Are Business Credit Card Payments Tax Deductible? A Guide to What You Can Write Off

Maybe you’ve wondered this while filing your taxes: should you include your credit card payments, list every purchase individually, or both?

Here’s the short answer: you shouldn’t write off your credit card payments. The IRS treats paying off a credit card balance as settling a liability, not a deductible expense. Instead, deductions come from the individual purchases made on the card. But that’s where things start to get more complicated. Tracking and categorizing each credit card expense can be time-consuming, especially if you’re doing it manually. It also raises additional questions around how to handle fees, rewards, and bonuses.

In this guide, we’ll explain how to report credit card expenses correctly. You’ll learn which business expenses are deductible, which are not, how the IRS defines qualifying deductions, and how to make sure your reporting is accurate and complete before tax season.

We’ll also look at how the Slash Visa Platinum Card can simplify reporting your business expenses by automatically categorizing transactions and keeping your records organized.¹ With Slash, your receipts and purchase details are captured and synced directly with your ledger, which can cut down on manual work and last-minute fixes. On top of that, you can earn up to 2% cash back on your spending, so you’re not just staying organized, you’re getting more value from every expense, too.

Payments vs. expenses: Understanding the key differences

To understand why you can’t deduct your credit card payments, it helps to separate how the IRS treats payments versus expenses. An expense is recognized at the moment you incur it, which is when you make a purchase for your business. A payment, on the other hand, is simply how you settle that obligation. When you use a credit card, the expense occurs at the time of purchase, not when you later pay off the balance.

For example, if you spend $500 on printer ink, that purchase may qualify as a deductible business expense. Paying off that $500 balance later does not create a second deduction, since no new expense has occurred; the IRS only allows you to deduct the original purchase.

To determine whether a purchase qualifies for a deduction, the IRS uses the “ordinary and necessary” standard. An ordinary expense is one that is common and accepted in your industry. A necessary expense is one that is helpful and appropriate for running your business. While the expense does not need to be essential, it should have a clear business purpose.

From there, expenses generally fall into one of three broad categories. Understanding these can help guide how you claim deductions:

- Business expenses:Costs that are ordinary and necessary for running your business, such as supplies, software, or services. These are generally deductible in the year they are incurred.

- Capital expenses:Costs for assets that provide value over more than one year, such as equipment, vehicles, or property. These are not typically deducted all at once, but instead depreciated over time, though some may qualify for accelerated deductions.

- Personal expenses:Costs related to personal, living, or family use. These are not deductible because they are not connected to operating your business.

Which business credit card expenses are tax deductible?

After separating business expenses from personal and capital costs, the next step is determining how each business expense is treated. Some are fully deductible, while others are only partially deductible or require allocation. Here’s an overview:

Fully deductible business expenses

Fully deductible expenses are costs you can write off at 100% in the year they are incurred, as long as they meet the IRS standard for being ordinary and necessary. These are typically straightforward operating expenses that are directly tied to running your business.

Common examples include office supplies, software subscriptions, professional services like legal or accounting support, and marketing costs such as ads or website hosting. Other fully deductible expenses can include rent, utilities, insurance, and certain types of equipment, depending on how they are classified.

There are many fully deductible card-related costs besides the purchases you make with them. If your card is used exclusively for your business, most of the associated fees are fully deductible. This includes annual fees, foreign transaction fees, and balance transfer fees. Interest on business credit card balances is also generally deductible. However, late payment fees and penalties are not deductible, since the IRS treats them as avoidable costs rather than necessary business expenses.

Partially deductible business expenses

Partially deductible expenses are costs where only a portion of the total can be written off. To qualify, the expense must still meet the ordinary and necessary standard, and it must have a clear business purpose.

This includes meals with clients, team meals tied to business activity, and meals during business travel. In most of these cases, only 50% of the cost is deductible. Importantly, business meals are a separate expense from entertainment. Entertainment expenses, such as taking a client to a sporting event or concert, are not deductible under current tax rules, even if business is discussed.

