Best Free Business Accounts for Small Businesses

Opening a business bank account is one of the first real steps a small business takes. It separates your personal money from the company's, makes bookkeeping and taxes far less painful, and gives the business its own financial footing. It's also where a lot of owners run into their first surprise: many business accounts charge a monthly fee just to stay open.

That fee doesn't always buy much. Plenty of free business accounts match the features of paid ones, and for anyone sorting out business finances for the first time, a zero-monthly-fee account is a sensible place to start.

A quick note on "free." We mean the monthly maintenance fee that most business accounts charge. Other activities can still cost you, including wire transfers, cash deposits over a monthly limit, outgoing international payments, and out-of-network ATM withdrawals.

Every account below either skips the monthly maintenance fee or makes it easy to waive. What you pay overall comes down to how you use the account. This article sorts the best free business accounts by who they suit and covers what to weigh before you commit. We'll also look at Slash, a free-to-open business account that includes a financial dashboard, accounting integrations, bill pay, an AI assistant, and more.¹

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What to Look for in a Free Business Account

The lack of a monthly fee is a good start, but it’s never the whole story. The right account often depends on how your company actually uses and moves its money. Here are some of the features you should evaluate:

Monthly Fees and Minimum Balance Requirements

There’s a difference between "free" and "conditionally free". Some accounts have no monthly fee under any circumstances, while others waive the fee when the business maintains a minimum daily balance. These minimums are often $2,000 or more depending on the bank. Many businesses are able to maintain these balances, but startups with uneven liquidity may end up incurring unexpected fees.

Transaction Limits and Payment Capabilities

Many neobanks and digital-first platforms support electronic transactions like ACH, business debit card purchases, and bill payments with no per-transaction fees. Business checking accounts found among traditional banks may impose limits on non-electronic transactions (teller deposits, written checks) before per-item fees apply. If your small business moves money frequently, it’s wise to take a look at their ACH and wire availability and whether or not they’re free.

Digital Banking Tools and Integrations

Accounting integrations, expense tracking, multi-user access with different permission levels, and mobile check deposit are important abilities for a modern business account to have. The quality of these integrations is also a key factor, as a sync that requires manual intervention and only pushes data in one direction creates unnecessary work. Slash, for instance, connects with QuickBooks Online, Sage Intacct, NetSuite, and Xero, allowing data to be pushed and pulled in both directions.

Many businesses have teams that need to access the account at different permission levels, such as a bookkeeper who can categorize but not initiate payments or an employee who can submit expenses but not approve them. For these use cases, access controls are a strength that some business checking accounts don’t support.

Branch Access, ATM Networks, and Cash Deposits

One advantage that traditional bank accounts come with is their in-person access. Businesses like retail stores and restaurants that handle physical cash may want to prioritize branch access and cash deposit capabilities. Digital-only platforms generally can't accept cash deposits directly, requiring a workaround or the use of participating Allpoint ATMs. Businesses that handle cash every day will probably find this inconvenient. Traditional bank accounts handle cash more naturally and typically include a monthly cash deposit allowance before per-deposit fees apply.

International Payments and Multicurrency Support

For companies paying overseas suppliers, receiving revenue from international customers, or managing contractors in other countries, FX conversion costs and international wire fees are an expense that won’t appear in monthly fee comparisons. Many traditional bank accounts charge $25–$45 per international wire and apply a 1–3% FX markup on currency conversion, which can be a pain for global companies. Some digital platforms offer international transfers at rates much closer to the interbank rate, or hold balances in multiple currencies, significantly reducing the cost of cross-border operations.

Watch for Hidden Fees and Usage-Based Charges

If you choose a free business checking account without doing research, you might be surprised by the fees you accrue as you use the account. Common fee triggers across even zero-monthly-fee accounts include:

- Outgoing wire transfers (domestic and international)

- Cash deposits above monthly thresholds

- Expedited ACH

- Out-of-network ATM withdrawals

- Overdraft fees

- Returned payment fees

- FX conversion on international card transactions.

Before opening any business account, review the fine print to see what fees you can expect as you perform routine activities. It may be free to hold the account, but the full monthly cost will likely depend on how you use it.

