Stablecoins vs Crypto: Differences and Use Cases for Businesses

$118,000,000,000,000. That was the total value of digital tokens traded, invested, and spent in 2025, per Yahoo Finance. As cryptocurrency grows in popularity and accessibility, business owners across industries are learning how to integrate it into their payment infrastructure. This has led to a new question: “What kind of crypto should I use?”

The word “crypto” is a broad term that’s often applied to a number of blockchain-based assets. In a business context, you’ll likely be deciding between two different types of digital currency: stablecoins and traditional cryptocurrency. Stablecoins are virtual tokens that attach their value to a government-issued currency like the U.S. dollar. Standard cryptocurrencies like Bitcoin are a form of decentralized money that can be used for payments and investments.

Both stablecoins and traditional cryptocurrencies offer valuable features that can help forward-thinking businesses save money and streamline payments. In this article, we’ll break down stablecoins and cryptocurrencies, their key differences, use cases for each, and their regulatory environments. We’ll also examine Slash, a neobank that allows users to send and receive stablecoins with the help of native on/off ramps.¹, ⁴

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Glossary

Here’s a quick glossary to get you up to speed on some important terms before we break everything down:

- Fiat currency: Federally-issued money that is declared legal tender, such as the U.S. dollar or the EU’s euro. The value of fiat currencies comes from their issuing government and central bank instead of a physical commodity like gold.

- Blockchain: A decentralized ledger that records and verifies transactions across a network of computers rather than relying on a centralized authority. Once a transaction is confirmed and added to the blockchain, it becomes extremely difficult to alter. This structure allows payments to be verified and settled without relying on an intermediary like a correspondent bank.

- Decentralization: The transfer of control and decision-making from a centralized entity (like a bank or government) to a distributed network of participants. Decentralization ensures no single entity controls the blockchain, enhancing censorship resistance, security, and trustless operation.

- Smart contracts: Self-executing contracts that automatically enforce agreements when predetermined conditions are met, such as terms agreed upon by buyers and sellers. This means human intervention and third-party verification aren’t required.

Cryptocurrency Explained

Crypto is a form of digital currency that can be used for both electronic payments and as a store of value. For the most part, each type of cryptocurrency operates on its own blockchain. Bitcoin, launched in 2009, was the first decentralized digital currency. In 2015, Ethereum introduced a programmable blockchain layer that enabled smart contracts and a broader ecosystem of decentralized applications. Cryptocurrencies like Bitcoin and Ethereum can be stored in digital wallets, traded on crypto exchanges, and used for payments on blockchain networks.

Unlike stablecoins or fiat currency, the value of traditional crypto is determined by open-market supply and demand. For this reason, crypto tends to be highly volatile, experiencing dramatic price changes rapidly. This can make its use risky for B2B transactions, since its value can fluctuate 5-10% between the time a payment is agreed upon and the time it’s executed. The average Bitcoin payment can take anywhere from 10 minutes to several hours to settle, depending on network congestion. When a crypto transaction is worth over $10,000, volatility can cost the recipient hundreds of dollars between initiation and settlement.

As a result, many businesses are instead using traditional crypto as a treasury diversification asset that hedges against inflation. Due to the fact that Bitcoin is capped at 21 million coins, its value can appreciate under inflation pressures in the same way that gold does. Some businesses also invest in crypto the same way they would a stock on the S&P 500, as there’s potential for significant value gains over time.

What Are Stablecoins, and How Do They Work?

