Treasury Account vs Savings Account for Business: How Treasury Management Works

Your business may know how to spend its cash, but do you really know how to save it? That's where treasury and savings accounts come in. Both put idle cash to work, but they generate returns differently, carry different protections, and suit different stages of a business's growth.

In this guide, we'll walk through the differences between treasury and savings accounts: how each generates returns, how they differ operationally, and what to weigh when deciding where to park your business's reserves. By the end, you'll have a clear framework for splitting cash across checking, savings, and treasury accounts based on how soon you'll need access to your funds.

For SMB owners looking for an integrated treasury provider alongside the rest of their financial stack, consider Slash. Slash is a business banking platform that offers corporate charge cards earning up to 2% cashback¹, FDIC-insured checking accounts², and treasury accounts that can earn up to 3.77% annualized yield from money market funds provided by Morgan Stanley and BlackRock.⁶ With same-day to next-day liquidity and no minimum balance requirements to open a Slash treasury account, your business gets the operational flexibility of a checking account along with the high-yield potential of treasury.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What is a Treasury Account?

A treasury account is a centralized cash management account that helps a business put its excess operating cash to work in low-risk instruments like U.S. Treasury bills, notes, and short-term money market products. Instead of letting large balances sit idle in a checking account earning little or nothing, the account allocates that money into short-duration government-backed securities that generate a higher annualized yield.

Treasury accounts usually sit alongside a primary business checking account. The idea is to keep enough cash in checking to cover day-to-day expenses, then place anything that isn't needed over the next 30 to 365 days into the treasury account, where it earns more without taking on meaningful risk.

A simple example: imagine a startup with $3 million in the bank. The founders keep three months of payroll (say, $600,000) in their operating checking account to handle salaries, rent, and vendor payments. The remaining $2.4 million gets swept into a treasury account, where it earns an annualized yield in line with current short-term Treasury rates. Earning 3.77% annualized yield in Slash Treasury, then, would earn that business roughly $90,000 after a year (assuming yield remains constant). The cash is still accessible if the business needs it, but it's no longer sitting unproductive.

What is a Savings Account?

A business savings account is a standard deposit account offered by a bank or credit union. Its purpose is straightforward: store surplus cash and earn basic interest on the balance. The money sits with the bank, which pays the business a declared interest rate in exchange for holding the funds.

The mechanics are familiar to anyone who’s used a personal savings account. Interest rates are variable and can be changed by the bank at any time. Most accounts allow overdraft protection linkage to a connected checking account so funds can sweep over automatically if a payment would otherwise bounce. There are usually limits on certain types of actions, with banks often limiting withdrawals to between 5 and 10 per month.

For many SMBs, savings accounts solve a handful of common problems. Owners can use them to build a one-to-three-month emergency buffer, set aside money for quarterly estimated taxes, or park funds for specific savings goals like a marketing push or equipment purchase, and determine which account features best match those goals. The expectation is modest yield, not aggressive returns.

One thing worth flagging: business savings account interest rates have historically lagged short-term Treasury yields, especially when rate environments shift quickly. When the Federal Reserve raises rates, Treasury yields tend to move within days, while banks often take weeks or months to pass higher rates through to depositors, if they do at all.

Treasury Accounts vs Savings Accounts: Key Differences for SMBs

Both savings and treasury accounts help a business earn yield on cash, but they differ in risk profile, structure, and how the interest or yield is generated. Some businesses end up using a combination of both treasury and savings. Checking and savings handle core operations and the immediate cash buffer, while a treasury account holds long-term or excess reserves that don't need to be touched for months.

Understanding the differences between both account types can makes it easier to decide what belongs where:

Who Issues the Obligation

With a savings account, the bank is the issuer. The business is lending money to the bank, and the bank promises to pay it back with interest. With a treasury account, the underlying obligation comes from securities issued by the U.S. Department of the Treasury to finance government spending, or from other short-term money market instruments. The business owns (or has a beneficial interest in) actual government securities rather than holding a deposit claim against a private institution. Treasury bills mature in one year or less, treasury notes mature in 2 to 10 years, and treasury bonds mature in 20 to 30 years.

