Payment Service Providers: How to Manage Payments and Choose the Right Solution

Accepting payments used to mean setting up a merchant account, connecting a payment terminal, and waiting for deposits. That picture has changed considerably. Today, businesses deal with multiple payment methods, including cards, digital wallets, bank transfers, and even cryptocurrency. Customers are global, payment expectations are high, and the systems required to manage it all have multiplied alongside the options.

The result is that businesses no longer just “accept payments.” They route transactions through different methods and geographies, reconcile across systems, manage payouts, and maintain compliance with regulations that vary by market. The infrastructure that makes this possible is built, in large part, around payment service providers.

This guide explains what PSPs are, how they process transactions, the different provider models available, what to look for in terms of features and limitations, and how to choose the right solution based on where your business actually operates. We’ll also take a look at Slash, a business banking platform that allows merchants to offer extra payment rails and gives them deeper insight into their live cash flow.¹

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What Is a Payment Service Provider (PSP)?

A payment service provider is a third-party company that enables businesses to accept and process electronic payments. By acting as an intermediary between the customer, the merchant, the card networks, and the banks, a PSP allows businesses to accept multiple payment methods through a single integration rather than establishing separate relationships with each bank or card network independently.

Let’s take a look at some of the common terminology you’ll hear in this space:

- A payment gateway is the secure technology layer that transmits payment data between the merchant’s platform (a website, app, or POS system) and the payment processor. It handles the data transmission side.

- A payment processor is the entity that actually executes the transaction. It communicates with card networks, issuing banks, and acquiring banks to authorize and settle payments.

- A PSP typically combines both functions, often also including a shared or aggregated merchant account. This is what makes PSPs accessible and fast to deploy; businesses can start accepting payments without establishing their own dedicated merchant account with a bank.

How Payment Service Providers Process Transactions

When a customer initiates a payment, a PSP coordinates a sequence of events that typically completes authorization in seconds, though the actual settlement often takes longer. That sequence includes the following steps:

- Customer initiates payment: The customer enters payment details at checkout or taps a card at a terminal. The data is transmitted to the PSP’s payment gateway.

- PSP encrypts and validates data: The gateway encrypts the payment data using tokenization or other security protocols, protecting sensitive card information from exposure during transmission. Basic validation checks like format, required fields, and initial fraud screening happen at this stage.

- Authorization request is sent to the issuing bank: The PSP routes the transaction through the relevant card network (Visa, Mastercard, etc.) to the customer’s issuing bank, requesting authorization to proceed.

- Payment is approved or declined: The issuing bank checks the customer’s available funds, credit limit, and fraud signals, then returns an approval or decline response through the card network back to the PSP.

- Settlement and fund transfer: For approved transactions, the PSP coordinates settlement — the actual transfer of funds from the customer’s bank to the merchant’s account. Settlement typically takes one to three business days, depending on the PSP, the payment method, and the merchant’s payout schedule.

Authorization happens in seconds, but settlement can take days. Understanding this distinction matters for cash flow planning, particularly for businesses with high transaction volumes or time-sensitive operational needs.

Common Provider Models

"Payment service provider" is a broad category. The actual providers in the market differ significantly in their architecture, pricing, target customer, and geographic reach. Here are the three most common models:

All-in-One Payment Platform Models

These providers offer a comprehensive payment stack under a single platform. This combination of functions may include payment gateways, processing, fraud tools, reporting, and developer APIs. They’re designed for businesses that want to build sophisticated payment experiences and have the technical resources to integrate deeply.

- Stripe: Stripe is the most widely used all-in-one platform for online businesses, particularly among startups, SaaS companies, and digital-first organizations. It supports over 100 payment methods, 135+ currencies, and provides a highly extensible API that developers can use to build custom payment flows. Its flat, transparent per-transaction pricing makes Stripe accessible across business sizes.

- Adyen: Adyen is geared toward larger enterprises with complex, global payment needs. It provides a single connection to card networks in multiple countries, supports omnichannel payment acceptance (online, in-store, mobile), and offers sophisticated authorization optimization tools. Adyen is the platform of choice for many large retailers and global brands.

