pricing tiers.

- Payment processor pricing structure: Your processor may structure its fees in specific ways, such as through flat-rate, interchange-plus, tiered, or subscription pricing. Each of these can affect the total amount you’re charged.

Some businesses also calculate what's known as an effective merchant discount rate, which divides total processing fees by total card volume to get a blended view of what they're actually paying. You might want to use this if your transaction mix includes multiple card types, since it reflects the average cost of card acceptance rather than the rate of one specific purchase.

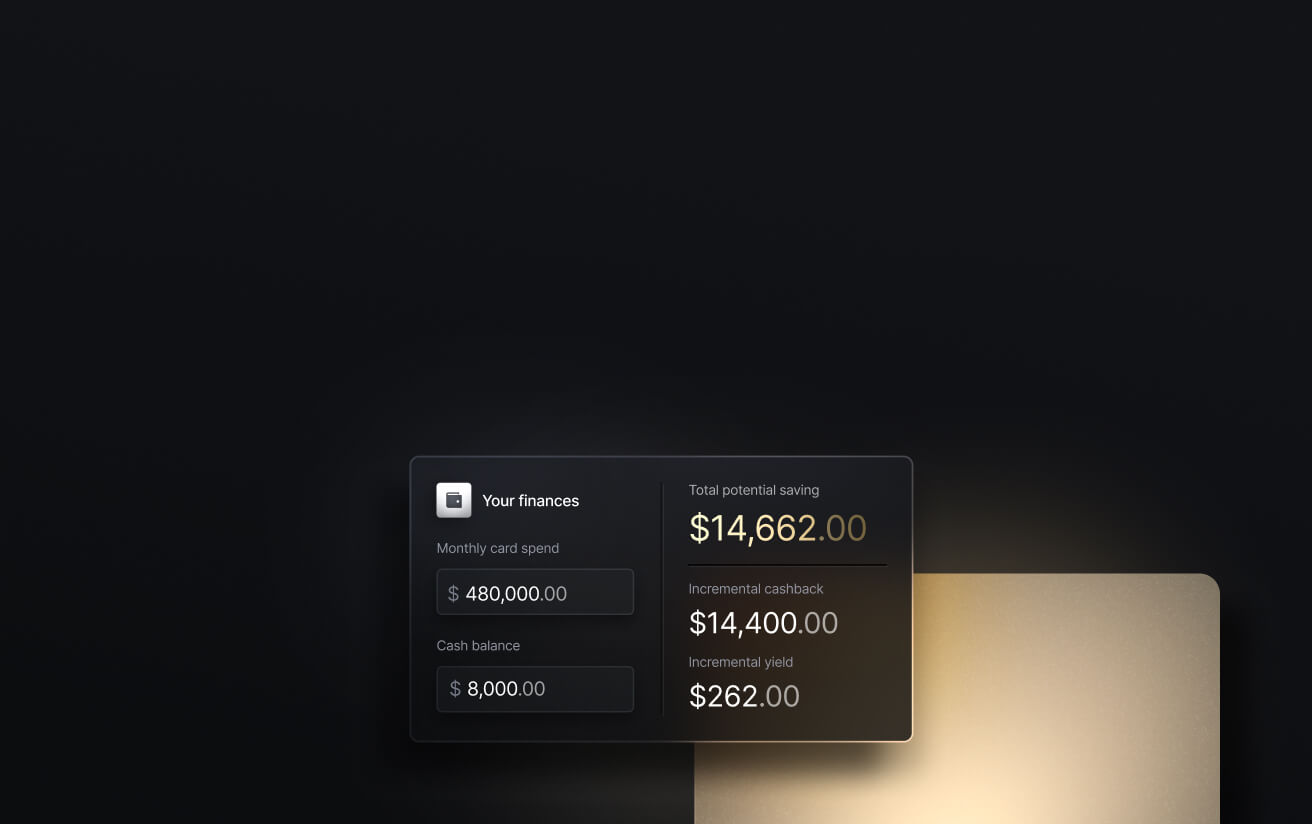

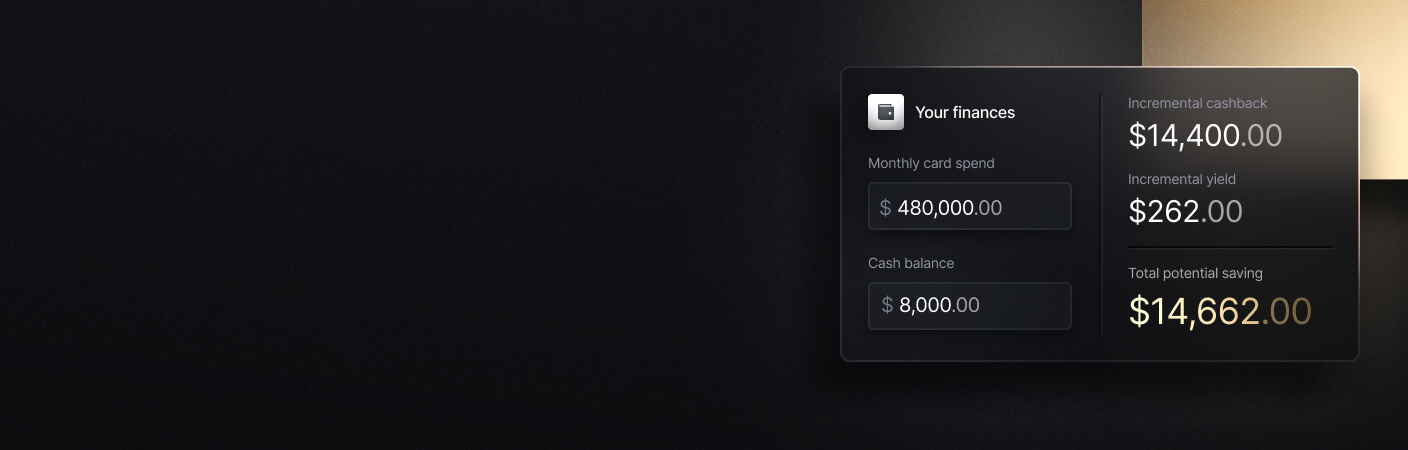

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Why the Merchant Discount Rate Matters for Businesses

Businesses shouldn’t be scared of MDRs, since they’re a necessary part of making your goods or services accessible to the average customer. Instead, they should be prepared by knowing what parts of their finances might be affected by the extra charges. Here are the areas where payment processing costs have the most impact:

Payment Processing Costs and Profitability

Small differences in MDR between providers can and will add up. If you process $500,000 in annual card volume at 2.5%, you’ll pay $12,500 in processing fees. If you instead pay 2.2%, you’ll save $1,500 per year without adjusting your pricing or offerings. This is why negotiations can matter, if your provider allows a little flexibility. An MDR discount of half a percent can be worth thousands.

Cash Flow and Settlement Visibility

MDR fees are generally deducted before funds settle into the merchant's account, though settlement timing and exact fee structures can vary depending on the processor and pricing arrangement. Being familiar with these fees and planning for them ahead of time can be important for cash flow forecasting. Using authorization data + the merchant’s pricing schedule, Slash can actually show users an estimated MDR/processing fee amount while incoming card payments are pending.

