6Working Capital Management Solutions Every Business Should Know to Boost Efficiency

As your business grows, so does the amount of cash you need to keep it running. More inventory, bigger supplier payments, and rising operating costs all put pressure on working capital—the cash your business relies on to function.

Growth can also make cash flow harder to track. When financial data is scattered across banks, processors, and accounting systems, it becomes difficult to see where cash is getting held up or when a strain is developing. Even strong, fast-growing companies can suddenly find themselves short on liquidity. The result is a common scenario: sales are rising, demand is strong, but cash is tight.

Working capital isn’t just about covering bills; it’s about having the flexibility to support growth without risking your company’s liquidity. That flexibility often depends on both better visibility and access to the right financial tools.

In this guide, we’ll identify the areas that can hurt your working capital and introduce strategies for improving them through automation and better decision-making. We’ll also highlight Slash’s capabilities for helping businesses optimize their financial workflows and showcase Slash Working Capital, an easily accessible financing solution that offers true 30, 60, and 90-day repayment terms. ⁵ Keep reading to learn more.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Why is Proper Management of Working Capital Important?

Working capital refers to the funds a company has available to cover short-term obligations and keep day-to-day operations running. In practice, this is the cash you use to pay employees, manage accounts payable, purchase inventory, pay invoices from suppliers, and more. It’s calculated using a simple formula:

Working Capital = Current Assets – Current Liabilities

Each component of the formula represents various types of short-term inflows and outflows. “Current” simply means within the next year. Current assets often include cash, accounts receivable, and inventory, while current liabilities include accounts payable, short-term financing, and other upcoming debts.

There are several downstream benefits to proper management of working capital, including:

- Fulfilling financial obligations: When your working capital is well-managed, you can stay current on supplier payments, take advantage of favorable payment terms, and avoid late fees or supply disruptions. This helps your business build stronger vendor relationships and improve overall cash flow stability.

- Driving growth and reinvestment: By shortening your cash conversion cycle, you free up capital that can be reinvested into growth initiatives instead of remaining tied up in daily operations.

- Maximizing capital efficiency: Properly balancing receivables, payables, and inventory ensures that you’re not over-stocking materials or waiting too long to get paid.

Managing working capital effectively ensures your business has enough liquidity for daily operations while still maintaining financial flexibility. Conversely, poor oversight can push businesses into negative working capital, leading to supplier delays, limited funds for growth, excess inventory costs, and other pressures.

Challenges and Factors Leading to Negative Working Capital

Before exploring strategies to strengthen your company’s working capital management, it’s important to identify common issues that can cause it to break down. This starts with understanding the working capital formula and how to increase your assets and cash inflows while keeping liabilities low. Below are several factors that can contribute to negative working capital:

Cash Flow Instability

When your revenue fluctuates month-to-month from seasonal demand, irregular sales cycles, or unpredictable customer behavior, it can become harder to maintain steady cash flow. If expenses remain constant while revenue dips, your business may experience temporary cash shortages that make it difficult to cover payroll, supplier payments, or inventory purchases.

Inconsistent Management of Receivables and Payables

Working capital can lower when incoming and outgoing payments aren’t properly aligned, so it’s important to keep a close eye on accounts payable and receivable. Slow customer payments, unclear invoicing processes, or paying suppliers too early can all create timing gaps. When your current assets leave the business before new funds arrive, your margins tighten, exposing you to external risks and making short-term expenses more difficult to manage.

High Dependence on Suppliers or Customers

Relying heavily on a limited number of buyers or vendors can increase financial risks and make forecasting more difficult. If a major customer pays late or a supplier changes their payment terms, your business may feel the impact immediately. Without sufficient liquidity, a single high-value partner can disrupt cash flow and create broader instability.

Inventory Inefficiencies

Holding more inventory than you need ties up valuable working capital. Slow turnover, inaccurate demand forecasting, or supplier requirements that force large minimum orders can all lead to excess stock. Over time, this can reduce liquidity and give your business less room to adapt or invest.

