Bluevine, Mercury, or Slash: Which Business Banking Platform is Right for Your Company?

Not every fintech platform can fully replace your bank. Some focus mainly on expense management or specific financial workflows, while others provide a more complete banking experience: business checking, treasury, financing, and more. Bluevine and Mercury both fall into the second category, positioning themselves as modern, digital-first alternatives to traditional banking.

On the surface, Bluevine and Mercury look fairly similar. Both are fintech companies that offer business checking accounts, corporate cards, and built-in expense management tools. But a closer look reveals differences that can have a real impact on fit depending on your company's size, structure, and financial needs.

In this guide, we’ll compare Bluevine vs Mercury across pricing, features, payment capabilities, and ideal use cases to help you find the best banking platform for your business. We'll also highlight the areas where both platforms fall short, and where Slash stands out as a more advanced, full-featured alternative. Slash not only can act as a replacement for traditional banking, but it also combines industry-aware tools, leading cash back rates, and native cryptocurrency support into a single modern financial platform.¹, ⁴

What are the primary services offered by Bluevine?

Bluevine is a digital business banking platform built for small businesses and entrepreneurs seeking a digital alternative to traditional banking. Its partner bank, Coastal Community Bank, member FDIC, provides the underlying financial institution infrastructure. Bluevine's core offerings include:

- Business checking accounts that earn interest, along with Bluevine debit cards and subaccounts for organized balance management.

- Expense management features including invoicing, bill payments, and accounting integrations with tools like Xero.

- Ability to accept cash deposits via Green Dot locations and MoneyPass ATMs, giving it a broader physical network than most fintech competitors.

- Lending options including tailored lines of credit, term loans, and SBA loans for businesses in need of additional financing.

Pricing & features

Ideal user profile

Bluevine business checking is best suited for small business owners and freelancers who want more than a basic banking experience. Its unique features compared to competitors include cash access via ATM networks or Green Dot or those who want interest on their checking balance; however, Bluevine lags behind some competitors in their supported payment methods and expense management features (e.g. Bluevine does not natively categorize transactions).

What key features does Mercury provide for business banking?

Mercury is another digital business banking platform designed with tech companies and startups in mind. Its partner banks (Choice Financial Group and Column N.A.) provide FDIC-insured deposit coverage of up to $5 million through their sweep program. Key features include:

- Mercury IO Mastercard credit card, a charge card that earns up to 1.5% cash back on purchases

- Business checking and treasury accounts with competitive yields for businesses looking to put their balance to work

- Expense management features including invoicing, bill payments, and accounting integrations for streamlined financial operations

- Working capital loans providing domestic financing options for growing businesses that need quick access to capital

Pricing & features

Ideal user profile

Mercury is geared toward startups, SMBs, and tech companies looking for an alternative to traditional banking. It covers the basics well enough, and its personal banking services adds some additional accessibility for users. But Mercury does have its limitations. Access to the highest treasury yield, one of Mercury’s headline features, requires a $250K minimum balance that may put it out of reach for some businesses. The Pro plan at $299/mo can also be hard to justify for the average SMB. Ultimately, the platform lacks some features for businesses that operate internationally, manage multiple entities, or have any need for crypto capabilities.

What are the primary services offered by Slash?

Slash is yet another digital business banking platform, partnered with Column N.A. for its core banking infrastructure. Slash is an advanced, industry-aware platform for complex startup operations, ecommerce operators, international businesses, Web3-native companies, and more. Our key offerings include:

- Slash Visa Platinum Card, a charge card that earns up to 2% cash back on eligible business spending.

- Multi-entity management and unlimited virtual accounts backed by millions in FDIC insurance protection for businesses running complex financial operations across entities.²

- Invoicing, accounting integrations, reimbursements, and cash flow analytics for unified expense management capabilities.

- Global USD account that enables foreign business owners to access USD banking without a U.S. incorporation or LLC.³

- Native cryptocurrency support, a feature largely absent from traditional banks and fintech competitors alike.