International and Cross-Border Payment Costs

Businesses operating across borders may incur higher payment than their base MDR. International transactions may involve foreign exchange (FX) spreads, currency conversion fees, and settlement-related costs that vary by country and payment method. A merchant selling to customers in other countries will often find the total cost of accepting a payment can differ depending on where the customer's card was issued.

Chargebacks and Transaction Risk

Chargebacks often carry extra costs, as many processors charge a per-dispute fee. If your business keeps experiencing chargebacks from its customers, pricing changes, reserve requirements, or account reviews can be triggered. On the other hand, businesses that consistently maintain a low chargeback rate are generally viewed as lower risk, which can positively influence their MDR. Preventing disputes before they escalate is, in a sense, its own form of processing fee management.

How Businesses Evaluate Merchant Discount Rates

When reviewing payment processing costs, it’s smart to examine both the headline rate and the structure behind it. A number that looks competitive on the surface can end up being different in reality, depending on how it's constructed and what it actually includes. Here’s what you should keep in mind:

Flat-Rate vs. Interchange-Plus Pricing

Flat-rate pricing charges a fixed percentage for every transaction, regardless of card type or network. It's predictable and simple to budget for, which can make it a good fit for businesses with lower volumes or those that value simplicity. However, since you pay the same rate for a low-cost debit transaction as for a premium credit card, you might end up overpaying if your customer base rarely uses premium cards.