Excessive Short-Term Liabilities and Operational Costs

Higher supplier prices, increased labor costs, or growing short-term debt obligations can cause your available working capital to quickly shrink. Businesses with thinner margins may feel this pressure more acutely, with less cushion to absorb cost fluctuations or delays in revenue.

Limited Access to Technology and Financial Tools

Relying on manual processes for invoicing, payment tracking, and expense forecasting isn’t just time-consuming—it also can make it harder to spot working capital issues early. Automating these processes with Slash can save time and effort while giving you better visibility into your cash flow, helping you make faster, more informed decisions about managing working capital.

Finally, if your business is facing negative working capital, a good first step is to review the systems and processes that support your daily financial operations. Start by examining:

- Cash flow forecasting tools that don’t provide accurate or timely projections

- Manual workflows that create errors and could benefit from automation

- Limited visibility into accounts receivable

- Ineffective reports that make it difficult to track current assets, current liabilities, or overall liquidity

What Strategies Can be Used to Improve Sorking Capital?

Pairing traditional working capital management strategies with the right technology can make the entire process faster and more efficient. From automated workflows to digital cash flow forecasting, financial platforms like Slash can help with procurement, payables, receivables, and accounting through powerful integrations. Below, we’ve outlined several ways your business can better leverage its resources and make smarter use of its cash on hand:

1. Utilize Strategic External Financing

Loans and lines of credit give businesses the short-term liquidity needed to cover major expenses without disrupting operations. With Slash Working Capital, you can draw down from a line of credit whenever your business needs it and choose flexible 30, 60, or 90-day repayment terms. This can provide improved float, steadier cash flow, and a more predictable way to manage large purchases or supplier payments.

2. Forecast Cash Flow

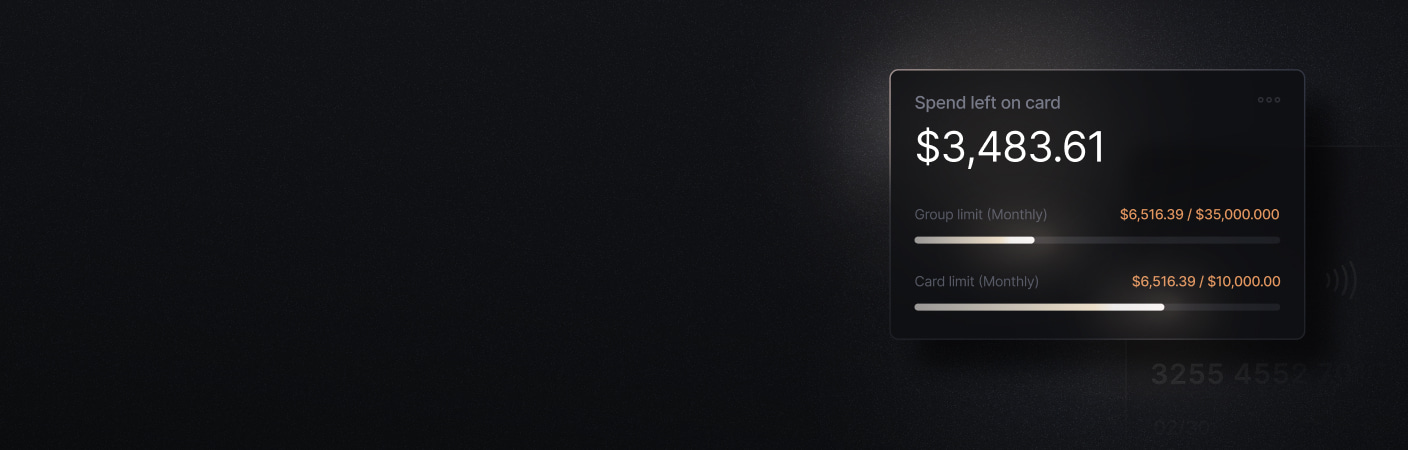

Strong visibility into your cash flow is essential for staying ahead of shortages and timing payments effectively. Forecasting tools help you anticipate when inflows and outflows will occur so you can make smarter operational decisions. The Slash dashboard provides real-time spend insights and cash flow analytics, giving you a clearer understanding of how expenses affect liquidity day-to-day.

