The Best Business Cards for Ad Spend: Top Picks to Maximize Your Ad Budget

While some businesses hope to capture lightning in a bottle with virality and guerrilla campaigns, steady growth usually requires a significant amount of money for advertising and marketing. In fact, publicly traded organizations spend an average of about 11% of their total revenue on marketing, per Gartner. As companies meticulously plan and organize their budgets, they may overlook a key ingredient: the card they use to spend those budgets.

Whether your business is buying ad space on Google or on billboards, your marketing budget is one of the highest-leverage places to earn rewards with business credit cards. Many providers offer business cards with cash back rewards or multiplied points on advertising spend, resulting in measurable savings that compound with use. Reward rates aren’t the only factor to consider when choosing a business credit card, though; cash back categories, annual fees, and sign-up bonuses vary widely across different options.

Below, you’ll learn about some of the top cards for advertising spend, what their strengths and weaknesses are, and how to choose the right card for your business. We’ll also take a look at Slash, a neobank that not only offers a card with granular controls and expense tracking, but also allows users to unlock cash back when paying for ads on Meta platforms through invoicing or bank debits.¹

Why Your Choice of Credit Card Matters for Ad Spend

Credit cards that offer cash back, whether in a specific spending category or on all business expenses, can give companies extra breathing room in their margins by returning much-needed capital right to their accounts. Some cards come with travel-specific rewards that give cash back and points based on flights and hotel bookings. While these cards are useful in their own right, most companies don’t spend as much of their budget on travel as they do on marketing and advertising. Among organizations with high marketing budgets, business credit cards tailored towards ad spend can help save thousands of dollars per year.

There are three factors that separate cash back business credit cards from standard credit cards. These are:

- Bonus categories: cash back or multiplied points on category-specific expenses

- Spending caps: the maximum amount of cash back you can earn in a period or year

- Annual fees: the fee the provider charges each year

Determining which business credit card is right for your company may require a little math. If you roughly know your annual marketing budget, you’ll be able to calculate how much cash back you can earn, whether you’ll break even against annual fees, and if you’ll approach spending caps.

Best Business Credit Cards for Ad Spend Compared

Let’s look at some leading business cards and compare them based on these characteristics:

Slash Visa® Platinum Card

The Slash card is a charge card that pairs up to 2% cash back with a banking infrastructure that helps manage high-volume ad spend. Charge cards, unlike traditional credit cards, require full payment at the end of each billing period rather than enabling you to roll over a balance from month-to-month. Slash users can access an integrated financial dashboard that tracks all incoming/outgoing payments, enabling business owners to monitor card spend along with the rest of their cash flow in real time.

With access to unlimited virtual and physical cards, Slash users can create sub-accounts to budget for specific categories like advertising spend. The Slash Visa® Platinum Card also comes with granular controls that allow administrators to customize spending limits and merchant category restrictions for each employee. Whereas the perks of most cards end at their rewards, the Slash Card comes with a full business banking platform.

- Rewards rate on ads: Up to 2% flat cash back

- Spending cap: None

- Annual fee:$0 (Free) / $25/mo (Pro)

- Sign-up bonus: N/A

Best for: Businesses of all sizes who want full operational control along with cash back rewards

