Multi-currency E-commerce: Managing Global Payments, Settlements, FX, and International Payment Processing

It's a reasonable assumption: offering products to more countries means reaching more prospective customers. For e-commerce businesses, positioning your storefront in the global marketplace opens access to a multi-trillion-dollar market. In practice, multi-currency e-commerce helps localize pricing and supports growth across regions.

But international expansion also brings added operational complexity; with increased sales potential comes a jumble of global payment infrastructure, processing considerations, and legal requirements that can quickly become difficult to manage without proper preparation.

Before your business sells anything overseas, one of the most important areas to plan for is global payment management. Accepting payments from different countries comes with added complications: currency conversion fees and international payment processing costs can chip away at margins, multi-currency checkout flows can confuse customers when prices shift between currencies, and outdated tools can make it harder to move funds quickly and cost-effectively. Over time, these issues can affect more than your bottom line. They may strain supplier relationships, complicate the customer experience, and pull attention away from growing your store.

In this guide, we explain how e-commerce businesses can simplify sending and receiving global payments, with a focus on where issues commonly arise in multi-currency management and FX risk management. We also highlight the benefits of using Slash for international payments, including native crypto rails, SWIFT wire transfers to over 180 countries in 135+ different currencies, and expense management tools built to support cross-border transactions.⁴ With Slash, global payments can become a competitive advantage, not an operational burden.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How do e-commerce platforms typically handle payment processing in multiple currencies?

Payment processing refers to the behind-the-scenes systems that enable a business to accept payments from its customers. In international payment processing, when a buyer clicks "Buy Now" at checkout, payment details are securely sent to a payment gateway, routed through a payment processor, and passed to the customer's issuing bank for authorization.

The payment gateway serves as the interface where customers enter and verify their payment information, which the payment processor connects issuing banks, acquiring banks, and payment networks. If the issuing bank approves the transaction, it moves into settlement, where funds are transferred through the payment network and ultimately deposited with the merchant.

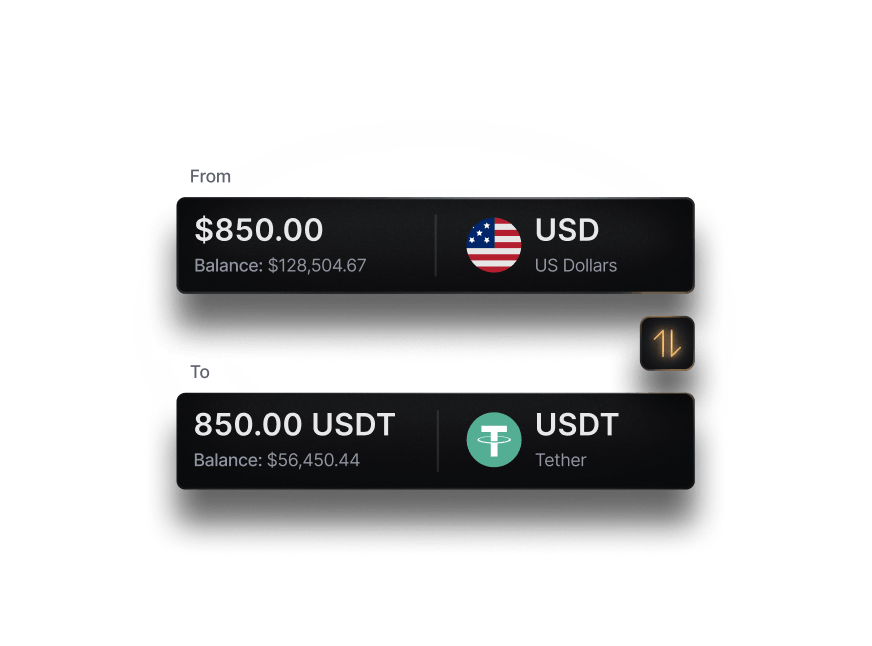

In multicurrency transactions, currency conversion can happen at several different points in this process. In some cases, the payment processor converts currencies before settlement. For card payments, the card network may perform the conversion on behalf of the issuing bank. In other setups, the business receives the foreign currency directly and converts it later using multicurrency accounts for businesses or treasury management tools. Because conversion can occur at multiple stages, the currency involved in an international transaction is often described using three distinct terms depending on where conversion occurs:

- Presentment currency: The currency shown to the customer at checkout.

