Are Credit Card Rewards Taxable? Debunking Common Myths

If you own a business in the United States, it might feel like the IRS wants a piece of every single dollar you earn. Whether your company receives money through standard sales, capital gains, royalties, crypto investments, or even canceled debts, you’ll usually be taxed on all of it. One more way some modern businesses make money is through cash back rewards on corporate credit cards. So, does the IRS tax that too?

For most business owners, the answer is no. This isn’t a blanket truth, though, and there are some nuances to corporate credit card reward rules that finance teams should know. Once you learn exactly how the IRS treats different kinds of rewards, you’ll know how to report them correctly and what actually counts as taxable income.

This article covers each aspect of the taxable card rewards question, including how they’re classified, the treatment of cash back and points, how to log them in your books, and some common misconceptions. We’ll also take a look at Slash, a business banking platform that not only automates accounting and reporting tasks, but offers a corporate card of its own.¹ The Slash Visa® Platinum Card is a charge card that earns up to 2% cash back on business purchases and comes with spend controls that can be configured for different employees and departments.

Introduction to Credit Card Rewards

Credit card rewards can either come in the form of cash back paid as a statement credit or direct deposit, points that can be redeemed for certain categories, and promotional bonuses tied to card sign-ups. For the most part, they're structured as incentives to use the card. Many programs reward spending at a flat rate, a tiered rate by category, or some combination of both.

While the mechanics seem straightforward, the tax treatment often isn’t. The answer to whether a given reward is taxable depends on how you earned it rather than how much you earned. Getting that distinction wrong can affect both your books and your tax return.

