Accounts Receivable Process: From Invoice to Cash

The traditional accounts receivable process can seem stressful and inefficient — which is true. But it doesn’t have to be. Accounts receivable (AR) refers to the money a company is expected to receive at a future date and serves as a payment agreement between your business and your customers. However, converting the invoice into cash is easier said than done.

From chasing clients with payment reminder emails to physically writing card information and PDFs being sent back and forth, the accounts receivable process unnecessarily increases the risk of payments slipping through the cracks.

AR automation and integrated banking platforms like Slash can help shorten the accounts receivable cycle and make cash flow more predictable.¹ On your Slash dashboard, you can easily view all outstanding invoices, automate data entry, and send invoices at the click of a button. For your customers, Slash makes paying invoices easier by embedding payment links and supporting a wide range of payment methods.

What is the accounts receivable process?

The accounts receivable (AR) process cycle is the end-to-end journey of converting outstanding credit into cash. The cycle typically begins with an issued invoice that has been delivered but not yet paid. The process is then completed once the invoice has been settled and the full amount has been paid.

Accounts receivable is viewed as an asset on the balance sheet, but it does not affect cash flow until payments are collected. While an increase in accounts receivable can indicate sales growth, high AR balances can delay cash flow, as more money remains in unpaid invoices rather than in tangible bank accounts. In the long term, an increased AR can lead to a shortage of working capital and increase the risk of bad debt.

AR has payment terms that are typically agreed upon when a customer signs a new purchase order or contract. Common AR payment terms include:

- Current: requires immediate payment upon receipt of the invoice

- Net 10, Net 15, Net 30: net terms are widely used and specify the number of days a payment is due after the invoice date

- Net 60, Net 90, Net 125: extended payments are common in retail, apparel, and other companies that need more time to sell products before paying invoices

- End of Month (EOM) Terms: allow businesses to extend the payment due date to the end of the month in which the invoice is issued.

Step-by-step accounts receivable process flow

The accounts receivable process can appear daunting, especially for small-to mid-sized businesses, with the underlying fear of “what do we do if they don’t pay.” Following the best accounts receivable process can prevent cash flow obstacles and reduce the risk of bad debt. The AR process flow should be standardized and documented, even for a lean finance team, to reduce errors and speed up collections.

Below are six steps and recommendations for a smooth AR process:

1. Customer onboarding and credit approval

The first step is to set up a new customer profile in the AR system with the legal name, billing address, tax IDs, and primary contacts. Then detail a basic credit approval, tagging each customer with a low, medium, or high risk level. Strong upfront credit approval generally reduces the likelihood of late payments and disputes.

