Understanding Expense Accounts: Helpful Tips for Better Management

A first-time founder building a startup might be able to pull off tracking all of their purchases through one simple business account. However, all it takes is the hiring of a few employees for company expenses to get away from you. As departments form and operations start branching out, business owners should figure out better ways to record what their business spends on a daily basis and how it affects their overall liquidity.

One solution to this challenge is the use of expense accounts, which are categories within your accounting system that record the expenditures your business makes during a certain period. Growing businesses that work without expense accounts may struggle with inaccurate financial analysis, broken budgets, and even tax penalties from reporting mistakes.

All that said, there’s a difference between simply adopting expense accounts and using them to their full potential. We put this guide together to cover what expense accounts are, where they may fit in your accounting structure, how to track them effectively, and best practices for managing them well. Along the way, we’ll explore Slash, a business banking platform that can help track your spending in tandem with expense accounts.¹Slash integrates two-ways with QuickBooks Online, Sage Intacct, NetSuite, and Xero, meaning data from your banking solution can zip to your accounting system without any manual copying and pasting.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What is an Expense Account?

Simply put, an expense account is a record of costs your business incurs during a given accounting period. Rather than rolling every cost together into a single ledger entry, expense accounts organize spending into categories like payroll, rent, marketing, or travel. This separation can make it a lot easier to understand where your money’s going, compare spending across periods, and detect areas that need attention.

In double-entry accounting, expense accounts are one of five main account types, alongside income accounts, asset accounts, liability accounts, and capital accounts. Just as in any account, a debit increases the balance in an expense account, and a credit decreases it. For example, when your business pays a software subscription, you’ll debit the technology expense account and credit your cash or liability account. Your debits and credits have to be equal for your books to stay balanced.

Unlike examples like asset and liability accounts, expense accounts are actually classified as “temporary”. This doesn’t mean you throw them out after you’re done; instead, they get zeroed out at the end of a period, with the balance closing to retained earnings. This draws a clean line between periods and allows you to compare your spending from one month to the next. At the beginning of the following month, when the first credit or debit hits, your expense account is back in action.

