Stablecoin Payment Fees Explained: Network Fees, Platform Fees, and FX Savings

Stablecoin Payment Fees Explained: Network Fees, Platform Fees, and FX Savings

If you’re part of a team that routinely pays vendors, contractors, or business partners located overseas, then you probably know how much money disappears into fees before a transfer settles. Correspondent bank charges and FX spreads were just the costs of doing business. That was true, and then crypto came along.

Between October 2024 and October 2025, $9 trillion in stablecoins were moved globally, up 87% year over year, according to 2025’s State of Crypto Report from a16z. Unlike a cryptocurrency like Bitcoin, stablecoins aren’t speculative investments, so those figures don’t come from trading activity. That $9 trillion is largely real businesses moving real money. If you’re considering using stablecoins for your business’s outbound payments, there are some things to know about before diving in.

The total cost of a stablecoin transfer includes on-chain gas fees, platform or processor fees, FX conversion at the off-ramp, and more. While these fees are often lower than a traditional bank transfer, it’s still important to know what they are, where they come from, and the best practices for minimizing fees.

This article breaks down the full fee structure behind stablecoin payments, along with some introductory information about how the blockchain really works. And if you’re a business owner looking to add crypto capabilities to your financial stack, consider Slash, a business banking platform that natively supports sending and receiving USDC and USDT stablecoins by converting your cash into crypto, a process called on- and off-ramping.¹,⁴ Slash’s built-in crypto on/off ramps connect your accounts to the blockchain without the complexity of managing a separate exchange platform or your own wallet, giving you access to the low fees and fast settlement of the blockchain.

Glossary

Here are some key terms about cryptocurrency and the blockchain that will be helpful to know throughout this guide:

- Cryptocurrency: A form of digital currency that can be used for both electronic payments and as a store of value. Cryptocurrencies use cryptography to secure transactions and record them on a public ledger.

- Fiat currency: Federally-issued money that is declared legal tender, such as the U.S. dollar or the euro. The value of fiat currencies comes from their issuing government and central bank instead of a physical commodity like gold.

- Blockchain: A decentralized ledger that records and verifies transactions across a network of computers rather than relying on a centralized authority. Once a transaction is confirmed and added to the blockchain, it becomes very difficult to alter. This structure allows payments to be verified and settled without relying on an intermediary like a correspondent bank.

- On/off ramps: Services or tools that allow users to convert cryptocurrency into fiat and vice versa.

- Crypto wallet: A digital tool that securely stores a user’s cryptographic keys, granting them access to their cryptocurrencies. Despite the name, it doesn’t technically hold coins; the funds live on a blockchain network.

- Validator: A specialized participant (or computer node) on a blockchain network that verifies the authenticity of a transfer and records it to the public ledger.

- Gas fees: Also known as network fees, these are the small fees networks charge per payment.

What Are Stablecoins?

A stablecoin is a digital token designed to hold a stable value, typically by maintaining a 1:1 peg to a fiat currency like the U.S. dollar. When businesses use stablecoins for payments, they’re almost always working with fiat-backed stablecoins like USDC (Circle) and USDT (Tether), which are backed by U.S. dollars and Treasury reserves. Those two tokens alone account for more than 90% of total stablecoin supply.

With crypto, payments settle in the recipient’s wallet in seconds. There are no bank cutoffs, batch windows, or correspondent banks to route through, which means minimal friction and little to no processing fees. The main on-chain cost is a gas fee, a small charge that offsets the computational power required to process the transaction on the blockchain. Gas fees generally range from a few cents to $2, even during peak trading hours. On Slash, you don’t pay these directly; our infrastructure partner Bridge covers them.

One important caveat: confirmed crypto transactions are irreversible. There are no chargebacks or recalls, so it’s important to verify recipient details before sending. Stablecoin payments also require both parties to have a compatible crypto wallet. As adoption grows, that obstacle will likely start to fade away.