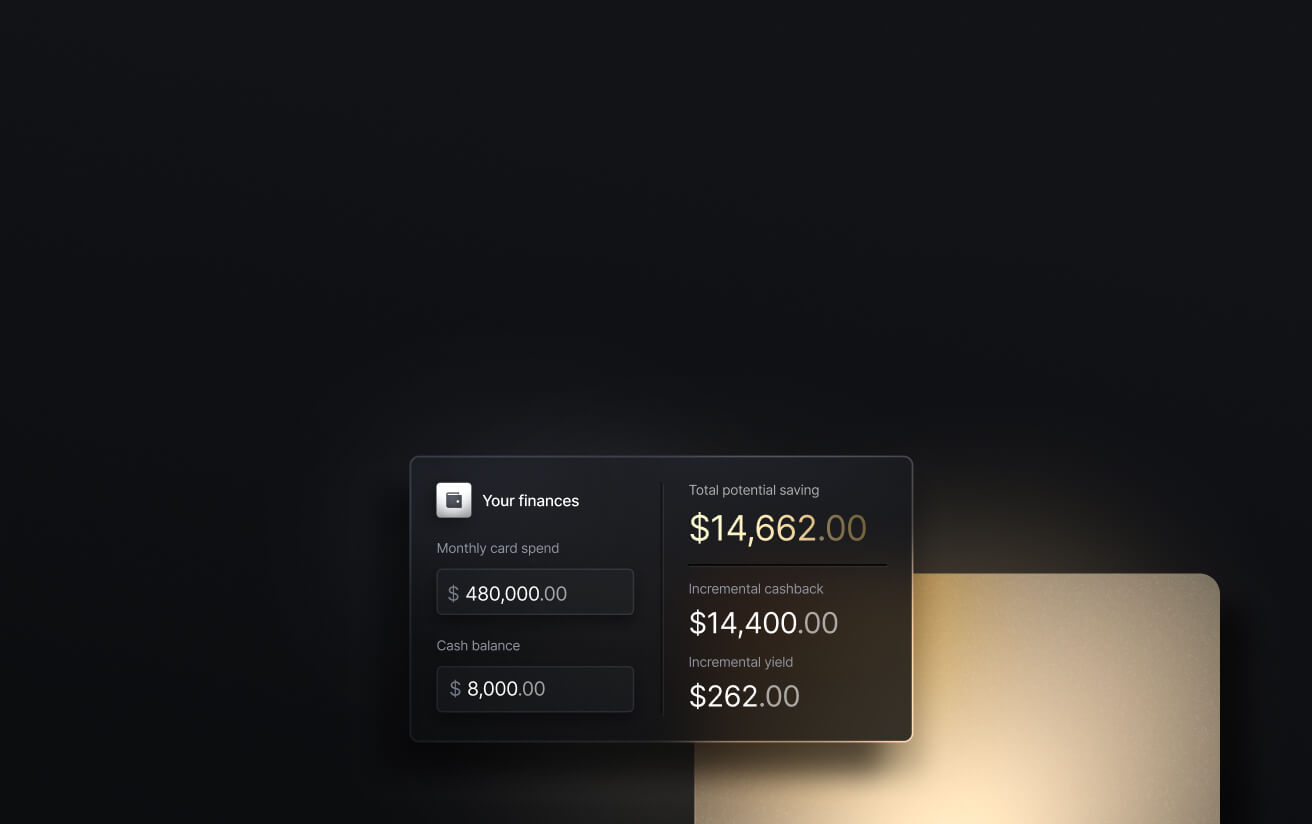

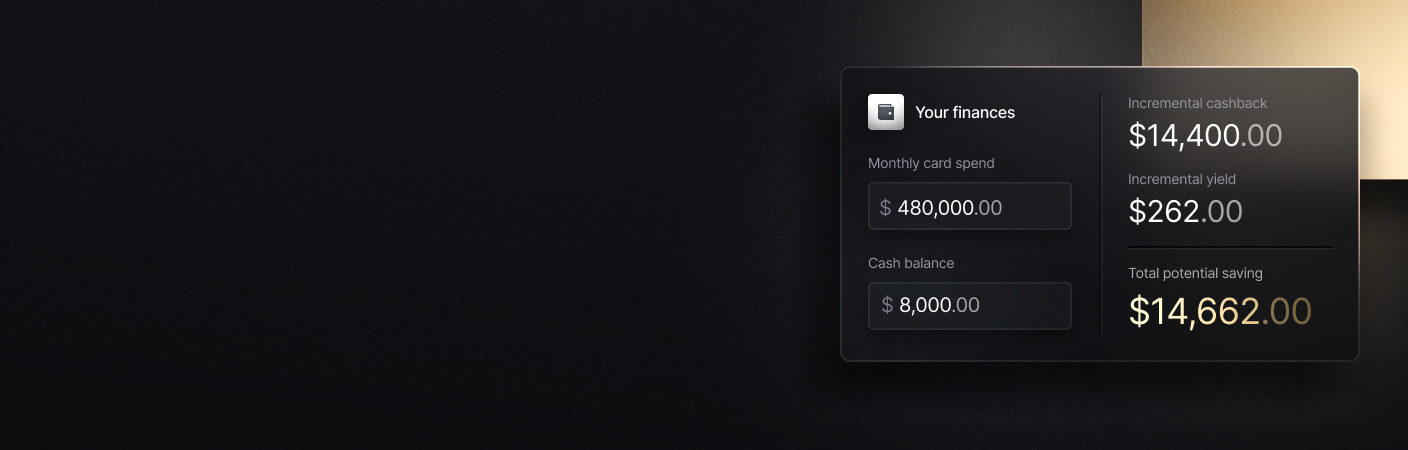

All rewards that count as taxable income need to be reported, just as any other income. On the other hand, rewards that just reduce your deductible expenses should also be recorded correctly to make sure you don’t overstate what you can deduct. To put this into perspective, if your business spends around $300,000 each year on a 2% cash back card, you’ll earn $6,000 back every year. You’ll likely have some inaccuracies on your tax returns and reconciliation reports if you don’t figure out how to correctly account for that number.

Taxable vs non-taxable: what’s the difference?

While the IRS doesn't have a dedicated section that covers credit card rewards, its broader guidance on rebates and income can give us an answer. Legally speaking, there’s a line drawn between two types of rewards. Rewards earned through spending are generally treated as a reduction in the purchase price, not as income. Rewards received without any spending requirement, such as sign-up bonuses, are more likely to be treated as taxable income.

That's the long and short of it. If you spent money with your card to earn the reward, it's probably not taxable. If you received cash or credit for opening an account or completing a referral, there's a good chance it is. While this is a quick way to remember the rules, not every single scenario matches these guidelines. The distinction between cash back and points rewards brings a couple exceptions.

IRS Tax Treatment of Cash Back and Points Rewards

Cash back rewards are flat financial bonuses awarded to cardholders when making purchases, while points rewards give virtual “points” that can be spent on specific categories like airlines and hotels. At their roots, they both give money back to the user. While they’re similar, there are a couple exceptions you should know before accounting for either of them. Here’s how they both work in the eyes of the IRS:

Cash back

Cash back earned on spending is treated as a purchase price reduction. If your card pays 1.5% on every dollar you spend, that cash back represents a discount on whatever you bought. If you bought a $4,000 item with a Slash Visa® Platinum Card and earned $80 (at 2% cash back), it’s considered a $3,920 purchase. From the IRS's perspective, you didn't earn income; you paid a little less for things you were buying anyway.

If you receive a bonus payment or statement credit as an incentive for opening a new account, that’s its own type of cash back. The IRS treats that as income, not a rebate. There was no purchase to discount; you simply received something of value for free. If that value happens to be $600 or more, the card issuer is actually supposed to send you a 1099-MISC form.

There's also a fairly obscure situation that can arise with cash back cards. If an employee uses a personal card for a business purchase, gets reimbursed by their employer for the full amount, and keeps the cash back from that transaction, the IRS may treat that cash back as taxable income to the employee.

Points rewards

Overall, points earned through spending follow the same rules as cash back. Whether your card awards one point per dollar or five points on travel and dining, those points are tied directly to purchases you made. The IRS treats them as a reduction in the cost of the underlying spending, not as income.

While a cash back rewards card might give you a financial reward just for signing up, some points-based cards offer rewards for hitting spending thresholds. A sign-up bonus that requires you to spend a certain amount, such as 50,000 points for $3,000 in the first three months, generally isn’t taxable because the points are connected to qualifying purchases. In short, a $600 welcome bonus for signing up is usually taxable, while a $600 bonus for hitting a three month milestone isn’t.