- Charge currency: The currency the customer's payment method is actually charged in.

- Settlement currency: The currency the merchant ultimately receives.

Even when the issuing bank does not handle the conversion itself, it may still charge fees to cover cross-border processing costs, network fees, and currency risk. FX fees, sometimes called currency conversion fees, refer to the markup applied to the exchange rate used during conversion, commonly known as the FX spread. Foreign transaction fees, by contrast, are separate charges applied by issuing banks or card networks for processing cross-border payments, regardless of whether a currency conversion occurs. Understanding how these fees differ makes it easier to identify where costs are introduced within the payment system.

What are multi-currency payments used for?

Setting up a multicurrency payment processor on your storefront often goes hand in hand with building cross-border payment infrastructure for your business. While the setup can be more complicated than a domestic banking arrangement, it can unlock meaningful operational benefits. Below are some of the most common use cases for multicurrency payments and how they support global commerce:

Processing payments from customers

Multicurrency payments allow customers to pay in their local currency at checkout while businesses get paid in their preferred currency. The payment processor handles routing, conversion, authorization, and settlement behind the scenes. Implementing multi-currency checkout can reduce friction by presenting clear, localized pricing.

B2B payments to overseas partners

Businesses use multicurrency payment systems to both send and receive payments to vendors, suppliers, and contractors in different countries. There are many different methods for sending payments across borders, including:

- International wires on the SWIFT network

- Global clearing house transfers

- Cryptocurrency transfers on the blockchain

- Closed-network digital rails.

Depending on the banking setup of your suppliers and partners, different payments work better in different scenarios.

Remittances

In the context of global payments, remittances refer to payments sent from an individual working overseas back to a bank account in their home country. Sending remittances is common for international contractors or employees working on-site at a foreign subsidiary.

Funding foreign subsidiaries

Parent companies with international entities use multicurrency payments to move capital between its foreign subsidiaries. These transfers often involve treasury workflows and must comply with local reporting and regulatory requirements.

Making investments in international markets

Multicurrency payments allow businesses to invest abroad without converting funds too early. Companies may hold funds in foreign currencies temporarily or convert them at the time of execution.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

What competitive advantages and drawbacks do businesses gain by offering multicurrency capabilities?

Multicurrency capabilities can support the next stage of growth for many businesses, but they also introduce new challenges that require thoughtful preparation. Understanding both the benefits and the tradeoffs can help your businesses implement global payment support more effectively:

Advantages of multicurrency capabilities

- Creates a smoother and more trustworthy customer experience at checkout by allowing buyers to pay in their localized currency and preferred payment method.

- Can reduce cart abandonment rates by eliminating some of the customers' uncertainty about pricing.

- Expands access to new international markets, products, and services. Improve relationships with overseas vendors by meeting their payment preferences, opening the door to more favorable contract negotiations and improved product delivery timelines.

- Makes it easier to hire employees and contractors overseas and manage payouts.

Disadvantages of multicurrency capabilities

- Increases exposure to FX risk, which can negatively affect margins when exchange rates move unexpectedly. Platforms with stablecoin support, like Slash, can minimize FX exposure by enabling blockchain transfers that settle in minutes, minimizing the chances of currency values moving against you in transit. Strong FX risk management policies further reduce volatility.

- Adds complexity to reconciliation and accounting, as charge and settlement currencies may be difficult to manage without automated conversion and matching. Slash can simplify month-end close by integrating global payment data directly into QuickBooks.

- Can introduce additional costs, including currency conversion fees and foreign transaction fees. Slash can help reduce these costs with native stablecoin support, cost-efficient bank transfers, and a low 1% or $0.40 FX fee on the Slash Platinum Card.¹

What challenges might businesses face when implementing multicurrency e-commerce?