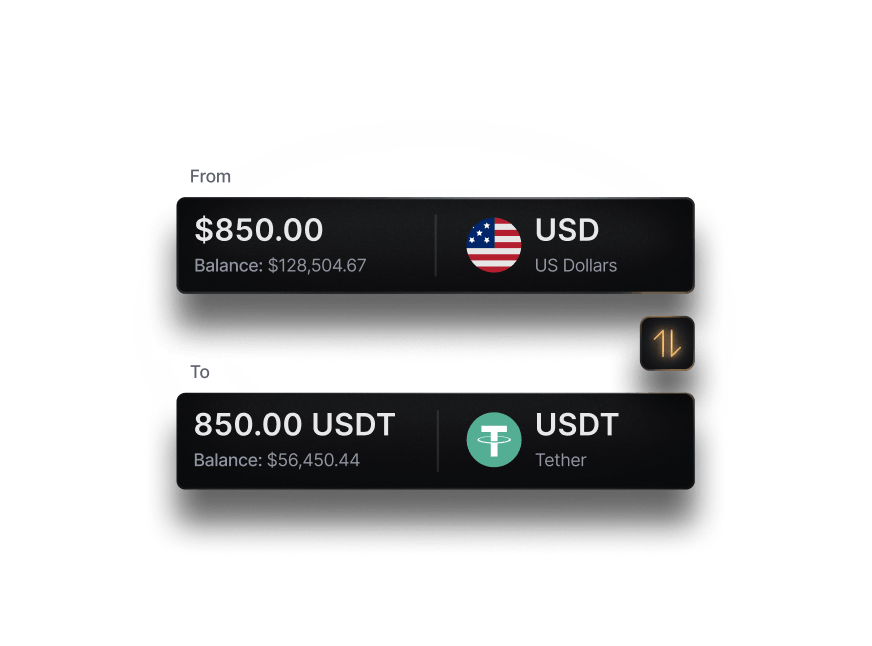

Stablecoins are virtual tokens designed to maintain price stability, usually by being linked to an underlying fiat currency. The two most popular stablecoins in use today are USDC (Coin) and USDT (Tether), which are both pegged 1:1 to the U.S. dollar.

These tokens can maintain their stability because the asset they’re pegged to is held in reserves. For example, a stablecoin with $8 billion in circulation would need to be backed by at least $8 billion in reserves from the issuer. USDT holds approximately $189 billion in total reserve assets against roughly $184 billion in circulation, while USDC holds $77.2 billion in assets backing $77.1 billion in circulation.

Their lack of volatility is the main feature that sets them apart from standard cryptocurrencies, as the value of a stablecoin rarely fluctuates more than 1-2%. They’re also created in different ways: stablecoins are issued by private companies and operate across multiple blockchains, while crypto is generated by independent parties through mining or staking and typically operates on its own individual blockchains.

Stablecoin settlement times are often under a minute, outpacing tokens like Bitcoin and Ethereum. The low volatility and high settlement speeds of stablecoins have made them appealing to businesses that wish to make quick, high-value payments. If a company sends $20,000 in USDT overseas to a business partner, it will likely arrive in minutes with a value of approximately $20,000. If a company makes the same payment with Bitcoin, it may take longer to arrive and settle, and its dollar value could shift by hundreds of dollars in either direction before settlement.

Stablecoins also exist as programmable assets, which means custom payment rules can be embedded directly in the transaction flow. These rules can govern conditional capital releases, split payments, automated transfers, and more.

While not as commonly used as traditional crypto, the stablecoin market has grown substantially in recent years. The combined market cap of USDT and USDC has grown from $120.41 billion in 2021 to $260 billion today. Slash supports both stablecoins, and offers built-in on/off ramps that allow users to automatically convert them to USD. Slash allows users to send and receive stablecoins with fees below 1% and near-instant settlement times.

Key Differences: Stablecoins vs. Cryptocurrency

From initial creation to transaction settlement, stablecoins and crypto carry a number of significant differences. Below, we compare them at a glance:

Business Payment Applications: When to Use Each

While cryptocurrencies and stablecoins are useful in several business scenarios, their use cases don’t necessarily overlap. Let’s examine some scenarios in which your company may want to use one, the other, or both:

Operational payments

For routine transactions that require predictable value, such as vendor or contractor payments, stablecoins are often the right choice. When both parties use a banking platform like Slash that offers native on/off ramps, stablecoins can be converted, sent, and settled in minutes. Given the popularity of standard crypto, a vendor may request Bitcoin payments only. While this is also an accessible payment method, everyone involved should be aware of the volatility risks.

Example: An IT contractor requests to be paid by USDT, as they’re adopting stablecoins into their payment operations and they prefer the speed of settlement. They can receive these payments at any time of day, and if they use Slash, they can off-ramp the funds immediately.

International payments

Stablecoins can outperform standard international payment systems in several ways. They offer near-instant settlement, lower transaction fees, and 24/7 availability that most banking infrastructures struggle to compete with. For example, a cross-border wire through SWIFT can take 1–5 business days and cost $25–$50 per transaction, with potential intermediary bank fees and processing delays. The same stablecoin transfer can settle in minutes for a fraction of the cost.

Example: A U.S.-based car company receiving supplies from a manufacturer in Japan forms an agreement to begin exchanging stablecoin payments. This saves both companies time and money, and minimizes production delays caused by delayed transfers.

Treasury management

While traditional treasury management involves bank accounts and bonds, crypto treasury management involves digital wallets and blockchains. A company may want to incorporate digital tokens into their treasury system in order to protect against fiat inflation and diversify their overall reserves. This is possible with both stablecoins and standard crypto, but the same risks and benefits exist: stablecoins will consistently hold the same value, while crypto may rise or fall without warning. Holding a lot of crypto in your treasury reserves is a gamble, but it’s a strategy that has high upside.