There are a couple edge cases to be aware of. For example, company-wide events or employee recreation may still be fully deductible if they qualify as employee benefits. Business gifts fall into a similar category of limited deductions, where you can generally deduct up to $25 per recipient per year, as long as the gift is tied to your business.

Mixed-use expenses

Mixed-use expenses are costs tied to both business and personal use. In these cases, only the business portion of the expense is deductible, and you are responsible for calculating and supporting that allocation.

For example, if you use your phone 30% for business and 70% for personal use, you can only deduct 30% of your phone bill. The same principle applies to expenses like vehicles, home offices, and certain types of equipment.

Since mixed-use deductions are based on usage, the IRS expects you to justify your allocation. Keeping clear records of how you determined the business portion will help support your deductions if they’re ever reviewed.

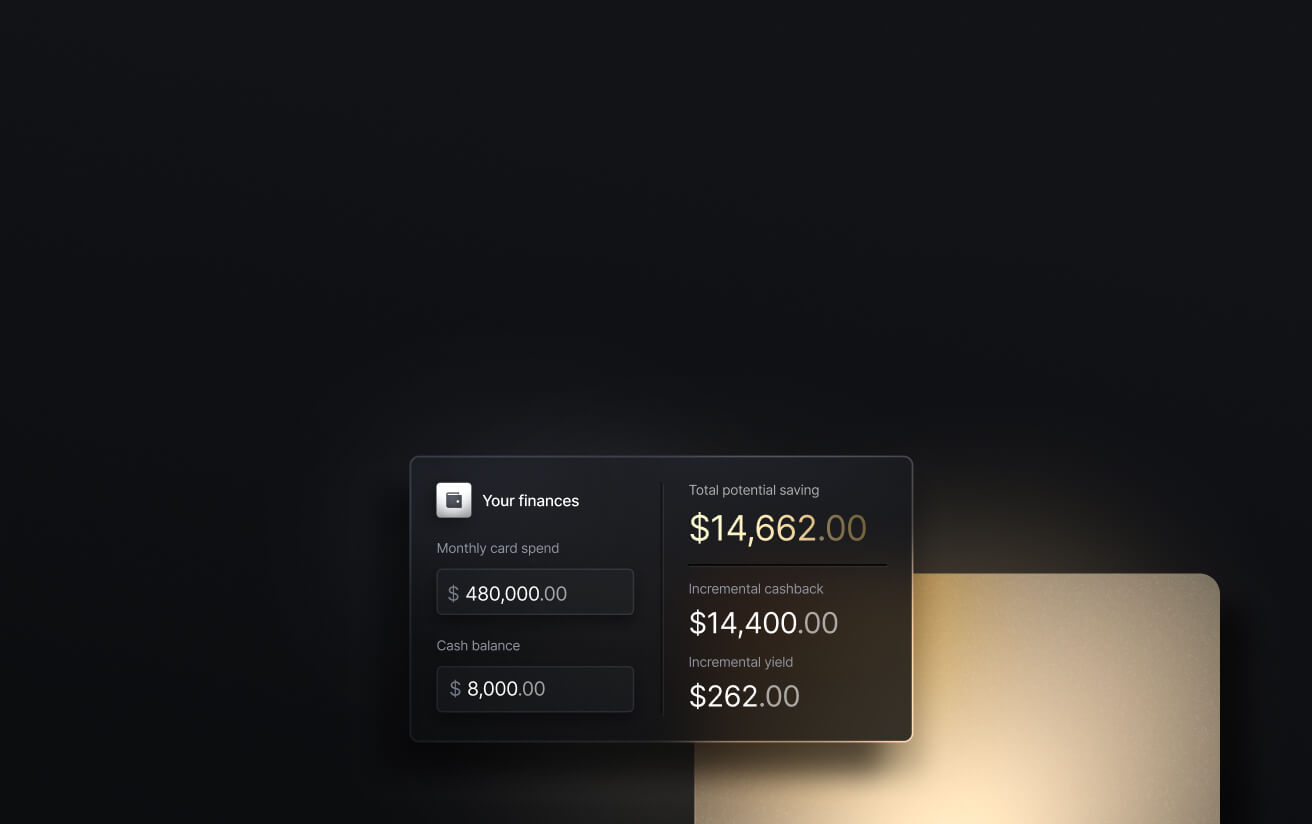

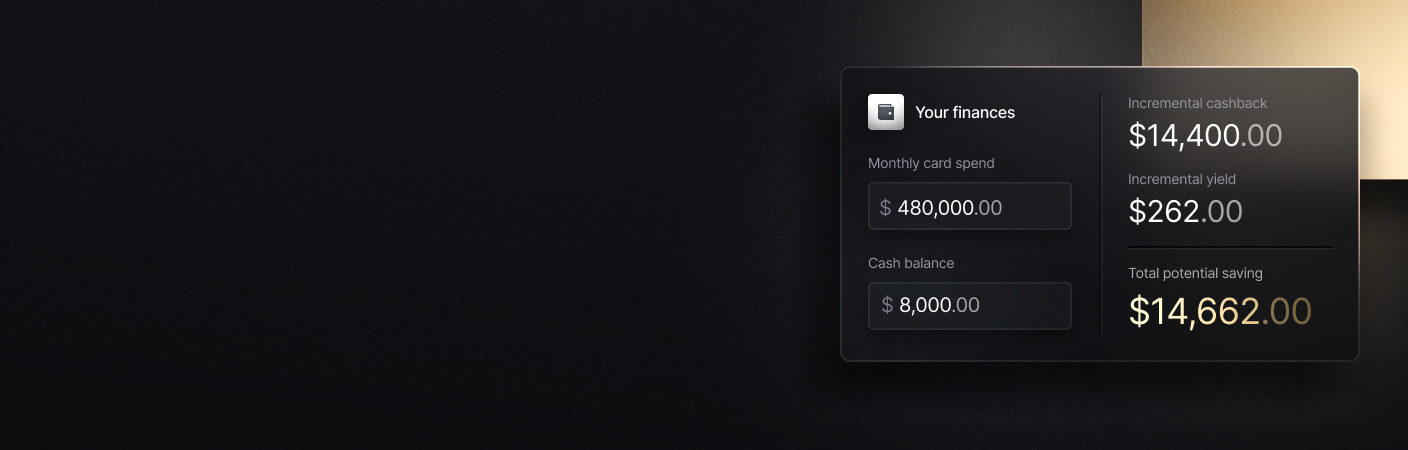

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Which business credit card expenses are not tax deductible?

Not every expense you put on a business credit card qualifies for a deduction. The IRS focuses on the purpose of the purchase, not the payment method. If an expense is not directly related to running your business or does not meet the “ordinary and necessary” standard, it cannot be written off, even if it was charged to a business card. Common non-deductible expenses include:

- Personal expenses:Any discretionary purchases for living, lifestyle, or family use are not deductible, even if they are accidentally charged to a business credit card.

- Commuting costs:Daily travel between your home and your primary place of work is considered a personal expense. This includes gas, public transit, and parking for your regular commute.

- Fines & penalties:Government-imposed fines, penalties, and late fees are not deductible. This includes things like parking tickets, tax penalties, and late payment fees on credit cards.

- Political contributions:Donations to political campaigns, parties, or lobbying groups are not deductible as business expenses.

- Entertainment expenses:Most entertainment costs, such as sporting events, concerts, or golf outings with clients, are not deductible under current IRS rules.

Lastly, capital expenses can be a source of confusion. While they are typically not immediately deductible in full, they are not disallowed either. These are large purchases (equipment, vehicles, property) that provide value to your business over multiple years. Instead of being deducted all at once, they are typically capitalized and written off over time through depreciation. In some cases, businesses may qualify for accelerated deductions, but they cannot treat these purchases as standard expenses without applying the appropriate rules.

