What Are Corporate Expense Cards? Types, Benefits, and the Top Providers

Spending money isn’t necessarily complex when you’re in the first stages of growing a business. However, as your company scales and you bring on more team members, employee spending may outgrow the systems meant to manage it. Receipts stack up in email inboxes, expense reports arrive weeks after purchases were made, and finance teams have no visibility into their cash flow until the month is already over. Trying to juggle this with one payment card and/or one person in charge of purchases essentially becomes impossible.

Corporate expense card programs exist to solve this. Modern card programs can give businesses real-time visibility into company spending, embed spend controls before purchases happen rather than reviewing them after, and reduce the administrative overhead that traditional expense reimbursement processes require at scale.

This article explains the main types of corporate expense cards, why businesses use them, what to look for when evaluating providers, and which platforms fit different operational needs. We’ll also take a deep look at the Slash Visa® Platinum Card, a charge card that up to 2% cash back along with the spend controls and financial tools to support your team at scale.¹

What Are Corporate Expense Cards?

Corporate expense cards are payment cards issued to employees for business-related spending, tied to company-level oversight, approval workflows, and finance visibility. Unlike personal credit cards used for business purposes, corporate expense card programs are designed around the company's financial controls. Spend limits, merchant category restrictions, approval routing, and real-time reporting are often built into the card program itself rather than enforced retroactively through expense review.

Corporate Credit Cards

Corporate credit cards extend a revolving credit line to the business, allowing card balances to be carried month to month. Interest applies to unpaid balances, and credit limits are set based on the company's creditworthiness. Corporate credit cards from traditional banks are often issued under the company's name, without requiring a personal guarantee from individual employees (though some programs require a personal guarantee from the business owner). They're well-suited for businesses that need financing flexibility and want to extend purchasing power beyond current cash on hand.

Corporate Charge Cards

Corporate charge cards function like credit cards in most respects, but the full balance must be paid at the end of each billing cycle. There's no option to carry a balance or pay interest over time. In exchange for this full-payment requirement, charge cards are often available without personal guarantees, approved based on the business's financial standing rather than personal credit, and frequently come with stronger spend management features and higher effective limits. The Slash Visa® Platinum Card, for example, offers unlimited virtual cards that can each carry their own customized budgets and restrictions.

Corporate Prepaid Cards

Corporate prepaid cards are pre-funded with a specific balance before issuance. These cards can only be used up to the loaded amount, which makes them well-suited for controlled disbursements like project budgets, contractor payments, travel per diems, or one-time purchases. Prepaid card structures vary across providers; some allow real-time reloading from a central company balance, while others require manual top-ups. They eliminate the credit underwriting process entirely, but require that cash be allocated upfront before spending can occur.

It’s important to note the distinction between corporate cards and traditional small business credit cards. Small business credit cards are typically tied to a personal guarantee from the business owner and underwritten primarily on the owner's personal credit history. Corporate cards are underwritten based on the company's financial profile, and the program is designed around multi-employee cardholder management rather than a single primary account holder.

Why Companies Use Corporate Cards

Here’s why many business leaders adopt corporate expense cards as they continue scaling:

Better Visibility Into Company Spending

Traditional expense management produces a picture of company spending that's always in the past. By the time employees submit reports, managers review them, and the finance team reconciles the data, the money is already gone and decisions have already been made without full information. Corporate expense cards shift this to real time: every transaction appears in the platform's dashboard at the moment it occurs, categorized and attributed to the correct employee, department, or cost center.

For finance managers overseeing multiple teams or budget lines, that real-time view changes how spending can be managed. Instead of discovering at month-end that a department overspent its marketing budget, the overage is visible the day it happens. It’s early enough to reallocate, have a conversation, or adjust the card limit before further damage is done.

More Control Over Employee Purchases

Spend controls embedded in the card are more reliable than policies written in a document that employees may or may not follow. Corporate expense card programs allow finance teams to set per-employee spending limits, restrict spending to approved merchant categories, block specific vendors, and require manager approval before a transaction above a threshold is authorized. When an employee tries to make a purchase outside these parameters, the card declines.

This also reduces the need for employees to ask permission for routine purchases that fall within their role's normal scope. A marketing manager with a card scoped to their ad platform budget can spend without friction, and the finance team maintains visibility and control without needing to comb through every transaction.