2. Making the sale and creating the invoice

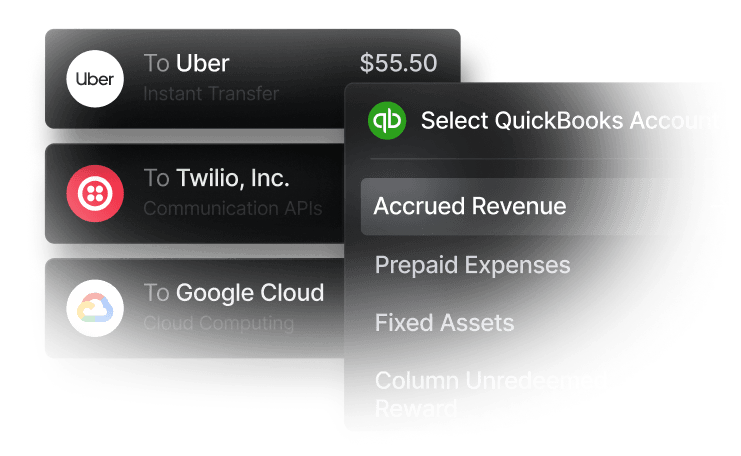

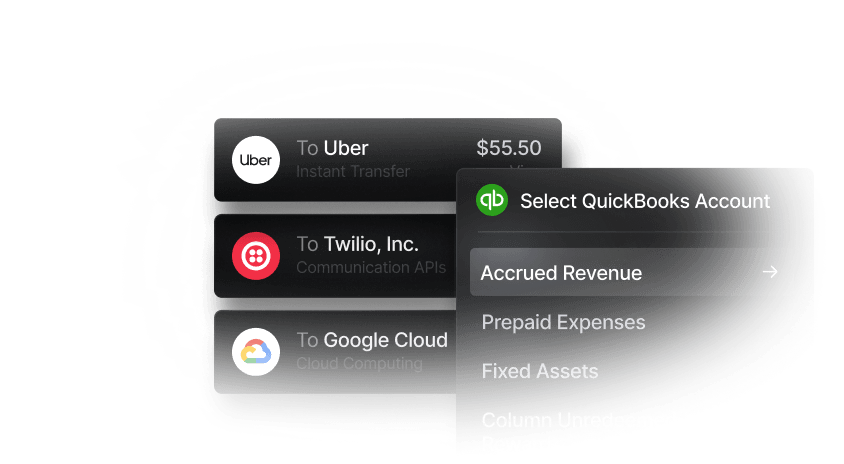

Once a sale has been concluded and a customer has sent a purchase order, sales or operations log the order so that finance can create an invoice recommended to be within 24 hours of a shipment, service delivery, or project milestone. AR-integrated invoicing tools like Slash make the invoice creation process easier by auto-populating your customer’s contacts banking details, which can help save time and reduce manual-entry errors.

3. Delivering the invoice and starting the clock

Days sales outstanding (DSO) is a metric that measures the average number of days it takes for a company to collect payment after a sale. Same-day electronic delivery is the best practice for shortening DSO by immediately starting the customer’s payment clock, eliminating the “we never saw the invoice” delays. From the Slash dashboard, you can quickly check payment status, review terms, and send automated reminders.

4. Recording the transaction and tracking open AR

Once an invoice is issued, the transaction should be recorded in your accounting system and added to the general ledger in accordance with double-entry accounting principles. The invoice should also be entered into the AR subledger with the customer name, invoice amount, currency, due date, and aging bucket. Organizations should daily, or at least weekly, review AR aging reports. Additionally, month-end cutoffs and reconciliation routines should be enforced to ensure that AR balances tie out to the balance sheet.

5. Collecting payments and managing the collections process

There is an assortment of payment methods commonly used today: ACH, wire transfer, credit card, check, or stablecoin. But not every company has the appropriate tools for every payment method. Slash supports each, including USDC and USDT invoice settlement and ACH debits for recurring charges.⁴ In addition, to streamline the payment process, Slash includes an embedded link in the invoices you send to your customers that leads directly to a secure payment landing page.

6. Dispute handling, cash application, and reconciliation

The most common reasons for disputes typically arise from product or service issues, pricing discrepancies, incorrect quantities, or missing approvals on the customer side. To minimize delays, organizations should set up a structured dispute resolution workflow; many businesses investigate within 3 business days and resolve the dispute within 10 to avoid stretching the AR cycle. At month-end, AR disputes should be recorded to ensure balances are accurate and up to date.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Key Accounts Receivable Metrics and Their Impact on Cash Flow

Key performance indicators (KPIs) aren’t intended to simply measure performance. KPIs can also help you strategize, manage, and improve cash flow performance. Below are some common accounts receivable KPIs to track:

- Days Sales Outstanding (DSO): as previously mentioned, this metric is crucial in AR as it reflects how efficiently a company collects cash from customers

- Average Days Delinquent (ADD): is used to determine how late, on average, customers pay their invoices. ADD provides additional insight into late payments that DSO can not provide alone

- AR turnover ratio: measures the number of times a business collects its average accounts receivable balance during a year to assess how efficiently a company is using its assets

- Aging distribution: provides a snapshot into cash flow health by categorizing unpaid customer invoices by the length of time they have been outstanding

- Bad debt percentage: the portion of receivables not expected to be collected.

Through effective monitoring of accounts receivable KPIs, businesses can improve their cash flow forecasting. Proactive measures to identify delayed payments and bottlenecks allow organizations to expedite collections, preventing a working capital shortage or high levels of bad debt.