How to claim deductions by entity type

How you claim business expense deductions depends on how your business is structured. While the underlying rules around what qualifies as deductible remain the same, the forms you file and how those deductions flow through to your personal or business tax return will differ by entity type. Here’s some general guidance for each U.S. business entity structure:

Sole proprietorship

Sole proprietors report business income and expenses on Schedule C (Form 1040). You’ll list your total income and deduct eligible expenses directly on this form, which then passes through to your personal tax return. Keeping clean, categorized records is especially important for sole proprietors since there is no separation between the business and the individual for tax purposes.

Single member LLCs

Single-member LLCs are typically treated as disregarded entities for tax purposes, meaning they are taxed the same way as sole proprietorships by default. You’ll usually file a Schedule C along with your Form 1040. The main difference is legal, not tax-related, but maintaining separate business records and accounts is still important for both compliance and clarity.

Partnerships and multi-member LLCs

Partnerships and multi-member LLCs file Form 1065 to report income and expenses at the entity level. The business itself does not pay income tax; instead, profits and deductions are passed through to each partner via a Schedule K-1. From there, each partner then reports their share on their individual tax return.

S-corporations

S-corporations also use a pass-through structure. They file Form 1120-S to report income, deductions, and credits. Shareholders receive a Schedule K-1 that reflects their portion of the business’s activity, which they report on their personal returns. One key consideration is that owners who work in the business must pay themselves a reasonable salary, which is treated separately from distributions.

C-corporations

C-corporations file Form 1120 and are taxed as separate entities. The corporation claims deductions directly against its income and pays corporate tax on any remaining profit. Unlike pass-through entities, deductions do not flow to individual owners. This structure can offer more flexibility in how expenses and benefits are handled, but it also introduces the potential for double taxation when profits are distributed as dividends.

Best practices for maximizing your business’s tax deductions

Deductions aren’t just a fixed reduction to your tax bill, they can be optimized. With the right approach, your business can capture more value from the same set of expenses. Below are some common best practices:

- Choose the right business structure:Your entity type affects how deductions are applied and how much you ultimately keep. Consider factors like your current revenue, growth plans, and administrative complexity when deciding between a sole proprietorship, LLC, or corporation.

- Understand the Qualified Business Income (QBI) deduction:Many pass-through entities may qualify for up to a 20% deduction on qualified business income. Eligibility depends on your income level, industry, and how your business is structured, so it’s important to evaluate whether you qualify.

- Plan for self-employment taxes:If you operate as a sole proprietor or in a pass-through entity, you may be subject to self-employment tax. Structuring your income properly, especially in an S-corp, can help optimize how much you pay in payroll versus distributions.

- Account for state and local tax rules:Deduction rules can vary by state, and some states do not follow federal treatment for certain expenses or credits. Make sure you understand how your state handles business deductions so there are no surprises at filing time.

- Maintain consistent, accurate categorization:The more organized your books are throughout the year, the easier it will be to claim deductions confidently. With the Slash Card, you can categorize expenses as they occur, keep receipts and supporting documentation organized, and ensure everything is properly recorded in your accounting system.

Maximize the value of your business’s deductions with Slash

Staying on top of your deductions comes down to how well you track and organize expenses throughout the year. Slash simplifies expense tracking by automatically capturing transaction details and keeping your records up to date.