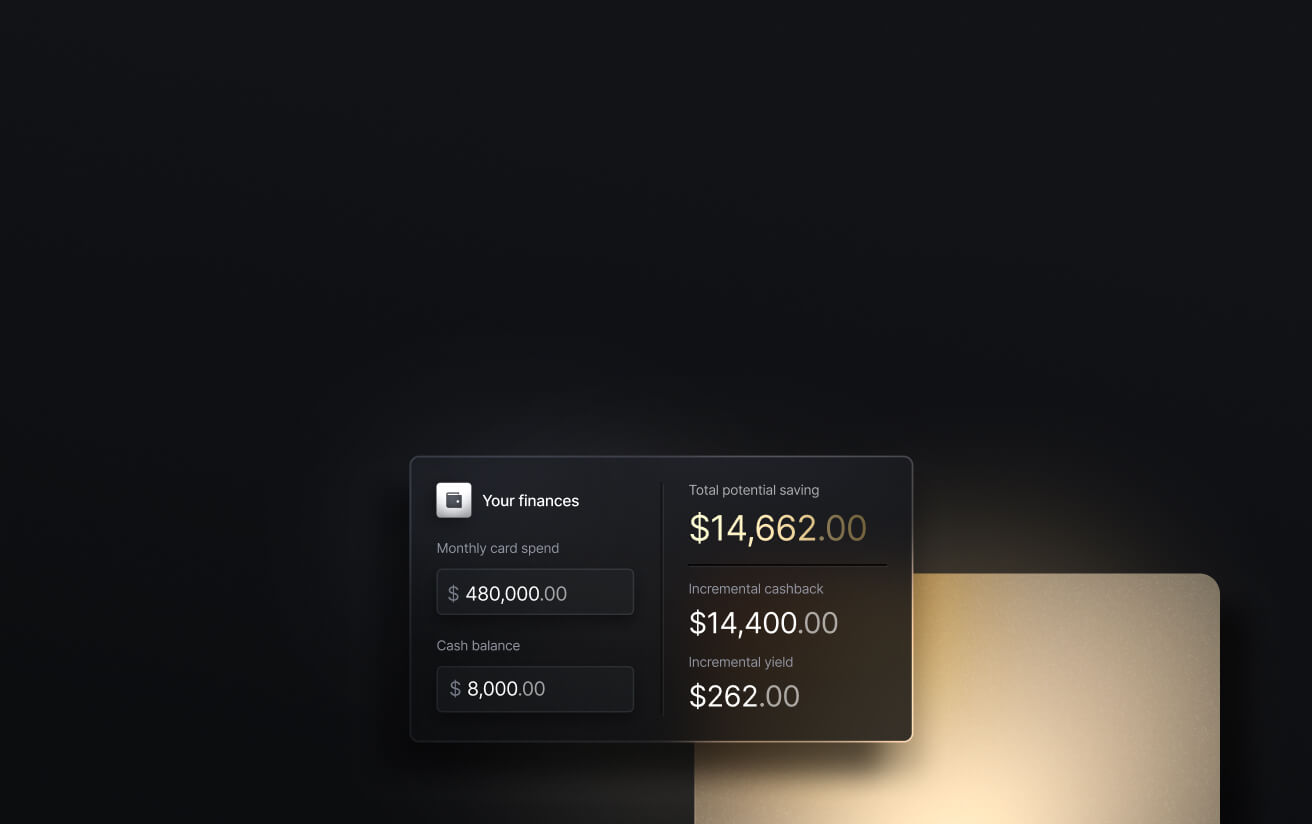

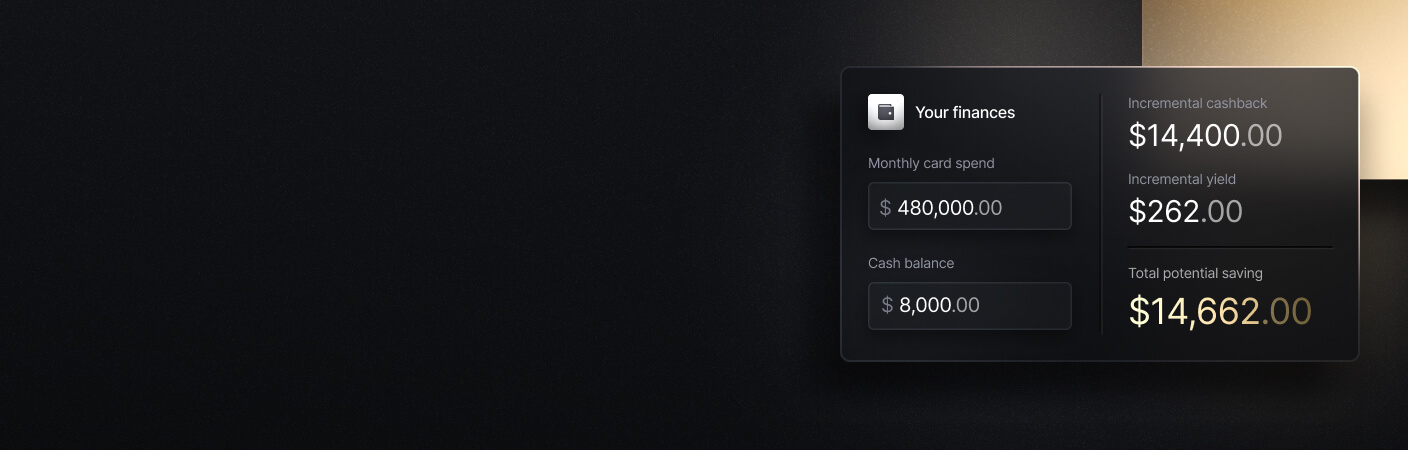

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

American Express Business Gold Card

The Amex Business Gold card earns companies 4x Membership Rewards® points on their top two spending categories each billing cycle, which can include advertising. This means that organizations with seasonal marketing pushes, such as tax prep businesses or vacation rental companies, can earn 4x rewards points on ads during the part of the year when they need them most. However, this perk is limited to $150,000 a year, no matter the categories you earn rewards on. After passing that threshold, your card Membership Rewards® points revert to 1x.

- Rewards rate on ads: 4x points

- Spending cap:$150,000/year at 4x, then 1x

- Annual fee:$375

- Sign-up bonus: Up to 200,000 Membership Rewards® points (after $15k in purchases through first 3 months)

Best for: Businesses with moderate marketing budgets or seasonal advertising

Chase Sapphire Reserve for Business

The Chase Sapphire Reserve for Business card offers 3x points on social media and search engine advertising with zero spending cap. Companies that prioritize online marketing year-round can use this card to scale their campaigns without having to worry about the end of the runway. The Sapphire Reserve card also offers premium travel perks, but it does carry an annual fee of $795.

- Rewards rate on ads: 3x points

- Spending cap: None

- Annual fee:$795

- Sign-up bonus: Up to 150,000 points (after $20k in purchases through first 3 months)