Simpler Expense Management and Reconciliation

Receipt capture, expense categorization, and accounting sync are the three points where traditional expense workflows generate the most friction. Good corporate expense card programs address all three: transactions prompt receipt capture at the point of purchase via a mobile app, are automatically categorized against the chart of accounts, and sync to accounting software without requiring manual re-entry. Month-end close becomes faster when the data is already organized and documented in the general ledger.

For employees, this eliminates the end-of-month expense reporting session. For finance teams, it eliminates the manual reconciliation work of matching employee submissions to card statements. It helps everyone out.

More Efficient Approvals and Spend Workflows

Manual approval processes like email chains and verbal permissions usually don't scale well. Corporate expense card programs replace these with structured digital workflows. Requests can route to the right approver based on configurable rules, approvals are logged with a timestamp, and the audit trail is maintained automatically. For businesses managing multiple departments or geographically distributed teams, this structure is the difference between a spend management process that scales and one that can’t keep up.

What to Look for in a Corporate Expense Card Program

Spending Controls and Approval Features

The depth and granularity of spend controls varies significantly between providers. At a minimum, most corporate card programs support per-employee spending limits, merchant category code (MCC) restrictions, and real-time transaction alerts. More advanced programs might support vendor-level restrictions, time-based limits, department-level budget allocation, and multi-level approval routing. For businesses with complex expense policies, the question is how much of that policy can be embedded in the card controls versus how much still depends on manual review.

Accounting and ERP Integrations

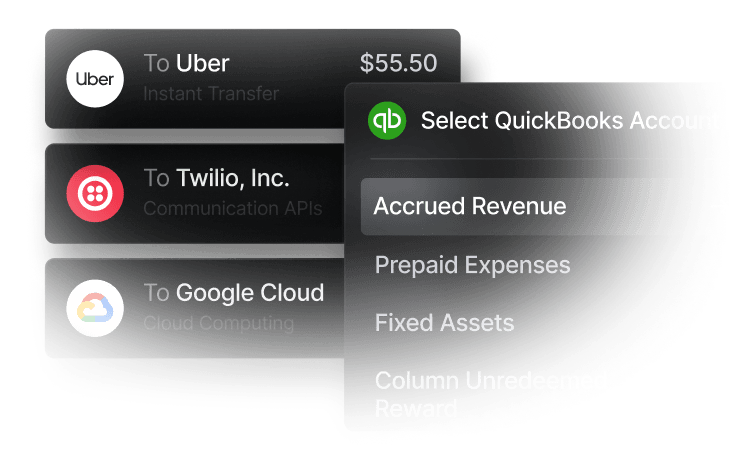

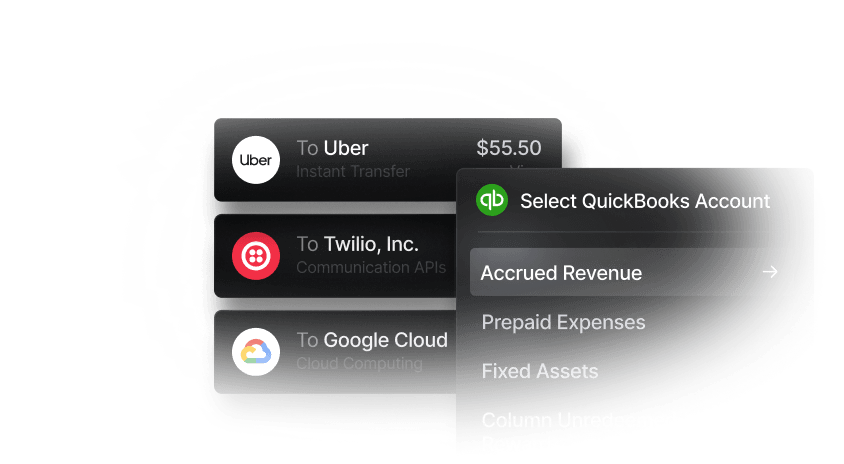

A corporate card program that doesn't integrate with the business's accounting software just leads to more manual transcription and mistakes. Slash integrates two-ways with QuickBooks Online Xero, and Sage Intacct, meaning transactions map to your general ledger automatically. Data is pushed from your accounting system to Slash and vice versa, making reconciliation easier and saving valuable time.

Virtual Card Capabilities

Virtual cards are digital corporate cards that feature unique card numbers for specific purposes. These cards can be scoped to a single vendor, a single transaction, or a specific budget, then cancelled or adjusted without affecting the company's primary payment credentials. The ability to issue virtual cards has become a key differentiator in corporate card programs. For businesses managing SaaS subscriptions, online advertising spend, or remote teams, virtual card issuance at scale is often a big deal.

