A Beginner's Guide to Crypto Tax Forms for U.S. Businesses

Only five years after the first cryptocurrency was created, the IRS began developing guidelines around how it should be legally classified and taxed. In 2014, they established that crypto should be considered property rather than currency. Since then, crypto has become more mainstream and the rules have expanded as a result. You can now expect to be asked about digital assets on just about any tax return you fill out, whether you’re an individual or a business owner. If you’ve spent the year owning and trading crypto, you should know what questions and forms to expect before you dive into filling out your paperwork.

If you’re part of a finance team that manages fiat operations and crypto payments at the same time, staying on top of tax regulations is especially important. While a wire transfer is straightforward to categorize, a stablecoin payment to a contractor might not be. You should know which events are considered income, when it's recognized, and how to report it on which form.

This guide covers the U.S. federal rules for reporting crypto activity using tax forms. We’ll walk through what triggers a taxable event, how the IRS categorizes crypto income, which forms you'll use, and what mistakes tend to trip people up. We’ll also take a look at Slash, a business banking platform that supports on/off ramps for stablecoins like USDC and USDT.¹, ⁴ With the help of a real-time financial dashboard and an agentic AI assistant, it’s possible to easily track and create audit trails for your business’s crypto transactions.

Crypto Glossary

Unsurprisingly, the upcoming discussion about crypto and tax regulations has some dense terminology. Let’s take a look at some of the words you’ll need to know:

- Stablecoins: Virtual tokens designed to maintain price stability, usually by being linked to an underlying fiat currency. The two most popular stablecoins in use today are USDC and USDT, which are both pegged 1:1 to the U.S. dollar.

- Blockchain: A decentralized ledger that records and verifies transactions across a network of computers rather than relying on a centralized authority. Once a transaction is confirmed and added to the blockchain, it becomes very difficult to alter. This structure allows payments to be verified and settled without relying on an intermediary like a correspondent bank.

- Hard fork: A major software upgrade that isn’t backward-compatible, resulting in the split of a blockchain network into two separate chains. One chain follows the newly updated rules, while the other continues operating on the original rules. This split can actually result in the creation of a brand-new digital asset.

- Custody services: The secure storage and management of digital assets on behalf of a customer. A custodial service holds a user’s private keys and controls their funds, while a non-custodial service gives the user full control.

- Cost basis: In the context of crypto, cost basis is the original total amount you paid to acquire an asset, including purchase price, transaction fees, and gas fees. It’s the baseline used to calculate your taxable capital gains or losses whenever you sell, swap, or spend your cryptocurrency.

- Crypto mining: The process of verifying cryptocurrency transactions and adding them to a blockchain. It also introduces new coins into circulation, which is the result it’s more known for.

- Airdrops: Promotional distributions of free digital tokens or coins sent directly to user wallet addresses, often for things like sign-up bonuses.

Which Crypto Transactions Can Trigger Taxes?

Tax liability from crypto depends on what you actually do with the asset, not just what you hold. In the eyes of the IRS, there are two categories of taxable events. These are disposals, which may generate capital gains or losses, and receipts of value, which are typically taxed as ordinary income.

Common taxable disposal events include:

- Selling crypto for U.S. dollars or another fiat currency

- Trading one token for another

- Spending crypto on business expenses (the asset's value at the time of the purchase, minus your cost basis, is your taxable gain or loss)

- Converting to stablecoins when the market value of the original asset has changed since you acquired it

The following events represent ordinary income, recognized at fair market value on the date received:

- Getting paid in crypto for services rendered

- Mining rewards (treated by the IRS as self-employment income)

- Staking rewards

- Airdrop distributions

- Tokens received from a hard fork

A couple of the most common crypto activities aren’t considered taxable events, including buying crypto to hold and transferring crypto between wallets or accounts you own. Inconveniently, though, if you pay a transfer fee in crypto, that fee itself often counts as a disposal and needs to be reported.

Capital Gains vs. Ordinary Income: How the IRS Treats Crypto

The IRS treats digital assets as property under existing tax law, which means you work with the same framework used for stocks and real estate. If you dispose of a digital asset you held as a capital asset, the gain or loss is considered a capital gain or loss. Crypto is instead treated as ordinary income when you receive it as payment for services.

In cases of capital gains, the holding period determines the rate. Assets held for 12 months or less generate short-term capital gains, taxed at ordinary income rates. Assets held for more than 12 months qualify for long-term capital gain rates, which tend to be lower. These gains are calculated on Form 8949 and summarized on Schedule D of the relevant return.

Ordinary income from crypto requires different forms, depending on how it was earned. Self-employed individuals receiving crypto for services or running a mining operation typically report on Schedule C and pay self-employment tax. Employees receiving crypto wages report it on Form 1040 like any other paycheck. Staking rewards typically appear on Schedule 1. If you’re part of a C corporation or a pass-through entity, you report income on your relevant return, which will likely be Form 1120 or 1065.

Key Crypto Tax Rules Business Leaders Should Know Before Filing

Whether you’re filing a Form 1040, 1065, or 1120, you’ll be answering the following yes-or-no question about digital assets: at any time during the tax year, did you receive, sell, exchange, or otherwise dispose of a digital asset?