Best for: Organizations with large budgets for online marketing

Chase Ink Business Preferred Credit Card

Like Chase’s Sapphire Reserve card, the Ink Business Preferred credit card earns 3x Ultimate Rewards points on social media and Google ads. The difference lies in the other two metrics: the Ink Business Preferred card costs only $95 a year and comes with a $150,000 spending cap. The two cards can both be valuable for businesses that stick to online marketing channels, but the Ink Business Preferred card is likely better for companies with mid-sized budgets.

- Rewards rate on ads: 3x points

- Spending cap:$150,000/year at 3x, then 1x

- Annual fee:$95

- Sign-up bonus: Up to 100,000 bonus points (after $8k in purchases through first 3 months)

Best for: Smaller businesses who want ad rewards without a high annual cost

Capital One Spark Cash Plus

A business card doesn’t necessarily need specialized advertising perks to be helpful for marketing spend. The Capital One Spark Cash Plus card earns a flat 2% cash back on all business expenses. In contrast to some cards that come with $150,000 spending limits, the Spark Cash Plus card’s annual fee is actually waived if you spend more than $150,000. While the rewards rate ceiling is a bit lower than category-specific cards, there’s still value in the consistency of flat cash back.

It’s important to note that the Spark Cash Plus card is actually a charge card, not a credit card. This means that the balance must be paid in full at the end of each billing cycle, and debt cannot be accrued.

