Interchange Fees Explained: How Credit Card Transactions Work

If you run a business that accepts card payments, you may have noticed that each card-based transaction incurs a small fee. This is called an interchange fee. Interchange fees are some of the largest components of card processing costs, yet they’re tough to get a clear picture of. The actual math is usually buried inside processor statements or aggregated into blended rates, and rarely explained in terms a business owner can act on.

Understanding interchange fees can shape which payment methods you encourage customers to use, how you negotiate with your processor, and how the revenue side of that interchange equation can work in your favor. In this guide, we’ll review how interchange fees work, what affects their rates, what they can cost your business, and strategies you can use to minimize them. We’ll also take a look at Slash, a business banking platform that unlocks greater visibility into small fees, large payments, and everything in between.¹

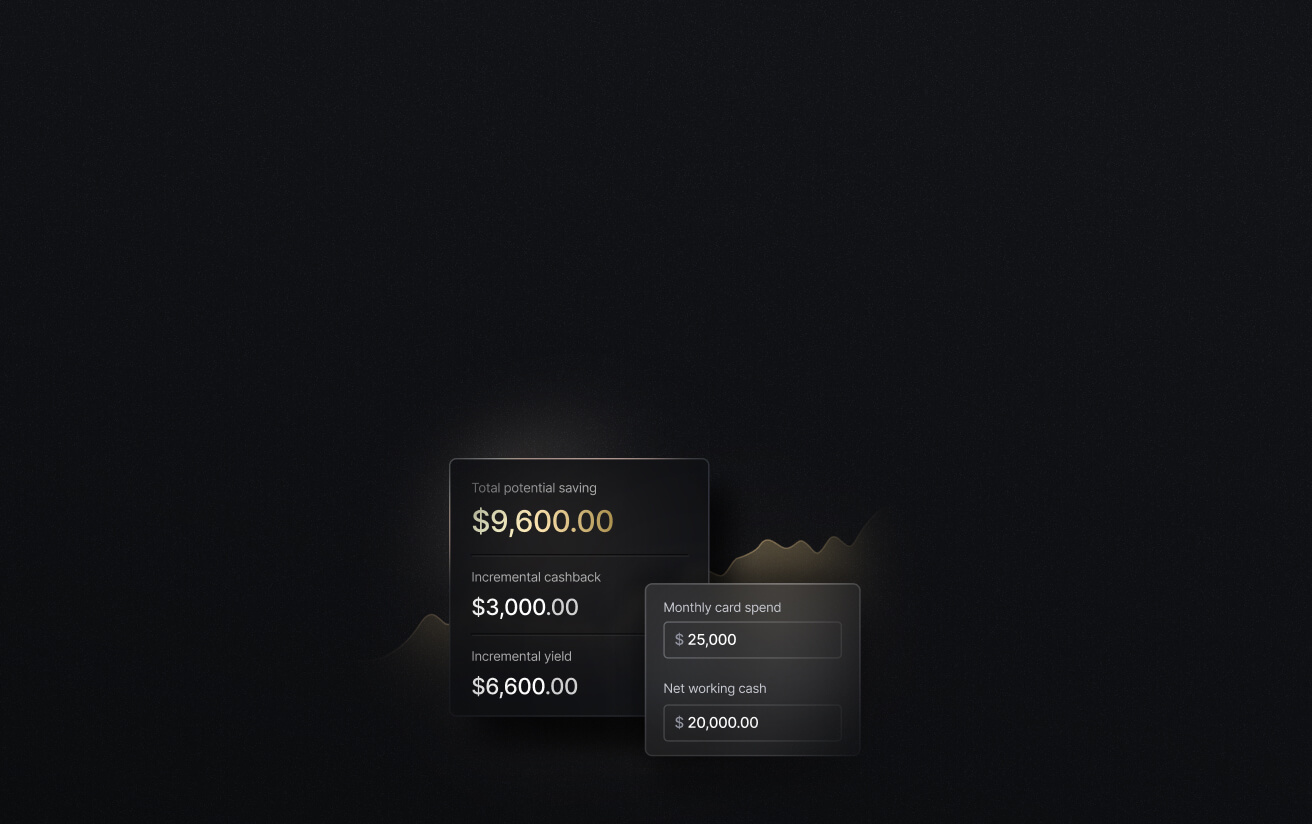

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What Are Interchange Fees?

