Decentralized Finance: What You Should Know Before Getting Started

Imagine walking into a bank and asking to borrow ten million dollars. No collateral, no credit check, no name on the paperwork. The only condition is that you pay it back within a few seconds, and if you don't, the loan is unwound as though it never happened. Every bank on earth would show you the door. In decentralized finance (DeFi), these are called flash loans, and thousands of them happen every day.

DeFi is a wild world. At one end are the parts that have grown into real industries and entered mainstream financial conversation, like dollar-pegged stablecoins and large crypto exchanges. At the other end are the more experimental facets like NFTs, prediction markets, and synthetic stocks, which not only carry a less reputable connotation, but can present real risks tied to thin market-making and code manipulation.

This guide walks through the basics of decentralized finance: the blockchain technology powering the sector, the main types of services used today, and the risks and benefits that come with them. One of DeFi's most practical outputs is stablecoins, which are dollar-pegged cryptocurrency assets that can settle faster and cheaper than a bank transfer. If you're wary of dabbling in DeFi just to use them, consider Slash: a business banking platform that lets you send and receive stablecoins like USDC and USDT from the same place you manage your corporate cards, business accounts, and more.¹, ⁴

What is Decentralized Finance (DeFi)?

Decentralized finance, usually shortened to DeFi, is a set of financial services that run on public blockchains instead of through banks, brokerages, or payment companies. Instead of a bank sitting in the middle approving and recording every transaction, the rules for transactions and approvals are written into software called smart contracts that execute automatically when certain conditions are met.

DeFi today spans a wide range of services. The two biggest pillars of DeFi by activity are lending and decentralized trading, but the idea underneath all of them is the same: financial services are handled by open-source code. Here's a shortlist of the different areas of DeFi:

- Lending and borrowing markets

- Decentralized exchanges for trading one token against another

- Stablecoins

- Yield strategies like staking and liquidity provision

- Derivatives trading

- On-chain insurance

- Crypto asset management

Most DeFi activity runs on Ethereum, though other blockchains host it too. The common thread is that these systems are permissionless and open: in most cases anyone with an internet connection and a crypto wallet can use them, without an application, a credit check, or approval from an institution. The openness is the appeal; however, as the later sections cover, it is also where much of the risk comes from.

Core Components of Decentralized Finance

DeFi is less a single product than a stack of building blocks. Three of those blocks form the base: the smart contracts that hold the rules, the decentralized exchanges where tokens get traded, and the peer-to-peer lending markets where capital is borrowed and lent. Here's how each works in more detail:

Smart Contracts

A smart contract is code deployed to a blockchain that carries out an agreement automatically once its conditions are met: swapping one token for another at the current pool price, releasing a loan when enough collateral is posted and liquidating that collateral if it falls too far, or paying out trading fees to whoever supplied liquidity. It's code that anyone can inspect, that follows the same rules for everyone, and that keeps a public record of what happened.

The advantage is that the logic is transparent and consistent. The terms are visible on the blockchain, they apply the same way to every user, and once the contract is deployed no single party can rewrite them. The tradeoff is that a smart contract will do exactly what its code says, including if the code has a mistake. If there is a flaw or an exploitable gap in the code, funds can be drained without much recourse to recover them. Reputable DeFi protocols try to manage the risk of vulnerabilities with independent security audits.

Decentralized exchanges (DEXs)

A decentralized exchange, or DEX, lets people trade one token for another directly through a protocol, without an exchange company holding their funds or matching their orders. Most DEXs skip the traditional order book that pairs a specific buyer with a specific seller. Instead they rely on liquidity pools: shared reserves of two or more tokens, locked in a smart contract, that you trade against directly. The price adjusts automatically based on the ratio of assets in it. This design is known as an automated market maker.

The pools are funded by users called liquidity providers, who deposit their own tokens and, in exchange, earn a share of the trading fees the pool generates. This is what lets a DEX run around the clock without a central market maker. Providing liquidity carries a specific risk: impermanent loss, which is the gap in value that can open up between holding two tokens and depositing them into a pool when their relative prices move.

Peer-to-Peer Lending

DeFi lending lets people lend and borrow directly through a protocol rather than through a bank. Lenders deposit assets into a pool and earn interest; borrowers draw from that pool and pay interest, with rates that typically adjust automatically based on how much of the pool is being borrowed at any given moment. This peer-to-peer lending approach uses code instead of human underwriters to coordinate loans at scale.