- Rewards rate on ads: 2% flat cash back

- Spending cap: None

- Annual fee:$150 (waived at $150k+ annual spend)

- Sign-up bonus:$2,000 cash bonus (after $30k in purchases through first 3 months) plus a bonus $2,000 for every $500k spent in the first year.

Best for: High-spend companies looking for predictable cash back

Chase Ink Business Unlimited

The Chase Ink Business Unlimited card also comes without category requirements, earning 1.5% cash back on all business purchases. With no annual fee and a sign-up bonus that only requires $6,000 in early spending, this card is tailored more towards small businesses with lighter cash flows. This card also comes with a 0% intro APR for 12 months, which isn’t usually found among similar options.

- Rewards rate on ads: 1.5% flat cash back

- Spending cap: None

- Annual fee:$0

- Sign-up bonus:$750 (after $6,000 in purchases through first 3 months), 0% intro APR for 12 months

Best for: Early-stage businesses with modest marketing budgets

Business Card Comparison Table

Key Factors When Choosing a Business Card for Advertising

The metrics we’ve charted above, the advertising channels your company utilizes, and a couple liability-related factors will all influence your choice of business credit card. Let’s break these down in detail:

Bonus Caps and Spending Thresholds

Bonus caps are often the simplest consideration, especially if you have a clear picture of your business’s cash flow. For many business cards with specific ad-spend categories, the bonus rate only applies up to a set amount annually. With the Amex Business Gold card, for example, you stop earning rewards after your 150,000th dollar is spent. Companies that spend $60k on ads annually will be able to take full advantage of a card with that kind of threshold, but an organization that goes through $400k annually will end up spending most of the year using a card that’s essentially rewards-free.

Points vs. Cash Back

The debate between points and cash back can get quite interesting. You likely understand the math behind cash back: a card that offers 2% cash back will give you $20 back on a $1,000 purchase. Credit card points work in a similar fashion, but the math can get complex across certain cards and categories.

As an example, let’s look at the Chase Ink Business Preferred credit card. Like most business cards, Chase allows users to earn a point per dollar spent, and each point is essentially equivalent to $0.01. So, a $1,000 advertising purchase with 3x points would earn 3,000 Ultimate Rewards points, valued at $30. This $30 can either be redeemed for cash back, gift cards, or for an additional 1.5x multiplier with a transfer to a travel partner or when used on a quarterly bonus category. Other card providers often follow the same structure: points are worth $0.01, but there are a variety of ways to multiply their earning rates and values.

As alluring as 3-4% cash back sounds, it won’t be as impactful if you breeze past the bonus cap in 6 month’s time. Points multipliers work best when your budget is near your card’s spending threshold, while flat cash back may be better when you’re planning on extending far past that limit.

Annual Fee Breakeven

Don’t put away the calculator just yet – it’s time to figure out how to break even on an annual fee. If you’re absorbing a $795 annual fee with the Chase Sapphire Reserve card, you’ll need to earn more through rewards for the investment to be worth it. Since the card has no spending cap, this isn’t too large of a hurdle. If an organization earns 3x points on $200k in annual ad spend, they’ll receive $6,000 worth of points, which is well above the annual fee. To find the minimum spend to reach breakeven, divide the annual fee by the effective reward rate.

Annual Fee ($795) / Reward Rate (.03%) = $26,500.

A company using the Chase Sapphire Reserve card would have to spend at least $26,500 on ads to match their annual fee. Of course, earning money is always better than breaking even, so this number should be considered your bare minimum.

Fraud Protection and Spend Controls

Perks matter less if your business card lacks safeguards against misuse. Look for a provider that offers real-time alerts and granular spend controls for cards. With Slash, you can set merchant and country restrictions, monitor transactions as they happen, and pause cards instantly from the dashboard if something looks off. These controls can help businesses respond quickly to suspicious activity and reduce the risk of fraud.