Fees, Repayment Structure, and Eligibility

Corporate charge cards require full monthly balance payment, meaning you won’t have to worry about interest, but you can’t carry a balance. Corporate credit cards offer payment flexibility with the addition of interest for carried balances. Pricing structures vary: some platforms charge no platform fee and generate revenue through interchange, while others charge per-user monthly fees that scale with team size. Many charge card programs also require minimum cash balances and exclude sole proprietors. Understanding the total cost of the program and whether the business actually qualifies is a necessary first step in any evaluation.

Support for Global or Multi-Entity Spending

For businesses operating across multiple countries, currencies, or legal entities, the card program needs to handle multi-currency transactions, FX conversion, and entity-level reporting without requiring separate programs for each geography. Not all corporate card platforms are built for this: several US-focused platforms have limited international support, while platforms like Airwallex are designed specifically for multi-currency, cross-border spending. Businesses with distributed international teams should evaluate global capability early rather than discovering limitations after implementation.

Top Corporate Expense Card Providers

The right corporate expense card depends on how the business operates, where it's located, how it manages company spending, and what infrastructure it already has in place. Here are some popular options:

Slash

Best for: SMBs and online-first businesses that want banking, cards, and spend management in one platform.

- Corporate charge cards with no personal guarantee: The Slash Visa® Platinum Card is issued by Column N.A., Member FDIC, and underwritten based on business financials rather than personal credit.²

- Unlimited virtual and physical cards: Businesses can issue cards to employees, vendors, subscriptions, or departments with configurable limits, merchant restrictions, and approval controls.

- Built-in banking and treasury: Slash combines expense cards with business banking, bill pay, treasury accounts offering up to 3.8% annualized yield, and real-time payment rails including FedNow and RTP.⁶

- Native stablecoin support: Businesses can send, receive, and convert USDC and USDT directly within the platform across supported blockchains, useful for global contractor payouts and internet-native commerce.

- Automated oversight and accounting sync: Transactions sync with accounting platforms like QuickBooks, Xero, Sage Intacct, and NetSuite. AI-powered monitoring can flag unusual activity for review.

- Rewards on business spend: Eligible purchases can earn up to 2% cash back.

