How to Start a Crypto Business: Requirements, Steps, and Setup

When launching their own companies, entrepreneurs often want to stay on the cutting edge of modern trends and technologies. For some, this means integrating cryptocurrency into their B2C and B2B payment processes. For others, this means building a business around crypto itself.

Starting a crypto business can mean navigating complex laws, establishing custom-built financial infrastructures, and implementing operational processes that satisfy both auditors and users. There are quite a few ways to enter the crypto market, from constructing helpful tools to creating your own exchange. Since each option usually involves evolving regulations and technologies, developing a plan ahead of time can save new founders a lot of stress.

This guide operates as a roadmap for entrepreneurs who want to start a crypto business. Below, we’ll discuss crypto business models, legal requirements, day-to-day operations, and more. We’ll also take a look at Slash, a neobank that not only supports native stablecoin payments, but can help founders from any industry navigate the financial landscape of building a company from scratch.¹, ⁴

Crypto Glossary

Here’s a quick glossary to get you up to speed on some important terms before we break everything down:

- Cryptocurrency: A form of digital currency that can be used for both electronic payments and as a store of value. Cryptocurrencies use cryptography to secure transactions and record them on a public ledger.

- Stablecoins: Virtual tokens designed to maintain price stability, usually by being linked to an underlying fiat currency. The two most popular stablecoins in use today are USDC (Coin) and USDT (Tether), which are both pegged 1:1 to the U.S. dollar.

- Fiat currency: Federally-issued money that is declared legal tender, such as the U.S. dollar or the Euro. The value of fiat currencies comes from their issuing government and central bank instead of a physical commodity like gold.

- Blockchain: A decentralized ledger that records and verifies transactions across a network of computers rather than relying on a centralized authority. Once a transaction is confirmed and added to the blockchain, it becomes very difficult to alter. This structure allows payments to be verified and settled without relying on an intermediary like a correspondent bank.

- Decentralization: The transfer of control and decision-making from a centralized entity (like a bank or government) to a distributed network of participants. Decentralization ensures no single entity controls the blockchain, enhancing censorship resistance, security, and trustless operation.

- Smart contracts: Self-executing contracts that automatically enforce agreements when predetermined conditions are met, such as terms agreed upon by buyers and sellers. This means human intervention and third-party verification aren’t required.

- Custody services: The secure storage and management of digital assets on behalf of a customer. A custodial service holds a user’s private keys and controls their funds, while a non-custodial service gives the user full control.

- Decentralized Finance (DeFi): A blockchain-based financial system that removes intermediaries like banks and brokers, allowing users to lend, borrow, trade, and earn interest directly via smart contracts.

What Qualifies as a Crypto Business?

A crypto business is any company that provides services related to digital assets, blockchain technology, or cryptocurrency transactions. These businesses typically fall into several distinct categories, each with their own regulatory implications and operational requirements.

- Exchanges facilitate the buying, selling, and trading of dozens of the most popular cryptocurrencies. These platforms match buyers with sellers, maintain order books, and often have high liquidity pools. Exchanges face heavy regulatory scrutiny because they typically take custody of user funds and operate as financial intermediaries.

- Wallets allow users to store, send, and receive digital assets. Custodial wallets take charge of a user’s security processes, while non-custodial wallets let the user hold their own keys and passwords. Wallets can also be "hot" (storing crypto on internet-based servers) or "cold" (storing crypto on hardware like drives).

- Payment processors enable businesses to accept cryptocurrency as payment for goods and services. These companies handle the complexity of receiving crypto payments and often provide instant conversion to fiat currency via on/off ramps. Crypto payment processors can be used by small merchants and global corporations alike.

- Infrastructure and tools can include node operators, API providers, blockchain analytics platforms, developer tools, and smart contract platforms. These make up the underlying technology that other crypto businesses depend on. These types of companies can face lighter regulatory requirements because they don't take direct control of user funds or financial transactions.