Interchange fees are charges paid between banks every time a card transaction is processed. Specifically, when a customer pays with a credit or debit card, the merchant's bank (the acquiring bank) pays a fee to the customer's bank (the issuing bank). That fee is set by card networks like Visa and Mastercard, not by the banks themselves.

The interchange fee flows from merchant to acquirer to issuer with each transaction. For example, a retail business accepting an American Express credit card doesn't write a check to Chase Bank, but a portion of every card payment they process ends up there. These portions are deducted before the merchant ever sees the funds. Interchange typically represents 70–90% of the total processing cost a merchant pays.

The typical range runs from around 0.2% for regulated debit cards to 3.5% or higher for premium rewards credit cards. For businesses accepting cards at significant volume, this is a material operating cost, and can be the third or fourth largest line item after payroll and rent.

The Players in Every Card Transaction

To fully understand the mechanics of interchange fees, you should know who’s involved:

- Card networks:Major networks set the interchange rate schedules, maintain the payment infrastructure, and collect their own small assessment fees (typically 0.10% to 0.15% of each transaction) separate from interchange. Most networks, including Visa and Mastercard, operate as four-party networks connecting the cardholder, the merchant, the issuer, and the acquirer.

- Issuing banksare the institutions that issued the card being used for the transaction. The issuing bank receives the interchange payment and uses it to fund fraud protection, dispute resolution, and importantly, the rewards programs that make premium credit cards attractive to consumers. In the case of the Slash Visa® Platinum Card, which offers up to 2% cash back, the issuing bank is Column N.A., member FDIC.²

- Acquiring banks and processorsare the merchant's payment partners that enable a business to accept card payments. They pass interchange through to the issuing bank and charge their own margin on top. When a business sees a processing fee of 2.9% + $0.30, a portion of that 2.9% is interchange flowing to the card issuer, and the remainder is the acquirer's markup.

- Merchantssit at the end of the chain, absorbing the cost in exchange for the ability to accept cards. The convenience and sales volume that card acceptance enables typically outweighs the fees, which is why cards are near-universally accepted.

How Interchange Rates Are Set

Card networks publish hundreds of interchange categories, typically updated twice a year. The rate that applies to any given transaction depends on a matrix of factors including card type, transaction method, merchant category, and whether the transaction data submitted meets the network's qualification criteria.

The underlying logic is risk-based pricing. Transactions where the card is physically present and the chip is read carry lower fraud risk and lower interchange. On the other hand, online purchases where a card number is manually typed in often carry higher fraud risk and higher interchange. Premium rewards cards can shift cost from the cardholder to the merchant, funding rewards programs with interchange revenue rather than annual fees.

Geography also plays a role. US interchange rates are among the highest in the developed world. The European Union capped consumer card interchange at 0.2% for debit and 0.3% for credit under the Interchange Fee Regulation, making European rates a fraction of their American equivalents. Australia, Canada, and the UK have similarly imposed caps through regulation or industry agreements. In the US, the Durbin Amendment to the Dodd-Frank Act capped debit interchange for large banks at roughly 0.05% + $0.22 per transaction. However, this cap only applies to issuers with $10 billion or more in assets, leaving smaller bank-issued debit cards on standard (higher) rate schedules.

Key Factors That Influence Your Interchange Rate

- Card typeis the single biggest variable. A consumer debit card usually carries lower interchange than a premium travel rewards credit card.

- Transaction methoddistinguishes card-present from card-not-present transactions. Swiped and chip-read transactions have lower interchange than keyed or online transactions because physical card presence reduces fraud risk.

- Merchant category code (MCC)classifies the type of business. Networks assign MCCs to merchants based on their industry, and interchange schedules usually include category-specific rates. Supermarkets, for example, operate on some of the lowest interchange categories due to their volume and thin margins. Utility companies, airlines, and government entities also receive preferential rates.

- Processing volume and business sizeaffect interchange indirectly, through the processor relationship and account type rather than through the published rate schedule. Large merchants can sometimes negotiate custom interchange arrangements with card networks, though this is generally reserved for businesses processing hundreds of millions annually.