For e-commerce storefronts, there are additional considerations to account for before selling products in the global marketplace. Expanding internationally without the right infrastructure can lead to accounting discrepancies, profit margin losses, strained supplier relationships, and more. Here are 6 key challenges to consider before selling your products overseas:

Transactional FX risk

FX risk refers to potential losses caused by fluctuations in exchange rates while payments are authorizing, settling, or in transit. For businesses processing large volumes of cross-border transactions, these shifts can add up over time, making FX risk management a core operational priority.

Some companies use forward contracts to hedge exposure, but these tools add operational overhead and only partially mitigate risk. Leveraging crypto can be a more effective hedging strategy against FX risk; since transfers settle in minutes, you can limit the amount of time that currency values can shift against you.

Slash natively supports holding and transferring USD-pegged stablecoins like USDC and USDT, allowing businesses to transact globally while minimizing FX exposure.

Reconciliation across different currencies

Reconciliation is the process of comparing financial records from multiple systems to ensure that recorded inflows and outflows match over a given period. When transactions occur in different currencies between the charge and settlement, reconciliation can become significantly more complex.

Many teams may manually convert foreign-currency transactions into a base currency using historical exchange rates or rely on spreadsheets to track FX gains and losses. This approach can be time-consuming, error-prone, and difficult to scale as transaction volume grows.

Slash can pair with QuickBooks to automate this process, syncing your global payment data and eliminating manual reconciliation work.

Refunds and disputes

Refunds introduce a second round of currency conversion and processing fees that can cut into your margins. If exchange rates shift between the original purchase and the refund, businesses may run into transactional FX risk, causing a return of more or less value than originally received. This added chance for fluctuation can also create accounting discrepancies as there's added room for error in reconciliation. Clear policies for multi-currency checkout and visibility into currency conversion fees can reduce surprises for customers and merchants alike.

Settlement timing and managing vendor relationships

Settlement timelines vary widely depending on payment method and destination country. International wires and bank transfers can take days or weeks to reach vendors, particularly when intermediary banks are involved. Delayed payments can slow production, frustrate suppliers, and strain long-term partnerships.

Using a payment platform that supports multiple payment rails and automated approvals, like Slash, allows businesses to choose faster options when timing is critical and helps ensure vendors are paid accurately and on schedule.

Compliance with international financial regulations

Operating across borders requires navigating complex financial regulations that vary by country and payment type. Businesses must account for KYC and AML requirements, local payment rules, tax considerations such as VAT or GST, and reporting obligations tied to cross-border transfers.

Slash is a SOC 2 Type II certified financial institution with full compliance for KYC, KYB, and AML requirements for sending payments worldwide. Additionally, stablecoins like USDC are MiCA compliant assets, making them usable for crypto payments in and out of Europe.

Disconnected financial systems

Managing multicurrency payments across a patchwork of disconnected tools can increase manual workload and make it difficult to understand your true cash position across currencies.

Slash unifies your finances into one powerful platform, consolidating global payment rails, invoice management, accounting synchronization, virtual bank accounts, card controls, and treasury management. With a centralized hub for all your financial operations, you can make data-driven decisions to improve cash flow management and identify opportunities to reduce fees in your global payment flows.

What are the best practices for implementing multicurrency payment options?

E-commerce businesses are not powerless against the risks of selling internationally. With proper preparation and access to modern financial tools, global payment operations can become easier to manage and more predictable. Here are some ways to improve how you implement multicurrency payments into your operations:

Simplify your invoice management

Make sure invoices clearly specify the pricing currency, the currency you expect to receive, and any applicable conversion terms. Using invoicing tools that support multiple currencies and saved payment details can reduce back-and-forth with customers, shorten payment cycles, and make it easier to trace payments during reconciliation.

Understand your FX exposure

Take time to map out where currency conversion occurs in your payment flow and which party controls the rate at each step. This visibility helps you understand when exchange rate movements affect margins and when pricing adjustments, settlement timing changes, or alternative payment rails can be leveraged to reduce unnecessary FX exposure. Treat this mapping as the foundation of your FX risk management program.