Ideal user profile

Slash is a vertical-specific platform, meaning its services are designed around the needs of specific industries. It's a strong fit for SMBs, startups, and international businesses with diverse spending patterns, complex entity or storefront management, or a need for built-in crypto infrastructure alongside their primary financial workflows. Slash's target industries and users include:

- Ecommerce operators and wholesalers

- Contracting companies

- Healthcare suppliers

- Web3-native companies

- Travel, affiliate marketing, and ticketing agencies

- Unincorporated businesses outside the U.S.

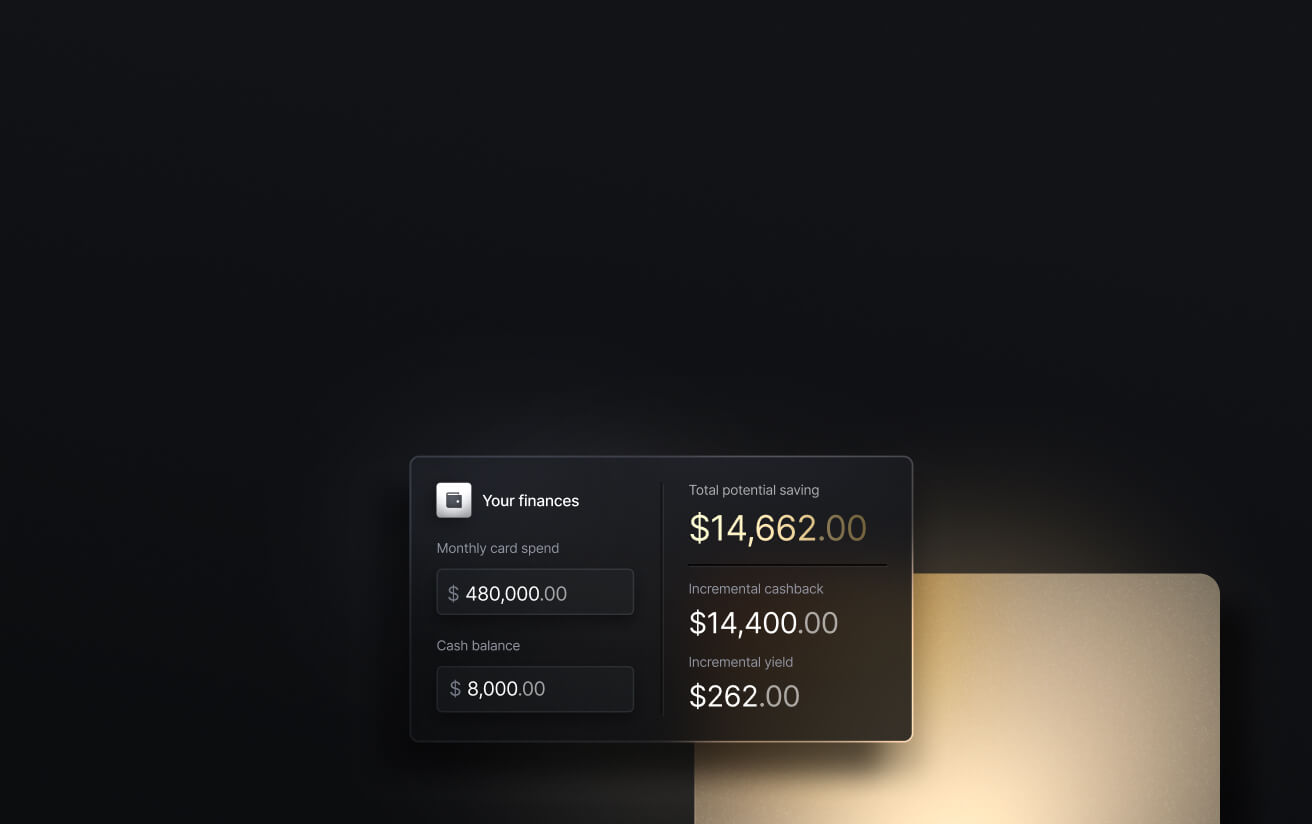

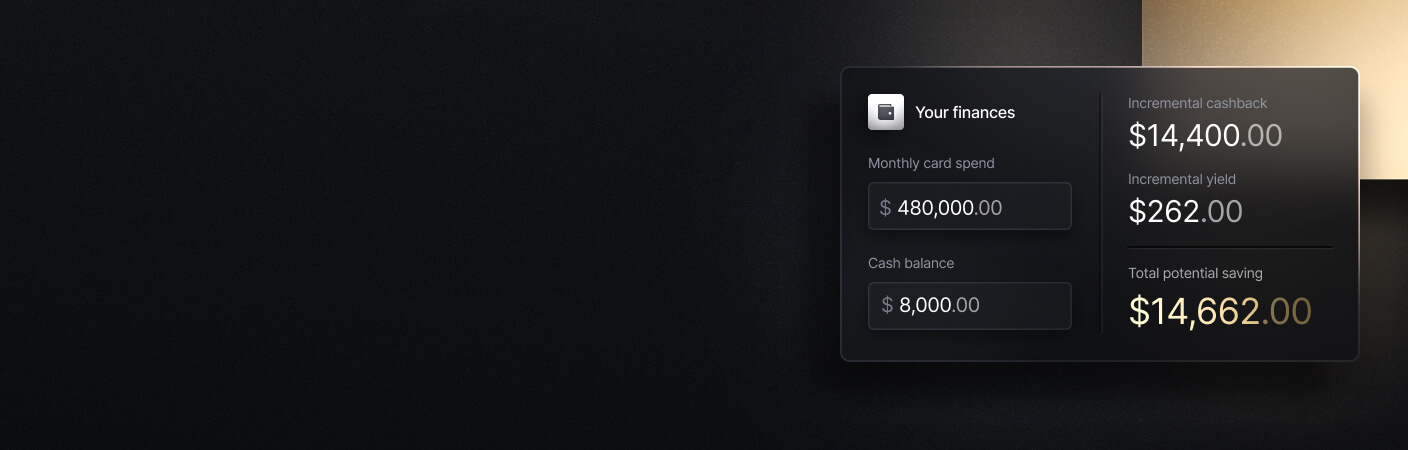

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What are the differences between Bluevine, Mercury, and Slash?

Headline features only tell part of the story. To get a clearer picture of how Bluevine, Mercury, and Slash compare, it can help to look at the specifics side-by-side. Here are some of the most notable differences across the three platforms:

Virtual account management

Slash offers unlimited virtual subaccounts and full multi-entity support at no additional cost on either plan, a major advantage for businesses running complex operations across multiple entities. Mercury is competitive here too, offering up to 100 checking or savings accounts at no extra charge, but falls short on multi-entity management. Rather than a unified dashboard, separate entities each require their own account and login. Bluevine lags behind both, capping Standard plan users at just 5 subaccounts and charging $95/mo for Premier to access up to 20.

Payment capabilities