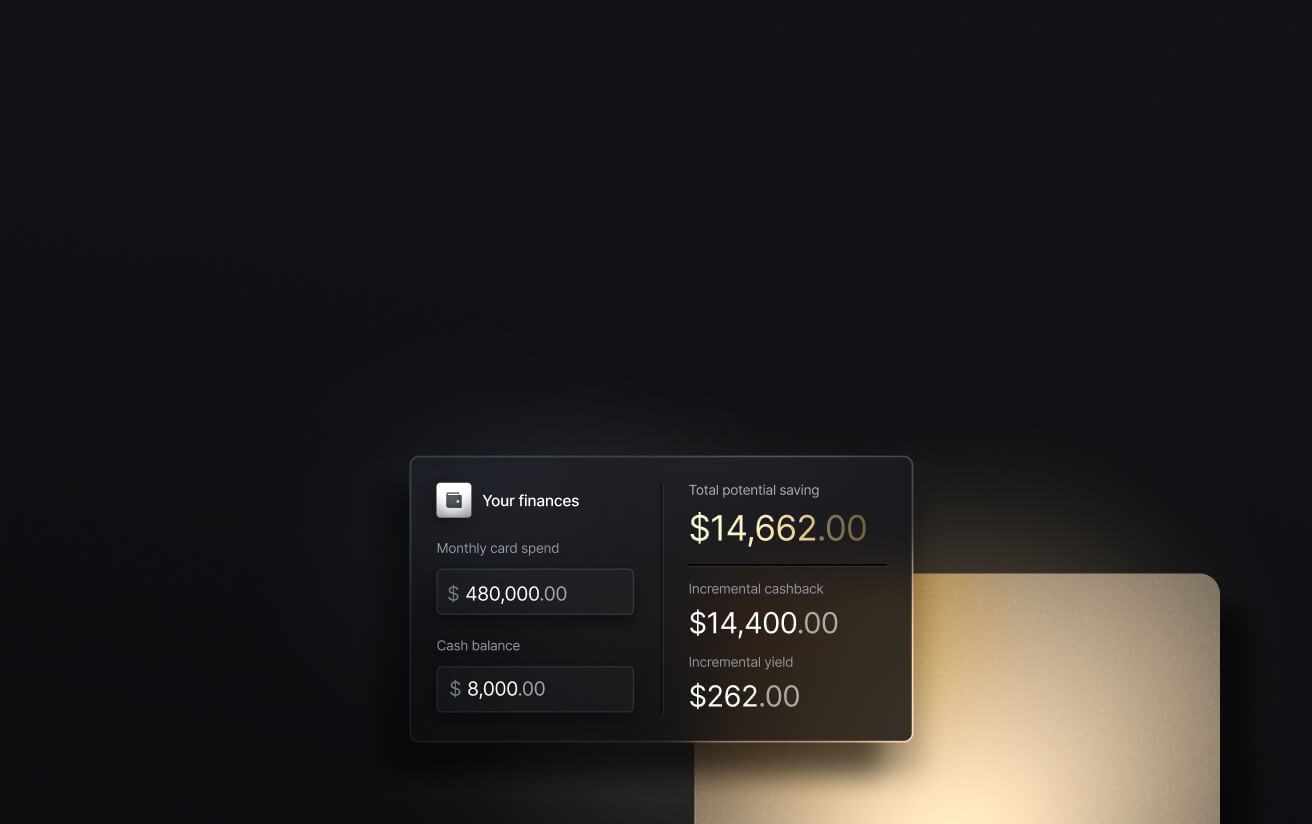

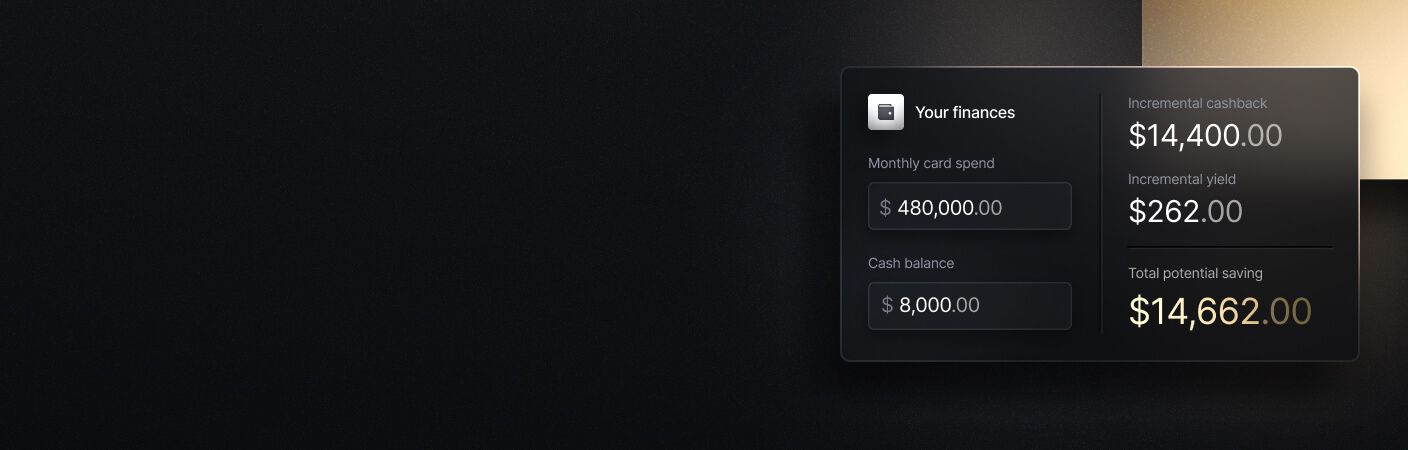

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Brex

Best for: Venture-backed startups and larger companies with complex spend management needs.

- High-limit corporate charge cards: Underwritten primarily on company cash balances, funding, and revenue rather than personal credit scores.

- Enterprise spend management tools: Includes travel booking, expense approvals, bill pay, reimbursements, and procurement workflows.

- Accounting and ERP integrations: Supports integrations with NetSuite, QuickBooks, Xero, and enterprise finance systems.

- Global support: Offers international reimbursements and multi-entity spend controls for larger organizations.

- Less accessible for smaller businesses: Brex is generally geared toward funded startups and larger companies with substantial operating balances.

Ramp

Best for: US-based incorporated businesses focused on spend controls and automation.

- Flat-rate cash back: Ramp offers 1.5% cash back on purchases with no annual fee.

- Expense automation features: Includes receipt matching, accounting categorization, approval workflows, and procurement management.