The tricky part about answering this question isn’t necessarily knowing what the relevant taxable events are. For many businesses, the hardest part is documenting it all. For just about every crypto event, you’ll need the date, the number of units, the fair market value in U.S. dollars at the time of the transaction, your cost basis, the wallet or exchange involved, the counterparty where applicable, and transaction fees. Fees paid in crypto may be added to your cost basis, which can make the math even tougher.

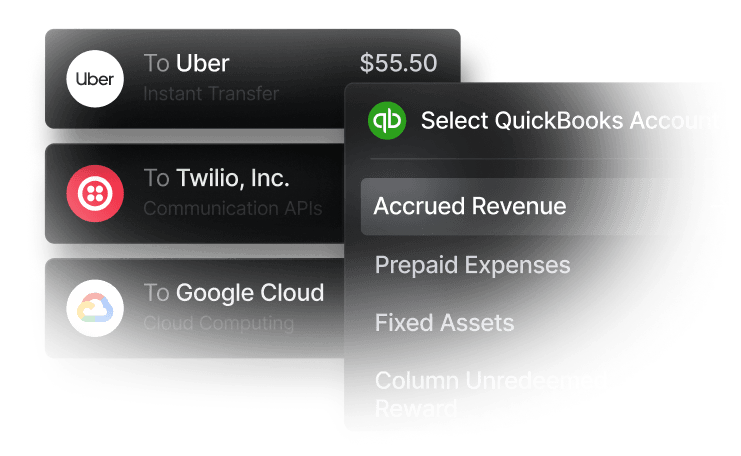

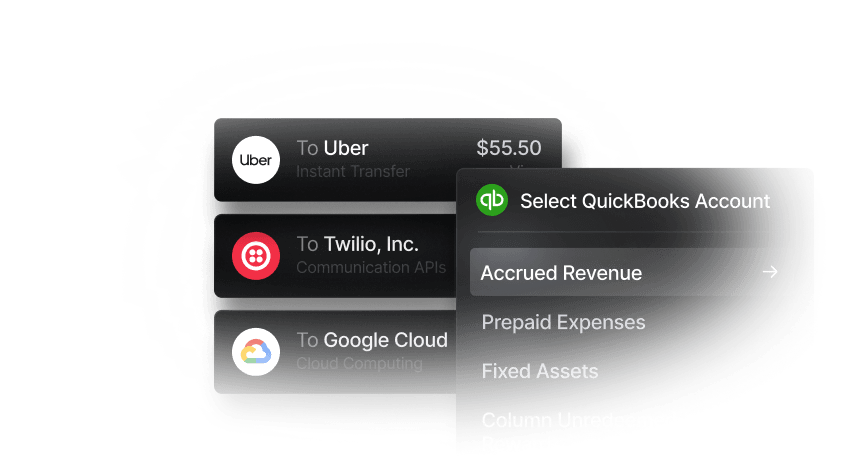

Without this data, you can't compute capital gains accurately and you could face penalties from the IRS. If your business consistently does business with digital currency, tracking it all by hand is nearly impossible. Neobanks that support stablecoin payments natively, such as Slash, can help create an audit trail with the data points you need for reporting. Slash’s agentic AI assistant, Twin, can also retrieve data from past transactions you may not have logged accurately.

Outside of careful documentation, there are a couple more crypto tax strategies worth knowing. For example, you can hold tokens for more than one year to access long-term capital gain rates, and you can use tax-loss harvesting techniques to offset realized gains with other realized losses. In any case, it’s wise to review strategies with a tax advisor before you try anything tricky.

IRS Forms You'll Use to Report Crypto Activity

If you run a business, you’ll start your returns on forms like Form 1040 or 1120. There isn’t an entirely separate system for businesses that utilize crypto. However, as you make your way through your standard tax returns, you’ll find that the following forms may be necessary to fill out or draw information from:

Form 1099-DA

Form 1099-DA is the IRS's new information reporting form for digital assets, introduced through the Infrastructure Investment and Jobs Act broker reporting rules. Since its introduction in 2025, custodial brokers like centralized exchanges and wallet providers are required to report gross proceeds from sales and exchanges of digital assets. As of 2026, brokers must also report cost basis for assets acquired on their platform.

With this change, businesses selling crypto through major exchanges may receive a 1099-DA showing both proceeds and basis. However, the form only reflects what the broker knows. If you brought crypto in from a different exchange, a cold wallet, or an older account, the broker has no cost basis information for those assets. Ultimately, it’s up to the taxpayer to fill in the correct cost basis.

Form 1099-MISC

When an exchange pays staking rewards or other miscellaneous crypto income, it may issue a 1099-MISC if the amount exceeds $600 in a tax year. If it’s below $600, no form is issued, but the income is still taxable and must be reported.

While an exchange will send you some details, you can’t count on it to spoon-feed you. Self-custody activity, DeFi transactions, transfers between wallets you control, and activity on platforms outside the current U.S. broker reporting requirements won't appear on any form you receive. That’s why tracking your crypto activity throughout the year is so important.