How Stablecoin Payment Fees Work

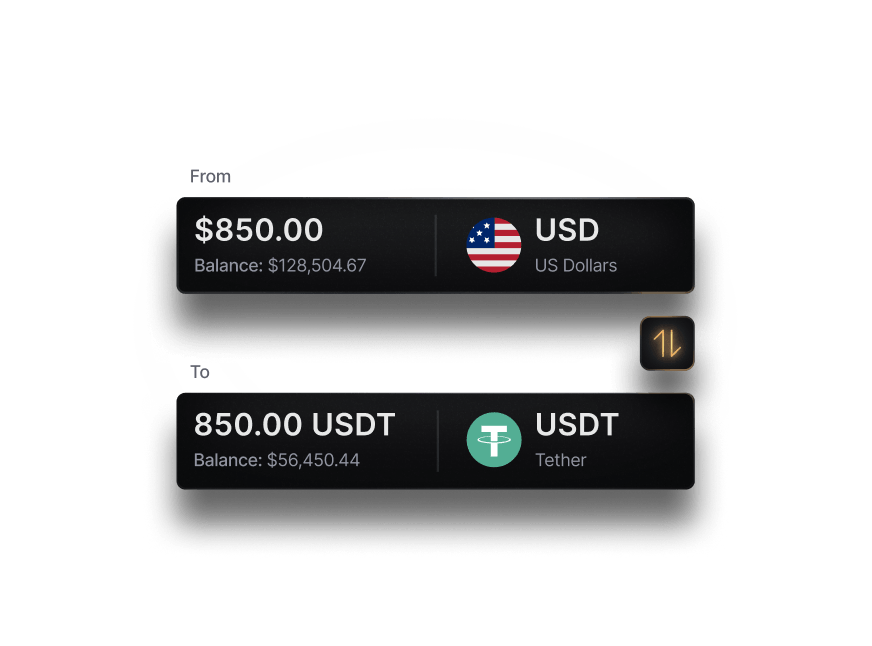

The main draw of using stablecoins is their relatively low fees, especially for outbound international payments. On Slash, the fees you pay are the on- and off-ramp fees: a charge when you fund your account and a charge when you pay from it. The layering of fees into a cryptocurrency transfer is often called the “fee stack,” since it can involve charges from a couple of different sources.

Consider a business funding its Slash account and then sending $10,000 of USDC to a contractor in France. Here’s where the fees show up:

- On-ramp fee (pay-in): Slash charges up to 1.5% to convert dollars into USDC when you fund your account.

- Off-ramp fee (pay-out): Slash charges up to 1.5% when you pay out from your account. There are no separate gas or network fees for Slash users.

- Recipient conversion: If the contractor converts USDC to euros, their own wallet or exchange applies a fee, usually 0.5–1.5%, plus any FX spread on the receiving side.

An international wire is often priced at a flat fee, which keeps it practical for large payments in the thousands of dollars. The percentage-based stablecoin fee stack tends to favor smaller, recurring payments.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Network Fees: How Blockchain Gas and Chain Choice Shape Your Costs

Network fees are charges paid to validators, the computers that process and record transactions on the blockchain. One thing that often catches people off guard when they try dabbling in crypto: network fees often can’t be paid in the cryptocurrency of your choosing. They’re paid in the native token of whatever blockchain you’re using. For instance, if you’re using the Solana network, then you’ll need a small amount of SOL in a crypto wallet to pay for the fees.

This is a point where newcomers to crypto might find themselves a little overwhelmed. To send stablecoins on-chain, you need a crypto wallet. That means that if you want to send USDC on the Solana chain, you’ll end up needing to monitor two balances instead of one and occasionally topping up your fee token when it runs low. If your SOL balance hits zero, your transaction won’t go through, even if your USDC balance is fine. Slash abstracts away this complexity; our crypto infrastructure partner, Bridge, handles gas fees for you whenever you on-ramp into USDC or USDT.

If you opt to manage your own crypto wallet for payments, however, you’ll find that some blockchain networks cost a little more than others. Here’s some of the typical network costs and settlement times among popular blockchains:

Ethereum fees work a bit differently than most other blockchains. Every transaction has a base fee set by the network, plus an optional priority fee if you want faster confirmation. When the network gets congested, both can spike, which can make Ethereum one of the pricier options. It’s still the dominant network for stablecoins, though, handling around 65% of USDC volume and 48% of USDT, per FXC Intelligence.

If your business runs regular contractor payroll or vendor payment cycles, batch transactions can be a good cost saver. Sending one aggregated transaction that distributes to 50 recipients in a single on-chain operation costs roughly the same in gas as a single payment, rather than 50 separate transactions. Not all networks support batch processing, however, so do some research beforehand if you intend on trying batches out.

Foreign Exchange Costs in Cross-Border Payments

Even though USDC is pegged 1:1 to the U.S. dollar, recipients getting paid in a different currency will need to convert it at some point. That conversion, the off-ramp on the recipient’s side, is where FX costs enter the picture.

Take a $2,000 payment from the U.S. to Colombia via USDC on Solana. A Slash sender pays no network fee on the transfer; Bridge covers it (a self-custody user would see around $0.02). When the recipient in Colombia converts into pesos through a local exchange or off-ramp provider, it’ll apply its own spread. Converting from stablecoin to fiat typically costs between 0.5% and 3%, though this varies by corridor and provider.