Choose Your Crypto Business Model

At the same time you choose your type of crypto business, you’ll be determining your business model. This comes in the form of a few decisions, including:

B2B vs B2C

Your company will either sell their product to other organizations or to individual customers. This will inform your customer acquisition strategy, sales cycle, and revenue model. B2B crypto businesses typically include payment processors and infrastructure providers that build APIs and compliance tools. B2C services can include wallets and public exchanges, but these two products can also be marketed with a B2B tilt.

Infrastructure vs product

Infrastructure businesses build the rails other companies use, such as node services, blockchain indexers, or development frameworks. These companies often require deep technical expertise to create, but may face less direct competition. Product-based businesses create end-user experiences built on existing infrastructure. Products can be easier to understand and market, but often live in a more crowded field. Ultimately, your choice of business will inform this decision.

Custody vs non-custody

Any crypto service that handles user funds, such as wallets, will be either custodial or non-custodial. Most crypto exchanges also face this decision, as exchanges often come with built-in wallets. Since custodial businesses hold user funds, they’ll often need robust security infrastructure, insurance, regulatory licenses, and extensive compliance guidelines. Non-custodial wallets let users control their own keys, usually reducing regulatory requirements and operational complexity. Both types of wallets have a similar market share, so your personal decision may depend on the regulations and compliance you’re willing to follow.

Traditional Crypto vs Stablecoins

Digital tokens come in two main forms: exchange-traded cryptocurrencies like Bitcoin and Ethereum, and stablecoins like USDT and USDC. Cryptocurrencies can be used for trading, long-term investments, and payments, while stablecoins are typically reserved for larger B2B transactions where stability is valued. Knowing what your product or service can offer to customers can help you decide which digital tokens you’ll support. Companies that work with stablecoins may want to utilize a platform like Slash that uses built-in on/off ramps to easily convert them to and from fiat currency.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Legal and Regulatory Requirements

Launching your own startup brings its own set of regulation and compliance guidelines that don’t necessarily relate to crypto itself, including:

Business structure

Before officially forming an entity, businesses must choose the structure that works best for them. Two of the most common options for new companies are LLCs and corporations. LLCs offer flexibility through limited liability protection, simplified governance, and profits that pass through to the LLC owner’s tax returns. With an LLC, a founder’s personal assets are protected against outstanding business debts.

A corporation is a separate legal entity that provides a more rigid structure that’s suitable for raising capital, though they face stricter compliance rules and can face double taxation (corporate tax + dividend tax). Corporations can be “C-Corps”, which allow for unlimited shareholders and easier access to investors, or “S-Corps” which offer limited liability protection without double taxation.

Corporations may be right for a crypto business that’s interested in expanding in the future and attracting investors, while an LLC may fit a business owner that values limited liability protection and pass-through taxation.

Required licenses and registrations

U.S.-based crypto wallets, exchanges, and payment processors are considered Money Services Businesses (MSBs). This means they must register with FinCEN, the U.S.’s Financial Crimes Enforcement Network, using FinCEN Form 107. Crypto businesses also face a wide variety of state-level requirements. Most states require money transmitter licenses, which often entail deep background checks and proof of capital reserves. Some states come with their own crypto-specific licenses, like New York’s BitLicense, which places regulations on crypto-based businesses. These regulations are particularly rigorous – in fact, after the BitLicense was introduced in 2015, ten different Bitcoin companies halted operations in New York entirely.

Know Your Customer (KYC) and Anti-Money Laundering (AML)

Whether they work with fiat currency or crypto, financial institutions are held to Know Your Customer and Anti-Money Laundering regulations. KYC checks verify customer identity through government-issued ID numbers, proofs of address, and biometric authentication. Large transactions may trigger enhanced due diligence, which requires additional documentation about the funds and business purpose in order to guard against fraud.