Form 8949

Form 8949 is where capital gains from crypto disposals are listed. Each taxable sale or exchange gets its own line that includes the asset description, date acquired, date sold, proceeds, cost basis, and gain or loss. Totals from Form 8949 link to Schedule D, which aggregates capital gains and losses and carries the net result into the main return. While tax software can sometimes import transaction data from exchanges, you'll probably need to review and supplement any records with missing or incorrect basis before filing.

Schedule 1 (Additional Income and Adjustments)

Your Schedule 1 is generally where staking rewards, mining income for those not running a dedicated mining business, airdrop distributions, and hard fork income get reported. If you’re a self-employed individual running a mining business, that income goes on your Schedule C instead, which also allows deductions for ordinary and necessary business expenses.

One more thing to note before we move on: if you’re part of a multi-entity structure, each entity files its own return and answers the digital asset question independently. A holding company with several operating subsidiaries should have consistent record-keeping across all their entities. With the ability to centralize subsidiaries on one dashboard, Slash can make it easier to coordinate records across banking, card spend, and stablecoin transfers.

Common Crypto Tax Mistakes

Given the complexity of the field, even experienced tax pros can make mistakes with digital assets. That doesn’t make the IRS more forgiving, though. Here are five common errors to watch out for:

- Undercounting transaction fees in cost basis: Any fees paid in crypto on a blockchain or exchange may be added to cost basis on purchases or subtracted from proceeds on sales. Either way, it reduces your taxable gain. Ignoring consistent fees over a full year can lead to large inaccuracies once you finally do the math.

- Treating wallet-to-wallet transfers as taxable events: Moving crypto between two wallets or accounts you own isn’t a disposal, so it doesn't trigger capital gain treatment. Sending crypto to someone else's wallet is a different matter.

- Missing a taxable event: Paying a contractor in USDC, buying software with ETH, or covering a business expense with a coin that’s grown in value since acquisition counts as a capital gain.

- Relying entirely on platform-provided forms: While getting a 1099-DA or exchange gain/loss report from a platform is helpful, it only reflects activity inside that platform. Assets transferred in from other exchanges or wallets will often show missing cost basis, meaning you’re in charge of filling in the blanks.

- Ignoring income from staking or rewards: Even if your staking yield and reward distributions are small amounts, they're taxable income in the year received and need to be tracked and reported.

How Slash Helps Make Crypto Tax Reporting Easier

Not all businesses that use crypto are embroiled in the world of mining and staking. Some simply adopted stablecoins to save money and time on B2B transfers. If you’re a stablecoin-native business, you can use Slash’s tools to easily transfer, convert, and reconcile your crypto.

Slash gives businesses a clearer way to manage stablecoin activity by bringing transfers, counterparties, transaction details, and supporting context into one system. While we can’t fill out your crypto tax forms for you, our clean records and audit trails can make it much easier to hunt down the data you need. If you can’t find a certain number, you can ask Twin, our agentic AI assistant, to dig through your transfers for you.

Our platform supports sending USDC and USDT across eight different blockchains, including Tron, Solana, and Ethereum. From there, we have built-in on/off ramps that allow you to convert your stables to fiat for fees generally lower than 1%.

Outside of the world of crypto, Slash also comes with:

- Invoicing features: With Slash’s invoicing and bill pay features, users can send customized invoices, collect payments, and manage vendor bills all in the same place.

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. Users can also earn up to 2% cash back on business purchases.

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, NetSuite, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Global USD: The Slash Global USD Account is designed as an alternative for foreign founders who want access to USD without forming a US entity.³ Balances are backed by Slash’s USDSL stablecoin, which is matched one-to-one in value with the US dollar.

If you’ve adopted stablecoins for cross-border payments and you want an easier way to keep track of them, try Slash today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

This guide is educational content, not legal or tax advice. The rules around digital assets are still evolving. Talk to a qualified tax professional about your specific situation before filing.

Frequently Asked Questions

Do businesses pay taxes differently on crypto than individuals?

Generally speaking, the same framework applies, but the rates and forms differ by entity type. A C-corporation pays corporate income tax rates on crypto gains and income, not the long-term capital gain rates available to individual investors. Meanwhile, pass-through entities like partnerships and S-corporations report crypto activity on their entity returns, and the income flows through to owners' personal returns.

Crypto Tax Guide for Businesses: Reporting, Calculating, Complying

Are stablecoin transactions taxable?

They certainly are. The IRS treats stablecoins as digital assets subject to the same property-based rules as other crypto. If you own a token that’s grown in value, converting it to a stablecoin is typically a disposal of the original asset, triggering a capital gain or loss. Receiving a coin like USDC for services is considered ordinary income at fair market value on the date of receipt.

How to Accept Crypto Payments as a Business in 2026

Do self-custody crypto wallets need to be reported on tax forms?

Self-custody and DeFi activity currently falls outside the 1099-DA reporting requirements, which apply only to custodial brokers. So, you won't receive a tax form for this activity, but you still have to report it.