The feature that makes this work without credit checks is overcollateralization. Because a protocol cannot chase a borrower for repayment the way a bank can, it usually requires the borrower to post collateral worth more than the loan itself (often significantly more). If the collateral's value drops too far, the smart contract liquidates it automatically to protect the lenders. This is why someone might borrow against crypto they already hold rather than sell it: they get access to cash-like assets while keeping their position, as long as they stay ahead of the collateral requirement.

The Role of Stablecoins in DeFi

Most cryptocurrency have incredibly volatile price swings, which is a problem if you are trying to lend, borrow, or settle a payment. Stablecoins solve that. A stablecoin is a token designed to hold a steady value; the leading stablecoins, USDC and USDT, are pegged one-to-one to the U.S. dollar and backed by cash and T-bill reserves.

What makes stablecoins useful is a mix of predictability (the balance does not double or halve while you hold it) and speed (a transfer can settle in minutes at most hours of the day). And, since they’re available on public blockchains, stablecoins can plug directly into smart contracts. Stablecoin usage in DeFi can include:

- Lending and borrowing: Stablecoins are the default unit for DeFi lending. A loan denominated in a dollar-pegged stablecoin is one you can actually reason about, since the loan’s value doesn’t swing with the market.

- Trading: Most token pairs on decentralized exchanges are quoted against a stablecoin, giving traders a steady asset to move in and out of.

- Collateral and yield: Stablecoins can be posted as collateral or supplied to a liquidity pool to earn a return without ever leaving the blockchain.

- Payments and settlement: Stablecoins move quickly and cheaply relative to traditional banking rails, which is especially useful for cross-border payments where the conventional options can be slow and expensive.

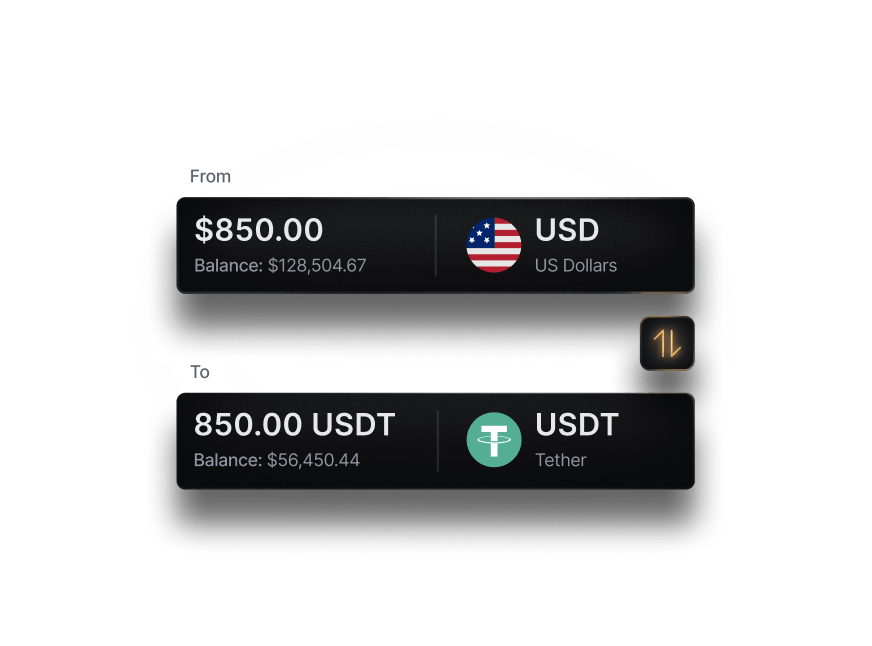

This is where a platform like Slash fits for a business that wants stablecoin functionality without operating deep in DeFi itself. Slash lets businesses send and receive USDC and USDT natively from the same dashboard they use for the rest of their finances. Transfers can settle across eight major blockchains and can be faster and lower-cost than a traditional bank transfer for international payments.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Understanding Decentralized Autonomous Organizations (DAOs)

A decentralized autonomous organization, or DAO, is a group that coordinates and makes decisions through rules encoded on a blockchain rather than through a traditional management hierarchy. In DeFi, DAOs are how many protocols govern themselves after launch. Instead of a board and executives deciding how an organization spends its money or changes its product, the members vote, and the outcomes are carried out by smart contracts.

Voting power is usually tied to governance tokens. Holding a project's governance token gives you the right to propose changes and to vote on proposals others make, often in proportion to how many tokens you hold. Decisions and the funds they control are typically visible on-chain, which makes a DAO more transparent than a conventional company.

This works better in theory than it sometimes does in reality; low participation or uneven token distribution can leave decision-making in the hands of a small number of stakeholders. Still, the model is central to how DeFi aims to stay decentralized rather than drifting back toward a single company in control.