The regulatory picture also varies by country. Nigeria has introduced a formal framework under its Investment and Securities Act 2025, requiring stablecoin issuers to obtain licenses and meet AML and KYC standards. Brazil has similarly imposed detailed rules through BCB Resolution No. 520/2025, including transaction limits, reporting requirements, and restrictions on algorithmic stablecoins. These frameworks don’t prohibit stablecoin payments, but they do add compliance layers that affect which off-ramp providers operate locally and how.

If the recipient is comfortable holding USDC, though, they can skip the conversion entirely. No off-ramp on their end, no FX spread, and no conversion cost to deal with.

Comparing Stablecoin Payments vs. Wires, Cards, and PSPs

Though it may seem like stablecoins are a minefield of fees, their fee stack still comes in lower than traditional bank rails for many payments. This can be especially true of international payments or smaller B2B transfers. Here’s a breakdown of several of the most common cross-border payment methods and their typical fees:

Outside of their lower costs for smaller or recurring cross-border payments, it’s worth bearing in mind that the blockchain comes with other benefits, too. Stablecoin payments can be sent anytime: at midnight, on weekends, and on federal holidays where supported. They also settle in a matter of minutes, while a wire on the SWIFT network can take anywhere from one to several business days depending on the corridor and correspondent bank relationships involved. For all these reasons, and due to the strengthening platforms supporting access to the blockchain, stablecoins have seen a meteoric rise in popularity for everyday business transfers.

How Slash Supports Stablecoin Payments

Even though stablecoins are becoming more common, not everyone is accustomed to accessing the blockchain or sending crypto. The biggest barrier to entry is often the technical complexity, but Slash has abstracted it away.

Slash supports USDC and USDT payments across 8 blockchains, but you don’t need to speak crypto to use it. All you see is a dollar amount, a breakdown of applicable fees, and a QR code for sending and receiving. Our infrastructure provider, Bridge, covers gas fees automatically, so there’s no need to maintain a separate wallet for your gas fee tokens. We also offer the Global USD Account, a business account available in over 130 countries that doesn’t require a U.S. entity.³ It’s backed by USDSL, our proprietary USD-pegged stablecoin backed by U.S. Treasury bills and USDC, and comes with Global Cards that off-ramp at the point of sale so you can spend anywhere Visa is accepted.

Along with our built-in stablecoin on/off ramps, Slash centralizes just about every payment method you could need on one business banking platform. Whether you’re receiving funds via the blockchain or international wire, users can track a transaction’s status in real time on our integrated dashboard. Outside of the world of crypto, Slash also offers features like:

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. Users can also earn up to 2% cash back on business spend.

- AI-powered finance: Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review cash flow, and much more.

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, NetSuite, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Invoicing: With Slash’s invoicing and bill pay features, users can send customized invoices, collect payments, and manage vendor bills all in the same place.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

If you’re paying high fees and waiting days to send money across borders, Slash can get you started with stablecoins today.

Frequently Asked Questions

What’s the difference between USDC and USDT?

For most use cases, USDC and USDT are nearly identical. However, this isn’t the case when making payments to Europe. USDC is compliant with the European Union’s Markets in Crypto-Assets (MiCA) regulations, which took effect in June 2024, while USDT is not. The MiCA regulation is the EU’s legal framework that enforces uniform rules for crypto-asset issuers and service providers (CASPs) across the EU, and it’s one example of how regulatory bodies set rules for stablecoin issuers in different regions.

Why is Ethereum more expensive?

Ethereum is more expensive because it sometimes adds an additional network fee during high activity periods.

Are stablecoin payments always cheaper than wire payments?

Not always. Since stablecoin fees are mostly percentage-based, and SWIFT fees aren’t, wire transfers can become cheaper for high-value transactions.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

What’s the difference between USDC and USDT?

For most use cases, USDC and USDT are nearly identical. However, this isn’t the case when making payments to Europe. USDC is compliant with the European Union’s Markets in Crypto-Assets (MiCA) regulations, which took effect in June 2024, while USDT is not. The MiCA regulation is the EU’s legal framework that enforces uniform rules for crypto-asset issuers and service providers (CASPs) across the EU, and it’s one example of how regulatory bodies set rules for stablecoin issuers in different regions.

What Is USDC? Payments, Uses, and How It Works

Why is Ethereum more expensive?

Ethereum is more expensive because it sometimes tacks on an additional network fee during high activity periods.

Are stablecoin payments always cheaper than wire payments?

Not always. Since stablecoin fees are mostly percentage-based, and SWIFT fees aren’t, wire transfers can become cheaper for high-value transactions.

What Is a USDT Payment? How It Works and Why Businesses Use It