3. Digitize Invoicing

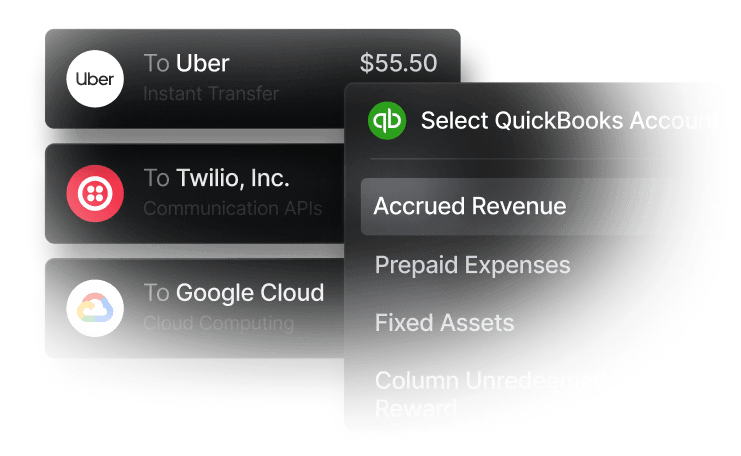

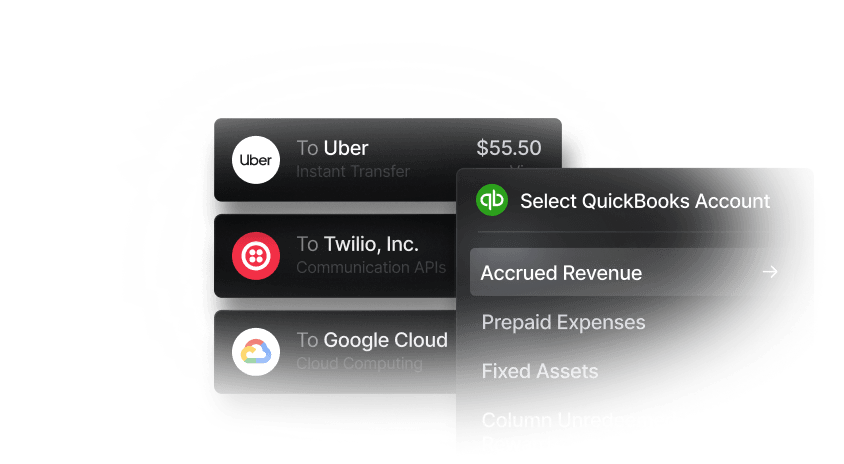

Electronic invoicing can simplify billing, reduce errors, and accelerate payment collection. Many systems can automatically generate invoices, match them to purchase orders, and keep everything organized in one place. Through its integration with QuickBooks, Slash supports these automated workflows by using AI to compile, categorize, and track invoices.

4. Leverage Dynamic Discounting

Dynamic discounting allows businesses to reduce costs by paying supplier invoices early in exchange for a lower total amount. Instead of fixed early-pay terms, discounts adjust based on how soon the payment is made, giving you flexibility to use this strategy only when your cash position is strong. When managed well, dynamic discounting lowers procurement expenses, strengthens supplier relationships, and helps you make more strategic use of surplus working capital.

5. Optimize Inventory Management

Managing inventory effectively starts with staying aligned with demand, which can help prevent cash from getting tied up in products that aren’t selling. Tracking your inventory turnover ratio can give you a clearer sense of how quickly products move and whether your current inventory strategy supports healthy working capital. A higher turnover ratio usually means your cash is cycling back into the business faster, signifying stronger overall liquidity.