KYC checks are a significant part of AML processes, which aim to prevent suspicious or illegal transactions from making the journey from sender to receiver. To do this, AML initiatives monitor transfers, report suspicious activity, and uphold risk-based compliance frameworks. The Anti-Money Laundering Act of 2020 specifically expanded regulations to include cryptocurrency exchanges and other non-traditional methods of financial transfer. Crypto businesses that hold and exchange funds are responsible for detecting suspicious activity on their platforms and reporting it to regulators like FinCEN.

Building Your Infrastructure

Cryptocurrency infrastructure is a topic that can get very technical, and may require more in-depth research than we can fit within this article. Here’s an overview of the different aspects of building crypto infrastructure:

Blockchain Integration

Most crypto businesses will decide in their early stages which blockchains they’ll integrate with and support. If you intend on working with Bitcoin, which only operates on one blockchain, that blockchain may be all you need. However, most exchanges and wallets integrate with a variety of cryptocurrencies and blockchains, such as Arbitrum, Solana, and Tron. Founders may also ask themselves whether they’ll deploy their own smart contracts or integrate with existing protocols. Ethereum, the industry’s largest blockchain, is well-known for its support for smart contracts.

Wallets and Custody Decisions

The choice of custody isn’t the only decision that crypto wallet creators have to make. Crypto wallets can also be “hot” or “cold”, which determines how and where digital assets are stored.

Cold storage keeps private keys completely offline using hardware security modules or air-gapped networks. This provides maximum security for large treasury holdings, but makes frequent transactions impractical. Hot wallets keep keys online for quick operational access, but can face higher security risks. If you’re developing a wallet, your choice may partly depend on your access to physical resources and storage. If you’re a business looking to choose a wallet, it may be smart to work with a combination: cold wallets for treasury and hot wallets for operational needs.

APIs and Backend Systems

An API is a set of rules and protocols that allows software to communicate and exchange data with other software. The utilities for APIs are nearly endless, but in the case of crypto, you may focus on APIs that process payments, track transactions, and connect with DeFi protocols or other crypto services.

Transaction monitoring may require robust indexing infrastructure. Blockchain data doesn't fit traditional database patterns, as events must be processed from blocks as they're mined, reorganizations can invalidate recent transactions, and queries differ from typical applications. Purpose-built indexing services can help solve these challenges, but may require ongoing maintenance.

Security Considerations

It’s important to conduct regular security audits to protect your digital assets, comply with securities law, and maintain trust with investors and users. Business owners may hire professional auditors to review code for common vulnerabilities, attacks, and edge cases. They can also use hardware security modules (HSMs), which are tamper-resistant physical devices designed to securely generate, store, and manage cryptographic keys. For all other financial operations, it’s generally wise to implement strict access controls with multi-party approval and maintain detailed audit logs.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Set Up Day-to-Day Financial Operations for Your Crypto Business

Financial operations in crypto businesses can be unique, as you’ll often be working with an even mix of fiat currencies and digital tokens. Here are some best practices for managing your day-to-day finances:

Set up accounts to hold fiat and crypto

Many crypto businesses may find themselves struggling to manage their fiat currency and their digital currency at the same time. They could open a bank account, adopt an accounting software, and get both hot and cold wallets, but fractured solutions can cause more headaches than they’re worth. Slash can help bridge that gap.