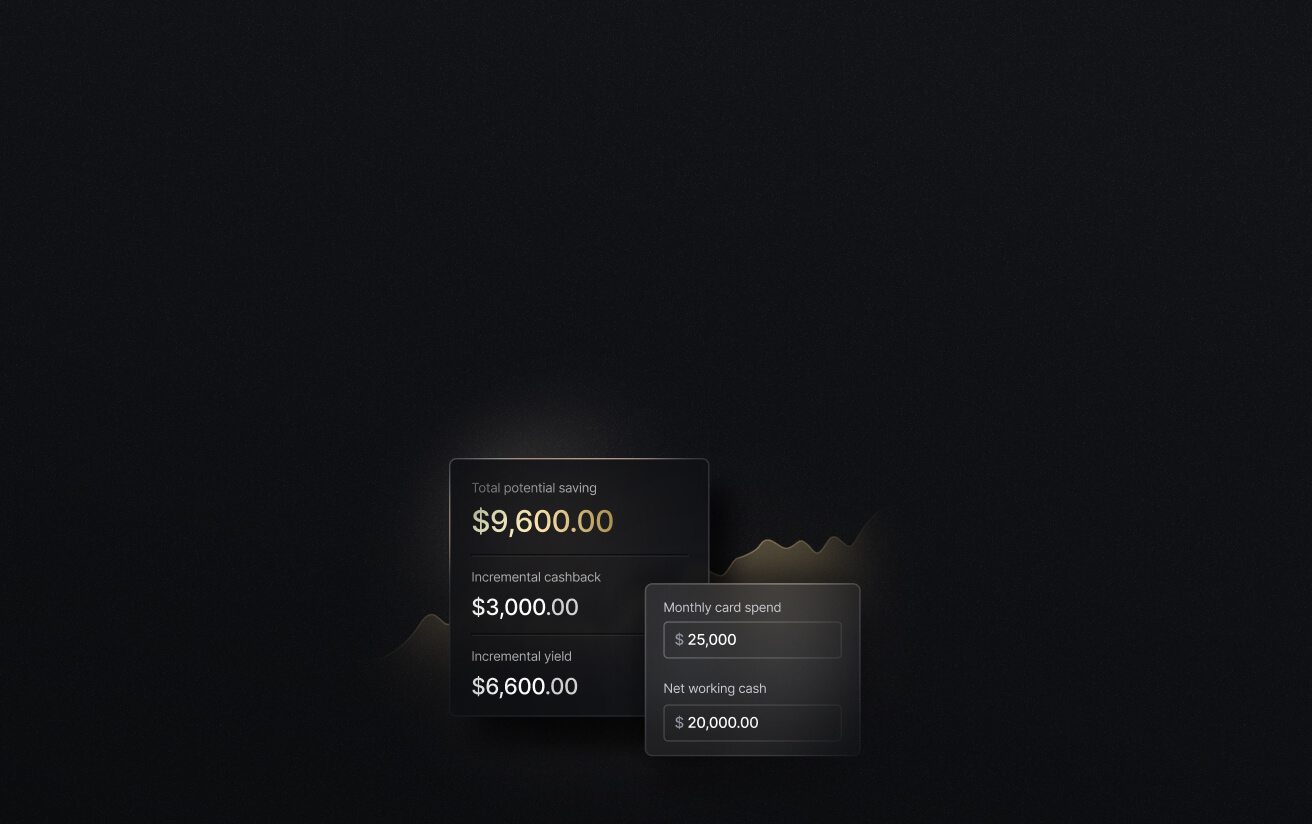

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Top Free Business Accounts by Business Fit in 2026

The best free business account depends on how the company manages money and how much of it comes in the form of cash. Below, we’ll take a look at both traditional bank business checking accounts and online banking platforms that provide banking services through FDIC-member bank partners.

Best for Digital-First and Remote Businesses

Slash

Built to centralize financial operations on one integrated dashboard, with no monthly fee.