6. Refine Accounts Receivable collection

Better AR collection shortens your cash conversion cycle and ensures money comes in at a pace that supports daily operations. Some ways to improve AR management is instituting clearer billing practices, timely invoicing, automated reminders, and flexible payment options. You can track your efficiency by calculating your collection ratio, which measures how quickly your business turns invoices into cash. And for companies operating across multiple brands or entities, Slash’s multi-entity support can make AR management even simpler by centralizing statements and consolidating data from different payment processors into a single dashboard.

How Does Automation Improve Working Capital Management?

Today, businesses have access to a wide range of tools that use AI, automation, and platform integrations to streamline working capital management. These solutions simplify financial processes and help teams operate more efficiently. Here are four examples of how smart tools can integrate and improve your existing workflows:

Cash Flow Visibility

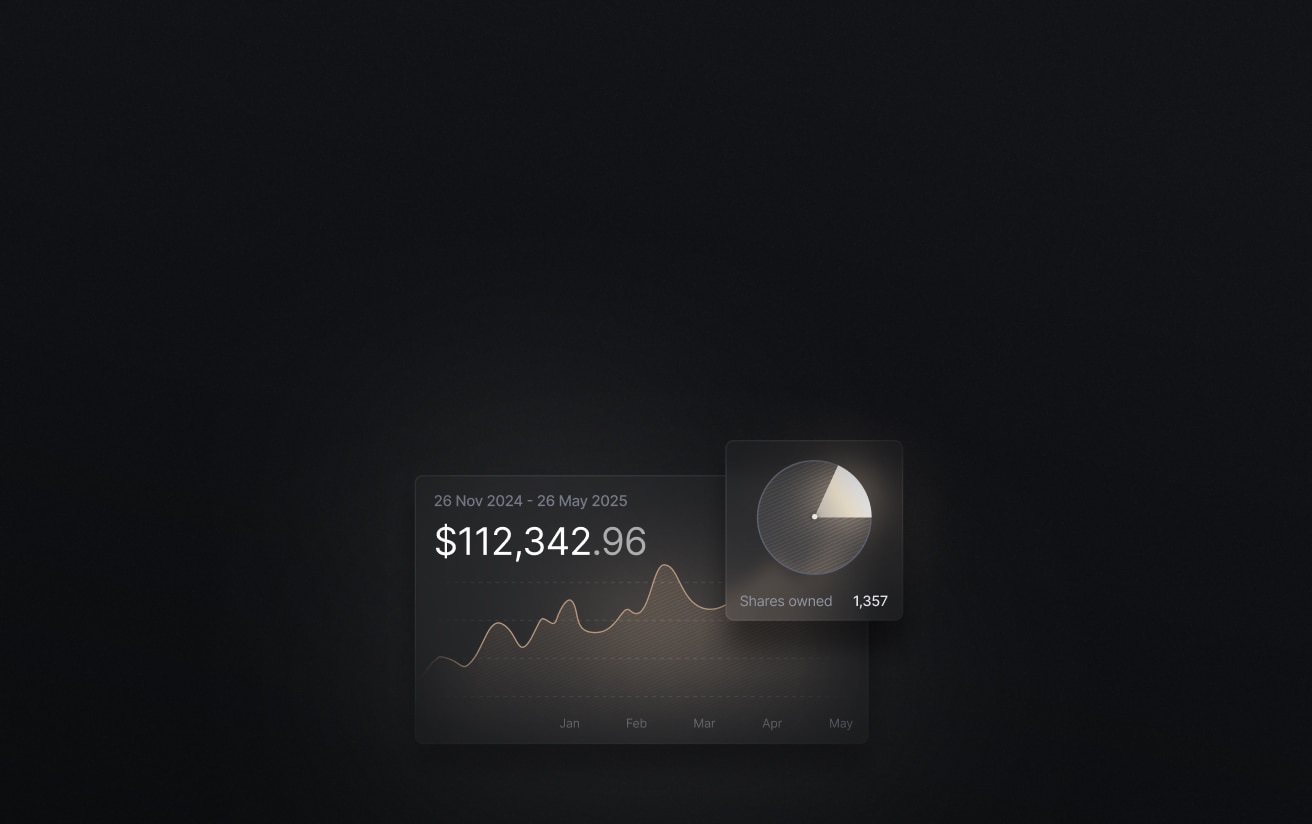

A financial dashboard like Slash that automatically tracks payments, expenses, and receivables makes it easier to understand how your business spends, where funds are going, and how to strengthen working capital. Slash provides real-time spend insights and automatically consolidates financial data from multiple entities, vendor payments, employee transactions, and more. Our analytics dashboard transforms this data into clear visual breakdowns organized by payment method, vendor, card group, and more, giving you a comprehensive view of your cash flow.