- PCI DSS (Payment Card Industry Data Security Standard) complianceaffects whether a business qualifies for the best available rates within its tier. Non-compliant merchants may be subject to higher rates or additional fees charged by their acquirer.

Why Credit, Debit, and Corporate Cards Have Different Rates

The type of cards you accept is typically the biggest deciding factor for the interchange fees you’ll encounter. This is why and how they vary:

- Consumer credit cardstypically carry fees in the 1.8% to 2.5% range, possibly rising to 2.5%–3.5% for premium rewards cards. The higher rates on rewards cards directly fund the points, miles, and cashback that cardholders earn. Merchants effectively end up subsidizing a customer's reward points when they use a premium card.

- Debit cardscarry significantly lower interchange: 0.2% to 1.0%, depending on whether the issuer is subject to the Durbin Amendment cap. For merchants accepting high volumes of everyday purchases, steering customers toward debit payment methods can meaningfully reduce processing costs. The trade-off is that many customers, particularly higher-spending ones, prefer to pay with rewards credit cards.

- Corporate and commercial cardsoccupy the highest interchange tier, typically running 2.5% to 4.0% and sometimes higher for specific card types. The higher rates reflect the enhanced data and controls these cards carry, including itemized line-item data, integration with expense management systems, and vendor-level controls. Corporate cards can also carry rewards or rebate structures that are funded, in part, through this elevated interchange.

- Prepaid cardsvary depending on structure. Network-branded prepaid cards typically fall under interchange schedules similar to debit, while the specific rate depends on whether the card is subject to Durbin Amendment treatment.

Real-World Rate Examples by Card Type

To make this concrete, consider a $500 transaction processed through a mid-sized US retailer:

- Consumer Visa debit (large issuer, Durbin-regulated):~$0.22 + 0.05% = approximately $0.47

- Consumer Visa credit (standard rewards):~2.1% = approximately $10.50

- Premium Visa Signature travel card:~2.7% = approximately $13.50

- Corporate Visa card:~2.9% = approximately $14.50

The difference between a customer paying with a regulated debit card and one paying with a premium corporate card is over $14 on a single $500 transaction. For a business processing $500,000 in annual card revenue, the difference between a customer base that skews toward regulated debit versus one that skews toward premium rewards cards could represent $30,000 to $70,000 in annual interchange cost. It’s smart for retailers and e-commerce companies to understand how their intended customer base spends their money.

Where Interchange Money Actually Goes

About 80-90% of the total interchange revenue collected flows to the card issuer. This income funds several functions that issuers have structured their business models around.

The largest single use is rewards program financing. With cash back, points, and travel perks, premium credit card rewards are expensive to fund. A card offering 2% cash back on all purchases needs at least 2% in revenue per transaction to break even on the reward alone, before fraud costs, operational expenses, or profit. High interchange rates on premium cards exist largely to make the economics of generous reward programs viable.

Fraud protection and dispute resolution represent another significant cost. Card issuers bear the liability for fraudulent transactions in most scenarios, while the merchant bears liability when a chip card is swiped rather than chipped. Interchange funds the fraud operations, dispute teams, and technology that manage this liability. Card networks can also collect assessment fees in the form of 0.1-0.15% charges that fund the payment infrastructure itself.

Business Impact: What Interchange Fees Cost You

For a business processing $1 million in annual card revenue with a blended interchange rate of 2.0%, the annual interchange cost is approximately $20,000. At $5 million in revenue, that's $100,000, even without the processor’s markup. These are real operating costs that belong in financial planning, not just on a payment processor statement that gets reviewed once a year.

The impact varies meaningfully by business type. Retail businesses with thin margins feel interchange acutely; a grocery store operating at 2% net margin and paying 2% interchange is effectively breaking even on every card transaction, with all profit coming from the narrow spread between total margin and processing cost. Professional services firms with higher transaction sizes and stronger margins experience interchange as a smaller percentage of profit, but the absolute dollar cost per transaction is still significant.

E-commerce businesses face card-not-present rate premiums on every transaction, adding 0.3% to 0.5% to their effective rate compared to an equivalent brick-and-mortar transaction. B2B companies face the highest exposure, because their customers and vendors often pay large amounts with high-fee corporate cards. The absolute dollar cost per transaction is often substantial.