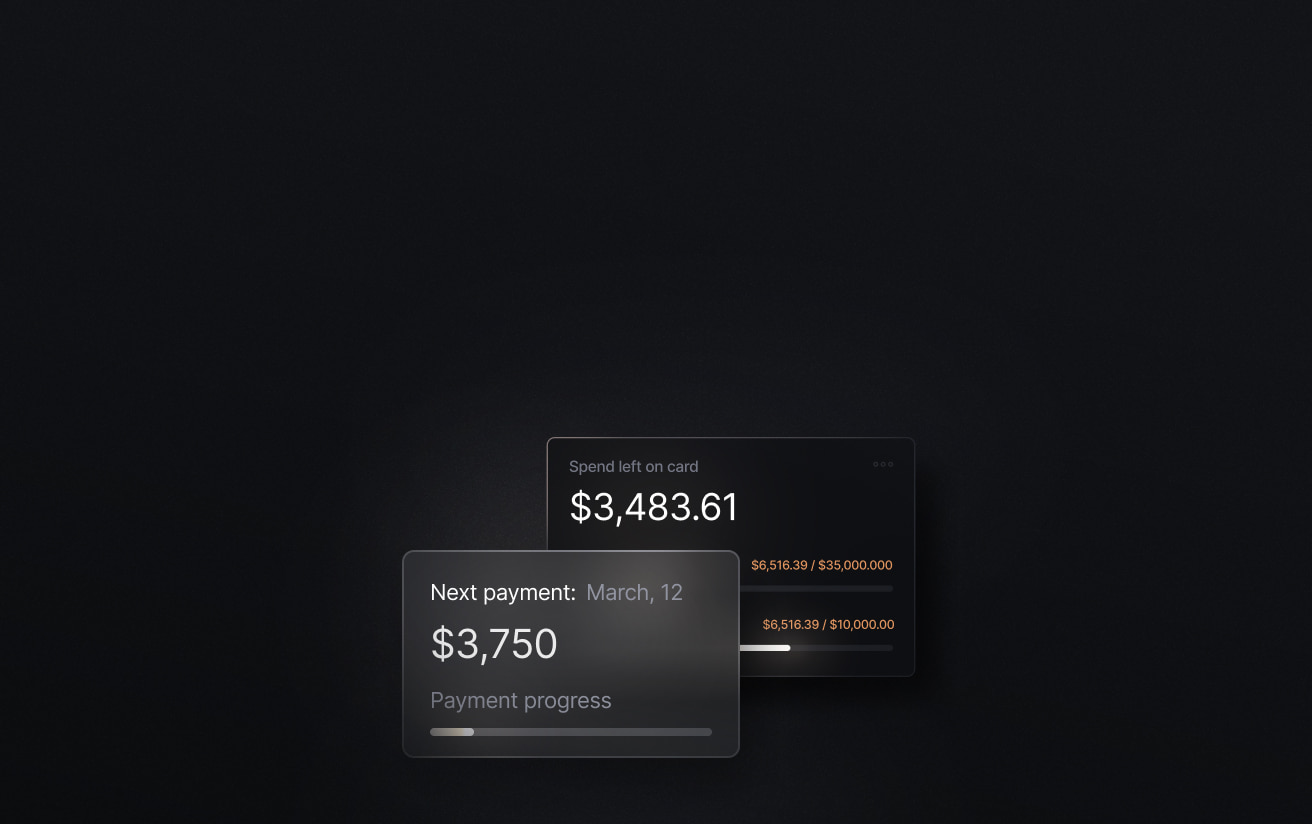

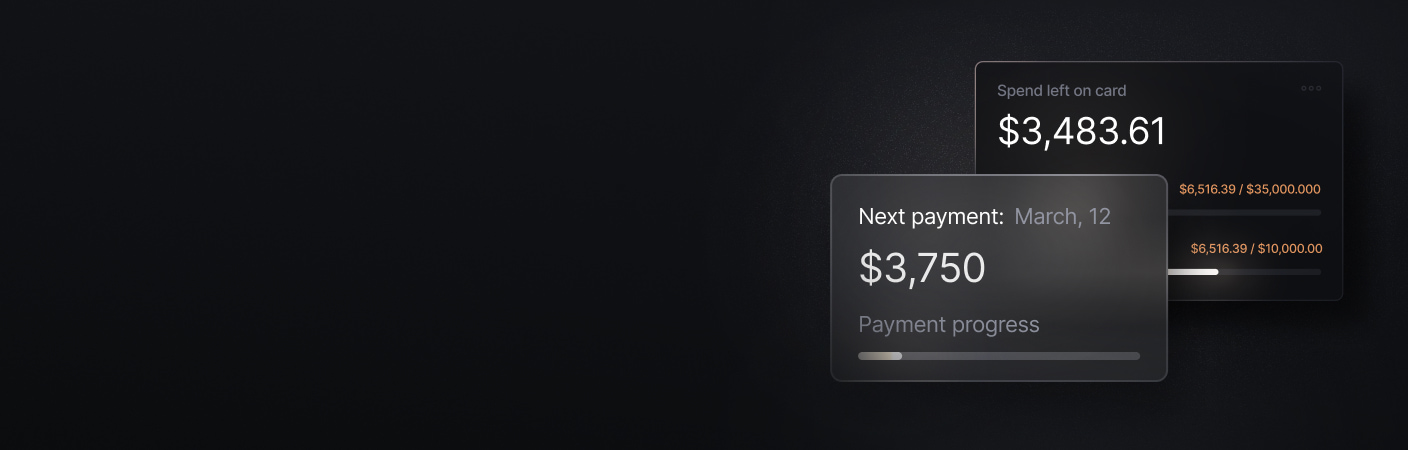

Expense accounts can also play an important role in budgeting and forecasting. By organizing historical spending into consistent categories, you can often see what you’re spending too much on and what you could afford to devote a little more cash to. Similarly, purchases made with the Slash Visa® Platinum Card are automatically categorized at the moment of purchase, saving finance teams time they might spend interpreting charges on a bank statement or re-keying items into expense reporting software.