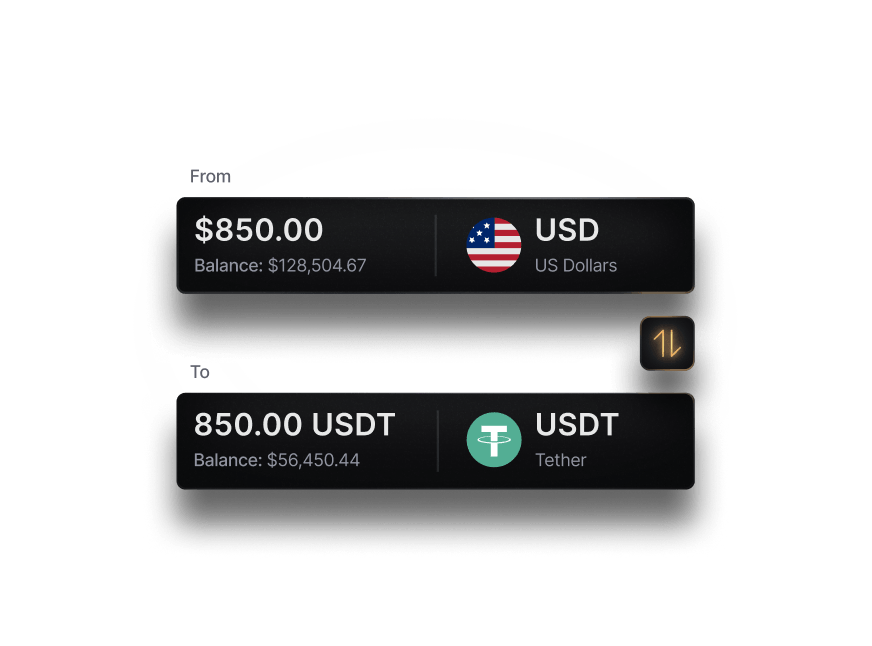

With Slash, users can hold fiat currency and stablecoins alongside one another and monitor both on the same dashboard. While Slash as a platform is not a digital wallet, we do give our users access to a custodial wallet that isn’t connected to an exchange, and can be used for payments and native cash conversion. Slash supports USDC, USDT, and its own U.S. Treasury-backed stablecoin USDSL.³

Define when and how to convert crypto to fiat

The actual process of converting crypto to fiat and vice versa can be simple, especially with a platform like Slash that offers built-in on/off ramps. However, business owners also have to determine when and why they’ll convert their currencies. Some companies may convert all newly-received crypto to fiat immediately to eliminate price volatility risk. Others can hold strategic crypto treasuries or pay expenses directly in stablecoins. The right approach depends on your business model, cash flow needs, and risk tolerance.

Choose how to send and receive payments

Working with both fiat currency and digital tokens means outgoing payments often come with extra options. When should you send funds through traditional rails like ACH or wire, and when should you send funds with stablecoins or over the blockchain?

If you’re making payments to vendors or business partners, it may be best to default to their preferences, especially when their infrastructure doesn’t support crypto. If both fiat and crypto are available for certain payments, though, the fast settlement times and low transaction fees of stablecoins may be worth considering.

Track your balances and funds

Financial management for crypto businesses means monitoring balances and payments across wallets, exchanges, and accounts. It looks a little different from typical financial management, but it follows the same core principles. Business owners should compare exchange statements to internal records, verify that on-chain balances match wallet tracking, and confirm fiat account balances against accounting system entries.

Common Mistakes When Starting a Crypto Business

Launching a crypto business can be tricky, especially given its extra regulations and complex technical structures. Knowing what not to do can be just as helpful as knowing what to do. Here are some mistakes to avoid:

- Ignoring compliance early can be costly, both due to legal fines and future fixes. Companies that operate without required licenses or skip KYC/AML implementation may find it difficult to secure banking relationships, raise institutional capital, and avoid regulatory penalties.

- Discounting the importance of security has serious implications for both you and your customers. Your own assets could be compromised due to a lapse in security that would have otherwise been caught in an audit. If you manage custodial wallets and your customers’ data and crypto gets stolen in a hack, you’ve got a disaster on your hands.

- Building before validating demand is a bad business decision in any industry. If you’re looking to create a bespoke tool that helps a specific sector of users, it’s smart to speak with potential customers first to find out what they’d value in the product. You can also build an MVP (Minimum Viable Product) to test core features against client interests.

- Underestimating operational complexity can be common among newcomers to the crypto world. Simply put, digital assets and blockchains are very complex. Running a crypto business often requires coordinating traditional financial operations, blockchain infrastructure, coding knowledge, regulatory compliance, security operations, and customer support simultaneously. Many of these areas call for specialized expertise that new founders may not have off the bat.