Type of Protection

Savings accounts are protected by FDIC insurance up to $250,000 per depositor, per bank, per ownership category. Treasury accounts work differently. Because the holdings are direct government securities, they carry the full backing of the U.S. Treasury for the underlying instruments, and the cash and securities are typically held with a custodian under regulated safeguards. Slash Treasury funds are protected up to $500,000 by the SIPC, which steps in to recover customer securities and cash held at a brokerage if that brokerage fails (separate from FDIC, which covers bank deposits).

How Rates Track the Market

Savings accounts pay a bank-set interest rate that the bank can adjust whenever it chooses. Treasury accounts pass through market-based yields from Treasuries and money market instruments, which often adjust as the Federal Reserve changes policy rates. If the Fed raises rates by 50 basis points, a treasury account's blended yield usually reflects that change within days. A savings account might take much longer to catch up, if it catches up at all.

Liquidity

Both account types are generally highly liquid, but the mechanics differ in how you can make withdrawals. Savings accounts typically allow instant internal transfers to a linked checking account at the same bank; banks will often set a maximum number of monthly withdrawals from a savings account, typically between 5 and 10. Treasury accounts can take a bit longer for withdrawls because the underlying securities trade on market hours, so same-day withdrawals usually have a cutoff time. In most cases, money is still available within the next business day, but it's worth knowing the timing if your business runs cash tight.

Minimums and Complexity

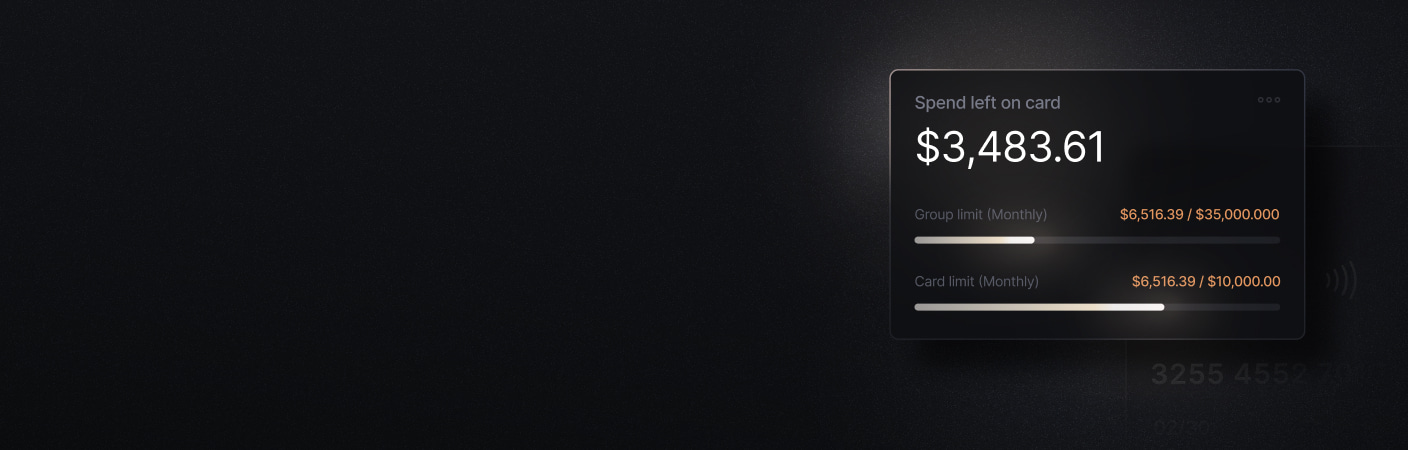

Savings accounts have low minimums (often $0 to $100) and simple monthly statements. Treasury accounts sometimes require higher minimum balances and produce more detailed reporting, including holdings, yields, and weighted average maturities. They're better suited to businesses managing six- or seven-figure cash balances where the yield difference is meaningful enough to justify the added structure. Slash has no minimum balance requirements for treasury, meaning you can start generating returns on your idle cash no matter how much you have set aside.