Payment Aggregators

Payment aggregators pool multiple merchants into a shared merchant account, making onboarding fast and removing the need for a formal underwriting process. This model lowers the barrier to entry but can mean higher per-transaction fees and less flexibility as transaction volume scales.

- PayPal: PayPal is the most widely recognized aggregator globally and remains a dominant payment method for consumer purchases, particularly in markets where it has high consumer trust. It supports low-volume processing without a monthly fee and offers consumer credit options that can increase conversion for certain customer segments.

- Braintree: Braintree, a PayPal subsidiary, offers more developer-friendly infrastructure for businesses that want PayPal’s acceptance network with greater technical flexibility. It supports multi-currency payments, digital wallets, and card processing through a more customizable integration layer than PayPal’s standard checkout flow.

Cross-Border Payment Platform Models

These providers specialize in international money movement — often with better exchange rates, more transparent fee structures, and faster settlement than traditional wire transfers. They are widely used for vendor payments, contractor payouts, and marketplace disbursements across borders.

- Wise: Wise (formerly TransferWise) processes cross-border payments using local bank accounts in multiple countries, which allows it to settle many transfers without crossing international banking rails. As a result, its customers often experience faster delivery and lower fees than standard wire transfers. Wise is particularly popular for freelancer and contractor payments.

- Payoneer: Payoneer serves clients that need to pay international partners at scale, such as e-commerce, digital advertising, and gig economy businesses. It offers local payment methods, multi-currency holding accounts, and payout capabilities to recipients in a wide range of countries, making it a frequent choice for marketplace and affiliate payment flows.

For teams that use multiple providers across these models, complementary platforms like Slash help manage and track international payment flows across accounts. Slash offers diverse payment rails such as global ACH, RTP/FedNow, and stablecoins, giving merchants an extra level of flexibility. Our real-time dashboard also provides visibility that individual PSPs typically don’t offer on their own.

What Are the Benefits of Using a Payment Service Provider?

The case for using a PSP is primarily operational. Here’s what businesses gain in practice:

Simplifies Payment Infrastructure Without Adding Operational Overhead

A single PSP integration replaces the need to build and maintain separate connections to card networks, banks, and alternative payment methods. For most growing businesses, this means shipping a payment flow in days rather than months. It also means a dedicated payments engineering team doesn’t necessarily need to be brought on board.

Enables Global Payment Acceptance

Expanding to new markets requires supporting local payment methods, such as SEPA in Europe, PIX in Brazil, UPI in India, and Alipay in China. PSPs with strong global coverage maintain these integrations on behalf of their merchants, allowing businesses to serve customers in new geographies without building each integration individually.

Accelerates Time to Market by Reducing Integration Complexity

PSPs provide pre-built checkout components, hosted payment pages, and well-documented APIs that allow development teams to integrate payment acceptance quickly. For businesses launching new products or entering new markets, this speed is a meaningful competitive advantage.

Increases Conversion Rates Through a Better Checkout Experience

Checkout abandonment is one of the most significant sources of lost revenue in e-commerce. PSPs that support saved payment methods, one-click checkout, and locally preferred payment options reduce the friction that causes customers to drop out at the final step. Better payment experiences translate directly to higher completion rates.

Reduces Compliance Exposure Through Built-in Security

Payment data handling requires compliance with PCI DSS (Payment Card Industry Data Security Standard), and in some markets, with additional regional regulations. PSPs maintain this compliance on behalf of their merchants, reducing the scope of what a business needs to certify and manage independently.

Speeds Up Reconciliation with Centralized Transaction Reporting

When all payment activity flows through a single provider, transaction data is organized in one place and managed with consistent formats, timestamps, and status information. This makes reconciliation faster and more reliable than trying to consolidate data from multiple disconnected payment systems.

What Are the Key Features That Payment Service Providers Should Have?

Not all PSPs offer the same capabilities. When evaluating options, these are the features that matter most:

- Multi-payment method support: The PSP should support the full range of methods relevant to your customers. These may include credit and debit cards, digital wallets (Apple Pay, Google Pay), ACH and bank transfers, buy now pay later, and regional alternatives. A narrow payment method library limits the markets you can serve.