Slash supports the broadest range of payment methods of the three: charge cards, global ACH, domestic and international wire, RTP/FedNow, and stablecoin payments using USDC and USDT. Bluevine and Mercury both cover the basics: card, ACH, wire, and check mailing. Neither offers real-time rails or crypto payment capabilities, both of which are increasingly relevant capabilities for modern businesses that want improved vendor payment turnaround or those operating across borders.

Included expense management features

Slash offers full platform functionality on its free plan, giving all users access to treasury accounts, crypto wallets, and complete expense management tools at no additional cost. Users can generate custom invoices with embedded payment links, integrate with leading accounting software and third-party tools, manage employee reimbursements, and access data-driven analytics on company cash flow and spending patterns. Both Bluevine and Mercury gatekeep some of their more functionality behind paywalls or balance minimums, whether that's full invoice management or treasury access.

Card structure

Both Slash and Mercury offer charge cards. Unlike a credit card, a charge card cannot carry a revolving balance month to month, meaning the full balance is due at the end of each billing cycle. Mercury's card earns up to 1.5% cash back, while Slash's Visa Platinum earns up to 2%. Bluevine, on the other hand, offers a debit Mastercard tied directly to the checking account balance. Rather than a proprietary rewards program, Bluevine routes its perks through the Mastercard Easy Savings program, which offers discounts at select merchants rather than straightforward cash back.