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

How Interest, Yield, and Original Issue Discount Actually Work

Business owners may see "interest rate" on a savings account and "yield" or "APY" on a treasury product and assume they're the same thing. They're not, and the differences matter when comparing accounts. Here's what you should know about how each generates returns:

What is interest rate for a savings account?

Interest on a savings account is a fixed percentage the bank pays you for keeping money on deposit. The bank sets a nominal rate, say 1.50%, which accrues daily based on your end-of-day balance and gets credited to your account once a month (though account fees such as a monthly service fee can reduce earnings on a savings account.) APY is just that rate expressed as what it would compound to over 12 months. Because the bank sets the rate, it can also change it at any time, so the stated rate may differ from the actual earnings you keep after fees.

What is annualized yield for a treasury account?

Annualized yield is a single percentage figure you can use to calculate what your treasury account may earn over a year, blended across all the underlying securities. The reason it needs to be calculated this way is that Treasury securities pay in different forms: notes and bonds pay fixed coupons every six months, creating periodic interest payments that can generate regular income for investors, while T-bills are sold at a discount to face value and mature at full face value, with the gap acting as the return.

A treasury account pools many securities together and shows a blended annualized yield on the total balance. Some treasury accounts also let businesses invest recurring deposits and automatically reinvest both income and principal, or send proceeds to a brokerage account. That yield moves as market rates change and the portfolio turns over, which is why treasury yields can shift daily while savings account rates may sit unchanged for months.

What is original discount?

Original issue discount (OID) is the return you earn when a security is sold below face value and pays out at full value when it matures. For example, buy a six-month T-bill at $97 per $100 of face value, and six months later it matures at $100. That $3 gain on a $97 investment over six months annualizes to roughly 6.2%. The entire return came from the gap between purchase price and maturity value, with no coupon along the way.

Use Cases: When a Business Should Use Each Type of Account

Deciding what cash goes where comes down to how soon the money is needed and how much of it there is. Here’s a simple framework to help determine how many dollars to keep in each bucket based on timing needs and reserves:

The exact ratios for how to divide up your cash can depend on how predictable your business’s cash flow is, which depends heavily on your model and operations, and the split helps you manage cash according to expected operating needs. Here are some examples:

- A subscription SaaS company with steady recurring revenue can run leaner on its operating buffer than an agency with lumpy project billings or a seasonal e-commerce brand that does most of its sales in Q4.

- E-commerce companies often keep more in treasury during slow months and pull it back ahead of peak inventory orders.

- Web3 and online travel businesses benefit most from treasury accounts because their large float balances (customer deposits, prepayments, escrowed funds) would otherwise generate zero yield while still needing full liquidity.

Treasury accounts can also support multi-entity setups cleanly. A holding company with several operating subsidiaries can consolidate yield reporting and cash visibility in one place, with sub-accounts per entity. Traditional savings accounts are usually siloed per entity, which means more logins, more statements, and more manual rollup work. Slash users can add multiple businesses under a single login and switch between dashboard views for each entity’s finances, so a founder or finance lead managing subsidiaries can see everything without juggling separate accounts.

What to Look For When Choosing a Treasury or Savings Account Provider

SMBs have more options than ever for their account provider: legacy banks, credit unions, neobanks, and specialized treasury providers. Before committing to one, a few criteria are worth checking:

- Transparency: Clear disclosure of rates, fees, custodians, and terms. If a provider can't explain in plain English where the money sits and how yield is generated, keep looking.

- For savings accounts: Minimum balance requirements, overdraft protection rules when linked to checking, monthly service fee details, and the quality of the online experience (mobile app, alerts, automatic transfer rules).