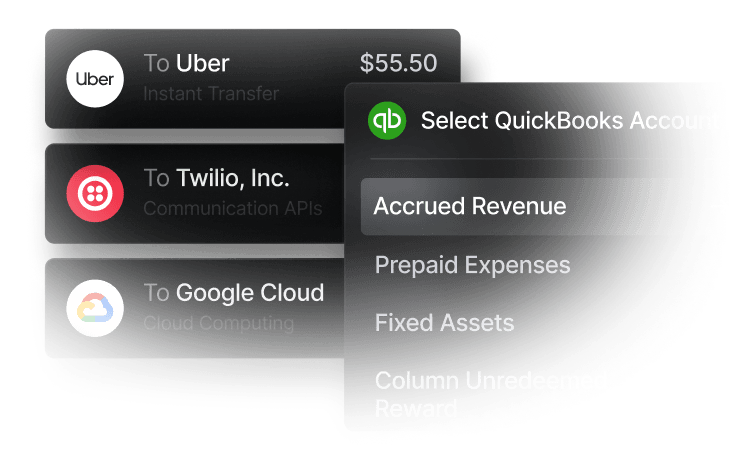

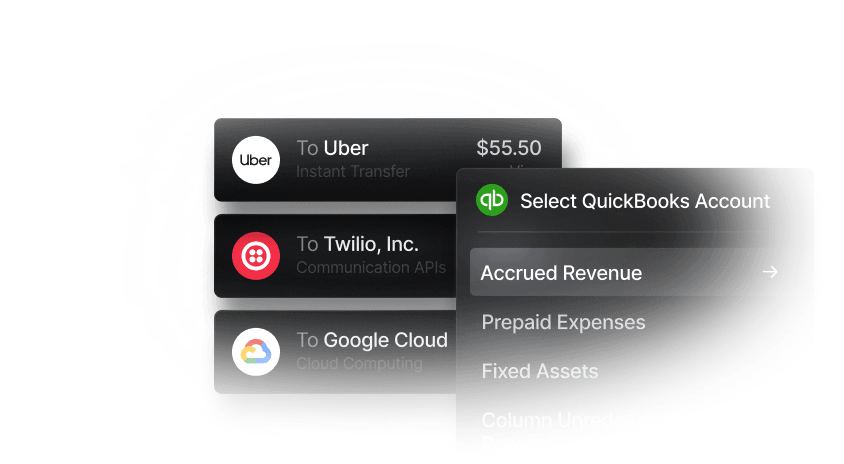

Instead of sorting through statements or reconciling at the end of the month, transactions are categorized as they happen, with receipts and purchase data attached. When it’s time to close your books or file taxes, you can export clean, enriched data directly into QuickBooks, Xero, or Sage Intacct, reducing manual work and improving accuracy.

Slash also helps you get more value from every dollar you spend. With the Slash Visa Platinum Card, you can earn up to 2% cash back, while built-in controls and real-time visibility give you a clearer view of your cash flow. You can set spend limits, track usage across teams, and organize funds to keep your finances structured.

With Slash, you get a more controlled and transparent system for managing expenses and maximizing deductions. Additional features include:

- AP/AR management tools:Create invoices using saved contact and banking details, and collect payments through built-in payment links. Easily track invoice payment status so you always know what’s outstanding and what’s been paid.

- Diverse payment methods:Support for global ACH, international wires to 180+ countries, and real-time rails like RTP and FedNow. Hold, send, and receive USD-pegged stablecoins like USDT and USDC for faster, lower-cost international payments.⁴

- Working capital financing:Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help manage cash flow gaps.⁵

- High-yield treasury accounts:Earn up to 3.83% annualized yield on idle funds through money market investments from BlackRock and Morgan Stanley.⁶

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

This guide is for educational purposes. The information presented should not be considered legal or tax advice. Tax rules can vary based on your business structure, state of operation, and individual circumstances. For guidance specific to your situation, consult a qualified tax professional or accountant.

Frequently asked questions

Can you write off credit card debt?

No, you cannot write off credit card debt. The IRS only allows deductions for the underlying business expenses, not the act of carrying or repaying a balance.

What happens if I accidentally charge personal expenses?

Personal expenses are not deductible, even if they are charged to a business credit card. You should separate and exclude them from your books, and ideally reimburse the business to keep records accurate.

How to Handle an Employee Who Uses a Company Card for Personal Use

How long should I keep credit card statements for taxes?

It’s generally recommended to keep credit card statements and supporting documentation for at least three years, which aligns with the IRS audit window. In some cases, keeping records for up to seven years can provide additional protection.

The Complete Guide to LLC Expenses and Tax Deductions

Are business credit card rewards taxable?

In most cases, credit card rewards are not taxable because they are treated as rebates or discounts on purchases. However, rewards that are earned without a corresponding purchase, such as sign-up bonuses, may be considered taxable income.

Business Credit Card Rewards Tax Guide: What You Should Know in 2026