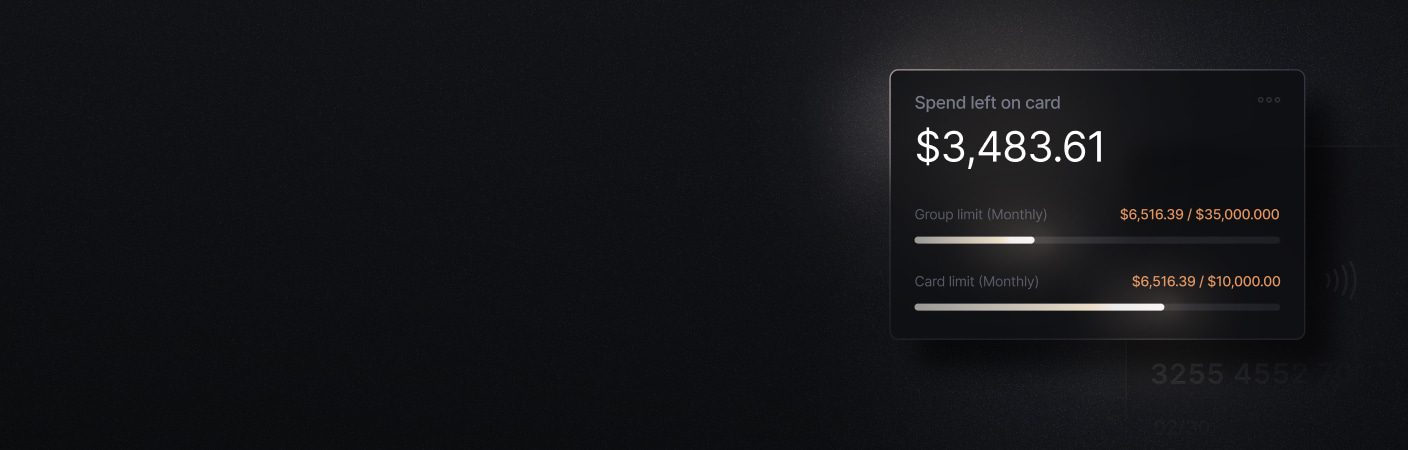

- Slash Visa Platinum Card earns up to 2% cashback on eligible purchases; apply granular spend controls and get real-time visibility into every transaction across cards and outbound transfers.

- SWIFT network wire transfer to 180+ countries, global ACH settlement, real-time domestic transfers via RTP and FedNow. Slash Pro users pay no additional per-transaction fees for domestic bank transfers.

- High-yield treasury earning up to 3.76% annualized on idle funds, through money market funds managed by BlackRock and Morgan Stanley within the account.

- Twin, an AI assistant included at no cost, can manage your cards, analyze and forecast cash flow, and make online purchases from end to end.

Bluevine

A solid no-fee checking option with an interest rate, though transfer fees run high.

- Earns 1.3% APY on balances up to $250,000, but only in months you spend $500 on the Bluevine card or receive $2,500 in customer payments; otherwise no interest accrues that month

- Optional line of credit up to $250,000

- Outbound expedited transfer fees on free plans; $10 same-day ACH, $15 domestic wires

Wise Business

Built for international payments, best used as a payment layer rather than a primary account.

- Multi-currency holding in 40+ currencies; international transfers at the mid-market rate

- Local bank account details in major currencies

- Issues debit cards with spend controls, but no rewards corporate card and limited invoicing

Novo

An accessible starter account that's light on advanced controls.

- ATM fee refunds up to $7/month

- Built-in invoicing

- Missing approval workflows, payment scheduling, and custom user permissions

- FDIC insured only up to $250k, less than most competitors

Mercury

Aimed at startups and tech-oriented businesses, with banking and yield handled in separate products.

- FDIC coverage up to $5M through sweep programs

- Mercury Treasury requires at least $250,000 held in Mercury accounts to qualify

- Integrations with Stripe, QuickBooks, and Xero

- IO card earns 1.5% cash back

- 3% FX fee on card transactions in non-USD currencies

Best for Brick-and-Mortar Businesses and Cash Deposits

For businesses with physical locations, regular cash handling, and a preference for in-person support, a traditional bank account may be the practical choice. Just know that genuinely free options are rare here. The accounts below all waive their fee under the right circumstances, but none are free by default the way a no-commitment fintech account is:

Chase Business Complete Banking

Widely available and built for cash deposits, but thin on digital tooling.

- $15/month fee, waived with a $2,000 minimum daily balance

- 100 free non-electronic transactions per month, unlimited electronic

- $5,000 in fee-free monthly cash deposits

- Nearly 5,000 U.S. branches

- Lacks the automation and transaction visibility of digital-first accounts

Bank of America Business Advantage Fundamentals

A traditional account that works best for businesses keeping a steady balance.