Bluevine vs. Mercury vs. Slash: Key criteria to choose the right business banking platform

When evaluating operational fit, the right platform depends on more than price or headline features. Here are the key features and capabilities to assess when deciding which banking solution makes the most sense for your business:

Platform accessibility

Based on the signup requirements and product focus, each of the three platforms cater to slightly different company profiles. Slash is the most accessible of the three, offering viable plans for small businesses, full-scale enterprises, and even unincorporated foreign businesses that neither Bluevine nor Mercury can accommodate. Bluevine skews toward small business owners and freelancers with straightforward banking needs, while Mercury is oriented around domestic startups and tech companies with room to scale.

Cross-border capabilities

Slash is the winner here, too. Slash’s Global USD accounts enables foreign founders without an incorporated US entity to access USD banking, a capability that neither Bluevine nor Mercury can match. Plus, Slash’s support for USDC and USDT enables your business to send near-instant, low cost transfers globally that bypass the fees and delays associated with traditional cross border transfers. While Bluevine and Mercury both support international wires, neither offers crypto-compatible infrastructure or the same level of accessibility for businesses operating primarily outside the U.S.

Reliance on cash and checks

If you’re looking for a platform that supports using cash and checks, then Bluevine is likely the best fit. Bluevine is the only one of the three platforms that supports check mailing and cash deposits via Green Dot locations and MoneyPass ATMs. Mercury offers check mailing, however does not cash deposits.

Lending and financing options

All three platforms offer some form of lending or working capital financing, but they differ in scope. Bluevine has the most credit offerings, with a line of credit, term loans, and access to SBA loans. Mercury offers working capital loans and venture debt. Slash offers working capital financing in the form of a tailored line of credit you can draw from whenever you need additional liquidity, with flexible 30, 60, or 90 day repayment terms that can be structured around your cash flow.⁵

Treasury access

Both Bluevine and Mercury require significant minimum balances to access their treasury accounts, which can make them less accessible for smaller businesses. Slash treasury accounts are backed by Morgan Stanley and BlackRock money market funds and require no minimum balance, giving businesses of any size the ability to put their idle cash to work from day one.

Make the right financial move with Slash

Bluevine and Mercury can both replace a traditional bank, but neither extends beyond traditional banking in the way Slash does. Instead of treating advanced capabilities as add-ons or premium upgrades, Slash brings them together in a single, cohesive platform built for modern businesses.

Whether you’re managing multiple entities, moving money across borders, operating a crypto-native company, or simply looking for a more powerful banking solution without an enterprise price tag, Slash can deliver where it matters most. Here’s what you get with Slash:

- Slash Visa Platinum Card: Earn up to 2% cash back on company spending, issue unlimited virtual cards, and set granular controls to restrict spending by category, merchant, or limit.

- Diverse payment methods: Send global ACH and wire transfers to more than 180 countries and move money domestically in real time through RTP and FedNow. Pro users pay no additional per-transaction fees.

- High-yield treasury: Earn 3.84% APY on idle cash through treasury accounts backed by Morgan Stanley and BlackRock money market funds.

- Native cryptocurrency support: Hold, send, and receive USD-pegged stablecoins such as USDC and USDT across eight supported blockchains for faster, lower-cost global payments.

- Separate virtual accounts: Create unlimited accounts to separate funds by project, department, or client, with real-time visibility across balances.

- Accounting integrations: Sync transactions directly with QuickBooks to keep records updated automatically.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

Is Mercury FDIC insured?

Yes, funds held in Mercury accounts are eligible for FDIC insurance through Mercury’s partner banks. Coverage applies up to applicable limits per depositor, per insured bank, subject to standard FDIC rules.

What is a Sweep Network and How Does it Work?

Does Bluevine pay interest?

Yes, Bluevine offers interest on eligible checking balances, up to certain limits and subject to account requirements. Rates and qualification criteria may vary, so businesses should review current terms before opening an account.

The Top 7 Platforms for Integrated Treasury, Forecasting, and High-Yield Accounts

Can Mercury accept cash deposits?

No, Mercury does not support direct cash deposits since it operates as a digital-first banking platform. Businesses that handle cash typically need to use an external bank or third-party service to deposit funds before transferring them to Mercury.

Read more from us