- Security and compliance infrastructure: PCI DSS compliance is a baseline requirement. Beyond that, look for tokenization, 3D Secure support, and real-time fraud detection that uses machine learning to identify suspicious transaction patterns before they become chargebacks.

- Reporting and transaction visibility: Finance teams need access to real-time transaction data, settlement status, and dispute information. A PSP with strong reporting capabilities reduces the manual work required to maintain accurate financial records.

- Global payment capabilities: For businesses with international customers or vendors, the PSP should support multi-currency acceptance and settlement, local payment methods, and geographic coverage that matches the markets you operate in.

- Integration with platforms and APIs: The PSP should connect cleanly to your existing e-commerce platform, ERP, accounting software, and any other systems that consume payment data. Developer-quality APIs and pre-built integrations significantly reduce integration and maintenance overhead.

- Settlement and payout management: Beyond accepting payments, businesses need to disburse funds to vendors, partners, and contractors. A PSP with strong payout capabilities, including support for international payouts, can serve both the inbound and outbound sides of the payment operation.

Challenges and Limitations of PSPs

PSPs solve significant problems, but they also introduce constraints that businesses should account for before committing.

- Fees and pricing complexity: PSPs typically charge a percentage of each transaction plus a fixed per-transaction fee. As transaction volume grows, these costs compound. Many PSPs also charge additional fees for currency conversion, disputes, and payouts. The advertised rate rarely reflects the total cost of processing at scale.

- Dependence on third-party infrastructure: When a PSP experiences an outage or makes a platform change, merchants absorb the impact. Businesses with high transaction volumes or mission-critical payment flows carry real risk in being dependent on a single provider’s uptime and policy decisions.

- Limited control compared to direct merchant accounts: PSPs aggregate many merchants under shared infrastructure, which means they apply uniform risk policies that may not reflect an individual merchant’s actual risk profile. Account holds, fund delays, or sudden terminations are more common with aggregator-model PSPs than with dedicated merchant accounts.

- Reconciliation across systems: When PSP transaction data doesn’t flow automatically into accounting software, reconciliation becomes a manual process. Businesses using multiple PSPs for different payment types face an even more fragmented picture, since each provider reports in its own format and on its own timeline.

- Settlement delays: Standard settlement windows of one to three business days are the norm, but some PSPs impose longer holds for new merchants or high-risk transaction types. For businesses with tight cash flow cycles, settlement timing needs to be confirmed before selecting a provider.

How Businesses Use Payment Service Providers in Practice

PSPs are a foundational layer in the payment stack, but how they’re used varies considerably by business model and operational structure. Here are some ways they’re commonly utilized:

Accept Payments from Multiple Channels

Businesses with both an online and physical presence use PSPs to consolidate payment acceptance across channels (e-commerce checkout, mobile app, and in-store terminal) into a single reporting environment. This reduces the operational complexity of managing separate processors for each channel.

Route Payments Across Methods and Regions

More sophisticated payment setups use PSP routing logic to direct transactions through the most efficient or cost-effective path depending on the payment method, geography, or transaction size. Businesses operating in multiple countries may route through different acquiring banks by region to optimize authorization rates and reduce cross-border fees.

Track Transactions and Reconcile Payments

Finance teams use PSP reporting dashboards and data exports to reconcile payment activity against bank statements and accounting records. PSPs that provide detailed, structured transaction data — with references, timestamps, and fee breakdowns — significantly reduce the time required to close the books each period.

Manage Payouts and Cash Flow

Beyond accepting payments, many businesses use PSP infrastructure to disburse funds to vendors, contractors, affiliates, and marketplace sellers. Payout capabilities vary significantly by provider, and businesses with complex or international disbursement needs often require multiple tools to cover the full scope of their payment obligations.

Integrate Payments with Accounting Systems

The most operationally efficient setups connect PSP transaction data directly to accounting software, so that sales, fees, refunds, and chargebacks flow into financial records automatically. This removes the manual export-and-import cycle that slows down reconciliation and introduces transcription errors.