How to Record Business Cash Back Correctly

Now that you know the taxation rules surrounding card rewards, you should know how to record them in your books. Here’s what you should keep in mind as you sit down to log your cash back or points:

Business vs. personal credit card rewards

When it comes to federal tax rules, personal credit card rewards and business credit card rewards actually work the same way. There's no separate IRS category for business cards. What changes is how the rewards affect your financial records, since business rewards have to monitor deductible expenses.

Regardless of whether you’re a C-corporation or a sole proprietor, rewards impact the deductions you can get back on your relevant tax return because they technically reduce what the business spent. If you spent $20,000 on a 2% cash back card (and every single purchase was tax-deductible), you can only claim deductions on $19,600 of it.

Reporting business rewards income

The right way to log business rewards income is to record it as a reduction against the expense being offset, not as a separate income line. If you spend $5,000 on office supplies in a month and earn $75 in cash back, your deductible office supply expense is $4,925, not $5,000.

This also relates to how you handle rewards that get applied to specific business costs. For instance, if you redeem rewards to cover a $400 hotel bill for a business trip, that $400 now can't be claimed as a deductible business expense. The rewards paid for it, so there was no out-of-pocket cost to deduct. If you were to use rewards to cover half the bill and pay $200 out of pocket, only the $200 in cash you paid can be deducted.

The cleanest approach is generally to record cash back credits against the expense category they relate to. For general statement credits that aren’t tied to a specific purchase, record them as a reduction in overall expenses. Either way, you want to make sure your deductible expenses reflect what you actually paid with your money after rewards are accounted for.

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Common Myths About Credit Card Rewards and Taxes

There are a pair of myths regarding how card rewards are taxed that tend to circulate among finance teams. You may have even clicked on this guide thinking they were true. Here’s what some people can get wrong about IRS rules:

Myth 1: All rewards are taxable

This myth probably comes from a misunderstanding of what’s considered a “card reward”. If you found out that you have to pay taxes on your $400 sign-up bonus, you may come away thinking that rewards from cards automatically get taxed. In the eyes of the IRS, one-time sign-up bonuses are very different from cash back and points earned from spending. Only some types of card rewards are taxable, not all of them.

Myth 2: Only high earners need to report

If your sign-up bonus is at least $600, you’ll receive a 1099-MISC in the mail. This has led to two different sub-myths within the same myth. Some cardholders believe that as long as their sign-up bonus stays below $600, they don’t have to pay taxes on it. Other business owners might think that they need to keep their annual cash back rewards below $600 to avoid the same taxes.

If you’ve been paying attention, you know neither of these things are true. The standard taxation rules apply to each category no matter how much you receive in rewards. The 1099 form doesn’t create a tax requirement on its own, it just works as a more standardized method of filing.

Earn More From Your Business's Spend With Slash

If you’re looking to maximize the value of your business card rewards, choosing a card with strong cash back and modern spend controls can make an even bigger difference.

The Slash Visa® Platinum Card is a corporate charge card that earns businesses up to 2% cash back on eligible spending. You can issue unlimited virtual cards with customizable spending limits, merchant restrictions, and approval controls, making it easier to manage employee spending at scale. Slash also monitors transactions for suspicious activity and alerts your team when potential fraud is detected.

Besides the card, the Slash dashboard brings all of your company’s spending into one place. Track card purchases alongside ACH payments, wires, stablecoin transfers, and other transactions in a single dashboard.⁴ With native integrations for QuickBooks, Xero, Sage Intacct, and NetSuite, transaction data flows directly into your accounting workflows, reducing manual reconciliation and making month-end close faster and more accurate.

Here’s a rundown of some of the other features Slash offers:

- AI-powered finance:Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury:Earn up to 3.83% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

- Reimbursements: Instead of managing reimbursements across multiple tools, teams can now submit, review, and approve reimbursements directly inside the Slash dashboard. Connect your bank account, upload your receipt, and let Slash capture the details.

Slash’s combination of rewards, controls, and visibility can be a big advantage for teams that spend a lot of money with corporate cards. If you’re interested in earning up to 2% cash back, check out the Slash Visa® Platinum Card today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Will I get a 1099 for my business credit card rewards?

For ordinary cash back and points earned through purchases, no. The IRS treats those as rebates, and rebates don't get reported on a 1099. A 1099-MISC will only show up for account-opening bonuses, referral rewards, or promotional offers above $600. Below $600, no form is required, but the income will still likely be taxable.

How Does Cash Back Work? Choosing the Right Credit Card Rewards Program

Can I deduct business expenses paid with credit card rewards?

Nope. Expenses paid with rewards aren’t deductible because there's no out-of-pocket cost to deduct. If you redeem cash back to pay for a business dinner, a software subscription, or a flight, the portion covered by rewards can't be written off.

Are Business Credit Card Payments Tax Deductible? How Payments Affect Your Deductions

Are referral bonuses from credit card programs taxable?

Generally, yes, since they typically aren’t tied to a qualifying purchase. Since there's no purchase being discounted, the rebate logic doesn't apply, and the value you received is treated as income.

Read more from us