Automate accounting processes

Relying on manual reconciliation or disconnected accounting systems can increase the chance of inconsistencies over time, especially as international transaction volume grows. Accounting tools that automatically sync transaction details and FX data into your ledger can save time and improve accuracy. Slash syncs with QuickBooks to eliminate manual data entry, simplify invoice matching, and help to draft compliant expense reports or tax filings.

Centralize payment and treasury visibility

Multicurrency operations often span multiple payment processors, bank accounts, and settlement schedules. Without a centralized view, it becomes difficult to understand your true cash position, monitor fees, or plan liquidity needs across currencies. Bringing payments and treasury activity into a single platform like Slash can improve visibility and support better forecasting. Over time, this clarity makes it easier to identify inefficiencies, adjust payment strategies, and scale international operations with more confidence.

Discover smarter global payment solutions with Slash

Managing multicurrency operations requires understanding where currency conversions happen, abiding by international regulations, controlling FX exposure, and moving money across borders without unnecessary delays or fees. The right combination of international payment processing tools and multicurrency accounts for businesses can streamline these workflows.

As your business expands internationally, these challenges can compound without proper foresight, especially if your payments and expense management tools are spread across disconnected systems. Choosing the right financial infrastructure can significantly reduce your operational complexity and give you clearer visibility into how to optimize your global cash flow.

Slash brings global payment management into a single, modern banking platform. By combining international payment rails, crypto-native transfers, accounting integrations, and powerful spend controls, Slash helps businesses simplify cross-border operations without sacrificing flexibility. Here are some more ways Slash can improve how your business manages its finances:

- Slash Visa Platinum Card: Earns up to 2% cash back on spending (in the U.S), issue unlimited virtual or physical cards, set customizable spending limits and controls, and monitor company-wide card activity in real time from a centralized dashboard. All transactions are automatically captured for better visibility and easier reconciliation.

- Virtual accounts and expense management: Create configurable bank accounts to separate funds by purpose, region, or team. Automatically capture payment details, gain real-time insights into cash flow, enforce compliant spending policies, and sync transactions directly with QuickBooks to simplify multicurrency accounting and month-end close.

- Slash Working Capital financing: Access financing built for growing businesses directly within your Slash account. Draw funds as needed to support operations or expansion, with flexible 30, 60, or 90 day repayment terms that align with your cash flow cycle.⁵

- High-yield treasury: Earn up to 4.1% annualized yield through money market accounts backed by BlackRock and Morgan Stanley.⁶

- Global USD Account: Enable international businesses to hold, send, and receive U.S. dollars without requiring a U.S. bank account or registered LLC.³

Optimize your global payments with diverse payment methods, more effective hedging strategies, and powerful cash flow management tools with Slash today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

How does displaying prices in a customer's local currency affect the shopping experience?

Displaying prices in local currency reduces friction at checkout by eliminating the need for customers to manually calculate exchange rates. This transparency builds trust and can significantly reduce cart abandonment, as customers see exactly what they'll pay without surprises from their bank or card issuer. A clear multi-currency checkout experience further streamlines the path to purchase.

The Best International Payment Gateways for Businesses

What options do e-commerce businesses have for managing cross-border funds?

Slash offers SWIFT wire transfers to 180+ countries in 135+ currencies, native support for sending and receiving stablecoins, global ACH settlement, and real-time rails like RTP and FedNow. Slash also enables non-U.S. founders to conduct send and receive payments in USD without a U.S.-registered LLC or bank account; watch the video below to learn more. These options help simplify international payment processing.

Which banks have multicurrency accounts?

Many institutional banks and fintech providers offer multicurrency accounts that let you hold foreign currencies without converting to your home currency. These can take the form of specialized digital accounts or correspondent banking arrangements. However, multicurrency accounts don't completely eliminate FX exposure and can be complicated to implement. Slash simplifies multicurrency management by combining native stablecoin support with traditional banking rails, offering faster settlement times and lower currency conversion fees while maintaining compliance across jurisdictions.

Read more from us