At the end of the day, PSPs are only one layer in the payment stack. Most businesses also rely on additional infrastructure, such as banking platforms, spend management tools, and financial dashboards, to maintain full visibility across all payment activity.

How to Choose the Right Payment Service Provider

The right choice depends on a combination of business model, geography, volume, and operational complexity. These criteria help frame the decision:

- Payment methods and fees required: Start by identifying the specific payment methods your customers use and the geographic markets you serve. Then map those requirements against what each PSP supports and what it charges for each. Compare the total cost of processing, including per-transaction fees, currency conversion margins, dispute fees, and payout costs. The difference between headline rates and effective rates at volume can be significant.

- Geographic reach: Confirm that the PSP supports payment acceptance in the countries where your customers are located, not just the countries where you’re headquartered. Local payment method coverage, local currency settlement, and in-country acquiring all affect authorization rates and customer experience in international markets.

- Transaction volume: PSPs optimized for low-volume merchants often have pricing structures that become expensive at scale. Conversely, enterprise-tier PSPs may have minimum volume requirements or contract structures that aren’t appropriate for early-stage businesses. Match the provider to where you are now and where you expect to be in 12 to 18 months.

- Integration needs: Evaluate how the PSP connects to your existing e-commerce platform, ERP, accounting software, and any other systems that process or record payment data. Poor integration creates manual work, while strong integration reduces it.

- Pricing model: Flat-rate, interchange-plus, and tiered pricing models each behave differently across transaction types and volumes. For high-volume businesses, interchange-plus pricing typically offers better economics. For lower-volume or early-stage businesses, flat-rate pricing provides predictability.

- Reporting and visibility: Look for a PSP that offers real-time transaction dashboards, exportable data in standard formats, and settlement reporting that maps cleanly to your accounting workflow. Chargeback and dispute management tools should also be evaluated; how disputes are handled and how quickly funds are withheld or returned materially affects cash flow.

- Fraud and chargeback protection: Understand what fraud detection tools are included versus available as paid add-ons, and what the PSP’s policy is for disputes. High chargeback rates can lead to account holds or termination with some providers, so confirming how the PSP manages dispute escalations is important for businesses in higher-risk verticals.

- Payout and cash flow details: Ask specifically about settlement timing, minimum payout thresholds, currency conversion timing, and whether funds are held during onboarding or for new transaction types. These details affect actual cash availability in ways that aren’t always visible in marketing materials.

Manage Payments Beyond PSPs with Slash

Choosing a payment service provider is ultimately about more than enabling transactions. It’s about how well the provider fits into your broader financial operations, and whether the combination of tools you’re using gives you a clear, current view of what’s moving, where, and at what cost. At first, you may have been asking yourself, “How many payments can we accept?”. As you scale, however, this question may turn into, “Can we see all of our payments, manage our cash, and keep our books clean without constant manual intervention?”. This is a question that Slash can answer.

Slash is a business banking platform that gives companies a place to receive and manage global payments alongside the rest of their financial activity. Our platform supports international wire transfers, crypto⁴, card payments, global ACH, RTP/FedNow, and more on a single dashboard. For teams that use multiple PSPs or manage international payment flows across accounts, Slash provides the operational layer that ties it all together.

No matter the payment rails your customers use, all transactions are visible in real time on our platform as they process. This not only enables a deeper level of transparency into your current balances, but it also gives businesses the ability to analyze their cash flow more accurately. With our built-in AI agent, Twin, users can create detailed forecasts of their future liquidity and profits with a simple prompt.

Other helpful Slash features include:

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. Users can also earn up to 2% cash back on business purchases.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury: Earn up to 3.82% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