Example: A tech company added both Bitcoin and USDC to its treasury reserves. Over a year’s time, their USDC helped them manage their liquidity, and their Bitcoin rose 6% in value.

Consumer purchases

According to PayPal, about 40% of U.S. merchants accept digital tokens. Among those merchants, crypto payments represent 26% of total sales. Even though stablecoins can be held and transferred at the individual level, many businesses only accept Bitcoin at checkout. The volatility risks that can plague B2B crypto payments still exist when making an online purchase, but the smaller scale of a singular transfer often means price fluctuations are negligible.

Example: A headphone manufacturer accepts Bitcoin within its online storefront. Their flagship headphone is priced at $40 USD, which means short-term crypto market volatility could cause the price paid in Bitcoin terms to fluctuate by a few dollars in either direction at the time of purchase.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Regulatory Landscape and Compliance Considerations

Cryptocurrencies and stablecoins are treated quite differently by various international bodies, meaning that businesses have to keep certain rules and regulations in mind when adopting digital tokens.

Stablecoin regulations

The last few years have seen the introduction of significant stablecoin regulations in a number of countries. In 2023, the European Union introduced MiCA (Markets in Crypto-Assets), which requires stablecoin issuers to obtain authorization, hold full reserves, undergo regular audits, and redeem at face value. Two years later, the United States passed the GENIUS act, which stipulates conditions for 1:1 reserves along with monthly reporting and public disclosure.

Businesses using stablecoin payment infrastructure will also likely encounter Know Your Customer and Anti-Money Laundering requirements, particularly in regulated jurisdictions. Frameworks like these don’t impede easy transactions – they give businesses more confidence in the regulatory standing and reliability of mainstream stablecoins.

Cryptocurrency classification

Major cryptocurrencies like Bitcoin and Ethereum are actually treated as commodities by the Commodity Futures Trading Commission (CFTC), placing them outside the regulatory perimeter that governs securities and banking. This status means businesses accepting or holding Bitcoin face tax treatment similar to holding a commodity, with market gains and losses recognized at each transaction event. For businesses, accounting for crypto may become a headache, as each payment generates a taxable event. Crypto transfers require the tracking of cost basis, fair market value at time of transaction, and the resulting capital gain or loss.

Simplify Your Stablecoin Transfers With Slash

While traditional cryptocurrencies can be fun to hold and trade, businesses may encounter volatility problems when initiating large transactions with digital tokens like Bitcoin. The quicker processing times and improved stability that stablecoins offer make them preferable for just about any type of B2B payment. However, moving between fiat currency and stablecoins can be tricky without a dedicated platform like Slash.

Slash’s built in on/off ramps enable seamless transitions between USDC, USDT, and actual US dollars without the need to juggle multiple payment infrastructures. Businesses can off-ramp stablecoins into USD with conversion fees of less than 1% per transaction. We also offer our own stablecoin, USDSL, which is backed by U.S. Treasury bills and USDC.

Our platform gives businesses access to a diverse range of payment rails. Users can send and receive funds through same-day ACH, RTP/FedNow, international wire, or eight different blockchains that support the near-instant transfer of stablecoins. For entrepreneurs based outside the U.S., the Slash Global USD account allows companies to open a business account without forming a domestic entity.³ Built on USDSL-backed infrastructure, the Slash Global USD account allows you to hold, send, and receive USD payments via ACH, wires, or blockchains.

Slash offers other features that help streamline financial management, including:

- Powerful integrations: Our platform integrates with accounting systems like QuickBooks Online, Xero, and Sage Intacct. Transaction data syncs automatically, reconciliation happens in real time, and finance teams maintain complete visibility without having to work across multiple fractured systems.

- Connected AI agents: With support for Model Context Protocol (MCP), users can now connect AI agents directly to their business finances. Create cards, send payments, manage invoices, and query your transaction data, all through Claude, ChatGPT, and other MCP-compatible agents.

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. U.S. users can also earn up to 2% cash back on business purchases.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Are stablecoins safer than Bitcoin for business use?

When it comes to safeguarding against fraud, both stablecoins and Bitcoins are rather safe (as long as you keep a tight hold of your private keys). However, given price fluctuations, stablecoins are safer for business purposes.

Can businesses use both stablecoins and traditional crypto?

They sure can – if a business wanted to use both at the same time, they may want to use stablecoins for payments and traditional crypto for treasury holding.

Crypto Accounting Guide: Workflows, Compliance & Best Software

How do transaction fees compare between stablecoins and Bitcoin?

Bitcoin transaction fees vary based on demand and blockchain space, while stablecoin fees vary based on the blockchain. Each transfer is different, but prices are typically low.

Crypto Payment Processors: Compare Top Platforms for Businesses