Forecasting Accuracy

Businesses track metrics like working capital, inventory turnover, and collection ratios to make informed decisions about the future. But gathering the data needed to calculate these metrics can be time-consuming, error-prone, and difficult if information is spread across different systems. A unified financial dashboard like Slash gives you a high-level view of your spending trends so you can base decisions on accurate past performance. And when paired with QuickBooks, Slash can make it easier to access the metrics you need to improve performance and plan ahead.

Accounts Receivable Management

Strong AR management helps stabilize cash flow and reduces the risk of delayed payments. However, staying on top of invoices, customer payment behavior, and outstanding balances can be challenging. Slash simplifies AR oversight with multi-entity support, which consolidates payment activity from all your business’s different subsidiaries and payment processors into one unified dashboard.

Scenario Analysis

Scenario analysis allows businesses to model how different financial decisions—such as changing payment terms, increasing inventory orders, or adjusting spending—will affect cash flow and working capital. Slash’s analytics dashboard pulls together transactions, supplier payments, entity-level data, and employee spending, giving you the information needed to run accurate “what-if” scenarios. Accessible, accurate data can help your business test assumptions, anticipate cash shortages, and make more confident decisions about budgeting, growth, and capital allocation.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Discover Smarter Capital Management Solutions with Slash

To turn strong operations into sustained growth, you need working capital tools that can keep pace with your business.

Slash Working Capital gives businesses access to a line of credit they can draw from whenever cash flow is tight. Slash lets you choose true 30, 60, or 90-day repayment terms for each drawdown. This allows you to match financing to your spending needs, pay suppliers on time, and keep more cash on hand for operations or growth. Because funds arrive in your Slash account within one business day, it’s a practical way to manage large invoices, inventory purchases, or seasonal gaps without draining your reserves.

For day-to-day payments, the Slash Visa Platinum Card offers the flexibility of a corporate charge card with powerful employee spend controls, real-time spend insights, and automated expense tracking that syncs directly with the Slash dashboard.¹ Businesses can earn up to 2% cash back on purchases, generating additional value from their company spending.

Unlock the working capital you need to accelerate your business growth. Discover how Slash’s business banking solutions can strengthen your financial foundation today.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

How to spot gaps in working capital?

Many businesses identify gaps in their working capital by tracking a few key metrics that measure performance. Relevant metrics include the working capital (or current) ratio, the inventory turnover ratio, and the collection ratio:

Working Capital Ratio = Current Assets ÷ Current Liabilities

Inventory Turnover Ratio = Cost of Goods Sold ÷ Average Inventory

Collection Ratio = (Net Credit Sales ÷ Average Accounts Receivable) * Number of Days

Working Capital Loans for Startups: Different Types and Options

What are the factors affecting working capital management?

Working capital is influenced by how quickly customers pay you, how efficiently you manage inventory, and the timing of your payments to suppliers. Seasonal sales patterns, rising operating costs, and unexpected expenses can also affect how much working capital your business has available.

What is net working capital?

Net working capital is a slightly more precise measurement of actual cash on hand. It still is the difference between current assets and current liabilities, but it removes elements like short-term debts from liabilities.

How to Get a Working Capital Loan: Key Insights for Small Business Owners

What is considered good working capital?

Good working capital means having enough short-term assets to comfortably cover your upcoming bills, while still leaving room for flexibility. Many businesses aim for a positive net working capital balance and a current ratio above 1.

Read more from us