Examples of expense accounts

A good expense account setup is going to include more than just a couple categories. Depending on your industry and headcount, your list of expense accounts may look similar to this:

- Payroll and employee-related expenses: salaries, benefits, payroll taxes, and contractor payments

- Rent and occupancy: office or retail space, storage facilities, and parking

- Utilities: electricity, water, internet, and phone service

- Cost of goods sold (COGS): raw materials, freight, and packaging for businesses that sell physical products

- Marketing and advertising: digital campaigns, content production, PR, and trade show costs

- Travel and entertainment: flights, hotels, client meals, and ground transportation

- Technology: software subscriptions, cloud services, website hosting, and IT support

- Professional services: legal fees, accounting, consulting, and recruitment

- Office supplies and equipment: printers, hardware, and small tools

- Maintenance and repairs: equipment servicing, vehicle maintenance, and facility upkeep

- Financial expenses: bank fees, loan interest, and payment processing costs

- Research and development (R&D): testing, materials, and experimentation

- Tax expenses: income, sales, and property taxes

- Miscellaneous: one-off or hard-to-categorize costs that don't fit neatly elsewhere

The point of this kind of organization is to give every purchase a home. Therefore, the “Miscellaneous” section should only be a last-ditch move if something truly doesn’t make sense anywhere else. It’s easy to make the mistake of filling the Miscellaneous account up with gray-area expenses that could be placed in another bucket. Once reconciliation comes around, you might be kicking yourself if a large chunk of your purchases live in Miscellaneous.

Where Expense Accounts Fit in Accounting

In double-entry accounting, every transaction makes one thing go up and something else go down. When your business spends money, you’ll record a debit to the relevant expense account and a corresponding credit elsewhere, typically to cash or an accounts payable account. This creates a complete record of both what was spent and what changed as a result.

Expense accounts don't actually appear on the balance sheet directly. While balance sheets capture assets, liabilities, and equity, the expenses you make affect that equity. Higher expenses reduce your net income, which in turn shrinks retained earnings on your balance sheet.

Your profit and loss (P&L) statement, on the other hand, displays your expense accounts more clearly. The P&L organizes revenue and expenses for a given period and shows whether the business made a profit or a loss, hence the name. Here’s a look at a simple example:

The more specific you get with your expense accounts, the easier it is to spot what’s changing your income. A single "operating expenses" line isn’t going to tell you much of anything. Separate lines for payroll, marketing, software, and more can break down what’s chewing into your budget and help you plan ahead.

If you’re new to the world of finance and accounting, you might mix up a P&L statement and a cash flow statement. They may both track revenue and expenses, but a P&L measures a company’s profitability while a cash flow statement tracks its liquidity.

How to Track Expense Accounts

The point of expense accounts isn’t necessarily to see a number pop up on your P&L statement. In order to avoid alarming surprises at the end of the month, it’s best to consistently track these accounts to make sure your ducks are in a row and no unusual trends form behind the scenes. They allow you to actively compare spending against your budget and have audit-ready records when tax season arrives. The question is: how do you track them?

In the past, you might have had to look over your accountant’s shoulder on a daily basis to see how spreadsheets are coming along. Meanwhile, if an employee spent money, they’d have to collect their receipts and wait for reimbursement after submitting reports manually. That’s all in the past for a reason. According to a study from the GBTA Foundation, one in five expense reports (19%) contains errors or missing information, costing an additional $52 and 18 minutes per report to correct. Most of these mistakes are good old-fashioned human error, whether due to miscalculations or typos. These are the types of problems that expense reporting software was made to fix.