Operating and Scaling a Crypto Business After Setup

So you’ve launched your crypto startup. If your initial operations are running smoothly, then it’s time to start looking ahead at growth and expansion. Scaling a crypto business, however, can be a little trickier than scaling your average company.

This is partly due to regional and global differences as your business crosses borders. While traditional U.S. state regulations often only apply to companies that form or operate storefronts in a state, virtual currency regulations may apply to your business no matter where you’re based. For instance, New York’s BitLicense compliance requirements apply to crypto activities involving New York or its residents. As soon as you get your first New York customer, your business must follow those regulations.

Companies looking to expand overseas may encounter the European Union’s MiCA (Markets in Crypto-Assets) regulation, which requires stablecoin issuers to obtain authorization, hold full reserves, undergo regular audits, and redeem at face value. Japan only allows stablecoins to be issued by trust companies, licensed banks, and registered payment providers. The country with the world’s second largest economy, China, currently outlaws cryptocurrency entirely.

Another obstacle is the scalability of blockchains themselves. A blockchain’s performance will often be negatively affected by increasing workloads, participation, and use. Blockchains come with a three-way dilemma: they should be decentralized, secure, and scalable, but it’s very difficult to achieve a balance of all three. As your crypto business scales and the blockchains you use see heightened traffic, you may need to find workarounds or use alternatives that are less secure and decentralized.

A couple technical solutions are known as Layer-1 scaling and Layer-2 scaling. Layer-1 scaling involves making changes directly to the base blockchain protocol to enhance its ability to handle more data, while Layer-2 scaling is the act of building additional protocols on top of the main blockchain to offload transaction processing. Business owners with a deep level of crypto expertise can turn to these options to open their blockchains up to extra traffic.

Run Your Crypto Business Operations With Slash

Launching your own crypto startup often requires in-depth knowledge about cryptocurrency, finance, and business practices. At Slash, we can help founders out with all three.

Slash is a neobank that offers financial management tools built to help first-time founders from any industry. Our dashboard displays employee spend, virtual accounts, financial analytics, incoming/outgoing payments, and more in one spot. Enhanced visibility into cash flow can give busy startups a clearer picture of their finances as their operations speed up.

For crypto businesses that exchange both fiat currency and crypto, Slash users can send USDT and USDC using eight different blockchains, including Ethereum, Solana, and Base. Users can then convert their digital token of choice into fiat currency using dedicated on/off ramps, with fees often less than 1% per transaction. Our platform also supports a diverse range of fiat payment rails, including card spend, global ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

Other Slash features that can help startups better manage their finances include:

- Accounting integrations: Our platform integrates with accounting systems like QuickBooks Online, Xero, and Sage Intacct. Transaction data syncs automatically, reconciliation happens in real time, and finance teams maintain complete visibility without having to work across multiple fractured systems.

- High-yield treasury accounts: Earn up to 3.83% annualized yield on idle funds through money market investments backed by BlackRock and Morgan Stanley.⁶

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. U.S. users can also earn up to 2% cash back on business purchases.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

We know how important it is for startups to streamline the tracking and movement of their money, whether it’s found in a physical wallet or a digital one. Slash can help users do both on one platform.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

How long does it take to get approval for crypto business licenses?

This largely depends on the region. For example, Canada's registration-based system typically takes 1-3 months, while the EU's strict regulations can lead to the process taking up to a year.

How do teams standardize reporting across crypto and traditional financial systems?

Business owners can use platforms like Slash that integrate with accounting platforms to align overall financial reporting. Slash syncs two-ways with QuickBooks Online, Sage Intacct, and Xero.

Crypto Accounting Guide: Workflows, Compliance & Best Software

Crypto Tax Guide for Businesses: Reporting, Calculating, Complying

What is crypto trading, and what business models work for crypto investors looking to try it?

Crypto trading is the act of buying and selling different types of coins and tokens in a similar way to stocks. Exchanges and digital wallets are both commonly utilized when trading cryptocurrency.

Read more from us