Personal Cards vs. Business Credit Cards

As business owners shop for credit cards, they may be tempted to look into personal credit cards that offer certain perks or an easier sign-up process. However, mixing business ad spend with a personal credit card creates tax and accounting complications that compound over time.

Business purchases made with a personal card are harder to substantiate as legitimate deductions, more difficult to reconcile at tax time, and blur the liability boundary between the company and the owner. Additionally, personal cards rarely come with spend controls, multi-user privileges, or meaningful bonus categories that businesses can take advantage of. No matter the size of your company, a business card is always the smart choice.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How Slash Helps Businesses Get More from Their Ad Spend

Digital marketing is a key element to modern advertising, regardless of your company’s industry or size. However, one of the biggest digital marketing channels on the planet just shut its doors on business credit cards entirely: Meta. In March, Meta announced that credit card payments would no longer be accepted from many high-spend advertisers, and that they would instead be prioritizing monthly invoicing or direct bank debits. If a majority of your company’s digital advertising is on Facebook or Instagram, the ad-specific rewards available on different credit cards just became a moot point.

Slash set out to change that. We created a first-of-its-kind solution that unlocks 1% cash back on Meta transfers, both through invoice and bank debits. Just as the Slash Card earns up to 2% cash back on all business expenses, the Slash platform restores 1% cash back on digital ad space purchased from Meta.

Our platform supports a variety of payment rails beyond cards and direct bank debits. Slash users can send funds via global ACH, international wire transfer, and real-time networks like RTP and FedNow. We also support the two most commonly used stablecoins, USDC and USDT, and offer native on/off ramps so you can send and convert your crypto in minutes.⁴

Other Slash features include:

- Working capital financing: Our users can choose between flexible 30, 60, or 90 day repayment terms, allowing their businesses to continue to scale while still supporting liquidity for daily operations.⁵

- Accounting software integrations: Slash integrates with QuickBooks Online, Xero, and Sage Intacct, helping finance teams work faster and with greater accuracy. Streamline your reconciliation with automated workflows for expense reporting, tax preparation, and more using financial data from your Slash account.

- Global USD accounts: With access to Slash’s Global USD account, founders in 130+ countries can hold dollar-based funds, send & receive ACH/wire, and make stablecoin payments without a U.S.-incorporated LLC.³

- Expense management features: Users can streamline their expense reporting with end-to-end SMS receipt collection for Slash cards, streamlined reimbursement flows, and automatic accounting updates.

If you miss the cash back you were earning on Facebook ad spend – or if you’re just searching for a banking platform that centralizes your financial tools – look no further than Slash.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Can agencies use multiple cards for ad campaigns?

If they choose to, yes. An optimal way to use multiple cards for different ad campaigns is by taking advantage of the unlimited virtual cards that a platform like Slash supports. Companies can create a virtual card for each campaign, assign them to different employees or departments, and customize their limits.

Mercury Bank Alternatives: Compare Features, Benefits, and Options

What’s the best business card for advertising spend?

It depends on whether you prefer points or cash back. The American Express® Business Gold Card offers 4x Membership Rewards® points on eligible advertising purchases, making it a strong option for points. For cash back, the Capital One Spark Cash card and Slash Visa® Platinum Card both offer up to 2% cash back depending on usage.

What limits matter for ad spend cards?

The bonus spending cap is typically the main limit companies should be mindful of when choosing a business credit card, since surpassing that limit halfway through your year will negatively affect the overall impact you can get out of the card. Small business owners who won’t spend anywhere near the bonus cap may focus more on annual fees.

Unlimited Cashback vs. Tiered Rewards: Key Differences Explained

Are there cards that offer specific perks with Google Ads or other types of online advertising?

Yes, some cards cater to online advertising in particular. The Chase Ink Business Preferred Credit Card offers point bonuses for social media and search engine advertising, while the Slash Card unlocks Slash Perks, which can generate over $1M in discounts on the platforms and services your business uses every day.