Interchange-plus pricing is a format that passes through consistent fees for each transaction, then adds a clearly defined processor markup at the end. This structure offers more visibility into where costs are going and can result in lower overall fees for established or high-volume merchants. Some processors also use tiered pricing models, which categorize transactions as qualified, mid-qualified, or non-qualified based on risk and card type. While helpful in theory, merchants typically don’t know which tier a transaction will land in until the funds settle.

Contract Terms and Additional Fees

It’s wise to review the full cost structure before signing with a payment processor. If you don’t do your due diligence, you may soon run into monthly minimums, PCI compliance fees, statement fees, chargeback fees, and early termination charges. Comparing the total costs, especially when you know your customers’ usual payment trends, can give you a more accurate picture of what you'll actually pay.

International Transaction Costs

For global businesses, it's important to evaluate how a processor handles international transactions. Research which currencies are supported, how foreign exchange is priced, and what additional fees apply. A good-looking domestic MDR can balloon once international fees are layered on top, especially if a meaningful share of your volume comes from outside the country. On the flip side, a provider with a high MDR on the surface might actually have decent cross-border support.

Reporting and Payment Visibility

Clear, itemized reporting is one of the more underappreciated factors in evaluating payment processors. Being able to see fees broken out by card type, transaction method, and time period makes it easier to understand your effective MDR. Some processors come with this level of detailed reporting, which can help business owners stay ahead of their cash flow and make better financial decisions.

Simplify Payment Operations with Slash

Fully understanding your merchant discount rate can make it easier to select a more cost-effective processor and prepare for unexpected fees. However, it’s better to get real-time visibility into payment timing and charges than to simply be prepared for them. This is the kind of access that Slash provides.

Slash is a neobank that comes with a built-in financial dashboard that gives users a live view into each of their payment rails, including customer card payments. Rather than functioning as a traditional merchant account provider or payment processor, Slash is a banking platform for businesses that want to centralize their incoming and outgoing payments, global transfers, corporate card spend, invoicing, and more. Our tools can generate an estimated MDR before transactions settle, meaning you get a head start on forecasting and reconciliation. If you want to see even further into the future, you can get some help from our agentic AI assistant, Twin.

Twin is a financial assistant that can use your current data to create cash flow forecasting graphs from simple English prompts. It can also analyze your overall financial trends, manage your Slash Cards, flag suspicious payments, and much more. Additionally, each action Twin takes is automatically logged and fully auditable.

Slash comes with a wide range of other features, including:

- Accounting integrations: Sync transaction data with QuickBooks Online, Xero, NetSuite, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury: Earn up to 3.79% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

- Native stablecoin support: Send and receive USD-pegged stablecoins USDC and USDT across eight supported blockchains for faster, lower-cost global payments.⁴

- Diverse payment rails: Slash supports a wide range of payments, including card spend, global ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through FedNow and RTP.

- Reimbursements: Instead of managing reimbursements across multiple tools, teams can now submit, review, and approve reimbursements directly inside the Slash dashboard. Connect your bank account, upload your receipt, and let Slash capture the details.

If you want a deeper look into how transaction fees and MDRs affect your cash flow, get in touch with Slash today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Does the merchant discount rate apply to refunds or reversed transactions?

Even if a transaction is reversed, the payment processor retains the original MDR. Consistent chargebacks can also hurt your overall rate, so it's helpful to avoid reversed transactions when possible.

What is tiered pricing in the context of payment processing?

Tiered pricing is a system where a payment processor combines their transaction fees into a few simple rate categories. Instead of passing the exact costs to the merchant, the processor assigns every transaction to a specific "tier" and charges a flat rate for that category.

Payment Gateway vs. Payment Processor: 5 Key Differences

Do certain card networks have better merchant discount rates than others?

As we've discussed, quite a few elements go into calculating the MDR. However, there are still a couple card network-specific trends to be mindful of. American Express tends to have higher MDRs than other options, typically landing in the 2.3%-3.5% range. Meanwhile, Visa, Discover, and Mastercard are usually closer to 1.5%-2.5%. Again, every situation is different, so be sure to look into specific payment processor setups before making any decisions.

Payment Gateway Integrations: What They Are and How They Work