Common Challenges in the Accounts Receivable Process

Many businesses still rely on manual accounts receivable processes that require significant time and oversight. When inefficiencies compound, businesses can experience slower cash flow, higher administrative costs, and reduced visibility into outstanding receivables. Below are some of the most common challenges companies face when managing accounts receivable:

Delayed invoicing and late payments

Delayed invoicing often leads directly to delayed payments. When invoices are not sent promptly after goods or services are delivered, payment timelines are pushed back and cash remains tied up in accounts receivable for longer. As overdue invoices accumulate, businesses may struggle to forecast cash flow accurately, manage working capital, and plan for upcoming expenses.

Inconsistent credit policies

Without standardized credit policies and payment terms, businesses can end up approving customers on a case-by-case basis and applying inconsistent collection practices. Unclear due dates, varying payment terms, and inconsistent credit reviews can create confusion for customers, increase payment delays, and expose the business to unnecessary credit risk.

Poor documentation

Accounts receivable depends on accurate records, but manual processes can lead to missing information, data entry mistakes, and invoice discrepancies. Errors such as incorrect pricing, outdated customer information, or missing purchase order details can trigger disputes and payment delays, requiring additional time and effort to resolve.

Ad hoc collections outreach

Many businesses rely on emails, phone calls, and spreadsheets to manage collections, making it difficult to consistently follow up on overdue invoices. Without a structured collections process, outstanding balances can be overlooked, collection cycles can lengthen, and the likelihood of bad debt increases.

Best Practices for an Efficient Accounts Receivable Cycle

Manual accounts receivable processes often rely on spreadsheets, email chains, and repetitive data entry, making them difficult to scale as invoice volume grows. The following best practices can help businesses collect payments faster, reduce administrative work, and improve cash flow visibility.

- Set clear credit policies: Establish standardized credit approval criteria, payment terms, and collections procedures before extending credit. Clear policies reduce credit risk and ensure customers know exactly when and how payment is expected.

- Invoice quickly: Send invoices as soon as goods are delivered or services are completed. The sooner an invoice is issued, the sooner the payment clock starts, helping reduce days sales outstanding (DSO).

- Automate reminders: Automated payment reminders ensure consistent follow-up without creating extra work for your AR team. Many late payments result from oversight rather than unwillingness to pay.

- Offer multiple payment options, including stablecoins: Giving customers flexibility to pay by ACH, card, wire transfer, or stablecoin reduces friction at checkout. Businesses with diverse customer bases may also benefit from faster settlement and lower cross-border payment costs.

- Embed payment links on every invoice: Customers are more likely to pay promptly when payment is only a click away. Removing unnecessary steps can meaningfully shorten collection cycles.

- Improve customer portals: Self-service portals allow customers to view invoices, payment history, and account balances without contacting your team. Greater transparency often leads to fewer disputes and faster payments.

- Encourage monthly AR review meetings: Regular reviews help identify overdue accounts, monitor collection trends, and surface cash flow risks before they become larger problems. Even a short monthly review can improve accountability across finance teams.

As your business grows, relying on spreadsheets and manually sending PDFs back and forth becomes increasingly inefficient. Integrated banking platforms like Slash allow businesses to create invoices, track outstanding balances, and manage collections from a single dashboard. By automating repetitive AR tasks and centralizing receivables data, businesses can reduce errors, improve collections efficiency, and maintain more predictable cash flow.

Streamline Your AR Process With Slash’s Invoicing and Cash Management

Slash is a modern business finance platform that helps companies streamline invoicing, payment collection, and cash flow management. By bringing accounts receivable workflows alongside banking and payments, Slash gives businesses greater visibility into outstanding invoices and incoming cash without relying on multiple disconnected tools.

With Slash, businesses can generate and send branded invoices directly from their dashboard, automatically populate customer information, and include payment instructions with every invoice. Once an invoice is sent, teams can track its status in real time, from draft and sent to paid or overdue. Automated reminders help maintain a consistent collections process by sending follow-ups before due dates, on due dates, and at scheduled intervals afterward.