Accounting software like QuickBooks and Xero can automatically give each transaction a home in their charts of accounts (CoA) and generate reports afterwards. You might also speed up your expense reporting by adopting a corporate card program that sends data to a dedicated platform each time someone makes a purchase.

Slash not only brings these two features together in the same place, but it also links them directly to your banking. With Slash, corporate card transactions are synced with accounting solutions so your spending data can move into your expense accounts without the usual tedious transcription work. If an employee's expense needs to be reimbursed, they can capture their receipt digitally with the Slash mobile app and let OCR technology extract the data for approval.

Best Practices For Managing Expense Accounts

As helpful as expense management solutions are, they can’t run your business for you. Managing your expense accounts often requires keen oversight and timely use of tools. Here are a few tips:

Log expenses daily

If you haven’t adopted any automation software, you’ll want to log your company’s expenses each day. When it comes to manual processes, the time that passes between a purchase and its recording opens the door for mistakes and overlooked expenses. Most modern platforms can handle this step for you in order to keep records as current as possible. The same goes for your employees, even if they don’t actively work with that software. Team members who make business purchases should attach receipts and submit documentation within 24 hours of the transaction.

Use technology for efficiency

There’s a reason the global expense management software market is projected to double within the next eight years. Most of these solutions are capable of a lot more than logging expenses as they happen. Automatic categorization, corporate cards, and receipt upload are key features that platforms like Slash use to supercharge efficiency. Some pieces of software can also enforce expense policies automatically, applying merchant restrictions and catching spending violations before they get out of hand.

Reconcile regularly and audit periodically

While it’s best practice to stay on top of your expense accounts on a daily basis, monthly reconciliation is still a key part of spend management. As you match expense account activity against bank statements and card records, you’ll be able to catch issues while they're recent and easier to investigate.

At the same time, this process can give you a defensible audit trail. If the IRS ever asks about a specific period, you can trace any transaction back to its source without having to dig through statements and spreadsheets. During your monthly reconciliation period, you also may want to examine the expense categorizations you’ve set up. Growing businesses often need to add new categories or remove some as they pivot, meaning your categorizations can quickly become outdated if you don’t check on them every couple months.

Stay on Top of Your Business Expenses With Slash

Expense accounts are meant to keep your company spending clean, organized, and ready for reconciliation. A problem, however, is that these accounts themselves are typically handled by your accounting team behind the scenes. If you’re a small business owner, they can help keep your finances in check, but you might need more help if you’re looking to actively manage your expenses and enforce policies on the spot.

That’s what Slash was built for. Banking, cards, spend controls, receipt capture, and accounting sync all live on Slash’s dedicated financial dashboard. The same expense data your accountants use can help shape your decisions before end-of-month reconciliation comes around. Every purchase that’s made with the Slash Visa® Platinum Card is visible in real time and monitored for signs of fraud. If our detection tools spot a broken spend policy or any other reason to be suspicious, it can alert admins and allow them to freeze the card with the click of a button.