- ERP and finance integrations: Connects with systems like NetSuite, QuickBooks, and Sage Intacct.

- Eligibility requirements: Only available to corporations, LLCs, and LPs with at least $25,000 held in a US business bank account.

- Built around cost control: Strong fit for finance teams prioritizing policy enforcement and operational visibility.

Airwallex

Best for: Companies with significant international operations and multi-currency payment needs.

- Multi-currency business accounts: Supports balances in 20+ currencies and international transfers to 150+ countries.

- Competitive FX infrastructure: Built around international payments and currency conversion rather than domestic banking.

- Wallet-based spending model: Cards pull from pre-funded Airwallex balances instead of a revolving credit facility or charge line.

- Less optimized for domestic US operations: Best suited for globally distributed businesses rather than primarily domestic companies.

Pleo

Best for: European SMBs that want lightweight expense management and AP automation.

- Employee cards and reimbursements: Simplifies expense submission and receipt capture for distributed teams.

- Accounts payable automation: Includes invoice management and approval workflows alongside expense cards.

- Multi-currency support: Supports currency exchange and international employee spending within the platform.

- EU-focused platform: Designed primarily for European businesses and not generally available to US-only companies.

- Strong usability for smaller teams: Particularly popular with startups and SMBs looking to reduce manual finance admin work.

Optimize Corporate Expense Management with Slash

What separates the Slash card from many competitors is that it does not force businesses to choose between strong card controls, flexible global spending, and integrated expense management. The card is designed for businesses with distributed teams, online operations, or cross-border spend that need more visibility and control than traditional business cards typically provide.

The Slash Visa® Platinum Card can earn up to 2% cash back while giving businesses access to unlimited virtual and physical cards, customizable spending limits, and AI-powered transaction monitoring that can flag unusual activity and request supporting documentation automatically. For founders located outside the U.S., Slash also offers corporate cards tied to Global USD accounts, allowing businesses to spend globally in USD by off-ramping crypto at the point of sale.³

The broader Slash platform adds operational tooling around our cards to simplify how your business manages its finances, including:

- Accounting and ERP integrations: Easily sync transaction data with QuickBooks Online, Xero, Sage Intacct, and Netsuite for reconciliation and reporting.

- Built-in reimbursements: Employees can submit receipts and reimbursement requests directly inside the dashboard rather than through separate tools.

- Multiple payment rails: Businesses can manage card spend alongside same-day ACH, international wires to 180+ countries, RTP, and FedNow payments.

- Native stablecoin support: Hold and transact in USDC and USDT across supported blockchains for certain cross-border payment workflows.⁴

For businesses that want more than a standalone corporate card, Slash combines modern card controls with the banking and payment infrastructure needed to manage company spending in one place.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

How do companies qualify for corporate credit cards?

Companies generally qualify for corporate credit cards by demonstrating high annual revenue (often million or more), a strong business credit score, and a formal business structure like an LLC or corporation. Unlike small business cards, these are issued based on the company's financial strength rather than personal credit, and they are designed for organizations with high expenses and multiple employees.

What are the Easiest Business Credit Cards to Get? Top Picks and How to Get Yours Approved

What's the difference between points-based rewards programs and cash back rewards programs?

Cash back rewards programs offer cash back to the user on every business expense a cardholder makes with a corporate card. Meanwhile, points-based rewards programs also earn the cardholder rewards on each expense in the form of points, which are typically worth somewhere around $0.01. These can be worth more or less depending on the way the business needs to redeem them.

How Does Cash Back Work? Choosing the Right Credit Card Rewards Program

Ramp vs. Brex vs. Slash: Which Corporate Card is Best for Your Business?

How do virtual cards and sub-accounts work help expense tracking?

Virtual cards and sub-accounts improve expense tracking by offering real-time visibility, automated reconciliation, and granular control over spending. They can enable companies to assign unique 16-digit virtual numbers to specific vendors or employees, restricting usage and instantly logging transactions to simplify accounting.

What Is a Sub-Account? Key Benefits, Features, and Use Cases

How do receipts help expense reporting?

Receipts are essential for expense reporting as they provide verified, categorized proof of business-related purchases. They justify employee reimbursements, ensure compliance with IRS and company policies, and support audit defense. Receipts substantiate the date, amount, vendor, and business purpose of transactions. With solutions like Slash, receipts can also be scanned automatically with a phone in order to streamline expense management and reimbursements.

Read more from us