From your customer’s side, Slash can help accelerate collections and minimize aging by embedding payment links in invoices. Your customers can easily pay their balances with the payment method of their choice: ACH credits and debits, wire transfers, USDC and USDT, credit card, or real-time payment. Giving your customers more options for how they pay can reduce the back-and-forth that slows AR down.

Here’s what else you get when you make the switch to Slash:

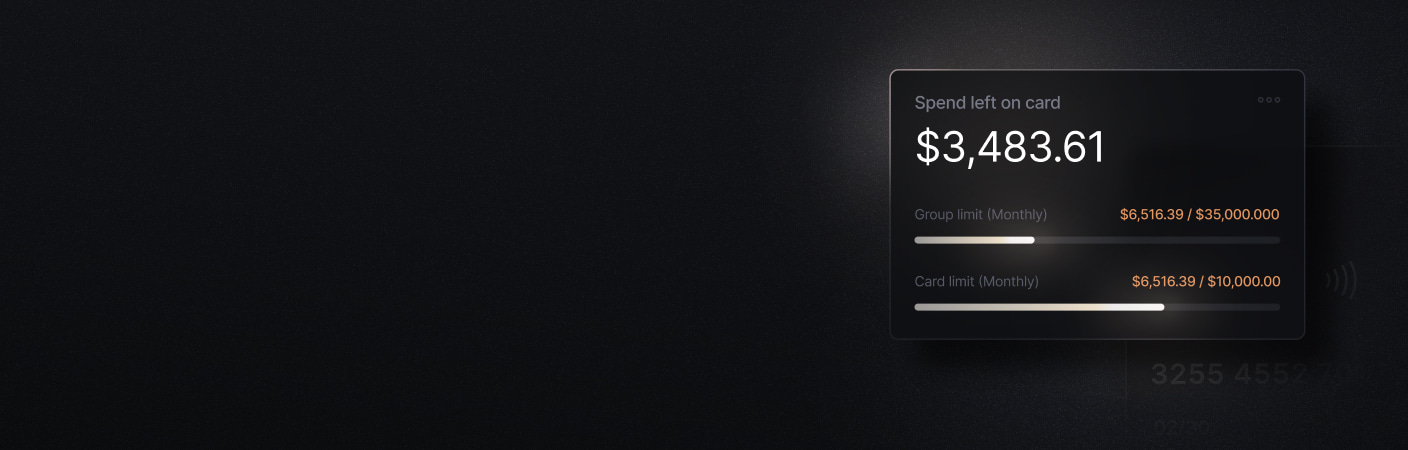

- Slash Visa® Platinum Card: Earn up to 2% cash back, set custom spending controls, and issue unlimited virtual cards for team expenses, vendor payments, and subscriptions.

- Expense management: Handle expense reporting with SMS receipt collection for Slash cards, simple reimbursement flows, and automatic accounting updates.

- Accounting integrations: Connect Slash with QuickBooks, Xero, Netsuite, or Sage Intacct so your transaction data flows straight into your books, already categorized and ready for reconciliation.

- Working capital financing: Access short-term financing with 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury accounts: Earn up to 3.80% annualized yield on idle funds through money market funds from BlackRock and Morgan Stanley, managed directly in your Slash account.⁶

The days of manually sending and tracking invoices are long gone, especially if you are a growing business. Platforms like Slash can help your accounts receivable processes run more smoothly. Sign up today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

FAQs

What is the difference between accounts receivable and accounts payable?

Accounts receivable represents money owed to a business by its customers for goods or services already delivered. Accounts payable represents money a business owes to its vendors, suppliers, or creditors for purchases it has made.

Top Accounts Payable Automation Solutions for Small Businesses in 2026

What are the 5 steps of the accounts receivable process?

The five core steps of the accounts receivable process are extending credit, issuing an invoice, tracking outstanding invoices, collecting payment, and reconciling the payment in accounting records. Some businesses also include collections management and credit reviews as part of the process.

How does accounts receivable affect cash flow?

Accounts receivable has a direct impact on cash flow because unpaid invoices represent revenue that has been earned but not yet received. The faster a business collects outstanding payments, the more cash it has available to cover operating expenses, invest in growth, and meet financial obligations.

How to Build a 13-Week Cash Flow Forecast

Read more from us