What are the Potential Risks and Benefits of Decentralized Finance?

Here's the appeal of DeFi: it is open to people who traditional finance leaves out, it runs continuously without banking hours or holidays, its rules are transparent and applied uniformly, and it can lower costs by removing layers of intermediaries. But those same properties come with risks that behave very differently from anything in the traditional financial system. Here's what you should weigh before getting involved:

Potential Benefits of DeFi

- Open access: In most cases anyone with an internet connection and a crypto wallet can use DeFi, without an application, a credit check, or approval from an institution.

- Always on: Protocols run continuously, without banking hours, holidays, or settlement delays, so lending, trading, and payments happen around the clock.

- Transparency: The rules live in public code and transactions are recorded on-chain, so the terms are visible and apply the same way to every user.

- Lower costs: Removing layers of intermediaries can reduce the fees attached to services like trading, borrowing, and cross-border payments.

- Self-custody and control: You hold your own assets rather than handing them to an institution, which generally means an intermediary is not positioned to freeze your account or block a transaction.

Potential Risks of DeFi

- Smart contract risk: Code can contain bugs or exploitable flaws, and when funds are lost to an exploit there is usually no way to reverse the transaction and no institution obligated to reimburse you. Audits help but do not eliminate this.

- Market and liquidation risk: Crypto collateral can fall sharply and quickly, and if yours drops below a protocol's threshold it can be liquidated automatically, sometimes at a bad moment.

- Custody risk: Self-custody cuts the other way from traditional banking. A lost recovery phrase or a mistaken transfer generally cannot be undone, and there is no customer support line and no deposit insurance standing behind your balance.

- Regulatory uncertainty: Rules for DeFi are still developing and can change how, or whether, certain services operate.

- Scams and fraud: In a permissionless space where anyone can launch anything, fraudulent projects and outright scams are common.

Add Stablecoins to Your Financial Stack with Slash

For most businesses, the appeal of stablecoins is practical: move dollars across borders quickly, without the cost and delay of a traditional wire. Slash makes that possible without asking you to learn DeFi or manage a crypto wallet. You can send and receive USD-pegged stablecoins like USDC and USDT, move between dollars and stablecoins when you need to, and settle across eight major blockchains, all from the same dashboard you use to run the rest of your finances. Because Slash handles the stablecoin rails rather than handing you a wallet to secure yourself, you get the speed of stablecoin payments with the guardrails of a compliant financial platform.

Stablecoins are just one part of the platform. Slash brings together FDIC-insured business accounts, corporate cards earning up to 2% cash back, multi-rail bank transfers, and a high-yield treasury account, with no monthly fees and no personal guarantee to get started.², ⁶ If stablecoins are becoming part of how your business moves money, Slash is a straightforward way to add them to your financial stack.

Here’s what else you get with Slash:

- Slash Visa Platinum Card: A corporate charge card that earns up to 2% cashback on eligible business spending. Set granular card controls, customizable limits, or team-specific groupings to better handle employee spending.

- Diverse payment methods: Slash supports a wide range of payments, including same-day ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- High-yield treasury: Earn up to 3.84% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.

- AI-powered insights: Ask Twin, Slash’s AI financial assistant, to analyze your finances for you, giving easy-to-understand explanations about your metrics. Make online purchases, freeze cards, and track spend from end-to-end with a simple prompt.

- Expense management: Streamline expense reporting with end-to-end SMS receipt collection for Slash cards, simple reimbursement flows, and automatic accounting updates.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

What is the Global Future Council on Decentralized Finance?

It is a working group convened by the World Economic Forum that brings together academics, industry executives, and public sector officials to build a shared understanding of decentralized finance. The aim is to support more consistent, globally coordinated policy rather than to run or regulate any individual DeFi service itself.

Is decentralized finance safe?

DeFi carries meaningful risks that differ from traditional finance, so "safe" depends on how you use it and which protocols you trust. There is no deposit insurance, transactions generally cannot be reversed, smart contracts can be exploited, and you are responsible for securing your own wallet. You can reduce risk exposure by sticking to established, independently audited protocols, starting with small amounts, and never committing money you cannot afford to lose.

Business Fraud Prevention: A Guide for Protecting Your Company

How Is DeFi different from bitcoin?

Bitcoin is a single blockchain built primarily to be a decentralized digital currency and store of value. DeFi is a broader category of financial applications, mostly built on programmable blockchains like Ethereum, that use smart contracts to offer services such as lending, borrowing, and trading without traditional intermediaries.

Stablecoins vs Crypto: What Businesses Should Know