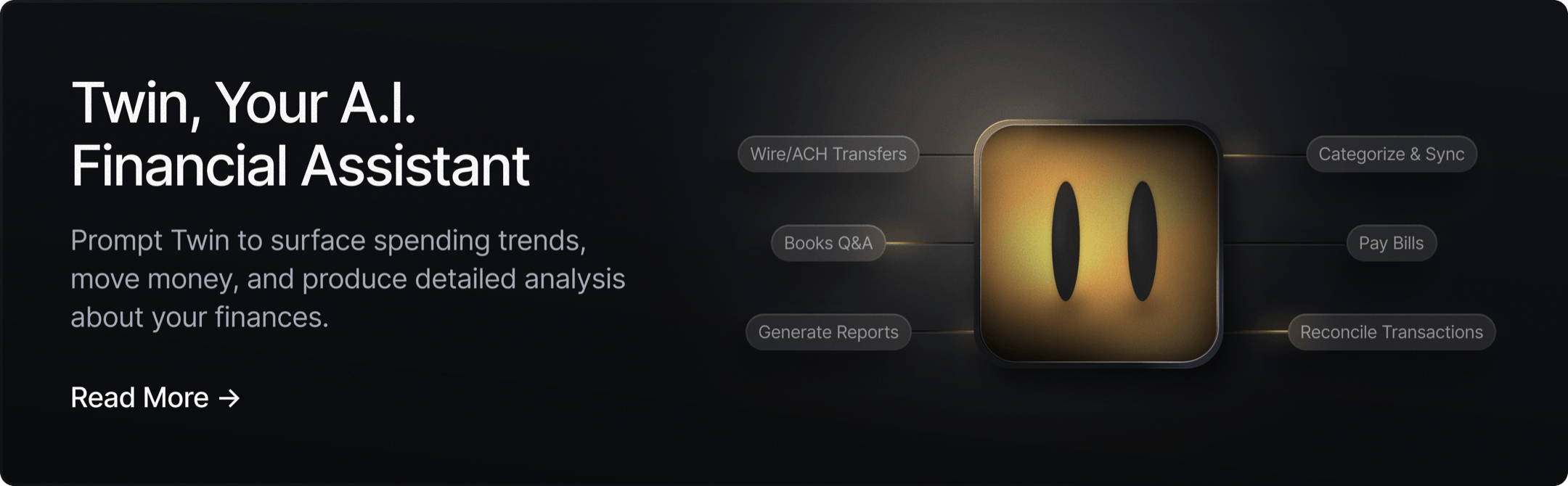

Slash users also get access to Twin, an agentic AI assistant that can be prompted in plain English to sift through your expense accounts and create graphs, draw conclusions, and diagnose issues that could take finance teams days to parse. Twin connects directly with your Slash account, meaning you can talk to it just like a regular employee. Beyond helping you with expense management, it can also execute complex tasks on your behalf, including making business purchases.

Business owners can also take advantage of the following tools:

- Invoicing features: With Slash’s invoicing and bill pay features, users can send customized invoices, collect payments, and manage vendor bills all in the same place.

- Action Center: A one-stop spot for employees to see pending tasks assigned to them. These may include card requests, expense submissions, reimbursement reviews, and more.

- Separate virtual accounts: Create multiple business bank accounts to silo cash flows by project, department, or client with real-time analytics across all accounts.

- Multi-entity support: Slash offers multi-entity account management tools without separate logins, allowing businesses to track spending, manage accounts, and download statements across all subsidiaries in one place.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

What’s the difference between an expense account and a liability account?

An expense account records costs your business has already incurred during the accounting period, such as rent paid or software subscriptions used. A liability account records obligations your business still owes, such as an unpaid vendor invoice or an outstanding loan. When a bill is received but not yet paid, it’s a liability that sits in accounts payable. Once paid, the cost moves through the expense account.

Cash Flow Management: A Guide for Making Smarter Business Decisions

Are all business expenses tax deductible?

Not automatically. The IRS allows deductions for expenses that are both ordinary and necessary, which essentially means that they’re typically for your industry and helpful for your business. Common deductible expenses include rent, utilities, payroll, and advertising. Non-deductible expenses include personal costs, fines and penalties, political contributions, and most entertainment expenses.

Can Businesses Deduct Utility Bills? Tax Rules Explained

Can Businesses Deduct Bad Debt on Their Taxes?

How often should you reconcile expense accounts?

At least once a month is ideal. Reconciling your expense accounts against bank statements and card records each month catches discrepancies while transactions are recent, makes financial statements reliable, and keeps the close process manageable. You also might want to plan periodic reviews of your expense categories to ensure your chart of accounts still reflects the things your team’s spending money on.

Bank Reconciliation Made Easy: Prevent Errors & Simplify Accounting

Where do expense accounts appear in my financial statements?

Expense accounts show up on your profit and loss (P&L) statement, where they’re listed by category to calculate operating income and net income. They don’t appear directly on your balance sheet.

Read more from us