- $16/month fee, waived with $500 in new net debit card purchases per cycle or a $5,000 combined average monthly balance

- May be less accessible for businesses with variable cash flow

- Fees for out-of-network ATM use, so a nearby branch helps

- 200 free transactions per month, then $0.45 each

- QuickBooks Online and Desktop integration

U.S. Bank Business Essentials

No-fee banking with branch access, held back by steep transfer fees.

- No monthly fee

- Branch and ATM access, with 25 free teller and paper transactions per month ($0.50 each after)

- Aimed at small businesses with simple needs and tooling

- Domestic wires $30 to $40, international wires around $70

- $1 per domestic ACH, which can add up at volume

Free vs. Paid Business Bank Accounts: Which Is Right for Your Business?

Free accounts work well for businesses in their early stages, with lower transaction volumes, online operations, or simple payment needs. A freelancer keeping business and personal finances separate, or a new LLC that pays vendors by ACH and receives deposits electronically, will usually find a zero-fee account covers everything they need.

Once you need higher transaction limits, expense management with approval workflows, corporate cards with configurable spend controls, or treasury yield on operating balances, a paid account often delivers more operational value than the fee savings are worth. Many paid plans also waive transfer fees, so they can pay for themselves once you run enough wires or ACH payments through them.

Your decision should follow how money moves through your business. A business running 200 transactions a month with international supplier payments has very different needs from a two-person startup taking in five ACH deposits. Weigh how much you send abroad, whether you handle cash, how many people need spending approval, and how high your monthly volume runs.

You don't have to choose between a bare free checking account and an expensive feature-rich one. Slash gives you both: a free plan with no paywalled core features, and the cards, payments, and treasury tools a growing business grows into.

Move Beyond Traditional Business Checking with Slash

Slash offers a business checking account that does far more than store money. The platform brings your banking, cards, payments, and accounting together on one dashboard, so you can run the financial side of your business from a single place. It's a digital-first platform built for businesses that want serious financial tooling, not just somewhere to park cash.

Two things set Slash apart from a standard checking account. First, your deposits are well protected. Through Column N.A.'s sweep network, balances are automatically distributed across multiple FDIC-insured banks, extending coverage into the hundreds of millions rather than the standard $250,000.² Second, you don't need a separate provider to earn yield on idle cash. Separately, Slash includes an integrated treasury that earns up to 3.76% annualized through money market funds managed by BlackRock and Morgan Stanley.⁶ You get accessible checking alongside competitive yield, all managed from one dashboard.

Other key features that can help small businesses include:

- Slash Visa® Platinum Card: Earn up to 2% cashback on eligible business spend. Set customizable spending controls and issue unlimited virtual cards for team expenses, vendor payments, subscriptions, and more

- Cryptocurrency support: With built-in on/off ramps, send and receive USDC and USDT across 8 supported blockchain networks straight from Slash.⁴

- Diverse payment methods: Slash supports global ACH, international wires via SWIFT to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- Global USD: The Slash Global USD Account is designed for foreign founders who want access to USD without forming a US entity.³ Balances are backed by Slash's USDSL stablecoin, matched one-to-one with the US dollar.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

If you’re looking for a free business checking account that comes with more features than many paid accounts, give Slash a try.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

How can I open a free business bank account online?

With online banking, opening a business checking account is often easier than opening one with a traditional bank. Traditional banks may require an in-person visit, while online banking avenues only require internet access and appropriate documentation.

What kinds of corporate cards do free business checking accounts come with?

Free checking accounts can come with all types of cards, including business debit cards, credit cards, and charge cards. The Slash Visa® Platinum Card is a charge card, meaning its balance must be paid in full at the end of each period.

The Top Business Cards for Small Businesses in 2026

Do free business checking accounts come with mobile banking capabilities?

Usually, yes. Mobile banking is common among free checking accounts from all sources, including credit unions. However, the transactions they're equipped to handle can vary.

Now Live: The New Slash Mobile App

What does the monthly maintenance fee pay for?

Generally speaking, the monthly maintenance fee pays for the upkeep of the checking or savings account, often including fraud protection tools and merchant services.

Read more from us