- For treasury accounts: Which instruments are used (T-bills, notes, money market funds), how funds are custodied, whether there's pass-through FDIC coverage on uninvested cash, and cut-off times for same-day liquidity.

- Yield disclosures: A quoted yield can be the current annualized rate, a historical average, or a promotional teaser. Ask how often it updates and whether the provider clearly notes that yields can fall as well as rise.

- Integrated functionality: Platforms like Slash combine high-yield treasury management, checking accounts, unlimited virtual corporate cards, working capital, crypto and stablecoin rails, and spend analytics in a single interface, which means fewer logins and cleaner month-end reconciliation.

- Operational features. Multi-entity support, role-based permissions for finance teams, API access for programmatic treasury operations, and clean reporting for board meetings and audits. These feel optional until the business hits the point where they're essential, and switching providers at that point is a real lift.

Put Your Idle Cash to Work with Slash

For most SMBs, the traditional split between savings and treasury exists because savings accounts offer easy access while treasury accounts offer better yield. Slash eliminates that tradeoff.

Slash treasury accounts earn up to 3.77% annualized yield through money market funds managed by Morgan Stanley and BlackRock, with same-day to next-day liquidity and no minimum balance to get started. Funds are protected up to $500,000 by SIPC, and the account sits alongside Slash's FDIC-insured checking and corporate charge cards in a single platform, with multi-entity support built in for businesses running more than one company.

That combination changes the calculus on where your cash should live. When a treasury account gives you near-instant access to your money and a yield that adjusts with the market, the case for keeping a separate savings account starts to make less sense. Slash lets businesses earn steady, high yield on idle cash while keeping the liquidity to deploy capital whenever they need it, all from one login.

Here are some additional Slash features to elevate how your business manages its finances:

- Slash Visa Platinum Card: Earn up to 2% cashback, assign granular spend controls for your team, and get real-time updates in your dashboard on team spend. Apply with just your EIN, with no hard pull on your credit, to access high-limit spending anywhere Visa is accepted.

- Multiple payment rails: Move money with no domestic per-transaction fees on Slash Pro. Send and receive SWIFT wires across 180+ countries and 135+ currencies, RTP and FedNow instant payments, and same-day ACH.

- Native crypto support: Built-in on- and off-ramps for USDC and USDT, so you can accept stablecoin payments and convert to fiat without a separate exchange account.⁴

- Invoicing: Send invoices directly from Slash with payment links your customers can use to pay by wire, ACH, or crypto. Payments arrive tied to the invoice.

- Accounting integrations: Native connections with Xero, QuickBooks, Sage, and NetSuite sync enriched transaction details into your books automatically.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Is a treasury account safer than a savings account?

Both are low-risk, but the protections work differently. Savings accounts are covered by FDIC insurance up to $250,000 per depositor, per bank, while treasury accounts hold direct U.S. government securities backed by the Treasury, with brokerage-level SIPC coverage on cash and securities (up to $500,000 at Slash). For balances above FDIC limits, treasury accounts often provide stronger protection than a single savings account.

Treasury Management for Startups: A Complete Guide to Cash Flow, Liquidity & Risk

Can a treasury account replace a business savings account?

For many SMBs, yes. Modern treasury accounts like Slash offer same-day to next-day liquidity, no minimum balance requirements, and yields that track market rates, which removes most of the reasons businesses keep a separate savings account as a middle layer. Some businesses still use savings accounts for very short-term cash within FDIC limits, but the case shrinks as treasury accounts get more flexible.

How much cash should a business keep in a treasury account?

A common framework is to keep 0–3 months of expenses in checking, 3–6 months in savings or a buffer account, and anything beyond 6–9 months in treasury. The exact split depends on how predictable your revenue is and the business’s cash-flow subject area of focus—such as payroll stability, seasonality, or upcoming obligations. Owners should maintain visibility in revenue and obligations to decide how much to hold before moving surplus into treasury.

Cash Flow Management: A Guide for Making Smarter Business Decisions

Read more from us