Settlement timing is a related consideration. When a merchant processes a card transaction, the funds don't arrive instantaneously, as typical settlement takes one to two business days over networks like Visa and Mastercard. For businesses with tight cash flow, that float has real cost.

Strategies to Minimize Interchange Costs

While interchange fees are largely out of your hands as a merchant, there are some strategies you can utilize to minimize costs:

- Encourage lower-cost payment methods:ACH and bank transfers carry no interchange, and debit cards carry far lower interchange than credit cards. While they can’t control their customers, businesses that can nudge payment behavior can reduce their interchange burden. The right move isn’t to ban credit cards, though: it’s smarter to make other payment methods more frictionless.

- Optimize transaction data for better qualification:Interchange is partly determined by the quality of data submitted with each transaction. Submitting required fields completely, including AVS data, CVV, and enhanced Level 2 or Level 3 data for B2B transactions, can qualify a transaction for a lower interchange tier. Many businesses unknowingly pay higher interchange because their checkout flows don't capture or submit all the data the network expects.

- Surcharging and cash discount programs:US merchants are legally permitted to add a surcharge for credit card payments, subject to card network rules and state laws. Cash discount programs, which offer a reduction for non-card payment, achieve a similar effect.

- Negotiate with your processor:Interchange itself is fixed by card networks and non-negotiable. However, the processor's markup actually is. Businesses processing significant volume can negotiate their effective rate down, often by moving from blended pricing (a single flat rate covering interchange plus markup) to interchange-plus pricing (interchange passed through at cost, with a separate transparent markup). The latter makes actual costs visible and eliminates the processor's margin from fluctuating with card mix.

- Use corporate cards strategically:While corporate card interchange is high from the merchant side, the same interchange dynamics that cost you money when customers pay you with corporate cards generate cashback and rewards when you pay vendors with your own corporate card. A platform like Slash offers up to 2% cash back on corporate card spend, meaning the interchange economics that represent a cost on the acceptance side can work in your favor on the spending side.

How Slash Can Enhance Both Your Financial Visibility and Your Rewards

Understanding interchange doesn't change the rate you pay today, but it changes the decisions you can make tomorrow. Knowing which payment methods to encourage, how to structure your processor relationship, and how to build payment costs into your financial model can help you manage and reduce these fees. With Slash, business owners can gain deeper visibility into these fees and into each payment that comes and goes from their company accounts.

Slash is a neobank that offers businesses a high cash back corporate charge card and an integrated dashboard that brings their finances together. Our users can prompt our AI agent, Twin, to break down their cash flow and fees in written detail and through custom charts. Slash can unlock financial information that never would have been accessible through a traditional banking platform.

You may end up finding that you’re losing capital to high interchange fees from corporate cards. By spending money with the Slash Visa® Platinum Card, you can earn that money right back with cash back rates of up to 2%. Additionally, the Slash Card comes with unlimited virtual cards and automated fraud detection, meaning you can extend spending to your whole team without having to worry about security.

Here are some other Slash features that can help merchants:

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury:Earn up to 3.83% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

- Accounting & ERP integrations:Sync transaction data with QuickBooks Online, Xero, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Native cryptocurrency support:Hold, send, and receive USD-pegged stablecoins USDC and USDT across eight supported blockchains for faster, lower-cost global payments.⁴

- Diverse payment methods:Slash supports a wide range of payments, including card spend, global ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

If you’re a merchant looking to gain deeper visibility into the interchange fees you pay every day, try the Slash business banking platform.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Who actually pays interchange fees?

Merchants and business owners pay interchange fees on almost every credit card transaction they accept. While the merchant's bank (acquirer) initially pays these fees to the customer’s bank (issuer), this cost is almost always passed directly to the merchant.

Can I avoid interchange fees on credit cards entirely?

Through surcharges, you can end up with a net zero on interchange fees, but you can’t eliminate their existence.

Managing Corporate Credit Cards: Automation, Expense Tracking & Slash Tools

Are interchange fees the same as processing fees?

No, interchange fees are only one element of processing fees, which also include card network assessment fees and processor markups.

Ecommerce Payment Processing Explained: Methods, Gateways & Best Practices

Read more from us