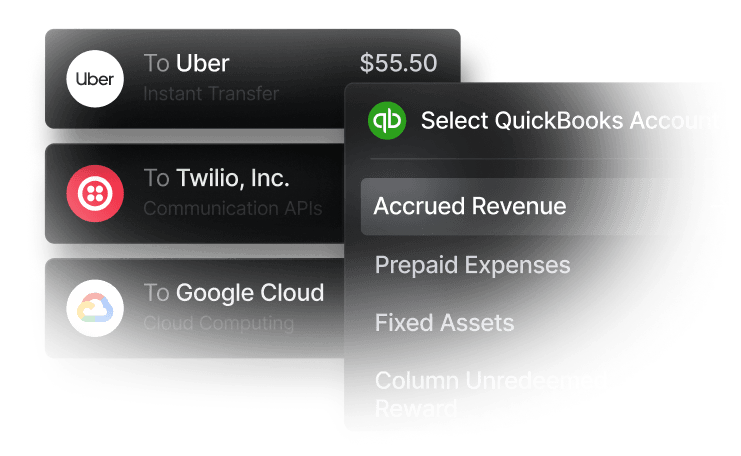

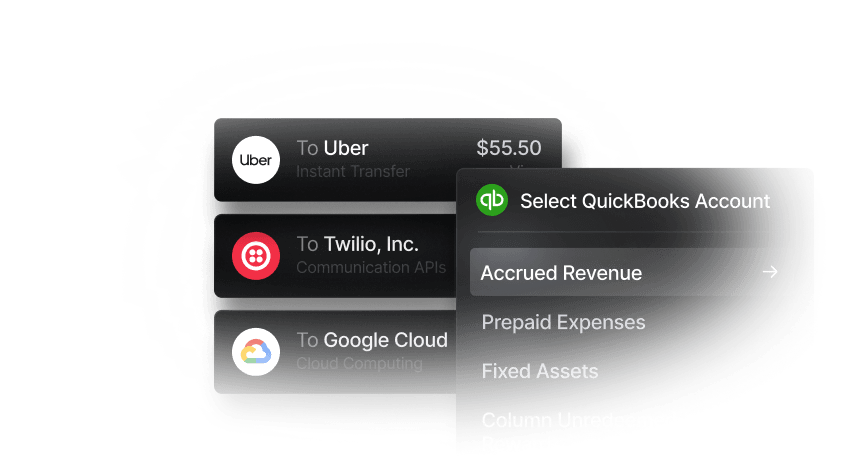

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Native cryptocurrency support: Hold, send, and receive USD-pegged stablecoins USDC and USDT across eight supported blockchains for faster, lower-cost global payments.

Pairing Slash with your PSP can both allow your customers to use a wider range of payment rails and give you a deeper look into your cash flow. Check out Slash today to see how we can help.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

What's the difference between ISOs and VARs?

The primary difference between ISOs (Independent Sales Organizations) and VARs (Value-Added Resellers) lies in their core focus: ISOs focus on selling and managing merchant accounts, while VARs focus on customizing and integrating software solutions.

How can cross-border and currency conversion costs impact online payments?

Foreign exchange risk is the financial danger that fluctuating currency exchange rates will cause a loss on international transactions or online payments. It occurs when a company or individual operates in multiple currencies, facing potential losses due to unfavorable shifts between a foreign currency and their domestic currency.

Mastering Cross-Border Fees: Essential Insights and Strategies for Reducing International Payment Fees

Cross-Border Payments: Everything You Need to Know

Do payment service providers come with fraud protection tools?

Yes, payment service providers (PSPs) typically offer robust fraud protection tools. They use AI, machine learning, and real-time transaction monitoring to detect, flag, and block suspicious activity. Common features include risk scoring, address verification (AVS), device fingerprinting, and compliance with industry standards like PCI DSS.

Business Fraud Prevention: A Guide for Protecting Your Company

Is payment processing any different between debit cards and credit cards?

Yes, payment processing can differ significantly between debit and credit cards regarding funding source, speed of settlement, and costs. Debit cards pull funds immediately from a bank account, while credit cards use a line of credit. For merchants, debit cards generally have lower fees, and for consumers, debit cards offer no interest charges, whereas credit cards offer better fraud protection.

How do you use crypto to make online payments?

In order to make online payments with stablecoins, users transfer their digital assets pegged to fiat currencies (like USDC or USDT) from a personal digital wallet to a merchant account, usually facilitated by payment processors like Stripe or Coinbase. It works via blockchain networks for fast, low-cost transactions, often bypassing traditional banking fees and delays.

Crypto Payment Processors: Compare Top Platforms for Businesses